HESAF - Hermes: The Fast Uptick

Summary

- The French luxury giant, Hermes, has seen an impressive run-up in price in the last quarter. This is supported by sustained growth across markets and high margins.

- But the expectation of weak global growth, continued uncertainty about China and sustained inflation can tell on its revenues, even if its target market isn't always vulnerable to economic lows.

- Its P/E at 52x also makes it historically pricey, and predictions of a generally bearish year for the stock market can pull it down too.

Since I last put a Buy rating on the luxury fashion company Hermes ( HESAY ) in October 2022, its price has risen by 28%. Its price-to-earnings (P/E) ratio, which was already much higher compared to peers at the time, is now at an even higher 53.2x. For context, this is more than twice the P/E for the S&P 500 (SP500) index at 20x. With this as the backdrop, here I analyse Hermes with the following questions in mind:

- Why did the price rise so much?

- Is there a case for a further increase?

- What’s the next best course of action?

Exceptional upward momentum

One key reason for Hermes’ rise is the continued exceptional upward sales momentum since last year. Over the past 10 years, it has grown consistently, save in 2020 when the lockdowns were in effect. In 2021, it bounced back with a huge 41% growth. Even that could be chalked up to a positive base effect and the release of pent-up demand post-pandemic. The company, has, however, continued to prove its mettle even in 2022.

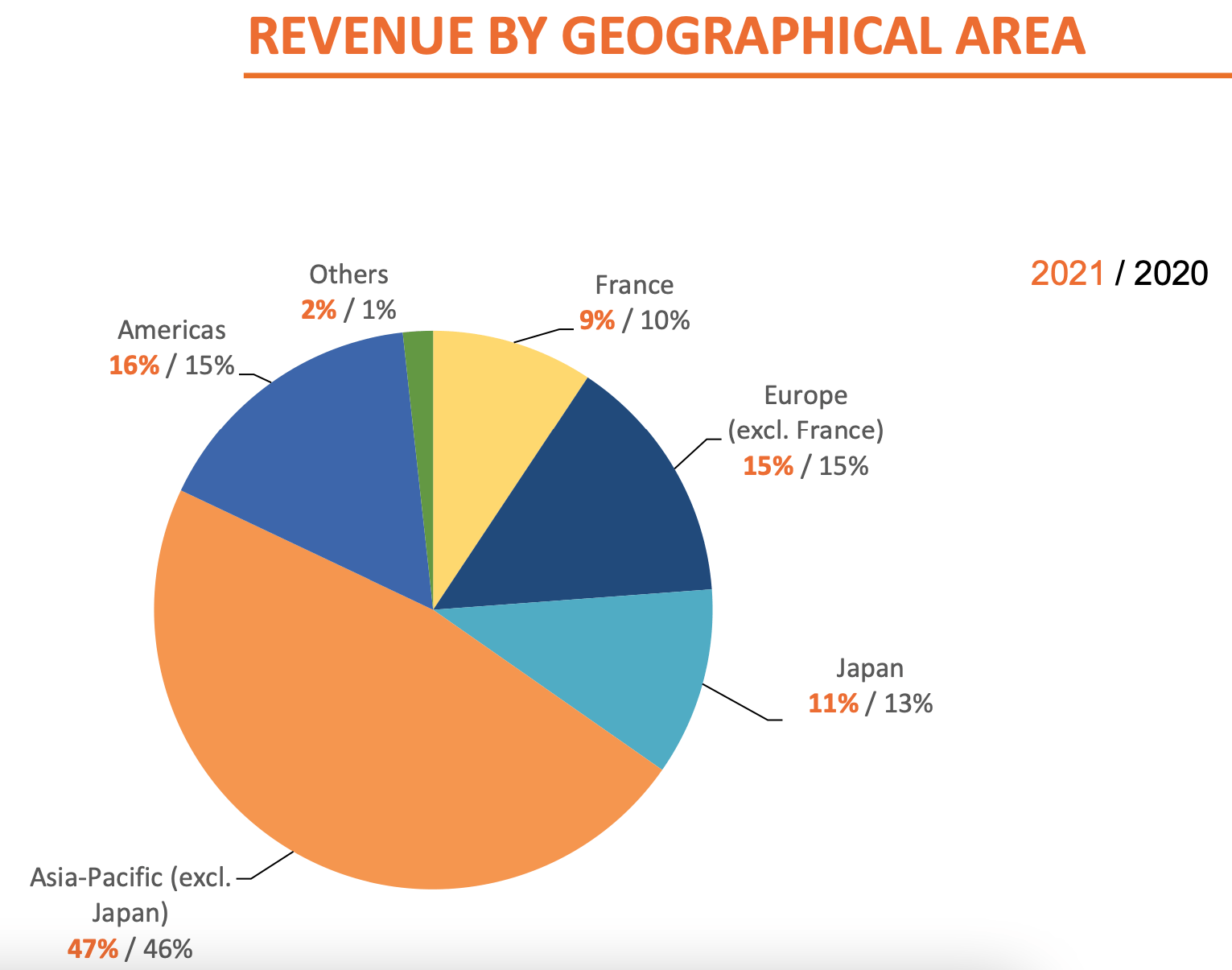

Its sales grew by 29% year-on-year (YoY) for the first half of the year. They continue to rise at a strong clip in the third quarter of the year, as per its last trading update released in late October, by 32.5% YoY. Even more notable is the growth across markets, both in terms of geographies and product segments. As far as geographies go, sales have risen most notably in the Americas and in France, but are at 20%+ rates elsewhere too.

Encouragingly, Asia ex-Japan sales came in stronger as China started recovering, though Hermes points to momentum in countries like Australia, Thailand, Korea and Singapore as well. The pickup in this market is particularly important since it accounts for 47% of the company’s revenues as of the full year 2021.

{kind=link}

How much further?

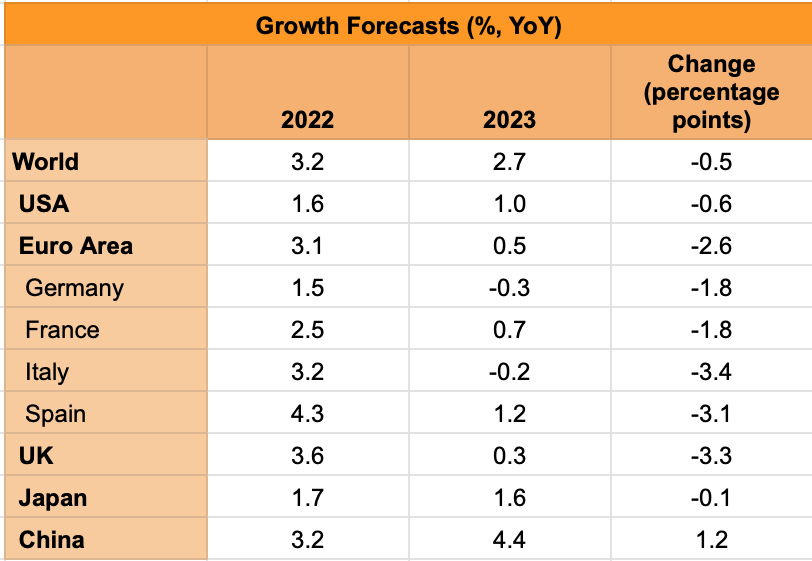

The big question, though, is whether Hermes can continue to rise. When I last wrote about it, my concern about the potential recession in big Western markets in 2023 was tempered by the hope for recovery in China, which according to the IMF is expected to grow by 4.4% next year.

However, the country’s situation is up in the air once again. It might have abandoned its zero-Covid policy, but coronavirus cases are on the rise. As per a recent Financial Times article on the country, the forecasts suggest “this winter wave would cause millions of deaths”. This is of course potentially bad news for companies that sell big in the market in any case. But if this is indeed the forecast, it’s hard to imagine the country remaining restriction-free either.

While banks’ forecasts for the Chinese economy were increasingly optimistic as it reopened, it’s also possible that these will be revised downwards as more clarity emerges. To condense the point into a takeaway, we can’t be sure of what happens next with China, so a growth impetus from the market can’t be taken as a given.

This brings us to other big markets of the developed West, which account for another 40% of Hermes’ sales. Global growth as such is expected to slow down to 2.7% as per the IMF from 3.2% in 2022 as inflation and interest rates stay high. But the extent of the drop is notable for these particular economies. Euro Area, for instance, is expected to grow by just 0.5% compared to 3.1% in 2022 as Germany and Italy fall into a mild recession (see table below). In sum, then, we are looking at a year ahead when 87% of the company’s markets are either uncertain or in a downright slowdown.

{kind=link}

Advantage luxury

Hermes ADRs aren’t without their advantages even now, though. One of the most attractive qualities of luxury companies is their high margin. And it sits right at the top of the list right now. With an operating margin of over 40%, the Birkin bag maker is far ahead of the next best, the Gucci owner Kering at 28%. This implies that even if its sales aren’t quite as buoyant next year as now, its earnings can still continue to stay firm.

It can, of course, be argued that sales might not be impacted significantly anyway since luxury goods’ consumers have enough financial cushion to weather through a bad economic climate. That said, in the past, the companies have in fact been impacted by recessionary conditions, so I wouldn’t take continue growth for granted.

Now, profits are a separate matter. As noted above, not only are its operating margins strong even now, but global inflation is expected to slow down to 6.5% this year from 8.8% in 2022. Hermes has seen some increase in costs recently, but with a better cost picture, its margins might just expand further.

What next?

It’s hard to overlook Hermes' high P/E ratio of 53x, though. Over the past 13 years, its median P/E has been at 42x, so it’s actually trading appreciably above the level. Can it rise higher still? Sure it can, in fact, the full-year results for 2022 will probably look quite good going by the first nine months’ numbers. And that release comes out only next month. Moreover, considering that its price is still down by 11% YoY, there could be some more steam left in the price.

But I doubt that 2023 will be the year when its P/E goes back up to the previous highs of 127x, going by the uncertainty around its key markets. Even if growth in China itself turns out well, just about any potential panic around it could drag the markets down. In any case, this is expected to be a poor year for the stock markets.

There’s no doubt that Hermes is a good investment for the medium or long term, something I noted in my last article on it. At the same time, it has run up really fast since October last year, and in the current environment, further price increases are hard to envisage. If I had bought it when I talked about it, I’d liquidate some of my holdings for a neat profit, but keep some invested for the longer term. In 2023, I reckon there could be opportunities to buy it on the dip.

For further details see:

Hermes: The Fast Uptick