HESAF - Hermes Stock Upside Is Limited And Correction May Be Ahead

2023-04-20 12:02:06 ET

Summary

- Hermes is a beautiful business, but it has high China exposure.

- With a P/E of 60x, the market appears to expect them to maintain high growth rates forever.

- The business model is more vulnerable to recession than people may realize.

- Given the likely too-high valuation with limited upside potential, I believe Hermes stock is a solid short for a balanced long/short portfolio.

Thesis

Hermes ( HESAY ) is a fantastic business, but it simply doesn't deserve a P/E multiple of 60x. The market seems to think that Hermes has close to infinite pricing power due to the ultra-wealthy cult-like customer base, but that is not totally true, and actually, they seem to be quite susceptible to recession. Looking from a fundamental perspective, the stock is overvalued, and from a trading perspective, the P/E rose above the historical average due to recent years' explosive revenue growth. However, when the growth rate normalizes, the P/E will likely return to the historical mean.

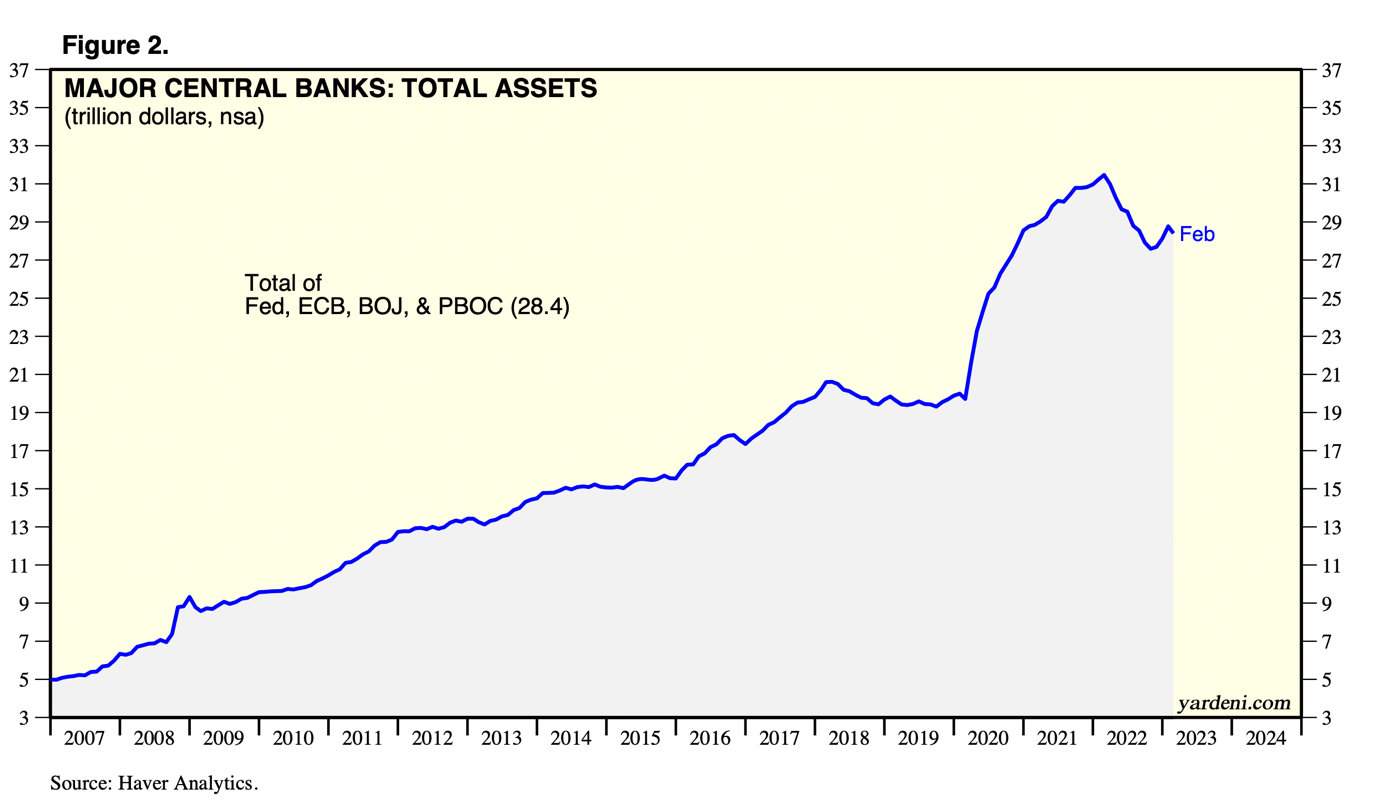

Macroeconomic boost

Since the pandemic, global central banks have created record amounts of liquidity to the market, and major central banks' balance sheets have expanded to nearly $30 trillion, 50% up from the pre-pandemic levels. Naturally, all of that liquidity ends up somewhere, and in the end, the major beneficiaries are wealthy individuals. Combine that with the closure of global borders, and there weren't that many places to spend such massive amounts of money, so savings ballooned. Obviously, the money must be spent somewhere, which leads to increased spending on crazy things like €100,000 handbags.

{kind=link}

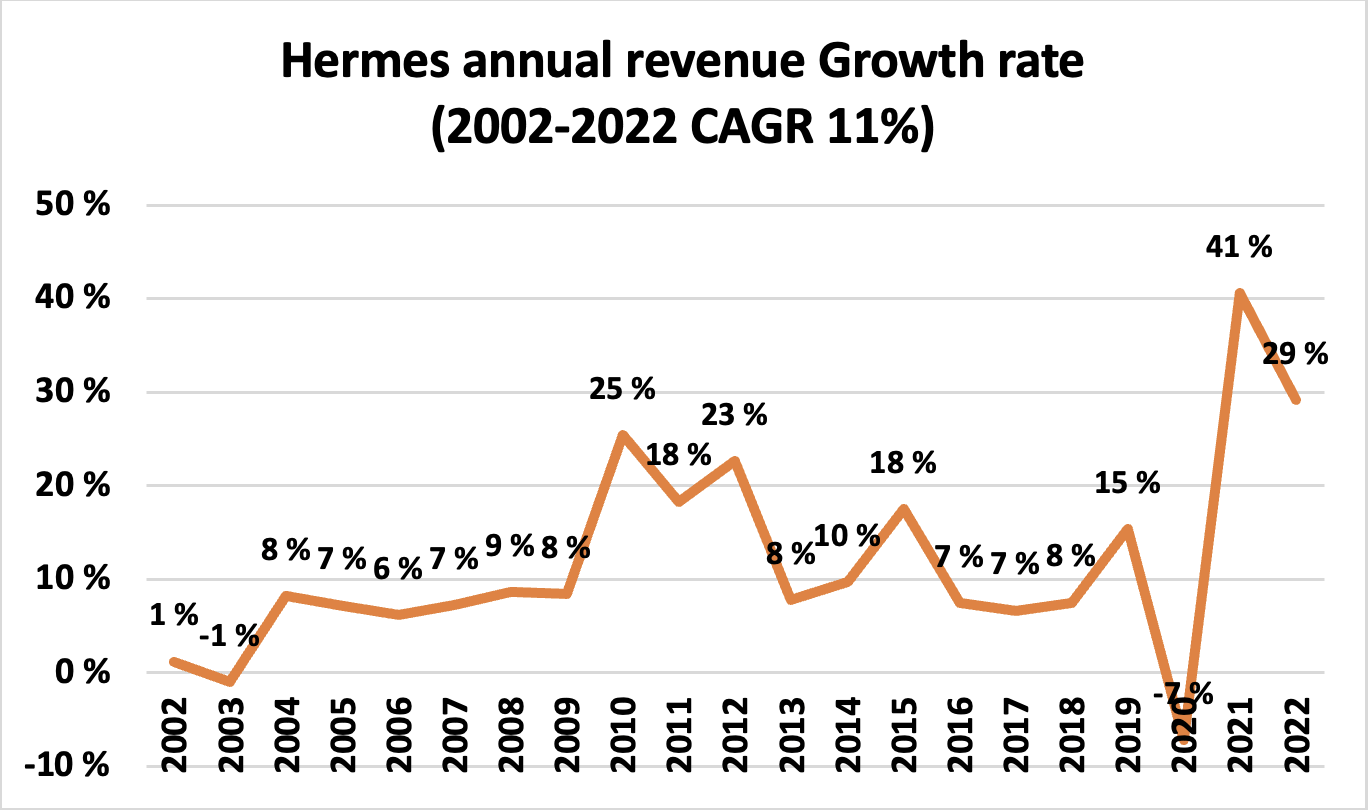

Over the last two decades, Hermes has demonstrated consistent but somewhat cyclical growth. Typically, annual revenue growth is in the high-single-digit. However, during recessions, the central banks' liquidity creation benefits mainly the wealthy people, and subsequently, Hermes always gets a significant revenue growth boost in the few following years.

Author's Excel, Sourced from Annual Reports

{kind=link}

The compounded annual revenue growth rate over the past two decades was 11%, and the question is, can Hermes maintain the historical growth rate over the next two decades? It is possible. However, an 11% CAGR from a €1.2 billion revenue starting point is a whole lot easier than achieving it from the current *€12 billion revenues. Making €120 billion in revenues by 2042 is a lot from just luxury fashion.

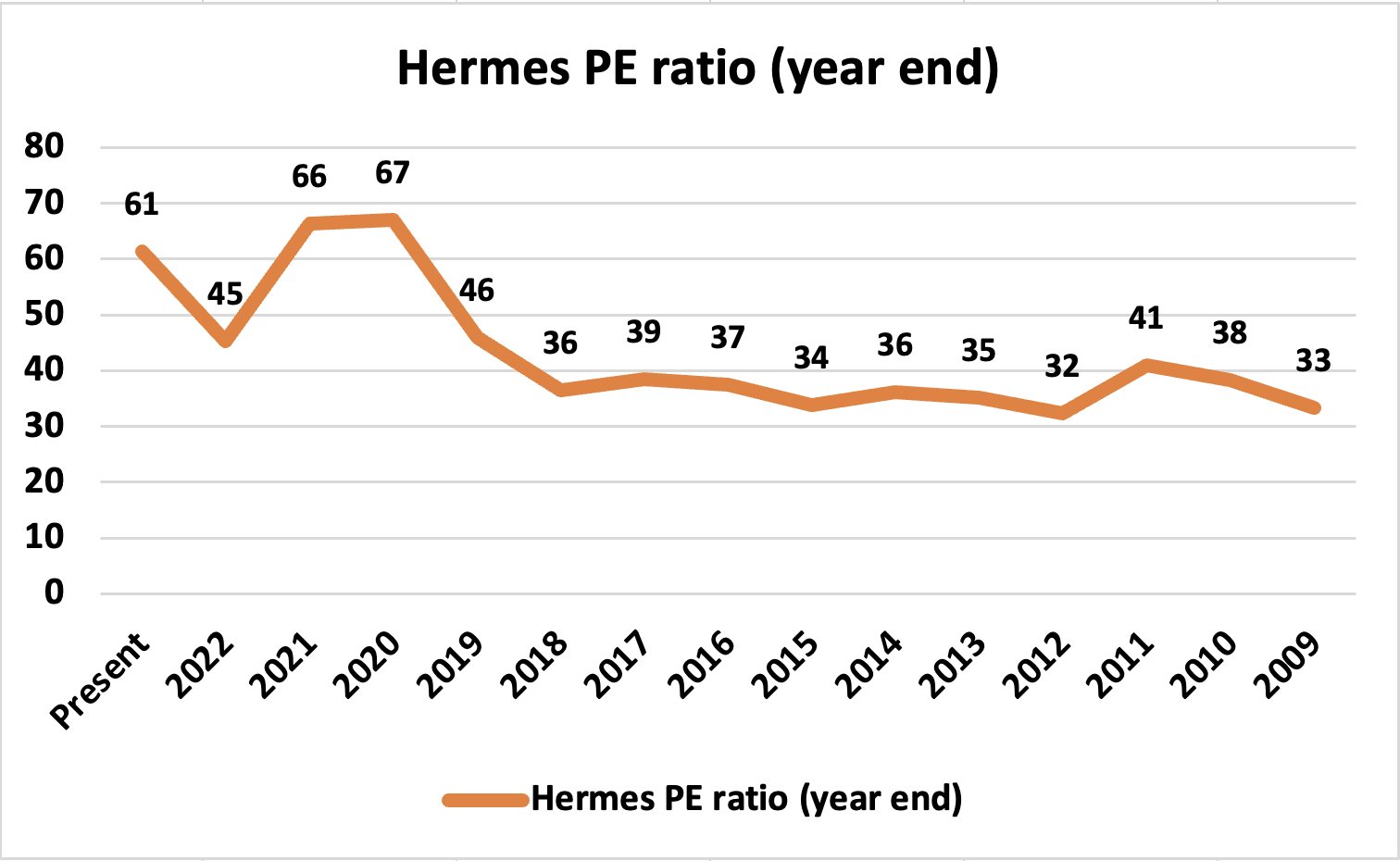

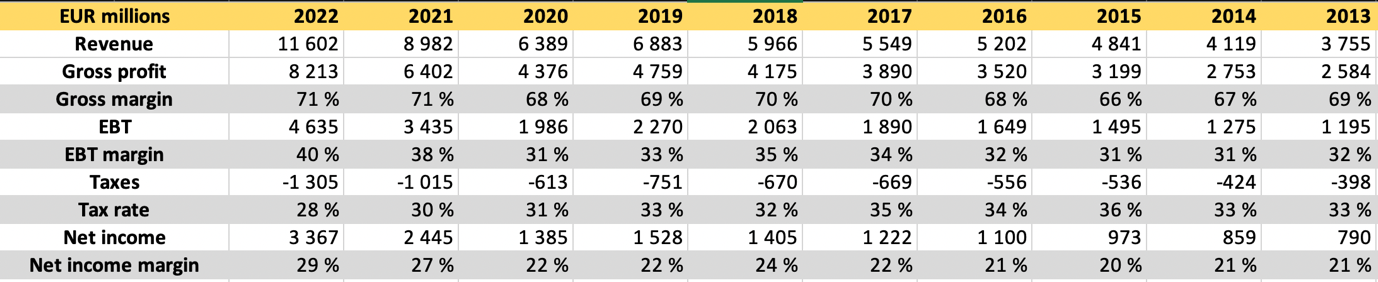

Historical P/E multiple

In the past two years, Hermes' growth skyrocketed, and as the growth accelerated, also the P/E multiple expanded.

{kind=link}

It's easier to justify a P/E multiple of 60x for a company growing revenues above 20% annually. However, when the growth slows down, let's say, to mid-single-digit or dare I even think that there might be a sales decline year. Then the P/E of 60x will become a lot more difficult to justify, and the multiple will likely return to its historical range.

Author's Excel, Sourced from Annual Reports

{kind=link}

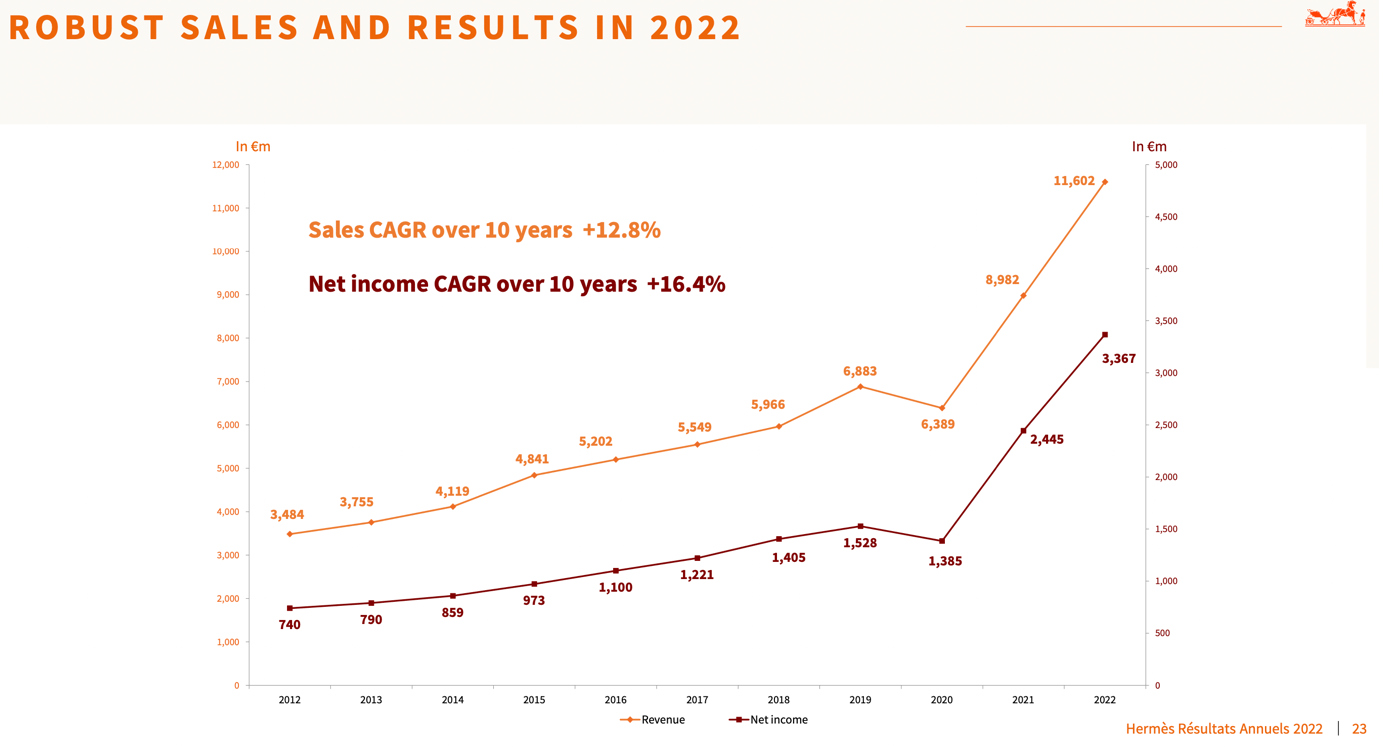

On top of receiving a temporary revenue growth boost, France also lowered its corporate tax rate , which led to net income margin expansion from the historical 20% range to the current 30%. Going forward, achieving further margin expansion will be more difficult, and there could even be a margin decline.

Author's Excel, Sourced from Annual Reports

{kind=link}

Pricing power

You may assume that because Hermes sells its products to ultra-high-net-worth individuals, they have almost infinite pricing power. I also thought so, and it is partly true. However, if we look at the 2022 constant currency revenue growth of 23%, only 4% was due to pricing increases , and the rest 19% was due to sales volume increases. In Q1 2023, the constant currency growth stayed at 23%, and for FY23, pricing increases were guided to be 7%; thus, we can conclude that there was approximately a 16% volume increase in Q1. Therefore, instead of growing by constantly increasing product prices, Hermes is mainly growing by increasing sales volumes, which means they are likely expanding their customer base into lower-wealth class customers.

Hermes' crown jewel product is the Birkin bag, which has limited production capacity. They don't disclose how many bags they produce, but it's estimated that only 200,000 to 300,000 pieces are outstanding . The bag increased its popularity only in the 90s, and if we assume the production increased slowly year over year, the current production rate likely stands at around 20,000 to 25,000 pieces. A Birkin bag costs between $9,000 to $400,000 , so even if the average selling price is as high as €80,000, with 25,000 pieces sold annually, that would lead to only €2 billion in revenues, which is plenty but still less than 20% of Hermes group total revenues. Also, note that actual production volume and average selling prices might be materially lower, as the following article suggests. So, the overall growth is mainly fueled by lower price point products that are also accessible to less wealthy people.

I confirmed of my thesis in the FY22 earnings call. When asked about growth in Europe, the CEO responded that it depends on the macroeconomics and dynamics of the middle class.

For a billionaire daughter, it may be irrelevant if she pays €50,000 or €500,000 for that Birkin bag. However, the lower price point products that are also accessible to the middle class and also, to some degree, the lower half of the high-net-worth individuals are more price sensitive, and if there is a recession, luxury products would be the first place to cut expenses.

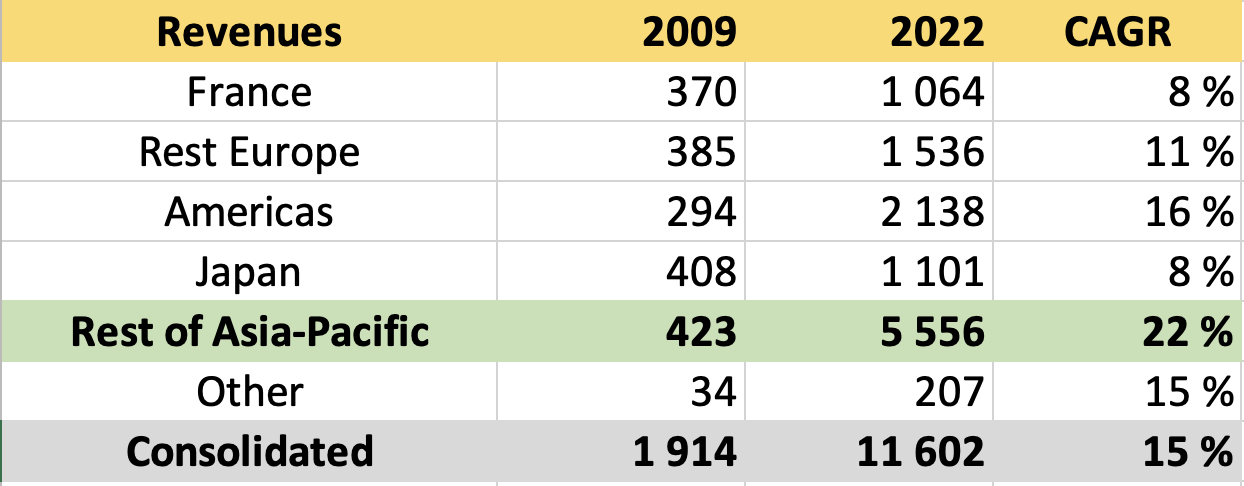

China exposure

Over the past decade, growth in China has been significantly faster than in the rest of the world, likely due to cultural changes. Currently, the rest of the Asia-Pacific region, which is primarily China, accounts for 48% of the group revenues.

Author's Excel, Sourced from Annual Reports

{kind=link}

So Hermes' business model is susceptible to an economic slowdown in China, potential real estate collapse, West's decoupling efforts, and the potential risk of China Taiwan war.

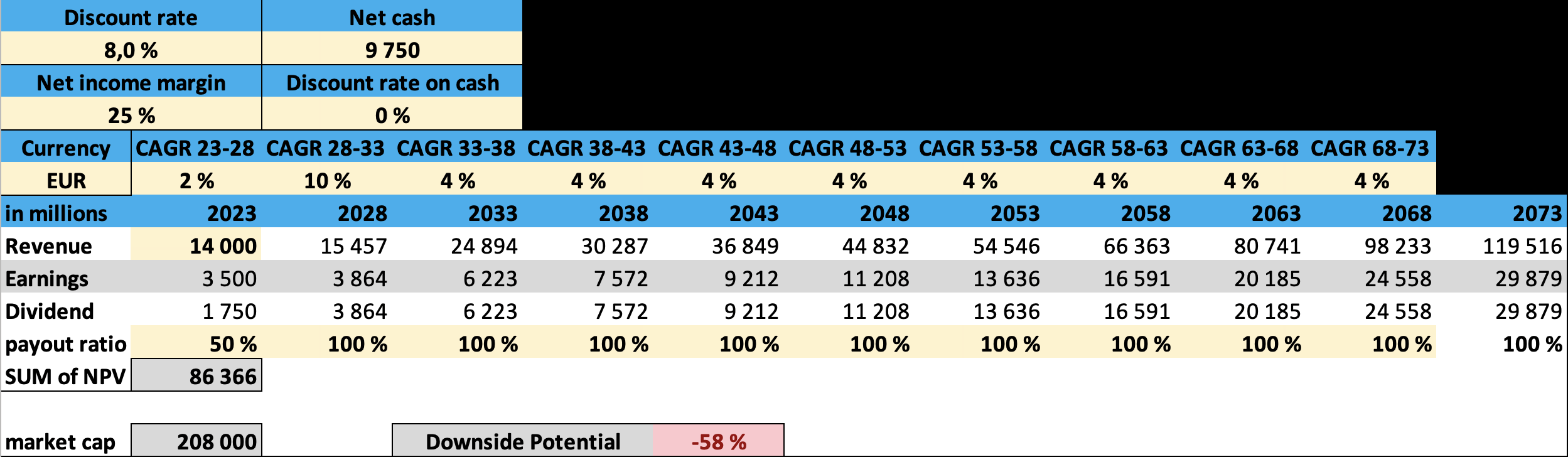

What is required for Hermes to deliver solid returns when the numbers are placed in a DCF model?

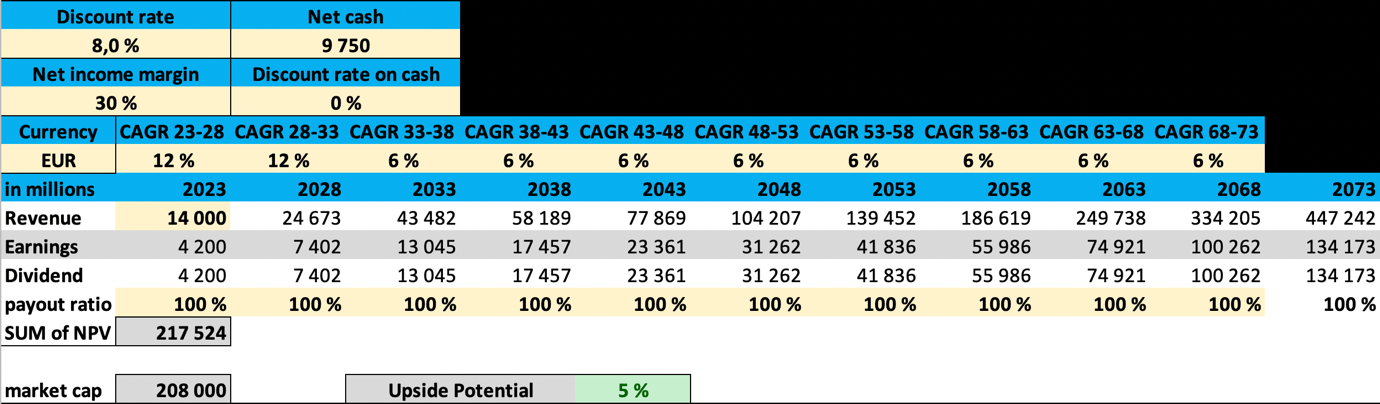

Let's assume that Hermes can maintain a 20% growth rate for 2023, leading to €14 billion in revenues. After that, they are required to achieve a CAGR of 12% over the next decade. As a result, in 2033, Hermes must earn €13 billion in net income, which is more than 2022 total revenues. After the first decade, to justify the valuation, Hermes would still be required to keep growing forever at a 6% annual rate, mandating the company to make €100 billion in profits by 2068.

Additionally, the dividend/buyback payout ratio used in the valuation model is 100%. Historically, Hermes has paid only around 40% of profits in dividends. However, as free cash flows align with net income, theoretically, they could have a 100% payout ratio. However, if they maintained only a 40% payout ratio and decided to hoard additional cash on the balance sheet, that would lower the net present value (as ROIC on reinvested dividends or buybacks is significantly higher than cash on a bank or short-term bonds). Additionally, this valuation model assumes that Hermes can maintain the record 30% net income margins forever.

If all of the above happens, the stock is fairly priced for an 8% annual return. Yes, 8%, not the 10x in 10 years, like investors enjoyed in the past decade.

{kind=link}

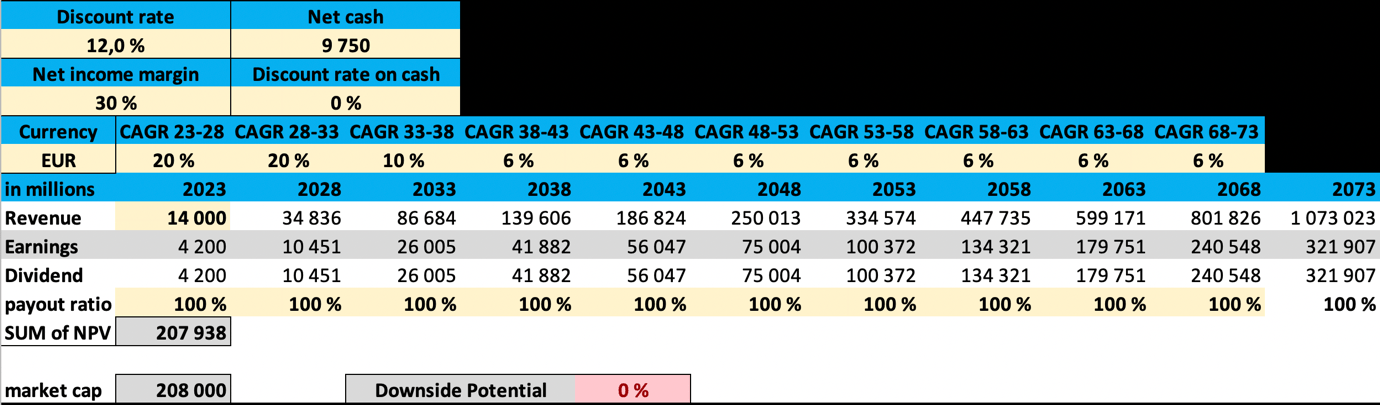

If investors demand a 12% annual return, the company must maintain a CAGR of 20% over the next decade. As a result, Hermes would need to make €26 billion in net income by 2033. Additionally, they would still need a CAGR of 10% over the next five years and then keep growing 6% annually forever after.

{kind=link}

However, if there is a recession and revenues either fall or slow down, and the CAGR over the next five years will be just 2%, then the next five years' revenue growth will be 10% instead of 12%, and the terminal growth rate is only 4% instead of 6%. Additionally, I assumed that the average net income margins would be 25% instead of the current record high of 30%. In that scenario, the net present value would be less than €90 billion, even if the required return for investors was only 8%.

{kind=link}

Upside risks

Maybe Hermes has infinite demand and pricing power and will keep growing at a 20% rate year over year. If they can maintain this high growth rate, the stock price will likely rise in line with the revenue growth rate. Additionally, even if the P/E multiple is already high, it's always possible that the market is willing to pay for an even higher multiple for the stock.

Even if the revenue growth would either slow down or decline, the stock price might not fall. Previously, there were times when the stock was expensive, but there was never a significant drop in the stock price. Instead, the stock stayed flat for a few years until the earnings caught up with the valuation, and the stock continued to rise afterward.

When shorting a stock, the downside is always unlimited, while the upside potential is limited.

Conclusion

Hermes has a beautiful business model, and it deserves a materially higher valuation than the rest of the stock market. However, the market might overestimate its ability to make constant price increases and them being recession-proof because a significant portion of sales goes to the middle-class or lower half of high-net-worth individuals. Given the high valuation, I don't see much upside potential from a fundamental perspective, and given the already significant market size of €200 billion, it is difficult for traders to move the stock up significantly. That being said, if Hermes can maintain high growth for a couple more years, it's possible to see the market cap being temporarily pushed to €300 or €400 billion, so keep in mind the portfolio exposure. However, I believe that shorting Hermes stock offers a nice 30% to 50% downside potential for a balanced long/short portfolio. Additionally, I'm long on some Chinese companies, so being short in Hermes, which is heavily exposed to the Chinese market, offers a decent hedge if any of the China-related risks will materialize.

For further details see:

Hermes Stock Upside Is Limited And Correction May Be Ahead