LVMHF - Hermes: Unjustified Historically-High Premium Over LVMH

2023-07-01 22:20:56 ET

Summary

- Hermès has been a top-performing investment over the past five years, returning 273% through price appreciation and dividends, as the company showcased industry-leading operating margins, growth, and cash generation.

- Currently, Hermès trades at a historically high premium over LVMH, a company that is arguably of similar quality.

- I project that LVMH will outperform in the foreseeable future and estimate that Hermès currently trades 22.4% above fair value.

- However, I don't rate Hermès a Sell due to its ability to constantly surprise to the upside, and my expectation is it will continue to exceed analysts' estimates.

- Therefore, I rate Hermès a Hold and reiterate a Buy rating for LVMH.

Hermès ( OTCPK:HESAY ) ( OTCPK:HESAF ) has been one of the best investments in the market over the past 5 years, returning 273% to investors through price appreciation, dividends, and special dividends.

Unlike its closest luxury peer in LVMH ( OTCPK:LVMHF ), Hermès is deeply concentrated on the very high end of luxury, specifically with its leather goods products. The company caters to the extremely rich, the kind of customer that doesn't care about a recession and isn't sensitive to price increases.

Trading at a 53.3 P/E multiple on 2023's projected earnings, it's clear the market has very high expectations for the company and values it at a significant premium compared to LVMH, the only true comparable.

So, let's find out if that premium is justified.

---

With July approaching, almost every luxury house in the world is set to report its financial results for the first half of 2023. For those interested in reading previous articles I wrote about companies in the industry, here are the links:

- LVMH: 2023 Should Be Another Stellar Year, It's A Buy

- LVMH: Q1 Numbers Show No Sign Of Slowing Down

- Capri Holdings: It's A Value Trap, But A Likely Takeover Candidate

- Tapestry: It's Not Luxury, But It Is An Attractive Investment

I plan to write a pre and post-earnings article on every luxury house. Stay tuned.

Company Overview

Hermès primarily operates as a mono-brand worldwide. In addition to the Hermès brand, the group sells products under the John Lobb, Bucol, Crystal Saint-Louis, Puiforcat, LeGrin, Mètaphores, and Verel de Belval brands.

The house was founded in 1837 by Thierry Hermès, who sold luxury harnesses and saddles. Six generations later, the group is still run by members of the founder's family, led by Axel Dumas.

Today, Hermès employs 19,686 people, of which 7,000 are trained and certified craftsmen who make the company's products in a vertically integrated operation. There is no mass manufacturing here, Hermès produces its products categorized under 16 métiers (lines of business), with 76% of the production located in France. Most of the products are distributed through 300 stores owned and operated by Hermès, and the rest is sold through wholesale partners.

Geographic Presence

{kind=link}

Hermès 2022 Annual Report

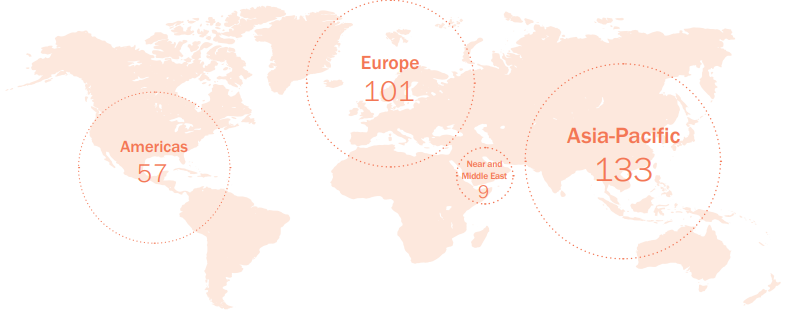

Of the group's 300 stores, 133 stores are located in Asia-Pacific, where Hermès generated almost 58.0% of its sales in 2022. For comparison, LVMH operates a total of 5,664 stores, 2,325 of which are located in Asia Pacific, where LVMH generated 37% of its sales in 2022.

Taking into account the fact that 2022 sales were affected by lockdowns in China, we understand that normal Asia exposure for both companies is even more significant, but for Hermès it is materially larger. For the near term, it means we should expect Hermès to be a slightly larger beneficiary of the China reopening. However, having a much smaller and much more concentrated group of customers, Hermès wasn't as affected by the China lockdowns as LVMH, so that's why I only expect slight outperformance in that geography.

Product Mix

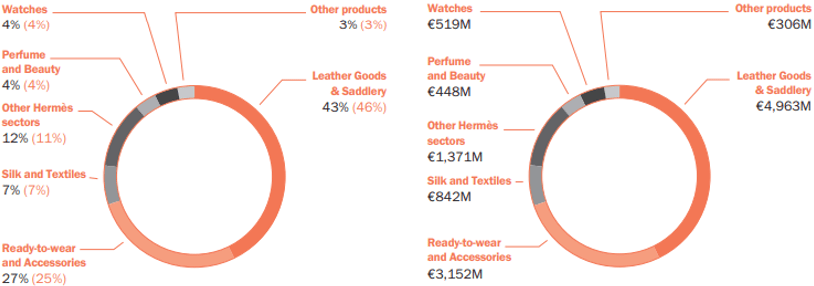

Hermès disaggregates its revenues into seven categories. The primary category is Leather Goods & Saddlery, consisting of the famous Birkin and Kelly bags, which are essentially ungettable to "normal" people. To get a viewpoint on just how hard it is to get a bag, here's a guide written by Vogue.

The second largest category is Ready-to-Wear and Accessories, which consists of men's and women's clothes and accessories including shoes, belts, hats, gloves, gadgets, and wearable jewelry.

Then we have smaller categories in Silk and Textiles, which consist mostly of scarves; Other Hermès Sectors which primarily comprise tableware and jewelry that isn't worn; Perfume & Beauty; Watches and-; Other Products, which are products sold by the non-Hermès brands.

{kind=link}

Hermès 2022 annual report

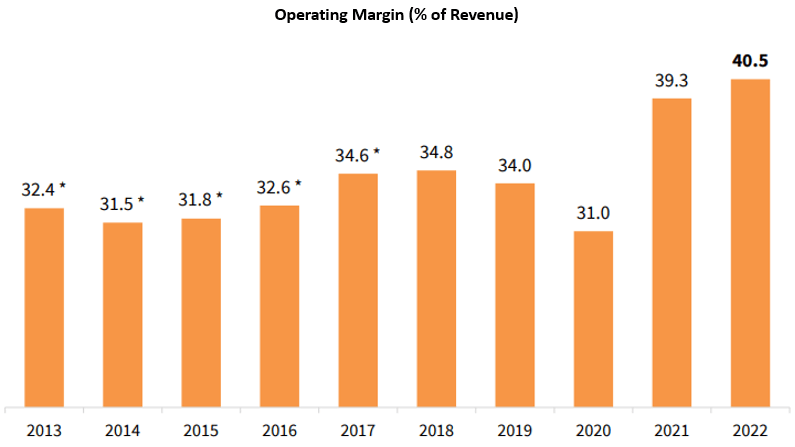

Unfortunately, Hermès doesn't provide us with a profit breakdown per product category. However, we do know that for LVMH, Fashion & Leather Goods is the most profitable segment, with a 40.5% operating margin in 2022. For LVMH, this segment is only 49.0% of sales, whereas for Hermès it's around 70.0% (depending on how much of the 27.0% in Ready-to-Wear and Accessories is attributed to jewelry). This explains the majority of the difference between Hermès' industry-leading operating margins of 40.5%, compared to LVMH's 26.7%.

Financial Performance

{kind=link}

Hermès 2022 Investor Presentation

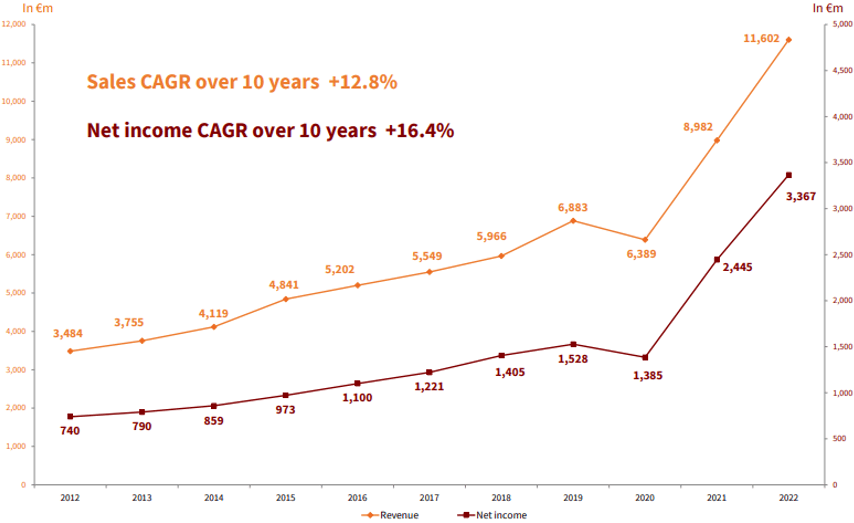

A graph that pretty much tells the whole story. Between 2012-2022, net income multiplied 4.5x, and unsurprisingly, the stock more than followed, multiplying by 6.9x. Growth in net income was primarily a result of revenue growth, combined with a significant margin expansion.

{kind=link}

Hermès 2022 Investor Presentation

Hermès Vs. LVMH

Covering most of the industry, you'll pretty quickly realize that there's Hermès, then there's LVMH, and then there are others like Kering ( OTCPK:PPRUY ) and Richemont ( OTCPK:CFRUY ). While those others trade at significantly lower valuations, they are incomparable to the two royals of luxury. Not in terms of growth, not in terms of margins, not in terms of future prospects, and not in terms of management quality.

In my view, there are only two alternatives for an investor who wants to get exposure to the true advantages of investing in luxury fashion, and those are, as you can understand by now, Hermès and LVMH. The only question that remains is which one is the better investment.

{kind=link}

Created and calculated by the author using data from the companies' financial reports; Data as of July 1st, 2023.

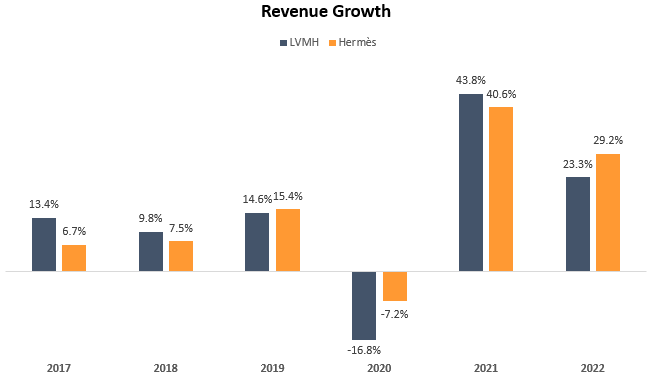

Beginning with revenue growth, Hermès is only marginally higher with a 14.3% CAGR between 2016-2022, compared to LVMH's 13.2%. However, LVMH outgrew Hermès in 3 out of those 7 years and came pretty close to Hermès in every year besides 2020. As I described in my LVMH articles, the company has much more exposure to Covid lockdowns due to its selective retailing (specifically Sephora) and travel businesses, so I wouldn't read too much into the 2020 performance.

Created and calculated by the author using data from the companies' financial reports; Data as of July 1st, 2023.

Continuing with operating margins, it's clear which is the more profitable business, with an average gap of 13.9% in favor of Hermès. In my view, this doesn't say much about the efficiency of the business, because as we discussed, LVMH derives 50% of its sales from less profitable categories. That being said, it means the gap isn't closing any time soon, and thus, each incremental Euro Hermès generates is more valuable.

{kind=link}

Created and calculated by the author using data from the companies' financial reports; Data as of July 1st, 2023.

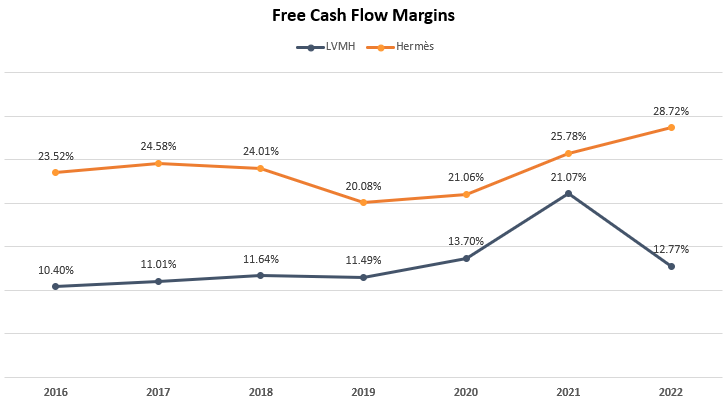

A similar story is told by the free cash flow margins of the two, with an average gap of 10.8% in favor of Hermès. As you can see, the average takes into account 2022, a year in which LVMH had a one-time drop in OCF margins due to inventory buildup and non-recurring tax installments, as well as increased capex spending for operating properties which are yet to yield return.

Before that, LVMH has been consistently narrowing the gap, and we can expect that as soon as this year, we'll see the gap return into the 4%-6% range. Over time, I think it's not improbable that LVMH will be able to leverage its scale into surpassing Hermès's FCF margins. Not in the near future, but definitely possible in the 5-year horizon.

Is Hermès' Premium Justified?

In the past, Hermès has always traded for a significantly higher multiple than LVMH, with the former's median multiple at 42.1 compared to the latter's 24.7. So by their respective medians, Hermès was historically valued at a 70% premium. Today, the gap is much wider.

Looking at their GAAP P/Es (2022), Hermès is at 62.4 compared to LVMH at 29.6 (ignore the graph above, which is affected by the USD/EUR exchange rate, it's here to demonstrate the overall trend). Based on current consensus estimates for 2023, LVMH is trading at a P/E of 26.0 and Hermès is at 53.3. Based on my estimates for 2023, LVMH is at 25.2 and Hermès is at 51.6.

The bottom line is Hermès is getting a 100% premium compared to the historical 70% premium. As I said, both I and the market expect Hermès to continue to outperform LVMH in 2023, but I don't think that justifies additional 30 percentage points over the historical premium.

For the near term, Hermès should benefit from its concentrated product mix and higher exposure to Asia Pacific, but over time, I think LVMH will provide steadier growth and could surpass Hermès in FCF margins. Thus, I find the current historically high premium unjustified.

Valuation

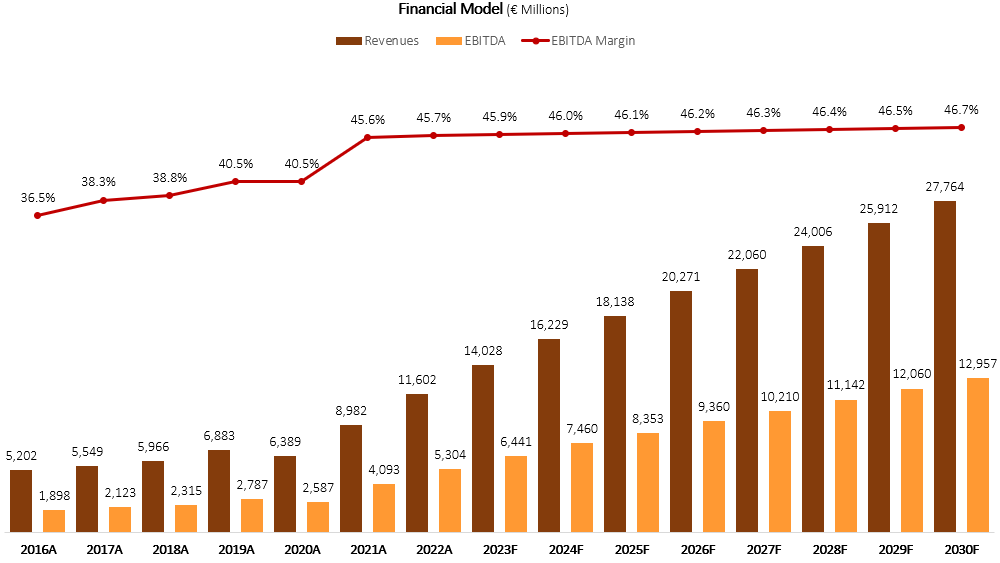

I used a discounted cash flow methodology to evaluate Hermès' fair value. I forecast Hermès will grow revenues at a 10.2% CAGR between 2023-2030. I estimate revenues will grow at this pace due to constant price increases, continued store openings, entry into new segments, recovery in China, and steady organic growth.

I project EBITDA margins will increase incrementally up to 46.7% in 2030. In my view, this is a reasonable projection as the company is constantly able to improve margins, but on the other hand, it's expanding lines of business that are less profitable.

{kind=link}

Created and calculated by the author using data from Hermès financial reports.

Taking a WACC of 7.3% and adding its net cash position, I estimate Hermès' fair value at €1,544 per share, which amounts to $1,675 per HESAF ADR based on the current USD/EUR ratio. This represents a 22.4% downside compared to the market price at the time of writing.

While this is a significant downside, I don't rate Hermès a sell, as the company is of such high quality that it seems every time investors think it's overvalued it will surprise them to the upside. Moreover, as we discussed in my previous LVMH articles, consensus estimates are typically way off when it comes to European companies, and I definitely project Hermès will beat expectations in the near term.

With immense dividend growth, no debt, and huge room for expansion, I estimate investors who continue to hold will be just fine.

Conclusion

Hermès is probably one of the best businesses in the world, appealing to the most resilient customer cohort there is. From royal families to worldwide celebrities, the demand for its luxury status-signaling products is endless, with full waiting lists years in advance.

Unfortunately, the company trades at a premium that I can't ignore. Typically, I don't mind buying companies at what is an objectively high multiple, as exceptional quality doesn't come cheap, and I seek to invest in companies for the very long term. However, Hermès is currently too rich even for my taste. When I compare it to LVMH, arguably a company with a similar or close-to-similar quality, I deem the premium unjustified and find LVMH as highly likely to outperform in the foreseeable future.

Thus, I rate Hermès stock a Hold and reiterate a Buy rating for LVMH.

For further details see:

Hermes: Unjustified Historically-High Premium Over LVMH