HESAF - Hermes: Look After It For The Next Generation

2023-11-10 03:09:57 ET

Summary

- Hermès continues to lead the luxury industry by consistently delivering impressive results despite growing industry concerns.

- Increasing profitability and robust cash flows demonstrate the resilience of the business and its potential to continue providing returns to shareholders.

- A long runway for growth and a deepening competitive advantage make for a compelling investment opportunity, but at a premium price.

For several years now, Hermès ( OTCPK:HESAF ) has been one of the best-known luxury companies on the stock market, consistently outperforming investors' expectations for growth and multiple expansion. As a result, many are wondering how long this success story can continue and whether these consistently high multiples are ever reasonable and compelling enough to invest in. I have asked myself this question many times and would like to share my findings with you.

Over the course of the year, Hermès' share price began another run to new highs as the luxury industry celebrated a revival as the darling of investors. But times have changed and the market has become much more cautious about the current macro environment. Consequently, luxury companies plunged and also Hermès is now trading 20% below its high, which indicated prospering opportunities in the past.

Business Model: Excellence

Unlike LVMH ( OTCPK:LVMHF ) or Kering ( OTCPK:PPRUF ), Hermès' business model does not consist of buying up and building various luxury brands. Instead, the family-owned company founded in 1837 is continuously expanding the Hermès brand, now in its sixth generation under Axel Dumas. This family-oriented leadership also includes a more cautious approach to expanding the brand portfolio in general, which is a very positive characteristic in the luxury industry, as otherwise the brand could risk becoming dilutive or plain for the customer.

That said, the company currently classifies its results in seven categories:

- Leather Goods and Saddlery

- Ready-to-wear and Accessories

- Silk and Textiles

- Other Hermès sectors

- Perfume and Beauty

- Watches

- Other Products

While an overview of its business segments shows that Hermès has explored several new product categories, leather goods remain the main contributor with 41% of total sales. In this segment in particular, the company has been able to maintain the desirability of its products, notably through the iconic Kelly and Birkin bags. Both are a tribute to Hermès' commitment to craftsmanship, as each bag is made by a single craftsman from start to finish. In an interview in 2019, Axel Dumas commented on the traditional process as follows:

A bag is done by one person from start to finish, which is not the most efficient way to do that. We know that. But I think there’s a special soul, there’s a special relationship with your bag when you’ve done it from the day one to the end.

In addition, each bag is given a number that is directly associated with the individual craftsman, which, according to Dumas, is an emotional ritual in the manufacturing process. This kind of dedication to excellence is one of Hermès' core values, but it is also its greatest limitation. Or as the current CEO describes it:

There’s one important thing when we recruit is that we don’t do craft shop with more than 250-300 people. Cause we believe that above that it’s not a craft shop, it’s a factory. […] That’s why we have 17 production facilities just for leather in France.

However, Hermès' sales growth is not limited by demand, but by its ability to expand its production capacity. And while other companies would give in to pressure from analysts and investors and start to expand capacity to the limits of demand, Hermès keeps its expansions at a level that ensures the same quality and excellent craft as before. In my view, the company combines the traditional craftsmanship of Swiss watchmakers with the high profitability of other leather goods manufacturers such as Gucci or Louis Vuitton. This positioning is underscored by the fact that the pace of new product launches is much slower than that of its oft-cited French counterparts, as evidenced by the simplicity and timelessness of its runway shows. And by not having started to follow trends, the company achieved to stay out of the competition of all trend-related brands and further stands above these brands while maintaining a high degree of desirability.

Business Segments (own illustration)

Management: Longevity

A similar picture emerges when we take a closer look at the management of Hermès. Since 2013, the company has been led by Axel Dumas, and is thus once again headed by a founding family member. Through various holdings, the Hermès family owns 66.7% of the total share capital and even 76% of the voting rights. Axel Dumas himself holds only about 0.01% of the outstanding shares, but these are currently valued at about €20 million and therefore represent sufficient "skin in the game". In addition, the family is committed to the ultimate goal of passing the company on to the next generation in better shape than before, which in my view offers a promising incentive package.

Luxury Goods Market

This brings us to a quick take on the market for personal luxury goods and its current developments. The last years were very pleasing for investors of luxury companies as most brands faced overall high demand mostly driven by filled pockets and the accumulated desire for extraordinary pleasure. However, as with most industries, only when the tide goes out, we learn who was swimming naked. And in this case, we're now seeing very different results across the luxury industry as demand seems to have settled and budgets have been exhausted, first in the U.S. and now in Europe. This development particularly affected Kering's flagship brands: Gucci, YSL and Bottega Veneta, which are also in a transitional phase. However, compared to other fast-growing luxury brands, Hermès stood its ground and remained the most stable in terms of slowing sales. A strength based on the solid fundamental approach of Hermès distribution and desirability, or in other words: If you waited 3 years for your option to buy a Birkin bag, you probably won't deny it.

| Sales Growth |

| Hermès |

| LVMH (F&L) |

| Kering |

| Brunello |

| Zegna |

| Latest 9M |

| 22% |

| 16% |

| -3% |

| 29% |

| 19% |

| Latest 3M |

| 16% |

| 9% |

| -9% |

| 21% |

| 11% |

According to Bain & Company , the global market for personal luxury goods is expected to grow about 5-8% this year, based on an overall growth that is impacted by slowdowns in mature markets and a slower recovery in China. Furthermore, customers seem to look for "less but better" purchases as luxury items are more often considered as valuable assets. This trend specially impacts the demand for watches and jewelry in the ultra-luxury segment, while also improving the desirability of iconic bags, e.g. the Kelly bag. And this trend could continue into the future, because it's based on solid ground: on the list of best performing bags in terms of resale value, you can find the iconic 1991 Mini Kelly Bag in 1st place, having more than 5 times its value. Hermès is set apart from its competitors by this perfectly applied approach to iconization, or perhaps simply by focusing on the product itself. Federica Levato, partner at Bain & Company , summarizes the outlook for the industry perfectly:

[...] Meanwhile timeless, iconic pieces remain coveted due to their scarcity and continuous appreciation. This means many newcomers are overperforming, but they are competing in a world of giants, who are also experiencing much success. To remain relevant in the long run, brands will need to continue to channel an insurgent mindset, championing hero products and their founders’ visions, while also tooling up to sustain long-term growth by getting the business fundamentals right.

From my perspective, Hermès is ticking all the right boxes to maintain the strong demand and desirability of its products, leading to a long potential runway for growth. However, it is important to keep in mind that all these arguments are not intended to validate an extrapolation of recent sales growth into the eternal future. Instead, future growth rates are likely to be more in line with the underlying market growth, which is expected to be around 6% p.a. until 2030. And if the iconization trend continues, we should see low double-digit EPS growth in the medium term, combined with Hermès' low exposure to fashion trends and well-managed inventories.

Capital Allocation

Analyzing French luxury flagships LVMH and Kering, a key part was looking closely at capital allocation strategy, as both companies are known for their acquisitive nature. In addition, the "other products" segment includes the sales of other acquired companies, which currently account for around 2% of the group's sales. However, one should not make the mistake of applying this approach to Hermès, as the company has focused solely on its own operational and strategic management, led to a few investments in suppliers and three wholly-owned brands. But apart from that, Hermès does not include M&A in their capital allocation strategy that was described by Dumas as follows:

The way we split the cash flow is one third dividend, one third in capex and one third in cash.

So let's take a look at each of them individually.

Dividends & Share Buybacks

Over the past decade, Hermès has paid out an average of about 32% of its operating cash flow in dividends and occasional special dividends, which is pretty close to the rule of thumb described by Axel Dumas. From my perspective, this is exactly the right way to approach a dividend policy, as I am personally not a fan of companies that consistently burn through their cash flow for the sole purpose of not losing their status as a dividend aristocrat. Apart from that, share buybacks are not part of the company's toolbox and are only used to compensate for employee share plans.

Dividend per Share, 2013-2022 (annual presentation)

Reinvesting in the Business

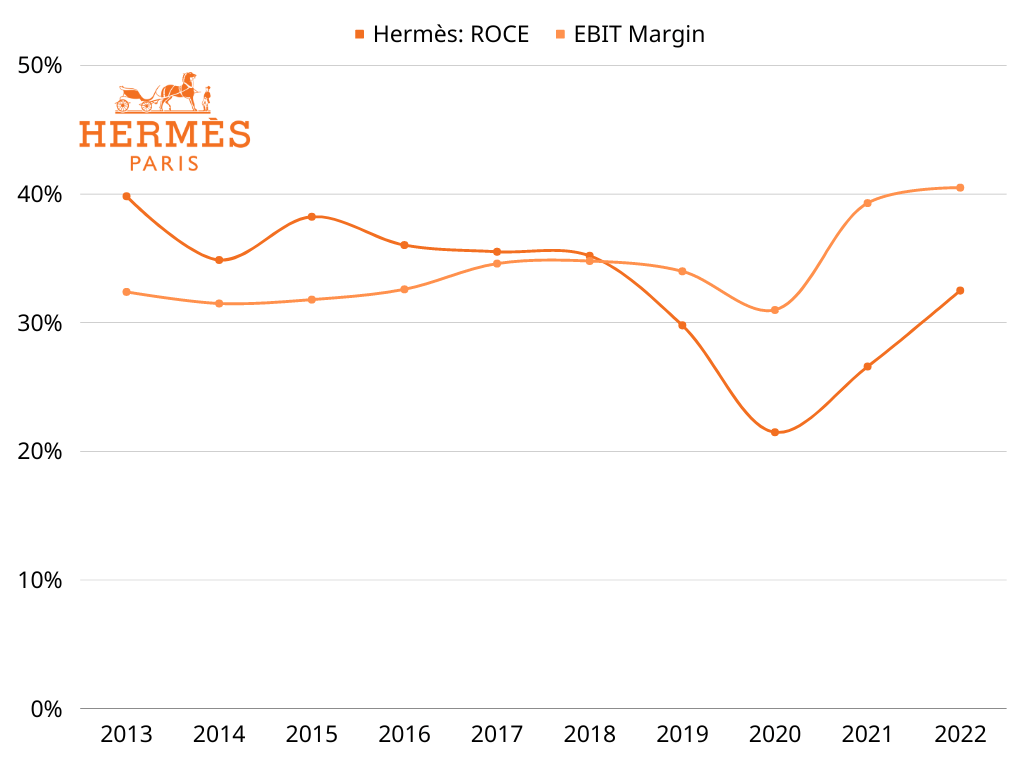

Instead of another third, Hermès reinvests an average of only 21% of its operating cash flow in the business in the form of capital expenditures and operating leases, resulting in a return on capital employed of around 38.5%.

{kind=link}

Return on Capital Employed, 2013-2022 (own illustration)

And although the company is facing a declining rate of capital turnover, the overall ROCE has remained strong due to increased profitability. However, the low reinvestment rate already suggests that Hermès' impressive capital efficiency is limited by its own ability to increase production capacity while maintaining exclusivity. And given its generally conservative management approach, the company is likely to reinvest cautiously rather than boldly, further strengthening the hard-to-measure intangible asset that is its brand. Potentially, this is a fact that cannot be underlined enough: Hermès will always focus on maintaining the highest possible product quality and will do any investment necessary to protect this and the desirability for the brand. Also, return on investments into the brand itself are difficult to quantify and therefore, one should be cautious when analyzing these metrics for the company.

Operating Investments, 2022 (annual presentation)

Cash Position

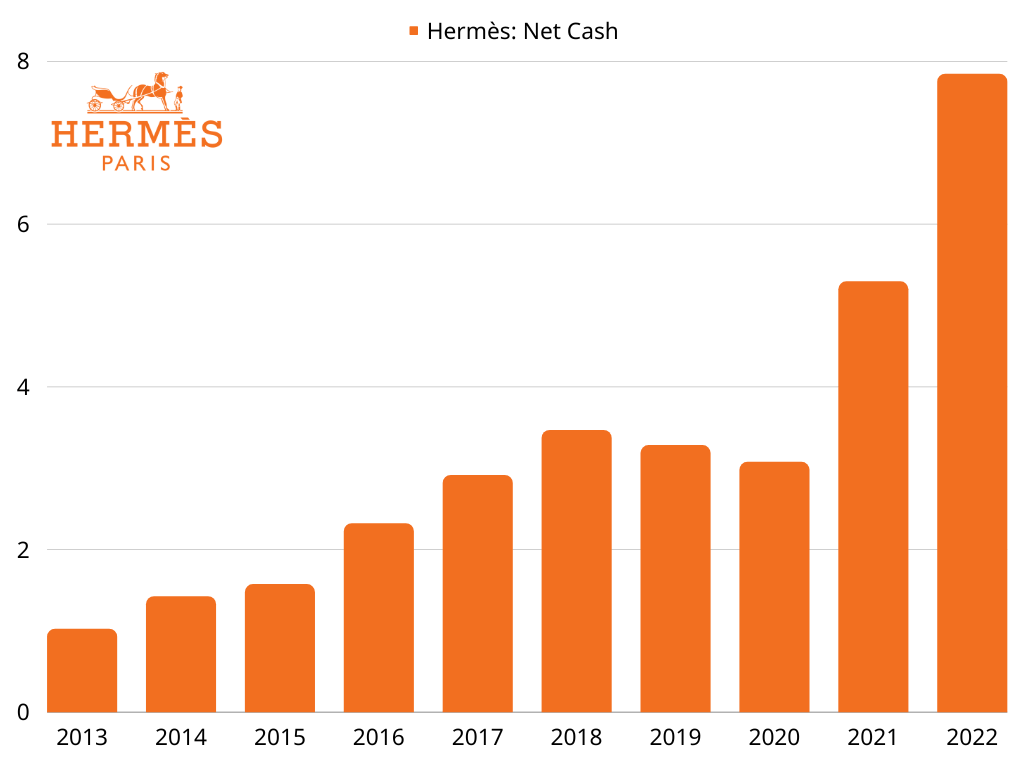

Having learned that Hermès has become more conservative in its use of capital, we can already predict that more than a third of its cash flow will be put in the bank account. In fact, over the last 10 years, Hermès has built up a net cash position of almost €8 billion, which has grown especially during the last boom years. So, instead of facing the challenge of refinancing in a higher interest rate environment, Hermès only has to worry about where to make the most of it. Or as the current CEO, Axel Dumas, put it in an interview :

So, when it's the craziness of 2006, analysts will say: ah terrible Hermès, you are leaving money outside, you have no debt that preclude you from paying ambassadors, opening more stores. And two years after, when there was a financial collapse, people will say: ah wonderful Hermès, you have no debt, you are so wise. So it's done by a cycle.

Therefore, it can be concluded that Hermès will always prefer a cash position over leverage, which is a consequence of the company's prudent nature. Nevertheless, the rapidly expanding cash position highlights that capital allocation at Hermès is restricted by time and the need to maintain the exclusivity of the brand, which will lead to a limited growth rate in the long term.

{kind=link}

Net Cash, in € billion, 2013-2022 (own illustration)

Cash Flows

In order to analyze a company's ability to generate cash from operations, I focus primarily on its free cash flow. Despite the usual calculation (OCF - CapEx = FCF), I adjust the operating cash flow for changes in net working capital and subtract the stock-based compensation. Using this approach, I try to get closer to the actual and sustainable cash generation of the business through the perspective of its owners.

For Hermès, the calculation looks like this:

| in € million |

| Operating Cash Flow |

| 4,550 |

| - Stock-based Compensation |

| 57 |

| - Changes in Net Working Capital |

| -175 |

| = Adjusted Operating Cash Flow |

| 4,668 |

| - Capex |

| 577 |

| - Payments on Lease Liabilities |

| 270 |

| = Free Cash Flow |

| 3,821 |

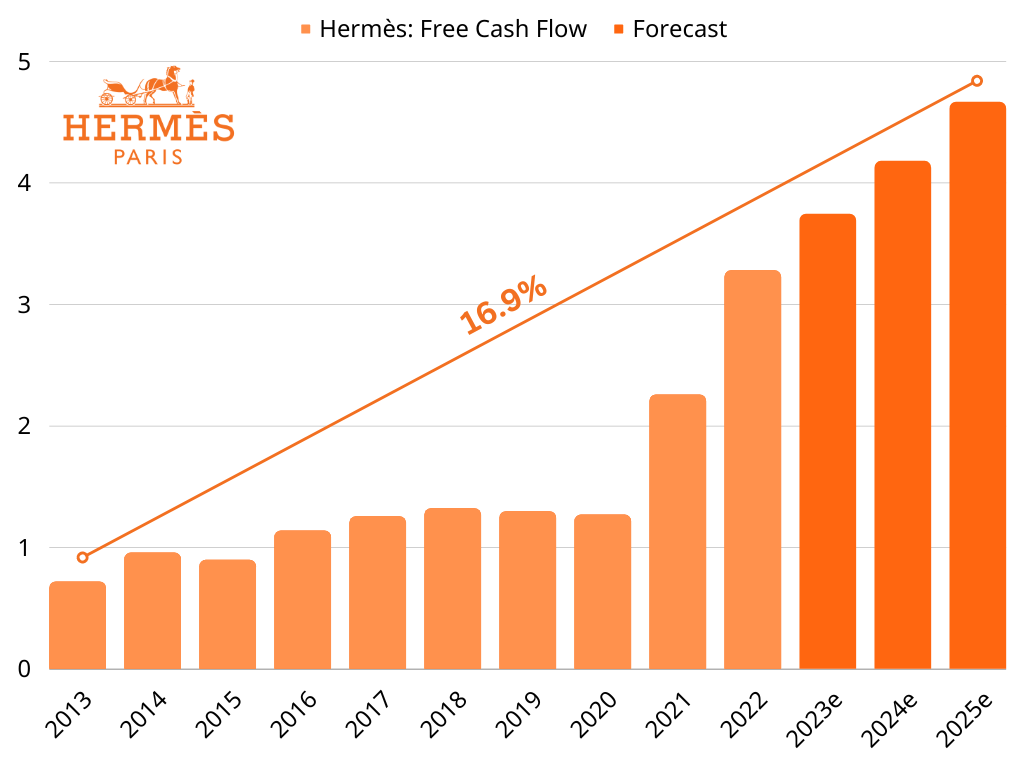

During the latest comprehensively reported period, H2/22-H1/23, Hermès was able to convert around 65% of its EBITDA into free cash flow, while the historical average is around 55%.

Applying this procedure for the last 10 years, Hermès achieved an CAGR of 18.4%, which is highly impressive and also corresponds to the simultaneous share price appreciation of around 20.8% per annum.

{kind=link}

Free Cash Flow, in € billion, 2013-2025e (own illustration)

In order to estimate future cash flows, I used an free cash flow conversion of 60% and the analysts estimates on EBITDA for 2023 to 2025.

According to these forecasts, Hermès is expected to grow EBITDA at 13.5% per year until 2025, which is already indicating the anticipated slowdown of demand, however, on a high basis. And I would further assume that Hermès will be able to maintain these low double-digit growth rates for quite some time as the company positioned itself perfectly for the luxury consumer. Firstly, by offering entry-level goods for the aspiring consumer, who later also must have purchased at least several more expensive products to finally be able to accomplish his long-awaited dream of owning one of the iconic Hermès bags.

Valuation

At a current share price of around €1,752 or $1,824 ( OTCPK:HESAF ), Hermès is currently valued with a market capitalization of around €183.5 billion, ranking it as the 3rd most valuable company in France. Including the company's net cash position of €7.8 billion, I arrive at an enterprise value of around €175.7 billion.

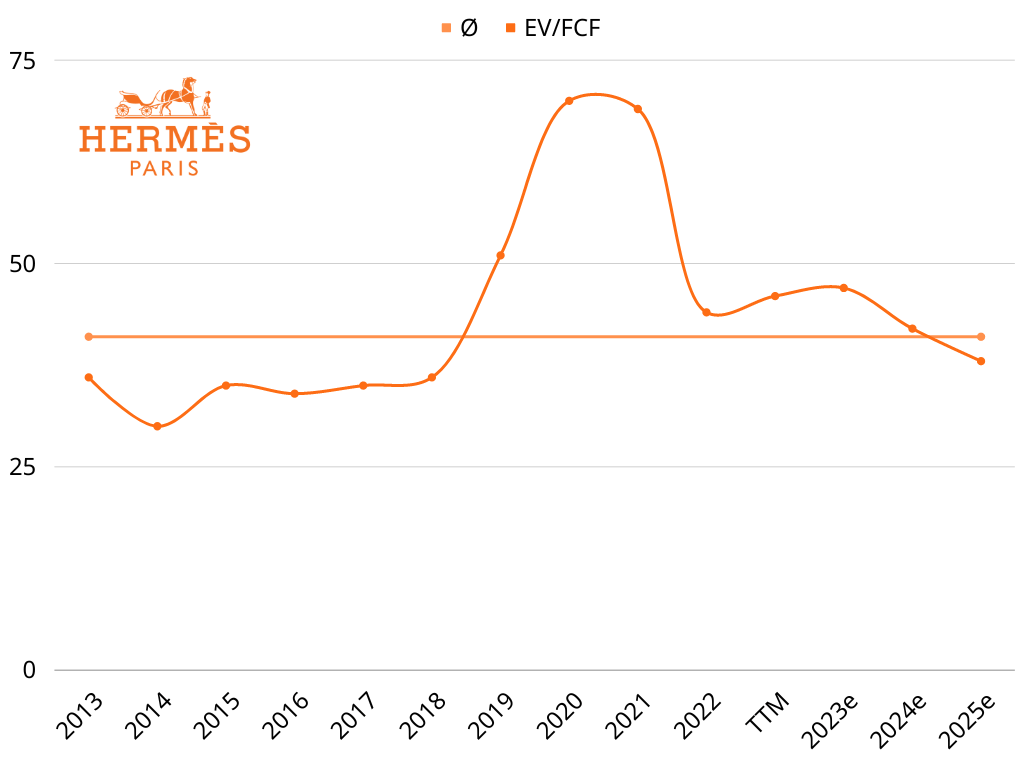

Regarding the latest 12-months figures for the company's cash flows, Hermès is trading at an EV/FCF multiple of around 46, which is below the 19' pre-pandemic level of 51, but still above the average over the last decade of 41. Generally, the shares of Hermès trade at a premium, even compared to its luxury peers in France.

{kind=link}

EV/FCF, 2013-2025e (own illustration)

The present multiple valuation signals that the market has grown more bullish on the company's future growth rates after Hermès almost tripled its free cash flow over the last three years. I believe this to be the case in the medium term, as the order backlog for the most valuable products should allow the company to maintain the higher growth rates for longer than other luxury companies. To understand the current growth rates that are factored into pricing, I utilized an inverse DCF model with the current data. So let's see what we find!

Inverse DCF (Own Illustration)

Looking out five years, the current share price suggests an annual growth rate of 17%, based on historical results and assuming that the company can maintain its current performance over the medium term. Given a standard 10% underlying discount rate and a higher yet reasonable 4.5% terminal growth rate, we project an annual growth rate of approximately 16% from year 5 to 10. That's exhaustingly high and also surprising given that the company almost reaches its 10-year average multiple. Therefore, I would assume that the company's expected growth rates must have constantly been at mid-teens. Further, the multiple didn't contract as the company kept delivering. That said, it becomes clear that Hermès is trading almost always at the upper end of the analysts' expectations, resulting in little upside through multiple expansion or short-term earnings surprises.

Nonetheless, my inverse DCF model examines only a ten-year period and assumes a sole terminal growth rate. This approach falls short of accurately assessing the value of a company possessing such exceptional qualitative and profitable brand equity as Hermès. The moment when the company will stop generating moderate operating growth is almost unpredictable, given the outstanding uniqueness and pricing power of its brand. As time passes, the brand and its heritage only continue to grow, making it increasingly challenging to rebuild and compete. Investors should consider this when evaluating an investment in Hermès, in my opinion.

Takeaway

Hermès is a special company. It is a family-owned business that has successfully increased its value across various market environments while maintaining a highly regarded brand and corresponding commitment to quality. In particular, the company has experienced accelerated growth and profitability in recent years, making it an ideal investment case. However, while medium-term growth prospects remain strong, limited reinvestment opportunities and a lack of M&A activity raise concerns about long-term growth drivers. Despite these factors, I anticipate the company will continue to perform well for some time, given its strong position in the market and its reputation for providing highly desirable products to customers. Hermès is expected to profit excessively from the industry's fundamental expansion, and to hike prices even more to stimulate future shareholder returns.

That being said, it must be acknowledged that the company is currently valued at an above-average multiple, implying growth in the mid-teens for the next decade. As a result, it is improbable for Hermès to double in value in the following year or be significantly undervalued. However, I believe it is a fantastic investment opportunity for investors seeking to purchase high-quality companies and hold them long-term alongside their owners. I believe that the long-term growth potential of a company is often undervalued due to its resilience, which can be difficult to quantify. Recently, I invested in Hermès and plan to increase my position if there is another market downturn caused by industry-related concerns.

For further details see:

Hermes: Look After It For The Next Generation