HCCI - Heritage-Crystal Clean: Value Out Of Waste

2023-04-25 08:16:22 ET

Summary

- HCCI stock is trading at the lower end of the last 10-year EV/EBITDA range.

- The discount is due to a potential bear thesis of HCCI oil business’s margins reverting to a single digit (pre-pandemic level).

- I believe the fear is overdue and margins should remain above pre-pandemic levels due to IMO 2020 regulation.

- The remaining business should fare well due to the stable waste disposal business and Patriot acquisition.

Heritage-Crystal Clean (HCCI) is currently trading at attractive valuations, primarily driven by investors' concerns about the potential reversion of margins in the Oil business to pre-pandemic levels, which were in the single-digit range. However, I believe that such fears are unfounded, and the segment is unlikely to witness such intense margin reversion due to the implementation of the International Maritime Organisation ((IMO)) 2020 regulation, which supports the segment's re-refining spreads. Furthermore, the Environment segment, which generates revenue from a more stable waste disposal segment, is expected to perform well in the short term, owing to the Patriot acquisition, and in the long term, due to the PFAS opportunity. I am optimistic that the market will soon realize the over-pessimism around HCCI stock price, and the stock will revert to its historical 10-15x EV/EBITDA multiple, compared to its current multiple of 7.36x.

Brief recap

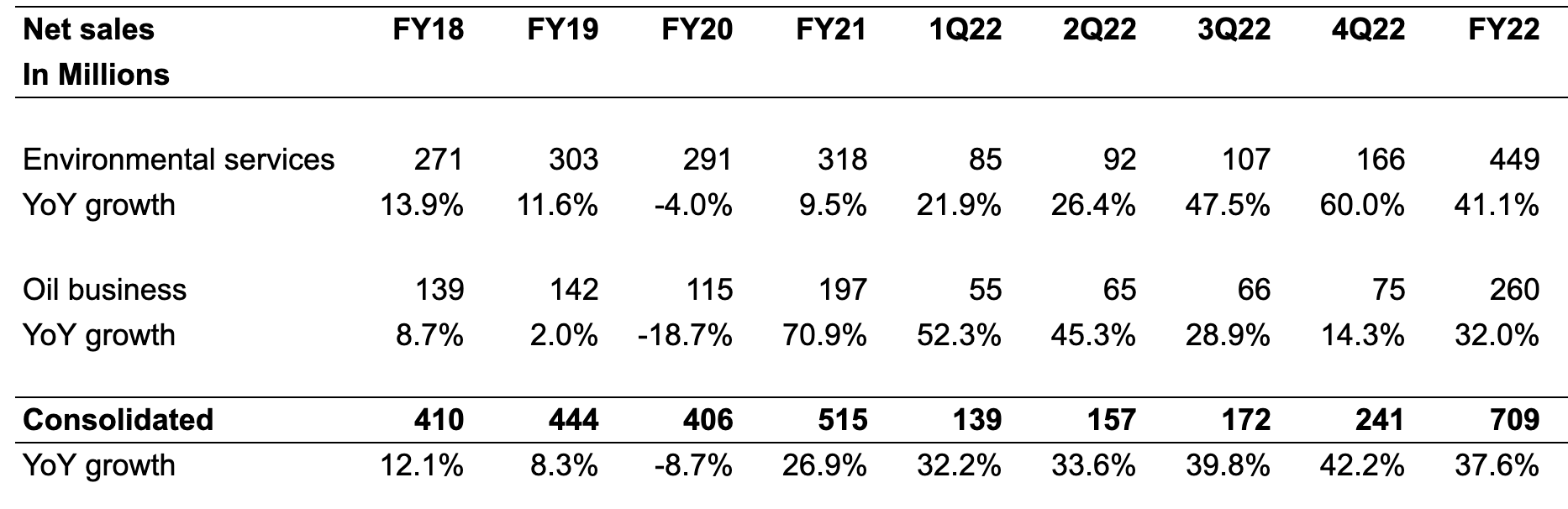

Post-pandemic HCCI witnessed strong performance with its topline growing at a CAGR of 20.2% which far exceeds the pre-pandemic growth rate CAGR of 6.7%. The impressive performance observed after the COVID-19 pandemic can be attributed to a surge in demand for waste disposal from various end markets and price hikes within the Environmental Services segment. Additionally, the oil business benefitted from wider base oil spreads, contributing to this strong performance.

While both segments performed well for most of FY22, the oil segment witnessed sequential normalization in demand during the latter half of the year, albeit up year over year. On the other hand, the Environmental Services segment’s YoY revenue growth accelerated in 4Q22 to 60% up YoY from 47.5% up YoY in 3Q22 primarily due to the Patriot acquisition in mid-3Q22.

HCCI's historical revenue growth

{kind=link}

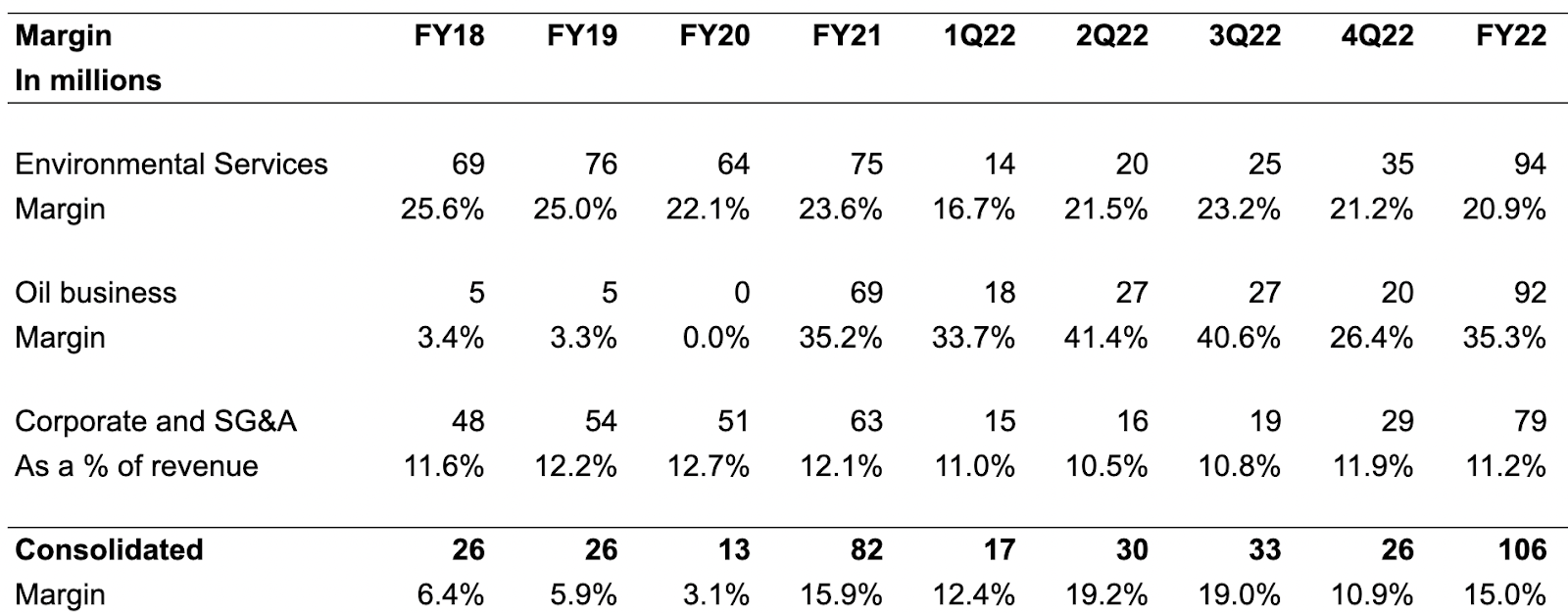

While topline numbers were good, profitability metrics were not so encouraging. Consolidated operating margins declined 350 bps YoY to 10.9% driven by a decline in margins in both segments. The Environment Services division experienced persistent inflationary pressure and faced challenges with the hazardous waste supply chain. Likewise, the Oil business segment observed a reduction in the base oil spread, which were the two key factors leading to the year-over-year decline in operating margins.

Historical Operating profit and margins

{kind=link}

Outlook

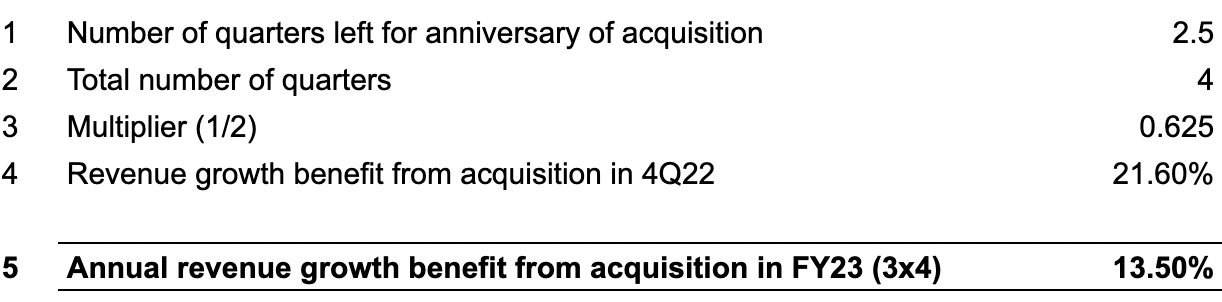

During FY22 HCCI witnessed strong revenue growth in all four quarters with revenue rising 30-40% in each quarter (as illustrated in the Revenue growth table). These whooping revenue growth figures in FY22 should pose pretty tough comparisons to beat in FY23. However, I still believe the company should post pretty good growth figures thanks to the recent Patriot Environment acquisition . HCCI acquired Patriot Environment in mid-3Q22. The acquisitions boosted consolidated revenue growth by 12.2% in 3Q22 and 21.6% in 4Q22. I believe HCCI’s topline should continue to benefit from the acquisition till 3Q23. The calculation for the full-year benefit from this acquisition on the FY23 topline is as follows.

{kind=link}

On the organic growth, the Environmental Services segment is expected to see favorable results thanks to price hikes implemented towards the end of the fourth quarter of 2022. Conversely, the Oil business segment should experience a headwind due to decreased base oil prices. Overall, I expect the topline to grow in the low double-digit for FY23 with a high double-digit in the first half of the year, gradually slowing down with the anniversary of the acquisition.

Looking at the profitability of the company, the oil business segment is anticipated to experience margin normalization after a considerable surge in FY22. Many investors are apprehensive about this segment, as before the pandemic, it generally had a single-digit operating margin. If the segment were to revert to those levels, it could prove detrimental to the overall consolidated operating margins as this segment contributes a sizable chunk to overall revenue. Although the operating margin for the oil business is expected to retrace back, I do not believe it will fall to pre-pandemic levels due to the improved re-refining spreads post-implementation of International Maritime ((IMO)) 2020 regulation.

The IMO 2020 regulation made it mandatory for the shipping industry to use bunker fuel with lower sulfur content (0.5%) than previously allowed (3.5%). Earlier, used/dirty motor oil was also used in the bunker fuel mix, which is the primary input for various used motor oil Re-refiners such as HCCI. After the implementation of IMO 2020, the demand for used/dirty motor oil from the shipping industry declined significantly, resulting in fewer competitors in the used motor oil market. This led to a better spread for the re-refining industry, coupled with higher recycled base oil prices, which resulted in significantly higher margins in the past couple of years. However, recycled base oil prices are expected to retrace back, which should lead to margin normalization. Nevertheless, the IMO 2020 regulation is still in place, supporting the spreads with lower input costs. Therefore, I do not believe the margins will fall to single-digit levels for the oil business segment.

On the other hand, the Environmental Services segment is likely to experience margin expansion due to easing inflation pressure and price hikes made in the latter part of 4Q22. Overall, I am expecting both segments to yield the mid-20s operating margins in FY23. For consolidated operating margins, I am anticipating 12% SG&A as a % of revenue, which is 86 bps higher than FY22 due to anticipated labor cost inflation. Ultimately, this should yield a consolidated operating margin of approximately 13% for FY23.

Long-term PFAS opportunity

Per and Polyfluroalkyl substances ((PFAS)) are a group of chemicals that are used to make fluoropolymer coatings and products that resist heat, oil, stains, and water. These chemicals are used in a variety of products such as clothing, adhesive, food packaging et cetera. PFAS contaminates drinking water through various means including effluent from industrial, manufacturing facilities, and landfills where PFAS leeches to the groundwater making it contaminated. Exposure to this PFAS-contaminated water can lead to various health issues including cancer.

Recently HCCI came up with an effective solution to treat contaminated PFAS water with the help of the 4never™ offering. Under these solutions, HCCI will deploy SAFF units on the site which will extract PFAS from contaminated water and create a PFAS hyper concentrate and transport it to HCCI’s facility where it will be destroyed using Battelle technology which will breakdown the PFAS compound’s molecular structure leaving the water, carbon dioxide and salt for disposal. These capabilities position HCCI to be a turnkey solution provider for PFAS disposal.

Although PFAS is not categorized as hazardous waste, demand for its disposal is still there due to the reluctance of municipal wastewater treatment plants for taking in PFAS-contaminated wastewater. Companies like Republic Services, Northrop Grumman, Marathon Et cetera are either using or in talks to use this service.

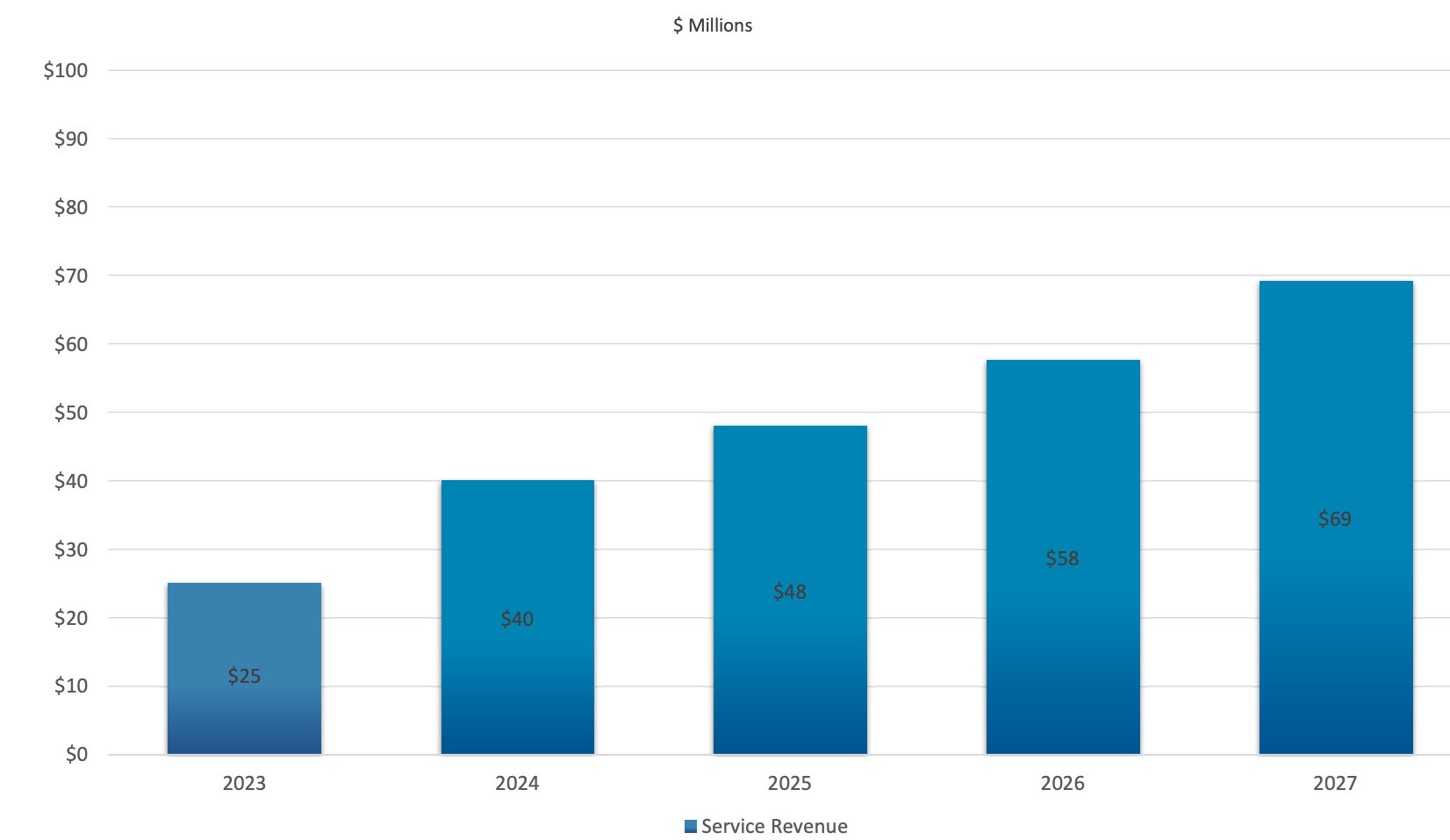

Management believes this business should generate ~$25 million in additional revenue in FY23 and is expected to grow subsequently (depicted in the graph below). Moreover, a Hazardous waste status should further bolster the benefits of this technology.

Forecasted incremental revenue from PFAS disposal services.

{kind=link}

Valuation

During the last 10 years, the company had traded at an EV/EBITDA ((TTM)) level of ~6.4x (at the lower end of the range) in 2016 and at ~20x (higher end of the range) during the end of 2019 and pre-2014. HCCI’s stock is currently trading at an EV/EBITDA ((TTM)) of 7.36x which is at the lower end of the range for the last 10-year history. The reason for HCCI to trade at such a low valuation is due to the anticipated reversion of the Oil business segment’s margin to pre-pandemic levels. Even though the margins fall to those levels which is the main thesis for bears to sell HCCI’s stock, its stock should trade at 10-15 EV/EBITDA ((TTM)) (pre-pandemic levels) which is much higher than current levels. In addition to this, the recent acquisition of Patriot Environment shifted the company’s revenue mix to a stable waste disposal business. Hence, I believe HCCI’s stock is undervalued at the current valuation and I would be buying at these levels.

{kind=link}

Risk

Although I expect base oil prices to normalize in the coming quarters, a significant decline likewise to 2020 can further depress spread which should lead to lower margins for the segment pressuring overall earnings.

Conclusion

I believe HCCI is providing a good opportunity due to pessimism among market participants for its volatile Oil business. Although the segment's earnings should decrease, it should remain above pre-pandemic levels. I believe the market should soon realize this in the coming few quarters as the company navigates through lower Base oil prices. Moreover, the stable Environmental segment should continue to support earning even if macroeconomic conditions worsen. Hence I am bullish on the stock.

For further details see:

Heritage-Crystal Clean: Value Out Of Waste