HGBL - Heritage Global: Time To Take Some Profits (Rating Downgrade)

2023-05-26 15:44:16 ET

Summary

- Heritage Global Inc. has roared to life in the last year, up 133%. But surging prices aren't alone reason enough to sell.

- Heritage Global has disclosed virtually nothing about one of their fastest growing lines of business, that of loaning money to buyers of charged-off loan portfolios. This makes analysis impossible.

- Heritage enjoyed one-time events last year that juiced EPS by $0.25. Those won't repeat this year.

- They also have a single customer with whom 77% of their notes receivable are held, and we know nothing about that customer. This implies considerable concentration risk.

- These factors combine to compel me to sell part of my Heritage Global Inc. position.

It's been over a year since I wrote about Heritage Global Inc. (HGBL). At that time I was of the opinion that in spite of considerable problems having to do with executive compensation and corporate governance, Heritage Global Inc. future financial results were going to be very good and the stock price was going to go up. The day that year-ago article was published, HGBL was trading for about $1.50. Now it is trading around $3.50. Not bad for one year.

My intent with this article is to determine whether or not HGBL is still worth holding, whether or not the pros outweigh the cons. (If you are new to HGBL I encourage you to read my other 4 articles on them in chronological order for context)

Key Indicators

I find Heritage Global Inc. unique among publicly traded companies in that the best indicator for future business results is all contained on the most recent balance sheet . There is little need to try and look at revenue trends and the like to gauge future demand. The best predictor for future results is there on the asset side of the balance sheet, where there are four metrics in particular that contain the entire HGBL business model: cash; notes receivable; equity method investments; and inventory. Let's break down each.

Cash: This is critical, as HGBL uses cash to buy surplus and used inventory (to include real estate, often in partnership with others) in their industrial assets division and then act as broker or principal in auctioning those stuffs off. In their financial assets division, HGBL has an online auction platform whereat they broker charged-off loan portfolios. HGBL also uses their cash to make loans to buyers of charged-off loan portfolios and then collect the interest payments. The more cash HGBL has, the more free money they have to pursue their lines of business.

Notes receivable: These are the outstanding loans they have made to buyers of distressed debt. The bigger the number here, the more they are getting in interest payments.

Equity Method Investments: HGBL often joins others in procuring particularly large industrial properties that they spruce up and then auction off. Equity method investments are the dollar amounts they have associated with these ventures.

Inventory: This is the machinery and equipment that HGBL buys used, re-furbishes if necessary, and then auctions.

That's really it. If these numbers are growing, then revenue growth will almost certainly follow. If these numbers are shrinking, revenue will definitely follow. It is straightforward. For the past 8 quarters, the total of the three revenue producing line items (notes receivable, equity method investments, and inventory) have consistently gone up. All three metrics are at or near all-time highs, and that by many millions:

{kind=link}

Taking this at face value is all extremely encouraging and bullish. However, I really want to dig particularly into the phenomenal explosion in notes receivable, which nearly doubled in value from just one quarter ago. Not the year ago comparable quarter, we are talking three months ago. And the quarter prior to that saw 300% growth. It is necessary to really drill down into this topic in order to surmise how bullish this is, and to do that we are going to have to provide a lot of background and context.

Bad Debt Purchasing

At least on an institutional level, the purchase and any subsequent re-sale of bad debt is a relatively nascent thing. The practice was born out of the savings and loan crisis that started in the 1980's. When 1/3 of all savings and loans associations in the U.S. went belly up, the government had to find buyers for all the "assets" of those failed institutions, which naturally included a proportion of non-performing loans. When the buyers looked at the portfolio's they had acquired and learned of the accounts in delinquency in the mix, a market was born where these loans in default could be sold off too other institutions, often collection agencies, for pennies on the dollar, and those agencies then employ their tactics to collect.

It was soon discovered that there was money to be made in this realm, and others flocked to take advantage. Even private investors could buy these packaged loans in default and then outsource the collection aspect to a collection agency. Or, an entity could buy a package of these loans, re-package them according to certain parameters (time in default, type of loan, etc.) and then re-sell them to others who might be interested.

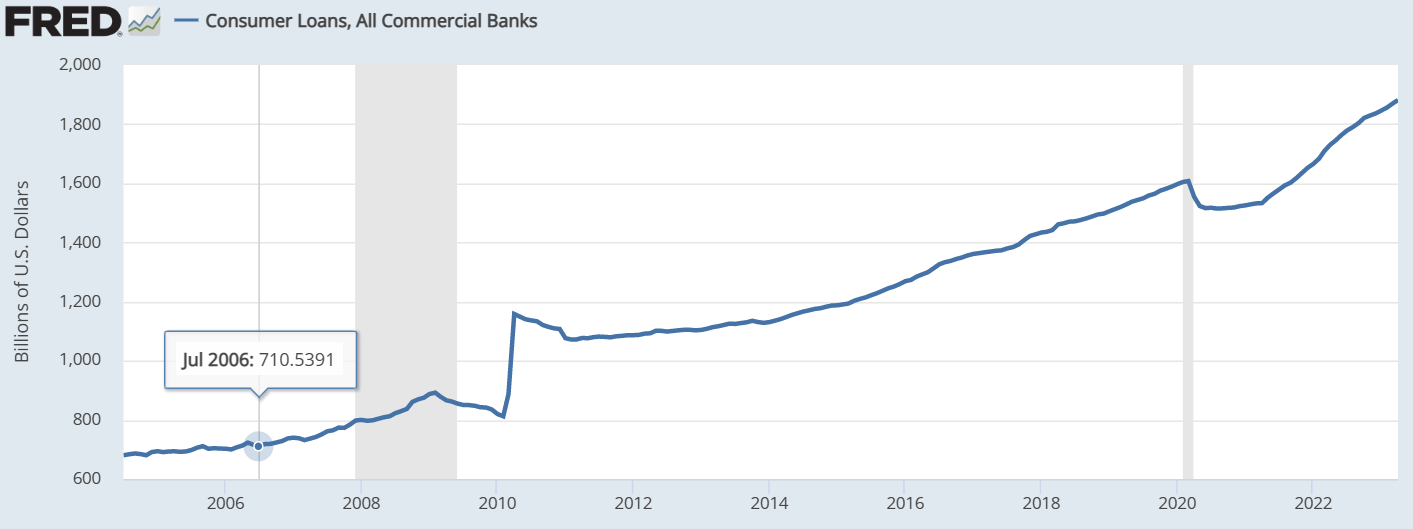

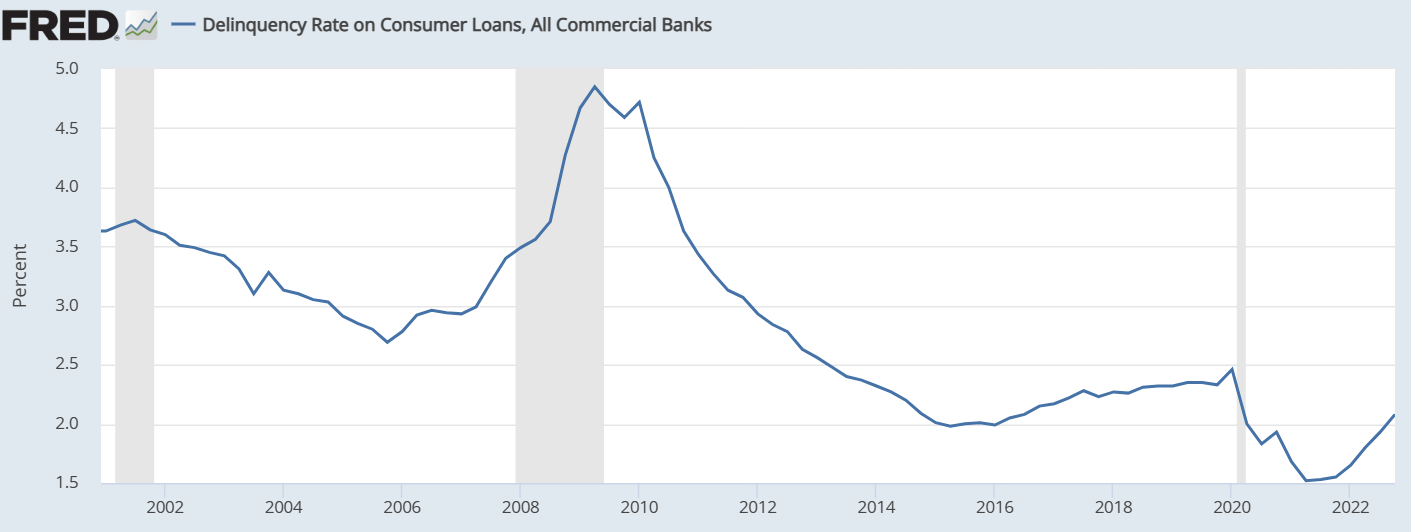

Enter HGBL, whose Heritage Global Capital division ((HGC)) is in the business of providing loans to those entities who want to acquire these packages of distressed loans. It is this division that has seen wild growth in a short time frame at the company. Whereas for years the outstanding investment in notes receivable fluctuated between $2 and $4 million, the past three quarters alone have rocketed from $2 million to $16 million currently. This is in part owing to the fact that consumer lending has surged lately, which is naturally followed by an increase in delinquencies:

{kind=link}

{kind=link}

As supply has become more available, more institutions are looking to invest and need capital to do so, which HGBL provides. This is all summarized in comments that HGBL management made in the last and several prior conference calls:

As consumer spending continues to increase, defaults naturally follow, to some extent. And as defaults follow, then charge-offs follow. So right now, we're looking at a great last year and a very pleasing multiyear future.

I am sure most of that is true. But to go from $2 million to $16 million in just 9 months seems a bit quick. For a bit of speculation on my part, I wonder if HGBL is so eager to chase this opportunity that they relaxed their standards for who they would loan to.

In any case, an exploration of some of the finer aspects of the larger bad debt market is warranted. And for me, an understanding of the following makes me much less enthusiastic about the stellar numbers HGBL has posted, at least as it pertains to their loan segment. To be clear, HGBL doesn't have direct exposure to bad debt. They are once removed from the situation, as a provider of capital to others who buy and then own the debt. Nonetheless, understanding what affects their debtors is critical to comprehending the health of their portfolio.

First, transparency is lacking as it relates to the documentation and detail that buyers of charged-off loans receive about each loan when they buy a package of them. This unfortunate matter exists logically. When loans go into default, it is often accompanied by a near elimination of communication between creditor and debtor. If something mortal happened to the debtor, there is no one to communicate with. If the debtor finds themselves unable or unwilling to pay back the loan, it is common for them to ghost the creditor in hopes of escaping the required payment.

This matter has been detailed in a study done by The Federal Trade Commission wherein they analyzed data gathered from the 9 largest buyers of debt in the USA from the years 2006 through 2009. The study is entitled, "The Structure and Practices of the Debt Buying Industry," to be referred to repeatedly throughout the rest of this article. Here is a relevant quote for the topic at hand regarding the sparse information available to buyers of debt:

When debt buyers purchase debt portfolios, they receive an electronic database or spreadsheet (or access to such a database) summarizing the debts included in the portfolio. These files often include only a name, last known address, the amount allegedly owed, the charge-off date, and the date and amount of the last payment. Notably, very few portfolios include documentation for the debts being sold...... (the) FTC estimated that debt buyers received documentation for as little as six percent of the accounts at the time of purchase.

Further, charged-off debts are often sold “as is,” without any representations, warranties, or guarantees as to the accuracy of the amounts claimed to be owed or the collectability of the debts.

The study also found that subsequent re-packaging and sales of the debts exacerbated the same problem, leading to a decrease in collectability. HGBL does not disclose and may not even have information regarding how many times the loans that their borrowers bought have been re-sold.

Second, another reason why excitement should be tempered regarding this explosion in investments is due to concentration risk. While details are sparse, we know this: HGBL has a single customer with whom 77% of the notes receivable investments (to include equity method investments) is concentrated. Without a doubt, in spite of this being the first time it is disclosed, this concentration risk has existed for at least a few quarters, unless last quarter saw such tremendous turnover that many millions went out to be replaced by many millions in from this concentrated patron. The 10k only has this to say:

Due to varied timing between loan origination and transfer of notes to senior partners, the Company may, from time to time, have concentration risk as a result. The Company does not intend to hold highly concentrated balances due from one borrower as part of its long-term strategy but may, in the short term, have concentration risk on its path to an established and diversified portfolio.

The Company does not evaluate concentration risk solely based on balance due from specific borrowers, but also considers the number of portfolio purchases, type of charged off accounts within the underlying portfolio, and the seller of the portfolio when determining the overall risk. Of the balance due from one borrower of $22.4 million, there are 20 distinct portfolio purchases and loan agreements, the underlying portfolio of accounts are diversified throughout FinTech, installment loans and credit card accounts; and further diversified amongst four separate sellers of these charged off portfolios.

The Company mitigates this concentration risk as follows. The Company requires, and monitors, security from each borrower consisting of their charged off and nonperforming receivable portfolios. The Company engages in a due diligence process that leverages its valuation expertise. In the event of default, the Company is entitled to call the unpaid interest and principal balances, receive all collections directly, and recover its investment by acquiring and liquidating the underlying charged off or nonperforming receivable portfolio through its Brokerage segment.

I take issue with the entirety of this statement. Again, those three paragraphs are the totality of what HGBL has to say about their concentration risk, and this is unfortunately the first-time investors have been made aware of it. Their attempt to minimize the problem consists of three points: i) The concentration is temporary, ii) the concentration of diversified, and iii) we have recourse if something goes south. But none of these arguments hold up under scrutiny.

i) Even if HGBL stages a repeat of last quarter and is able to grow their notes receivables balance by $8 million, all spread out among new customers, they will still have a 60% exposure to the one customer. Then if they do that again the quarter after that they will still have 50% exposure. That is still super high. Temporary is a relative term, and any duration of time where one customer accounts for such a huge portion of their investments isn't something to be shrugged at.

ii) As it relates to diversification, the fact that the concentrated customer used their loan from HGBL to buy a relatively diverse portfolio does not change the fact that they entire portfolio is junk! And I don't say junk pejoratively, it is truly junk status, as is the parlance in the industry. I stand corrected: the portfolio is lower than junk. Junk loans or bonds are below investment grade that are at high risk of default. The loans that HGBL debtors own are already passed default and into charged-off status, or beyond 150 days overdue. So the fact that these charged-off loans are diversified means nothing.

Explained another way, imagine going to the person in charge of your retirement account to check in on your portfolio and you find out that they have invested your money into a bunch of companies who are and have been burning cash, with low likelihood of ever turning a profit. And in response to your outrage your investment advisor attempts to belay your concerns by explaining how all these cash burning, profitless companies are diversified across various industries, so it's fine. Would that help you feel better? Me neither.

iii) As for their third argument, that they have immediate recourse if a loan goes south, what good is it going to do to demand immediate repayment of the entire loan if the debtor misses a payment when the reason they likely missed the payment in the first place is because they have no money available! If they don't have money for a payment they aren't going to have money to pay back the loan that you call in the event of default. Then, HGBL will be left with a loan in default that was used to purchase a bunch of defaulted loans. Not a great position to be in.

Third, recoverability rates for charged-off loans are predictably low , 12% at the median and 17% at the average. Naturally, buyers of debt always demand and always get these loans for pennies on the dollar, to the tune of 4.5 cents per dollar of original value, on average. That way, even if they only recover a fraction of the loans they can still make a profit. But the point remains, there is great risk here, particularly because not all collection agencies are created equal. As it relates to a potential investment in HGBL, we have no idea and no data about ANY of the entities to whom HGBL makes loans and their success rates in making recoveries, let alone the single entity with whom they are 77% concentrated.

What if this entity happens to be really bad at collecting? A layer of complexity deeper has to do with the number and amount of government regulations in this arena. The FTC has increasingly laid down the law in recent years that dictates what tactics collection agencies can use and how often. What if the HGBL customer that makes up 77% of the receivables gets on the wrong side of the law for bad practices?

Fourth, and related to the above information about the amount and accuracy of the data debt buyers get concerning each loan they have, the study beforementioned also found that 3.2% of these loans end up being disputed by the people who allegedly owe the money:

Consumers disputed 3.2% of debts that buyers attempted to collect themselves. There was no statistically significant relationship between the likelihood of a dispute and a debt’s age, face value, or whether it had been purchased from an original creditor or reseller. Although the 3.2% dispute rate may understate the extent of information problems in purchased debt, even a 3.2% dispute rate, if applied to the entire debt buying industry, indicates that each year buyers sought to collect about one million debts that consumers asserted they did not owe.

Fifth, of utmost importance is the amount of time on average that a loan book has been in default. The longer the default has lasted, the harder it is to make a recovery. Success rates plummet after just a few months. An article from the National Service Bureau says:

Across the industry, the likelihood of write-off increases by more than 1% with every passing week after the past-due date. After just seven months at past-due status, the average account will have a collectability rate of 50%.

Simply put, accounts that are past due for longer than 6 months are recoverable in half of total cases. That likelihood drops to only about 25% after 12 months. Clearly, speed is key to success in debt collections.

At very least, HGBL should be sharing with us the average time in default the portfolios are of the people to whom they have made loans for those portfolios.

In summary to this section, the problem for potential investors of HGBL is that the company has shared so little data with us that there is no way for us to surmise even a modicum of insight into the health of the businesses that they are making loans to or the details of the underlying portfolio. It makes analysis impossible. And with their loan division quickly becoming a larger segment, it become all the more important for us to have relevant information.

It must be noted to that as of the last quarter, HGBL has recorded a big fat $0 under allowance for potential losses. They don't think that a single cent of their loans are in danger. This seems very suspect.

Now, please don't misunderstand me. I am not saying that we should all be bearish on HGBL because of the foregoing. What I am saying is that HGBL has made it impossible for us to analyze the situation so that we can make a fair assessment of the bullishness or bearishness of it all. Potential investors need to weigh this matter carefully, and analysts should apply appropriate pressure on management to both procure and then transparently disclose A LOT more detail about who their money is going to and what those underlying portfolios look like.

Specialty Lending

HGBL refers to their activity making loans to buyers of charged-off portfolios as "specialty lending." Now typically, companies who make loans disclose in considerable detail the duration of the loans they have made and the interest rates associated with them. This is vital information needed to assess the health of the enterprise, the competence of management, and for analysts to model future results. With HGBL we get none of that. No disclosure of duration or interest rates. This all just adds to the confusion and problems stated above about how little we know about what HGBL is doing in their specialty lending segment.

Valuation

Heritage Global Inc. had GAAP EPS of $0.08 last quarter. Using this as a baseline, we can put together a simple best- and worst-case scenario for future business results that, when combined with a reasonable multiple, will give us a picture into what kind of stock price we should buy or sell into.

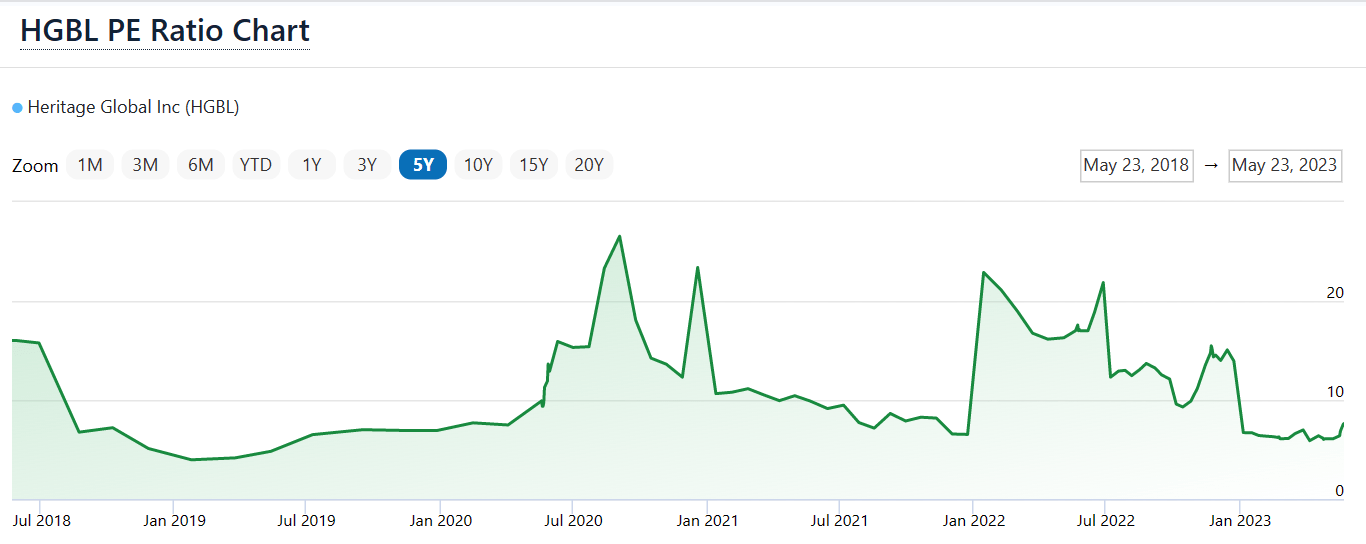

First, we need to look at the historic multiple that the market has given the company and use that to inform our assumption about what multiple they should be assigned now. Unfortunately, their P/E ratio jumps around a lot, very much a consequence of their lumpy business model:

{kind=link}

Suffice it to say that HGBL's trailing P/E of ~7 is below the 5-year average of 11. Their TTM EPS is $0.47. Reverting to the mean would result in a stock price of $5.17. As for forward earnings, I am expecting 2023 EPS of around $0.35. The considerable decline would be owing to two items that happened last year that won't happen this year, a large property sale as part of a joint venture and an income tax benefit. These items made up $0.25 worth of EPS that won't be there in 2023, partially made up for by improved numbers from the financial assets side. $0.35 of EPS at an 11 multiple would mean a stock price of ~$3.85. We are approaching that level.

In conjunction with the cloudy situation that formed the bulk of this article, I wouldn't feel comfortable marking HBGL as an attractive investment at this time on a valuation basis. Yes, they are trading below the fair value I calculated, but that fair value is subject to quick change as there are so many variables in play.

Miscellanea

A few more significant items and we will wrap this up. First, the Heritage Global Inc. cash balance is a little bit misleading. While it currently sits at $15,733,000, more than half of that does not really belong to them. The line item "payables to sellers" on the liability side of the balance sheet includes amounts that they are holding only briefly, included in the cash line item, as part of the settlement logistics that occurs in their brokerage business. They collect money from buyers and transfer that to sellers after the buyer confirms receipt of the goods. So it's all a timing issue, and the "payables to sellers" line has an outstanding balance of $8,333,000. So HGBL really only has $7,400,000 in cash.

They also have a fat chunk of third-party debt falling due in June, in the amount of $4.5 million. So take that $7.4 million down to $2.9 million. In other words, the cash available to them to grow their business and seize opportunities on the specialty lending side is actually extremely limited without them tapping into outside capital, which of course has a price. Don't expect another $8 million increase in notes receivable.

The final thing that I am compelled to say is that, in spite of what everyone seems to think and opine, HGBL is NOT a countercyclical company. Part of many folks investment thesis, it would seem, is that an investment in HGBL is a hedge against a recession. This is due to comments management has made in the past about how their business will do well in recessionary environments. Their substantiation of these claims revolves around how their industrial side will allegedly do well because of recessions putting people out of business and HGBL will profit from those businesses needing to liquidate assets. The argument on their financial division is much the same. Recessions will cause people to default on loans and thereby give HGBL a supply of distressed assets to broker. While this might make sense on its face, I don't think it holds up well when critically considered, and every time management makes comments in these regards it is NEVER backed up with data.

Heritage Global Inc. in their present form has only been through one recession, and that was the pandemic. While that particular recession was peculiar for a lot of reasons, it's the only one we can pull data from. As it turns out, Heritage Global Inc. didn't do well during that recession. Their metrics dipped just like everyone else's:

As can be seen, no flurry of activity occurred in 2020 that saw their numbers jump. But this stands to reason. What, after all, is a hallmark of recessions? A general decline in economic activity born of higher unemployment, lower consumer spending, and a dip in asset values.

Now consider those recessionary hallmarks in context of what HGBL does. On the industrial assets side, they broker industrial assets and also act as principal in these transactions. But companies don't sell off machinery during recessions, they make what they have last longer because they don't have the funds to buy new machinery that would replace the old. Furthermore, selling off assets during recessionary times is ill advised because they wouldn't be able to fetch a high price for them if they can find a buyer at all. Again, recessions are marked by a decrease in transactions generally. Less buying and selling results in a huge hit to HGBL's bread and butter as a broker.

On the flip side, during economic expansions, businesses are keen to sell off old equipment to invest in new, and all that because business is good and they can afford it. Particularly on the real estate side, which has generated considerable windfalls for HGBL historically, those transactions are simply more likely to occur during healthy economic times. The seller wants as a high a price as possible and the buyer will be more confident in their ability to afford it.

The same is true on the financial side. More transactions and more spend are all a tailwind for what HGBL does. They have even said as much! Here is the quote I already shared earlier:

.... we're seeing increased consumer spending in all of the segments we operate in. As consumer spending continues to increase, defaults naturally follow, to some extent. And as defaults follow, then charge-offs follow. So right now, we're looking at a great last year and a very pleasing multiyear future.

So which is it? Is it a decrease in economic activity during hard times that will be a boon to the business, or increased activity during good times? There is a bit of incongruence in what management is saying.

I lean much more towards to good economic times being the best for the business. Remember the graphs from the beginning showing an obvious correlation between consumer spending and charge-offs? One naturally follows the other. This makes sense anecdotally and the data is plain to see. I would argue that recessions are bad for HGBL just like they are bad for everyone else, as decreased spend and fewer transaction inhibits multiple lines of business for them. But we might have to wait for a "normal" recession to find out.

Many will disagree with me and point to the stimulus packages the government sent out to businesses and individuals during the pandemic recession that made it so that perhaps HGBL didn't get the advantages they claim would come during hard times. And that may be true. But for me, building an investment thesis around HGBL that revolves around the counter-cyclical argument just doesn't have any real evidence backing it up.

Conclusion

Heritage Global Inc. stock has soared over the past year. Anyone who bought around the time my last article was published is enjoying a 133% annual gain. I believe every penny of that increase is justified by the financials. The market got it right.

That being the case, the risk reward profile for Heritage Global Inc. stock has tilted considerably, and not just because the stock price has gone up, but because my old concerns remain about exuberant executive compensation that will make it impossible for them to have operating leverage AND because I have uncovered the concerns related to the specialty lending line of business. I anticipate slower growth from here, if growth continues at all. If consumer lending levels out and charged-off loan portfolio's follow suite, HGBL is back to their old selves: lumpy results driven largely by timing issues related to large asset sales.

I have decided to sell part of my position in Heritage Global Inc. I have cashed in on my lots that were at higher prices. This lowers my average cost basis and reduces the tax bite that would have been incurred from selling lower priced lots. I would encourage others to consider the same approach. I will hang on to my smaller position. Even though it wasn't the premise of this article, there is evidence pointing to this being a positive turning point for HGBL where finally what they have been trying to build for years is finding its critical mass. Right-sizing my Heritage Global Inc. position was the best course of action for me, insulating me from potential downside while keeping available the opportunity for further gains.

For further details see:

Heritage Global: Time To Take Some Profits (Rating Downgrade)