PPRUF - Hermes: Reiterating My Sell Rating Despite Being Wrong Regarding My Initial Thesis

2023-04-03 04:44:43 ET

Summary

- Hermès outperformed the S&P 500 by a wide margin since my initial article.

- I still think that Hermès will face gross margin headwinds in the near-term future.

- I underestimated Hermès' operating leverage on the OPEX level.

- I have to reiterate my "sell" rating due to the sky-high valuation.

Author's note: Since Hermès is reporting in EUR, I will refer to the EUR numbers and only add the USD equivalent for per-share and valuation purposes.

Introduction

This will be an update article on my initial article on Hermès (HESAY) (HESAF). As can be seen in the snippet below, my initial "sell" rating didn't go well.

Performance since Author's initial article (Seeking Alpha)

Since my last article, Hermès outperformed the S&P 500 by a very wide margin. I will cover the drivers for this outperformance in this article and critically review my initial thesis, including an update on the valuation.

What happened since my initial article?

When I wrote my initial article, Hermès had only released the full financial statements for FY2021 and the sales report for the first quarter of FY2022. Hermès discloses the full financial statements every six months so there was no data on first quarter FY2022 earnings. I will just compare the numbers that I used in my last article. In the chart below I compiled the changes in TTM revenue, net income and free cash flow since my last article (numbers in €million):

| Metric |

| Last article |

| Currently |

| TTM Revenue |

| 9,663 |

| 11,602 |

| Net Income |

| 2,445 |

| 3,367 |

| Free Cash Flow |

| 2,873 |

| 3,666 |

At the time I wrote my last article, Hermès traded at €1,074 per share at a P/E of around 44 (on a cash-neutral basis). Assuming the same valuation on the current TTM net income of €3,367 million would result in a price per share of €1,415.

TTM Revenue grew by 20.1% while Net Income grew by 37.7%. Disregarding valuation changes, revenue growth contributed to a 20.1% share price increase and net income margin expansion to another 11.7% share price increase. That means that the remaining 41.2% (!) of the share price increase was solely attributable to an increase in the valuation from a P/E of 44.1 to the current PE of 55.9. The remaining increase on a USD basis as seen in the snippet above resulted from currency effects.

Nevertheless, an increase in the share price of 31.8% on an unchanged valuation level due to underlying performance is very impressive. This is where my initial thesis comes into play.

Initial Thesis

My initial thesis was that Hermès benefitted from a temporary increase in margins due to an aftereffect of the pandemic. I wrote the following regarding what to look out for following my initial article:

Hermès will publish first half results for the FY2022 on 07-29-2022. The most important part of this report will be the margin development. If there are signs of the margins already starting to compress compared to the record highs of FY2021, this could lead to a further drop in the stock price.

My guess is that we will only see margins start to compress in the results of the second half of FY2022, which should be released around February 2023. I will probably write an update article after these results are published.

Source: Initial article - What to look out for

And here is what I wrote in early January as a reply to a comment from a reader who asked what the reason may be that the stock already went up 60% since my article:

The multiple expanded from the already high P/E of 44 to the current 55, so around half of the gain came from multiple expansion. The rest came from sales growth (around 10%) and another spike in net margin. As I stated in the article my guess is that we will only see margin compression from the second half of FY22 or maybe even later in FY23. I still intend to write an update article once FY22 are released in February.

Source: Initial article - Comments

Thesis review

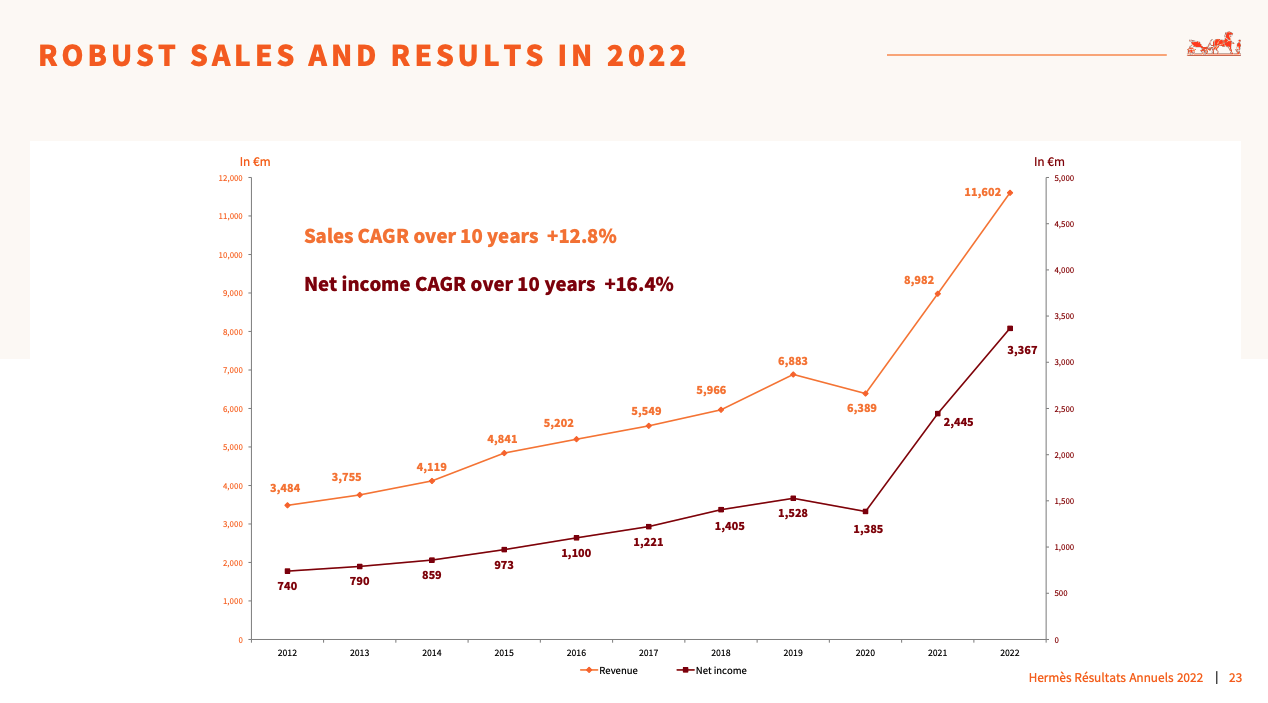

I want to start with two updated charts from Hermès recent FY2022 results presentation:

Sales and Net income FY2021-FY2022 (2022 full year results presentation)

{kind=link}

Hermès nearly doubled its revenue and net income from 2012 to 2019. That's a period of 7 years. From 2020 to 2022, Hermès nearly doubled its revenue and net income again in a period of just 3 years. However you look at it, this looks not sustainable and rather like a one-time event driven by extraordinary external factors.

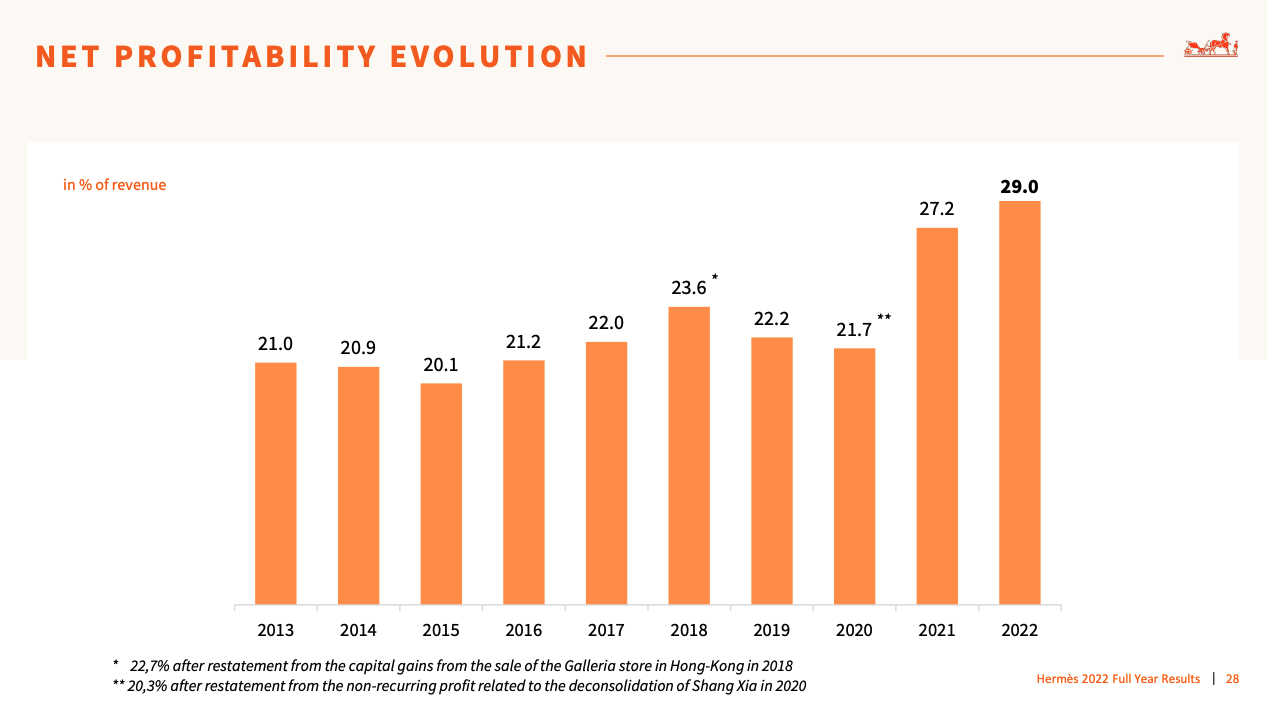

Net profitability FY2013-FY2022 (2022 full year results presentation)

{kind=link}

Here we can see that the margins hovered around 22% over the past and only started to explode in FY2021 and FY2022. Again, this looks unsustainable and like an outlier to the upside.

Looking at peers LVHM ( LVMHF ) ( LVMUY ), Richemont ( CFRHF ) ( CFRUY ) and Kering ( PPRUF ) ( PPRUY ), we can see that this margin development is not unique to Hermès but rather a phenomenon throughout the whole luxury sector.

Hermès' operating margins hovered a bit above the 30% mark in the past decade and exploded to 40% right after the pandemic. LVMH managed to meaningfully expand its margin as well (from around 20% to the current 25%). Kering and Richemont weren't able to expand margins throughout the last decade but also experienced a spike in the past two years.

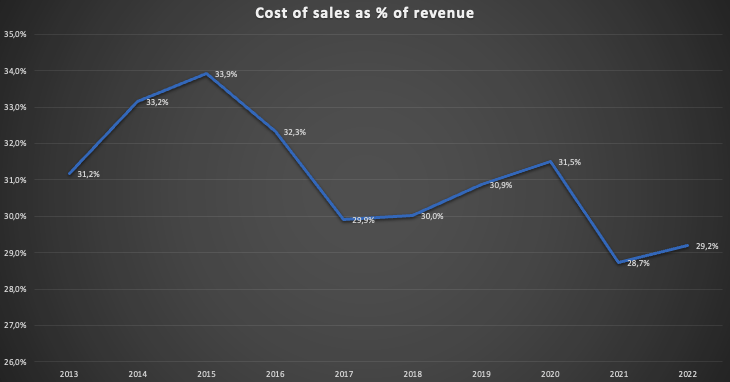

In my initial article, I guessed that this was due to a shift of revenue from FY2020 to FY2021 and beyond because the closure of stores hindered the sale of already produced goods while those goods were accounted for in FY2020. If this was the case, costs of sales as a % of revenue should have dropped meaningfully in FY2021, causing a noticeable margin improvement. The below chart shows the costs of sales as % of revenue over the last decade:

{kind=link}

We can see that costs of sales as % of revenue indeed declined sharply in FY2021 and started to slowly rise in FY2022. The table below shows the development over the past financial reports of the company:

| Report |

| Costs of sales as % of revenue |

| First half FY2020 |

| 35.0% |

| Second half FY2020 |

| 29.3% |

| First half FY2021 |

| 28.5% (bottom) |

| Second half FY2021 |

| 28.9% |

| First half FY2022 |

| 29.0% |

| Second half FY2022 |

| 29.4% |

I still think that this might be a continued headwind over the near term.

Where have I been wrong?

After taking a deeper look at the structure of the operating expenditures (OPEX), I realized that the aforementioned gross margin improvement in FY2021 was just one part of the puzzle and I failed to look at the other parts.

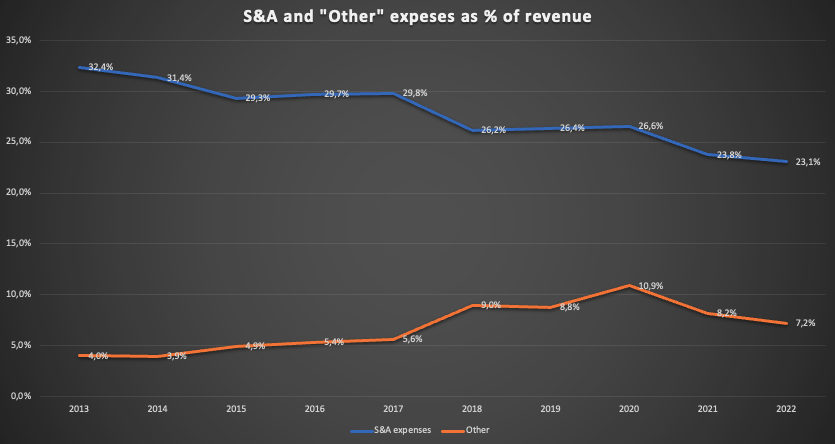

While I correctly assumed that there would be some margin headwinds on the gross margin level, I underestimated the operating leverage of the OPEX. The chart below shows the development of S&A and "Other" expenses as % of revenue over the past decade:

{kind=link}

S&A expenses as % of revenue steadily declined over the past decade, a trend that doesn't seem to stop. Regarding the "Other" expenses, the spike in FY2018 was due to IFRS16 and changes in accounting. Under this position, Hermès mainly reports depreciation, amortization and impairment expenses.

In conclusion, the huge margin spike in FY2021 was due to three factors: (1) declining costs of sales as % of revenue, (2) declining S&A expenses as % of revenue, (3) depreciation and amortization expenses not growing hand in hand with revenue.

My initial article only covered reason (1) and failed to address the other two. With these new insights, my past "sell" rating seems exaggerated. While I still think Hermès didn't deserve a "buy" rating back then (at a P/E of 44 on a cash-neutral basis), a "hold" rating would have been appropriate.

Taking into account that S&A and "Other" expenses as % of revenue will likely keep declining or stay where they are, even factoring in a possible gross margin headwind of around 100-150 basis points, the current margin level might be sustainable after all.

Valuation

Note: The USD equivalents refer to one ADR (HESAY). 10 ADR = 1 share on the Euronext Paris.

Hermès currently trades at €1,864 ($202.60 per ADR) at the Euronext Paris stock exchange. The FY2022 average diluted shares outstanding stood at 104,936,295 shares, resulting in a market capitalization of €195.6 billion ($212.6 billion). After deducting the net cash position of €7.3 billion, the enterprise value (EV) amounts to €188.3 billion ($204.7 billion). With FY2022 net income of €3,367 million and free cash flow ((FCF)) of €3,611 million, the current PE stands at 55.9 and the FCF yield at 1.92%. Both valuation metrics are very high. Hermès was able to generate returns on capital employed (ROCE) of around 50% over the past few years, an outstanding number.

With these kinds of valuation levels, I will refrain from calculating my usual long-term return prospects using FCF yield and potential growth. I will instead just jump right into a DCF valuation. Assuming a 10% discount rate and 6% growth into perpetuity (as I usually assume for businesses with outstanding ROCE), at what rates would Hermès need to grow over the next decade to justify the current valuation? Hermès cash conversion averaged 105% over the past few years. Current earnings per share are:

€3,367 million divided by 104,936,295 shares = €32.09 ($3.49 per ADR)

Normalized FCF per share would have to be:

€32.09 x 105% cash conversion = €33.69 ($3.66 per ADR)

I will use a reverse DCF calculation with the aforementioned numbers. Here is the result:

DCF valuation (moneychimp.com)

Hermès would need to grow earnings at a CAGR of 15.3% over the next decade and 6% thereafter to justify the current valuation.

According to S&P Capital IQ, Analyst estimates predict 13.7% revenue growth in FY2023 and 10.8% in FY2024. Even factoring in the huge revenue growth spikes in FY2021 and FY2022, Hermès "only" grew sales with a CAGR of 12.8% from FY2012 to FY2022. Especially a company like Hermès can't grow revenue exponentially because the main revenue driver will be price increases. If unit sales were to rise dramatically, the Hermès brand would lose part of its exclusivity, ultimately hurting the brand's image as the undisputed leader of luxury brands. If you want to read more about my thoughts on why Hermès is the absolute leader in the luxury space, I would like to refer you to my initial article.

Hermès is also overvalued if we just look at how it has been priced in the past, as can be seen in the chart below:

The average PE over the past decade was around 45. Excluding the outliers from 2020 to 2021, the median was probably around 40. At the current cash-neutral PE of close to 56, Hermès looks overvalued.

Risks

Regarding risks, I wrote the following in my last article:

The main risk to this thesis is that the margin expansion in the recent past is not temporary, but rather sustainable into the future.

Source: Initial article - Risks to the thesis

While I outlined in this article that I still see margin headwinds on the gross margin side, I underestimated or failed to see the operating leverage on the OPEX level. After all, factoring in that S&A and "Other" expenses as % of revenue will keep declining or stay flat, current margins might be sustainable after all.

Since I will reiterate my "sell" rating, the only risk I can see is that I underestimate Hermès' revenue growth potential or the potential for further operating leverage. Hermès would need to grow earnings at a CAGR of around 15% over the next decade to justify the current valuation. This might be possible, even if I highly doubt it, with healthy revenue growth accompanied by more operating leverage/margin expansion. If Hermès manages to push operating margins to the area of 45% over the next decade, it might achieve such earnings growth rates with the revenue growth rates it has shown in the past.

Conclusion

After reviewing my initial thesis, I conclude that I underestimated Hermès' operating leverage potential on the OPEX level. The "sell" rating in my last article was a wrong call and a "hold" rating would have been appropriate.

Hermès continues to be the absolute leader in the luxury goods space, with ROCE averaging around 50% over the past few years. It is still an excellent company and I will keep covering it in the future.

However, the rise in share price over the past year lifted the stock to a valuation level that not only leaves no room for error but probably prices in more than the company will be able to deliver.

I will close this article with a quote from Warren Buffett in the 1982 letter to shareholders of Berkshire Hathaway:

For the investor, a too-high purchase price for the stock of an excellent company can undo the effects of a subsequent decade of favorable business developments.

Source: Berkshire Hathaway 1982 letter to shareholders

With this, I reiterate my "sell" rating on Hermès.

For further details see:

Hermes: Reiterating My Sell Rating Despite Being Wrong Regarding My Initial Thesis