PPRUF - Hermès: Getting Closer To Buy Territory

2023-10-09 14:07:48 ET

Summary

- Hermès has reported excellent results for the first half of FY 2023 while the stock has been on a decline since July.

- The selloff took place throughout the whole luxury sector with Hermès showing the least volatility.

- The valuation level has improved compared to my prior article in April.

- I upgrade my prior "sell" rating to "hold" and may be inclined to give a "buy" rating if the stock drops a bit further and closer to fair value.

Author's note: Since Hermès is reporting in EUR, I will refer to the EUR numbers and only add the USD equivalent for per-share and valuation purposes.

Introduction

This will be a short update article to my two prior articles on Hermès ( HESAY ) ( HESAF ). I covered Hermès in my initial article on June 12, 2022 called " Hermès: Margin Headwinds Ahead " and in an update from April 3, 2023 called " Hermes: Reiterating My Sell Rating Despite Being Wrong Regarding My Initial Thesis ".

My initial article, where I assigned a "sell" rating, was a bad call as described in the update article. In the update from April 3, 2023, I reiterated my "sell" rating because despite being wrong initially, the sky-high valuation made Hermès an unattractive investment at that time. Here is how the stock performed since that update:

Performance since the prior article (Seeking Alpha)

Hermès underperformed relative to the S&P 500. In this article, I will address Hermès' recent results and why the stock might have declined. I will also give an update on the valuation and finish as I always do, addressing risks and giving a conclusion.

Recent Results

Hermès releases results on a half-year basis. The last available earnings numbers for the first half of FY2023 were released on July 28, 2023. Here is a summary of the YoY growth for the most relevant metrics (in € million):

| First Half 2022 |

| First Half 2023 |

| YoY% |

| Revenue |

| 5,475 |

| 6,698 |

| 22.3 |

| EBIT |

| 2,304 |

| 2,947 |

| 27.9 |

| Net Income |

| 1,641 |

| 2,226 |

| 35.6 |

| Free Cash Flow |

| 1,523 |

| 1,827 |

| 20.0 |

Hermès reported excellent YoY results again.

Here is the comparison of the trailing twelve months ('TTM') numbers compared to the time of my last article (in € million):

| FY2022 |

| TTM First Half 2023 |

| YoY% |

| Revenue |

| 11,602 |

| 12,825 |

| 10.5 |

| EBIT |

| 4,697 |

| 5,340 |

| 13.7 |

| Net Income |

| 3,367 |

| 3,952 |

| 17.4 |

| Free Cash Flow |

| 3,611 |

| 3,915 |

| 8.4 |

Hermès' momentum doesn't seem to slow down at all. We will also see this later on when looking at the margin development. Before that, here are two charts regarding revenue composition:

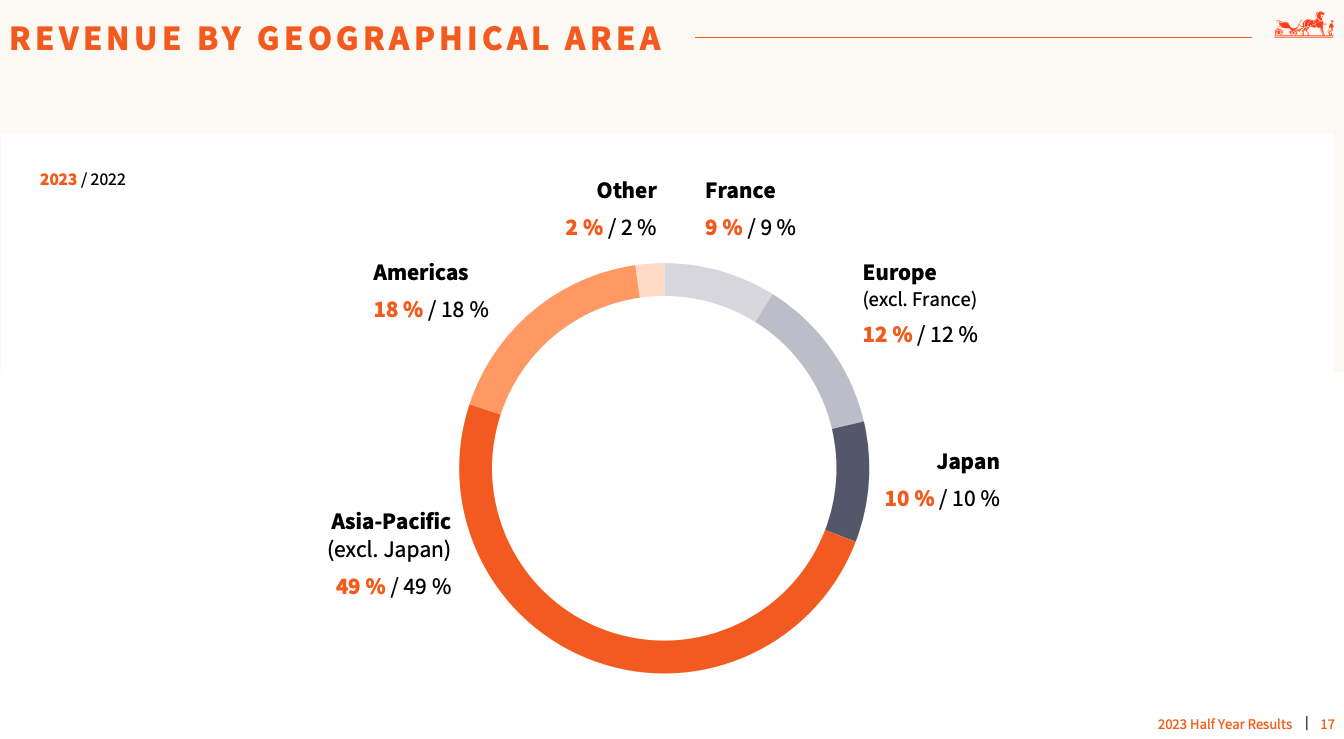

Revenue by geographical area (Hermès IR)

{kind=link}

Hermès generates close to 50% of revenue from Asia. And that is already excluding Japan, so probably mainly China, Hong Kong and Singapore. This large revenue concentration is a risk factor investors should keep in mind. In the scenario of a major decoupling between "the West" and China, Hermès revenues might come under pressure.

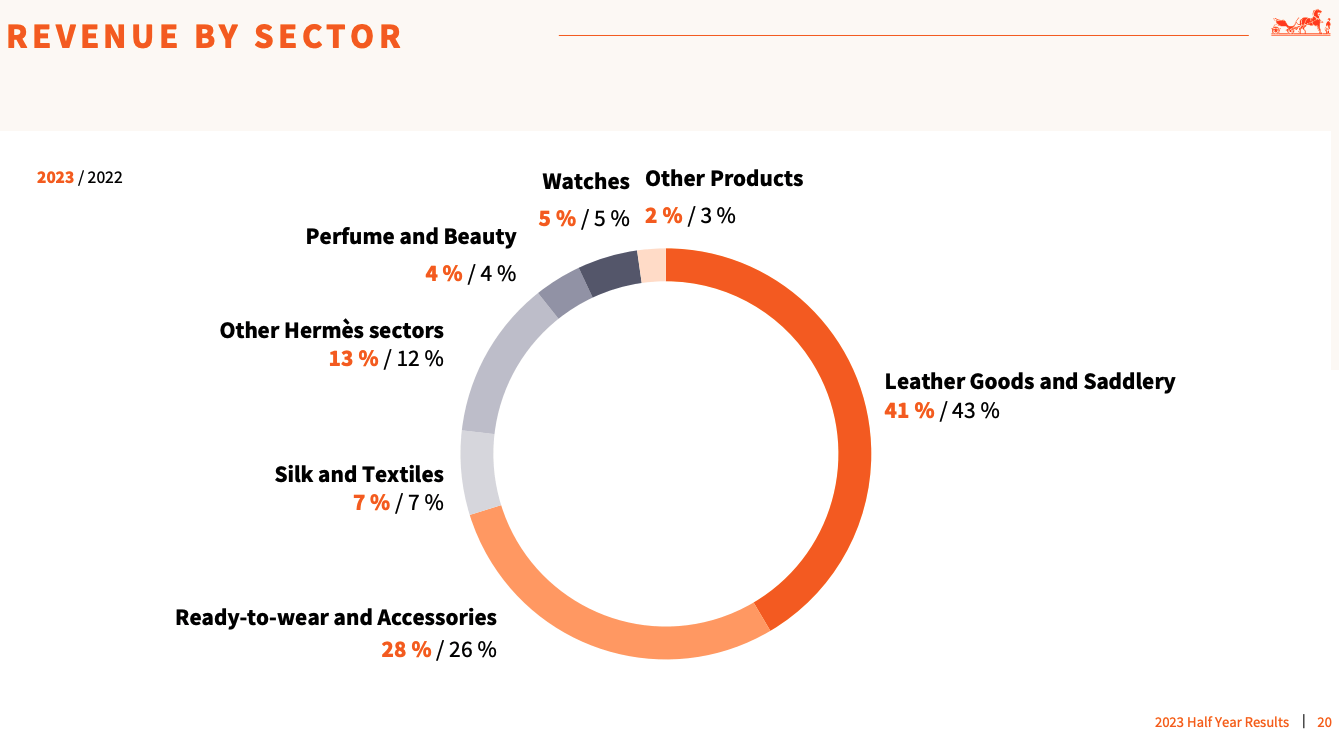

{kind=link}

Here we can see that Hermès mainly operates in clothing and accessories. Leather Goods and Saddlery are mainly Handbags like the Birkin and Kelly Bags which I would count as Accessories as well. Notably, the "Perfume and Beauty" segment is pretty small and there is no "Wines and Spirits" segment contrary to competitor LVMH ( LVMUY ).

Margins

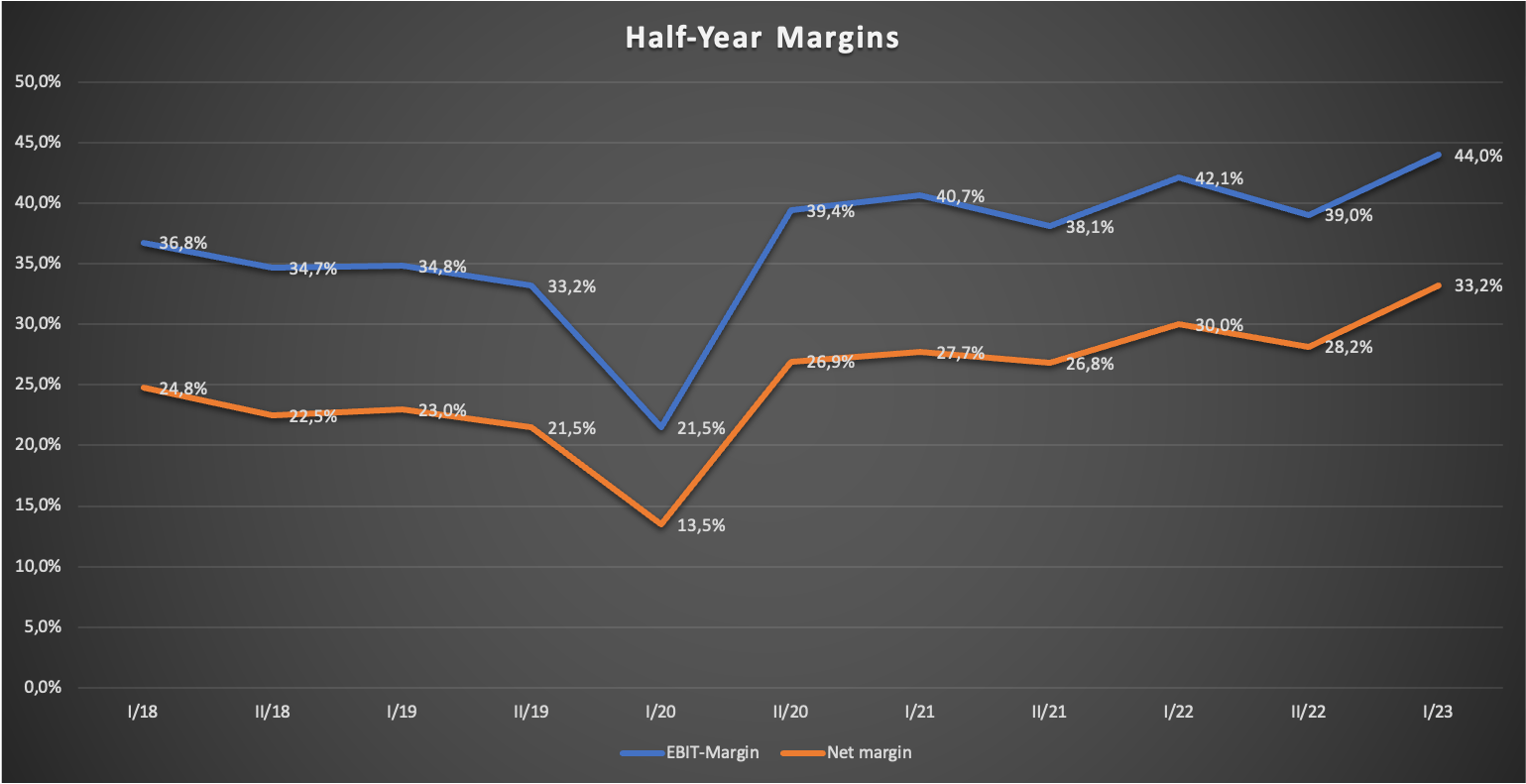

The margin development was a big part of my initial two articles so I will address that here as well. I will start with the updated chart regarding the development of EBIT and net margins:

Margin Development (Company Reports - compiled by Author)

{kind=link}

In my prior article, I assumed that Hermès would be facing margin pressure on the gross margin level while negating these by further expanding operating leverage (declining OPEX as % of sales). In the above chart, we can see that margins expanded even further in the first half of FY2023. To dig deeper, here is my updated overview of the costs as % of sales on a half-year basis since 2018:

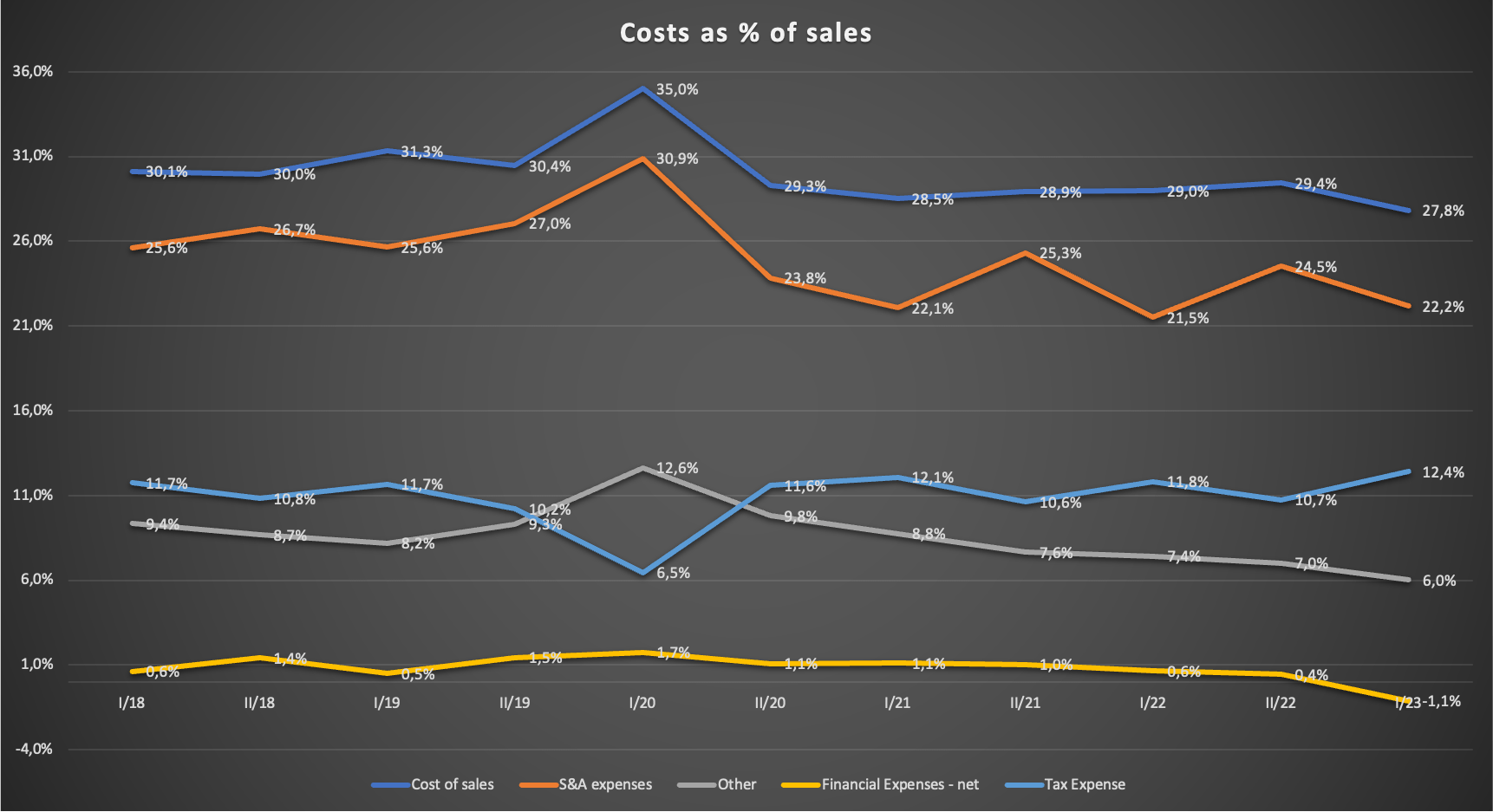

Costs as % of sales (Company Reports - compiled by Author)

{kind=link}

Here we can see where the margin improvement came from. The gross margin improved because the costs of sales as a percentage of revenue reached a new low of 27.8% (-120 basis points YoY). Meanwhile, S&A expenses as a percentage of revenue only increased 70 basis points YoY. Tax Expenses, Other and financial expenses declined by 250 basis points, mainly driven by lower depreciation/amortization expenses (-140 basis points YoY) and financial income of €75 million (-170 basis points YoY - compared to financial expenses of €35 million in the prior six-month period).

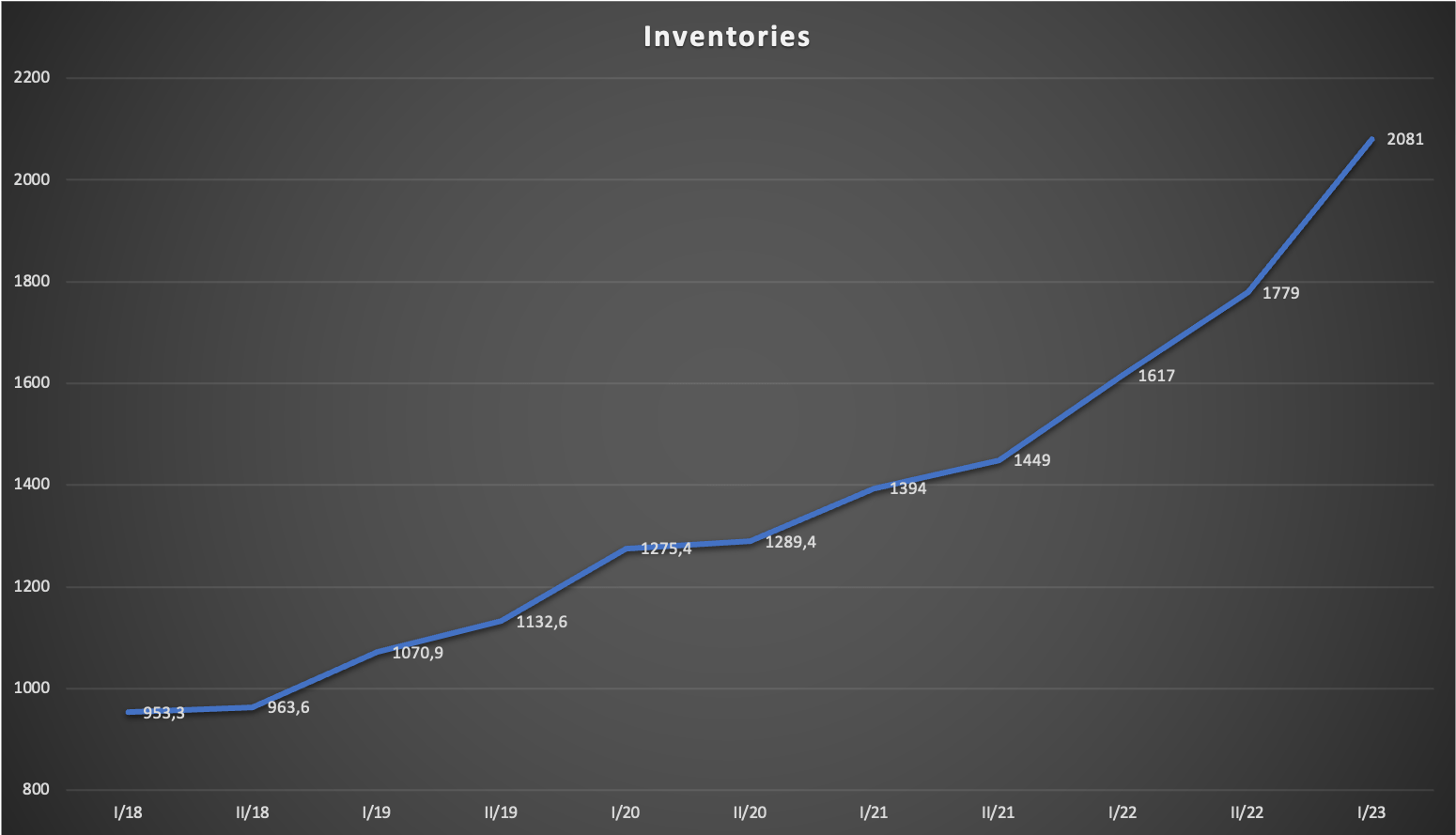

It will be interesting to see how the gross margin development will play out over the next few years. While I always say that I think Hermès should start facing some gross margin pressure soon (costs of sales as a percentage of sales hovered around 31% until 2020), the inventory development indicates that this should not be the case:

Inventories since 2018 (Company reports - compiled by Author)

{kind=link}

Here we can see a steady increase in inventories (in € million). Declining gross margins usually come from an oversupply of inventory that is sold at discounted prices, resulting in higher revenue, lower margins and declining inventory. If we look at the ratio of revenue to inventory, it doesn't look extraordinary. With FY2018 revenue of €5,966 million and €963.6 million inventory as of December 31, 2018, the revenue to inventory ratio came in at 6.19 times. For the TTM, the same number comes in at 6.16.

Explanations for this could be that (a) Hermès is doing an incredibly good job of handling working capital/inventory and (b) Hermès just doesn't sell at discounted prices (which is 100% true and one of the main reasons why I think that Hermès is one the best companies I know).

To be honest, I don't really know what to do with all this information. I somehow feel that there should still be gross margin pressure ahead, but even then I think that further operating leverage should be able to negate nearly all of it. On the other hand, inventory development gives me no reason to expect declining gross margins. As I will keep covering Hermès, I will watch margin development closely over the next earnings releases. I think it is one of the main things to look out for in the future.

Some thoughts on YTD Performance

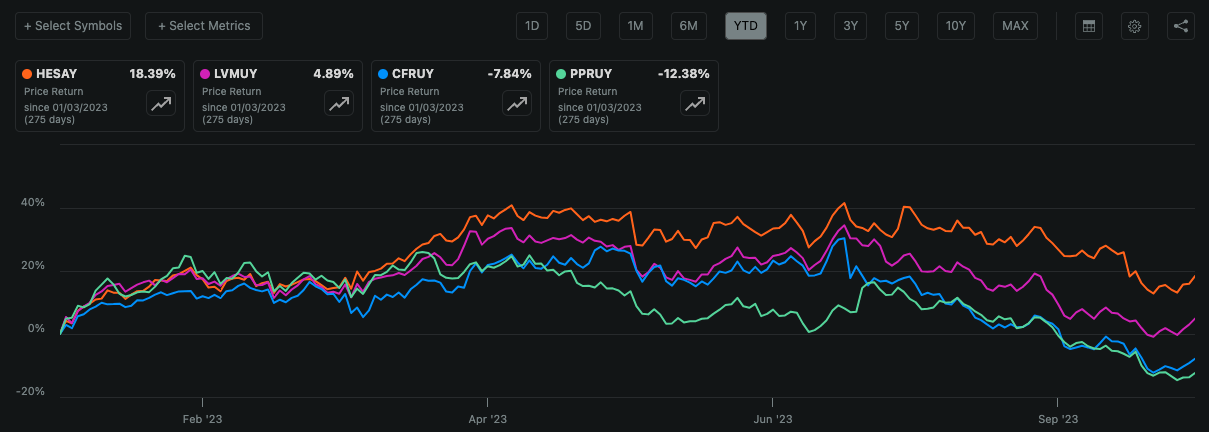

Luxury retail stocks had a turbulent year so far, as can be seen in the following screenshot from Seeking Alpha charting comparing the YTD performance of Hermès to LVMH, Richemont ( CFRUY ) and Kering ( PPRUY ):

YTD Performance vs. Peer Group (Seeking Alpha)

{kind=link}

I highlighted in my initial article why Hermès is the absolute leader in the luxury goods space. The performance this year in comparison to the peer group shows that once again. After peaking on July 14, 2023 (except Kering), the luxury sector as a whole declined sharply with Hermès seeing the least volatility.

The main differentiation for Hermès compared to other luxury retailers is that Hermès doesn't target a wider customer base like Kering with Gucci or LVMH with Louis Vuitton. While those two brands are still expensive, I wouldn't consider them high-end luxury brands because they are also affordable to average or upper-class customers. The market seems to price in that a pullback in overall consumer spending will hit the peers harder than Hermès because the customer base is more prone to cut back spending on luxury goods.

Another reason for the YTD outperformance of Hermès might be that it doesn't operate in markets that were severely hit over the last few months. Hermès doesn't operate in wines and spirits while main peer LVMH does. LVMH's wines and spirits division was the only segment that reported organic negative growth for the first half of FY2023, with revenue declining by 3% YoY. Hermès' perfume and beauty segment is also small at only 4% of revenue. With Estee Lauder ( EL ), a leader in this space, declining close to 43% YTD because of really bad results, we can already see that it was positive to not operate in this sector (for this year at least).

Valuation Update

Note: The USD equivalents refer to one ADR. 10 ADR = 1 share on the Euronext Paris.

There are 104,697,914 shares outstanding as of the latest report for the first half of 2023. With the stock currently trading at €1,756.40 (ADR: $185.8) on the Paris Stock Exchange, the market capitalization amounts to €183.9 billion ($194.5 billion). After deducting the net cash position of €7.4 billion ($7.8 billion), the Enterprise Value (cash-neutral valuation) stands at €176.5 billion ($186.7 billion). With a TTM net income of €3,952 million and Free Cash Flow of €3,915 million, Hermès currently trades at a PE of 44.6 and an FCF yield of 2.22%. The valuation is still very high.

What kind of growth rates would Hermès need to deliver in the future to justify this kind of valuation? We can come close to an answer to this question by performing a reverse DCF calculation. Earnings per share for the TTM come in at €37.75 (ADR: $3.99). Hermès long-term cash conversion rate hovered around 105%, so normalized FCF should be around €39.64 (€37.75 x 105%) or $4.19 per ADR. Assuming a 10% discount rate and 6% growth into perpetuity (as I always assume for very high-quality businesses), the growth rate over the next decade would need to be around 12.4%, as can be seen in the following screenshot:

DCF calculation (moneychimp.com)

Hermès grew sales with a CAGR of 12.8% from FY2012 to FY2022, nearly in line with what seems to be priced in at the moment. In conclusion, I think Hermès approaches or already reached fair value, resulting in a rating upgrade from my prior "sell" to "hold".

Hermès also seems to be close to fairly valued regarding historic multiples, but it isn't quite there yet. The chart below shows Hermès' PE ratio over the past decade and the average throughout this timeframe.

If we factor out the outliers throughout the pandemic, the average PE ratio might be a bit above 40, indicating that the stock might have some more downside until it reaches the valuation levels we have seen in the past.

Risks

As of right now, I can only see two major risks: (1) The large China exposure and (2) the possibility of margin headwinds on the gross margin level.

The first one is, in my opinion, mainly a geopolitical risk. We have already seen companies pulling out of or being boycotted by Russia as the Ukraine conflict began. The tension between China and Taiwan might bring a similar scenario some years from now regarding China. As the Chinese market is very important for Hermès, this would be a very hard hit for the company. It is impossible to say how likely this scenario is, but investors should keep it in mind and check the overall China exposure of their portfolios.

Regarding the second risk, I outlined some of my thoughts earlier in this article. The gross margin development will be one of the most important metrics to look out for in the upcoming earnings reports. A reversal to the margin levels in the past might pose a headwind for the company, especially since Hermès is a company that can't and shouldn't grow revenue in the double-digit percentage range over a longer period in my opinion. If it did, it would have to be the result of volume and price increases. Large volume increases would cause the Hermès brand to lose exclusivity which is the most important asset the company has.

Conclusion

Hermès reported excellent results for the first half of FY2023. With the share price declining over the past couple of months, Hermès seems to approach fair value, but it isn't quite there yet.

I am kind of torn about my rating for Hermès. I don't think that it is a "buy" right now because there might be some more downside ahead. On the other hand, I think that it might be the right time to initiate a really small position for investors who have been watching the company for a long time trying to find a window to start a position. This is what I did recently as I started a tiny position a bit above €1,700 (ADR: $179.8) just to have an even closer view of the stock. Should it drop a bit further, I will buy more and slowly build a full position. If it rises, I won't complain.

After thinking about it for quite some time, I ultimately decided to upgrade my rating on Hermès from "sell" to "hold". I might upgrade it to "buy" if it drops a bit further, maybe below the €1,600 (ADR: $169.2) mark.

For further details see:

Hermès: Getting Closer To Buy Territory