HESAF - Hermes: Why I Think It's The Best Company In The World

2023-08-17 09:44:09 ET

Summary

- Hermès is a French company founded in 1837 that initially made harnesses for the French nobility.

- The company expanded its catalogue to include saddles.

- Thierry Hermès is credited with establishing the company.

Hermès (HESAY) is a French company that was established as such in the year 1837 thanks to the work of Thierry Hermès. The company began by making harnesses for the French nobility and high aristocracy, and later introduced saddles to its catalogue. The company expanded then its offering they became the purveyors of articles to many European royal families, such as the Tsar of Russia. At the beginning of the 20th century, the company initiated the manufacturing of apparel and other complements, which again broadened the range of products that the company sold. The company has survived to 7 generations of the family Hermes-Dumas and it has proven how resilient it can be to all sort of economic cycles.

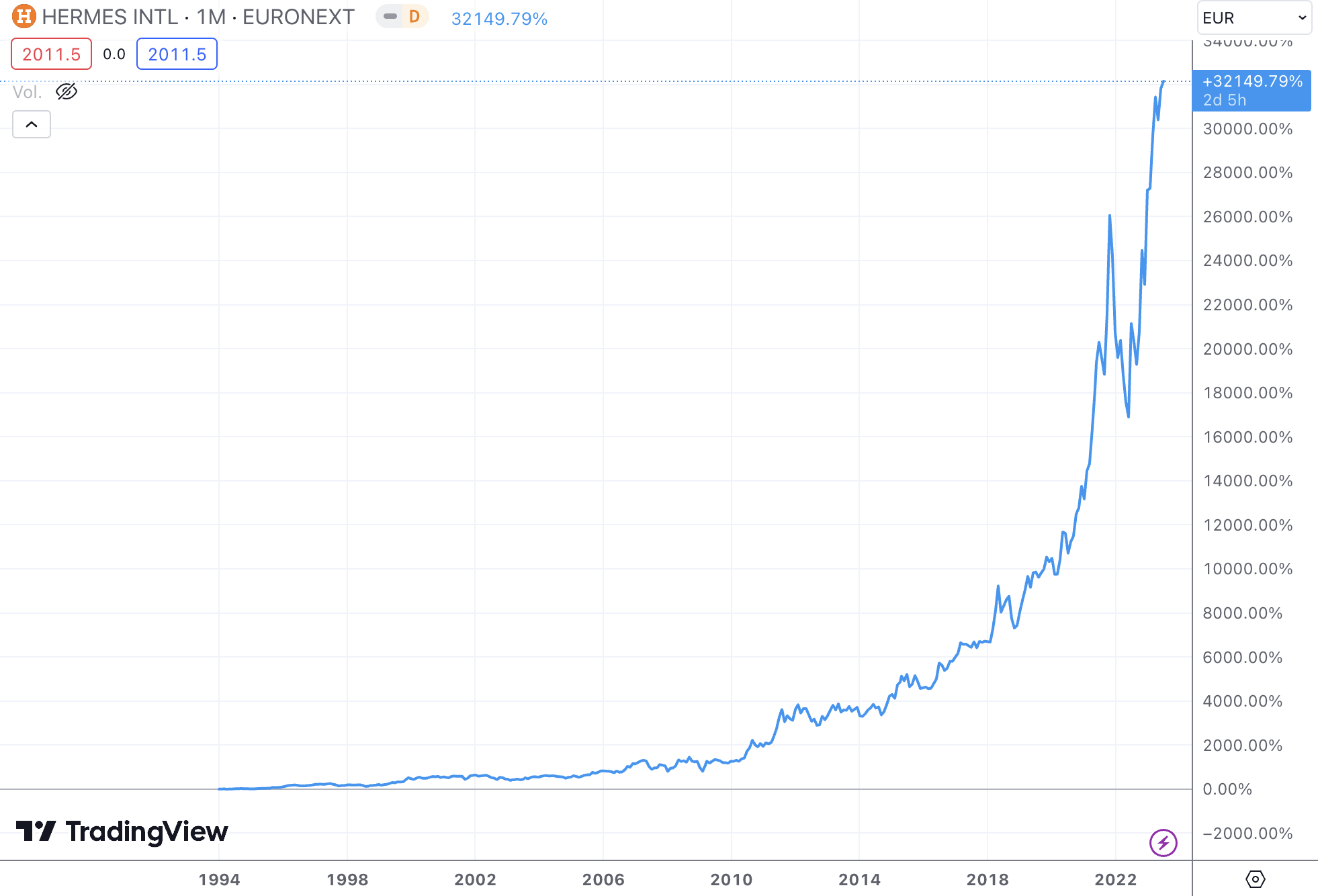

Hermes Total Returns (tradingview.com)

{kind=link}

Business description and company culture

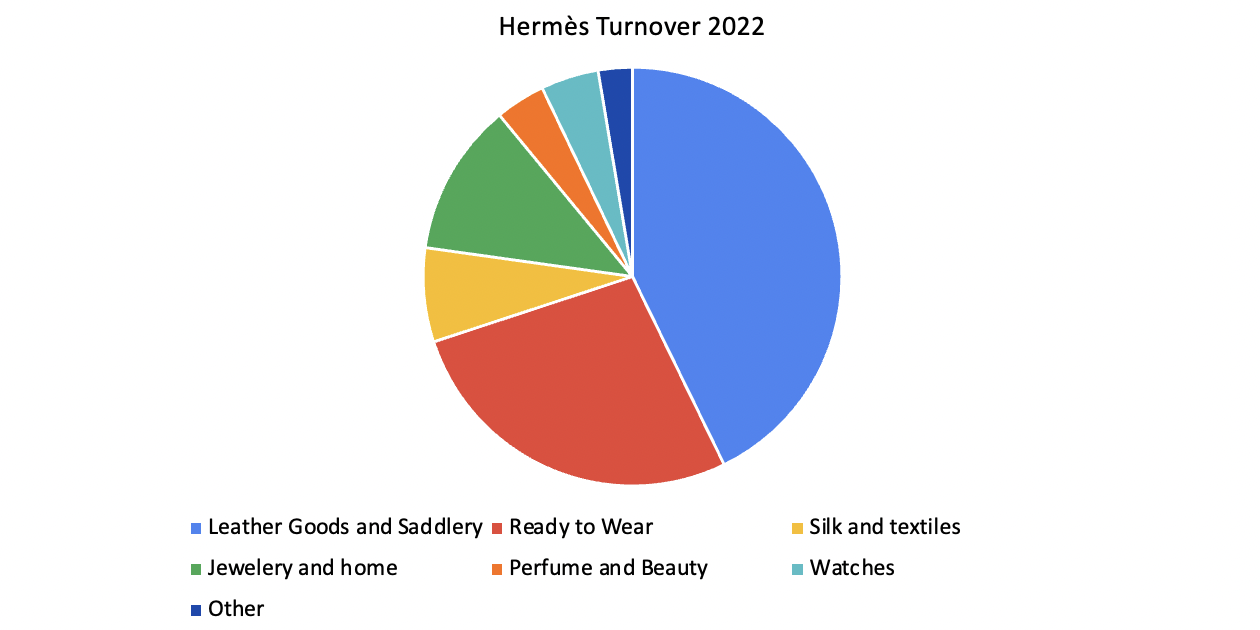

Hermès is a quality company focused on excellence and differentiation. This definition is consistent with the products they manufacture, always focused on maximum customer satisfaction and providing differentiation from other goods sold on the market. The company segments its sales into several categories, although the bulk of revenue is made up of the Leather goods and Ready-to-Wear accessories segments. Other segments such as Perfume, Silk and Beauty, Watches and Other make up the remaining part of the turnover. In 2022, the amount of revenue per segment was the following:

Hermès turnover (2022) (Own Model)

{kind=link}

Almost 50% of the revenue consists of leather goods, which includes famous fashion complements such as the Birkin bag. As an anecdote, the most expensive Birkin bag ever sold was a Himalaya 35, which fetched $500,000 at an auction in 2019 . Another important part of the revenue comes from new verticals which they began to explore years ago, such as watches, jewelry and silk products. The most cyclical part of the company is the discretionary segment of Perfume and Beauty, where they face intense competition from other luxury companies such as LVMH (LVMUY), Kering (PPRUY) and even L'Oréal (LRLCY). Luckily, this part represents a small fraction of total turnover and does not affect greatly the financial performance in aggregate.

This company is probably way different than any other company that the reader might have heard of. Its unique production structure and vertical integration make the company a fascinating object of study. Hermès is known to have high gross margins, which have oscillated between 65-70% in the last 20 years. This indicates a high degree of vertical integration and a cost-optimized structure that allows the company to have control over production, hence reducing the risk of depending on key suppliers that may alter the production process in case of incidences. Hermès is also known to have an extraordinary entrepreneurial culture which I think is a guarantee of quality of the products they manufacture for their clients.

Hermès has long-standing relations of excellence with its suppliers and partners for loyalty and high demand in quality, maintaining unique quality of Hermès objects, training know-how, dedicated workshops.

The previous quote can be found here . A substantial difference with other peer companies (although I doubt that Hermès has really a directly comparable peer) is the attention they pay at workshops and craftsmen. I want to stress that not anyone can be recruited into Hermes' workforce, so an intense recruitment process must be followed in order to belong to the corps of artisans of the company. First of all, the company selects candidates and through a program of 18 months each pupil is assigned to a tutor to learn the techniques of leather treatment and transforming paper designs into reality. After that, the pupil becomes an official and after some years of experience acquires the rank of artisan.

In addition to this, the company also has incentive programs to maintain the loyalty of employees and encourage their long term presence in the company. In a recent press release, the company announced a free share distribution plan plus extra cash remuneration for workers. I believe this philosophy of maintaining happy employees translates into a better customer service and hence an increased satisfaction that results in better reviews and a positive shopping experience.

Another key to Hermès success is the high level of decentralization that has governed in the company since its creation almost two centuries ago. The company, although vertically structured to reduce costs, has always been characterized by the high level of freedom that gave not only to métiers (the designers of products) but also to artisans, who are responsible from beginning to end of the product they manufacture. This attitude clearly favors the company's adaptation to local markets (and increases customer satisfaction) but also makes the artisans responsible of their work and also responsible in maintaining the brand reputation. As they usually say:

Learning a craft and not a task. Never stop learning.

If I had to define the enterprising culture at Hermès I would say that quality is what they focus on. A culture built around quality where the CEO, the management team, the métiers and the artisans work rowing in the same direction towards a common goal: put the customer in the center and produce the quality goods they demand.

Management team

Another key point to understand Hermes' success is the outstanding management team that has been leading the company for years. More than 6 generations of the Hermès-Dumas family have lead the business through bright and turbulent periods, and yet the company has managed to survive. The company had some difficult times in the 70s where it pursued an aggressive and expansive policy that resulted in some store closures. After those disastrous events, the management team reconsidered, paused the expansion and continued doing things as they had been doing them for the past century. In the following years, the company decreased Hermès franchises and increased company-owned stores to better control sales of its products.

As Charlie Munger always says: show me the incentives and I will tell you the outcome . The Hermès-Dumas family controls 66.7% of the circulating shares and exercises at the same time the management and investing guidance in the company. Investors should understand that the fate of the family is tied to that of the company. This is, in order to preserve their wealth and make it grow, the company must thrive and continue generating cash flows that will be re-invested and also distributed to shareholders. I believe there is no better sign of alignment with long term shareholders than the patrimonial view that the Hermès-Dumas family has.

Financial data and capital allocation

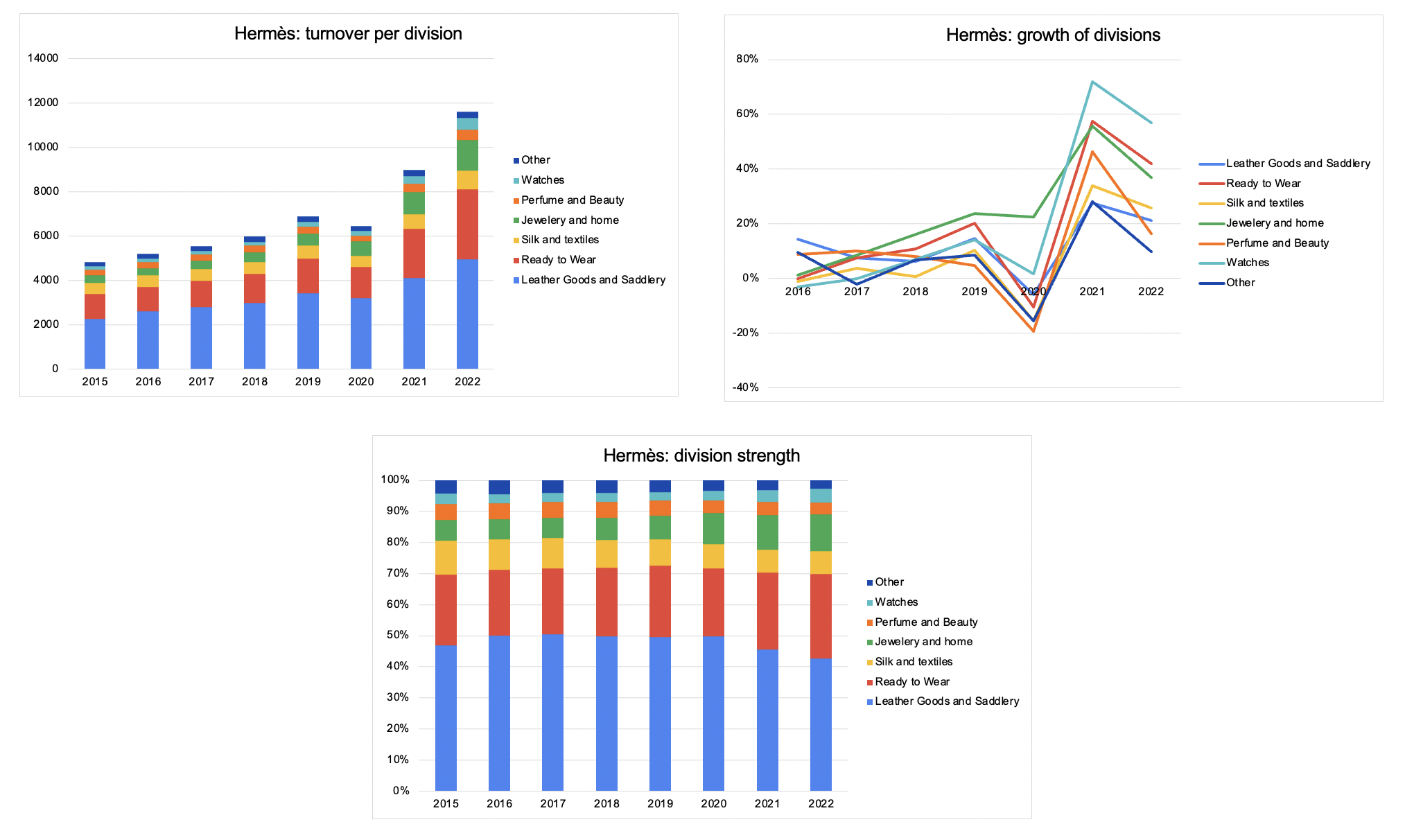

Performing an extensive analysis on financial data provided by the company can be useful to understand which segments are most profitable and more resistant to economic cycles. In this article I present the evolution of yearly sales, their yearly growth and also how sales are distributed across different segments.

Hermès revenue growth (Own models)

{kind=link}

The previous figure shows how revenues have more than doubled over the last years and the dominant segments of the brand are Leather and Ready to Wear Accessories. In addition, one can also see the evolution of sales of the different segments and how sensible they are to the economic cycle. Even in an economic recession (supply shock of 2020) the company had a low drop in sales and performed 'relatively nice' taking into account that the bulk of their stores were closed for a relatively long period of time.

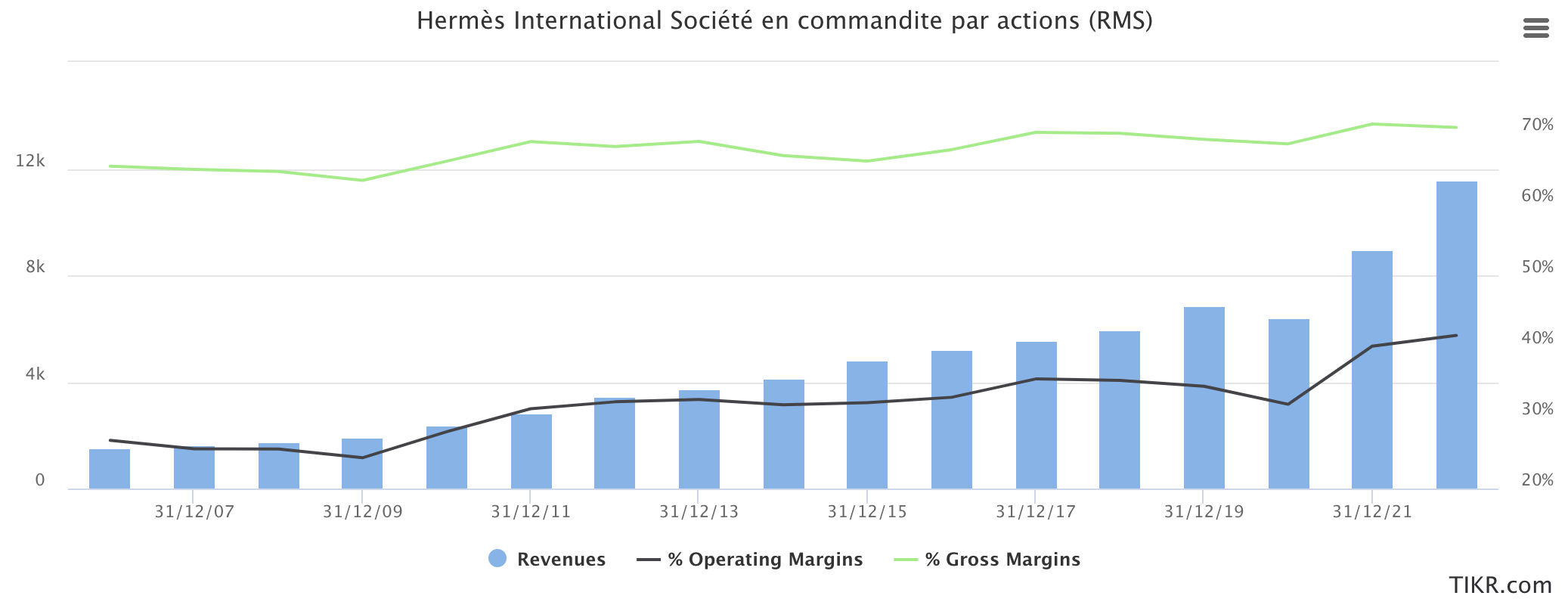

Gross margins and operating margins (%) (Tikr.com)

{kind=link}

The previous figure shows how well vertical integration and cost control have been done at Hermès for almost 20 years. Gross margins have never dropped below 65% and operating improvements and reduction in marketing spending have helped boost profit margins for the company. This has clearly led earnings per share to grow at faster rates than revenue growth and has also resulted in outstanding generation of value for shareholders.

Another key point in assessing a company is how deep its moat is. This can be done using a combination of quantitative and qualitative factors. The latter include aspects such as business culture, management excellence and long term view. The quantitative aspect of this translates into ROIC, which is quite high since the capital base grows less than the profits the company generates. Its current return on capital adds to 33%, and the company has been able to maintain it and expand it in the last years. Being able to maintain and grow the returns on capital shows indeed how profound the moat is.

The company has also a very disciplined policy when it comes to debt management. The current net debt position is negative, hence they have accumulated more cash than debt and their interest coverage is high. There is almost zero risk regarding the financial position of Hermès.

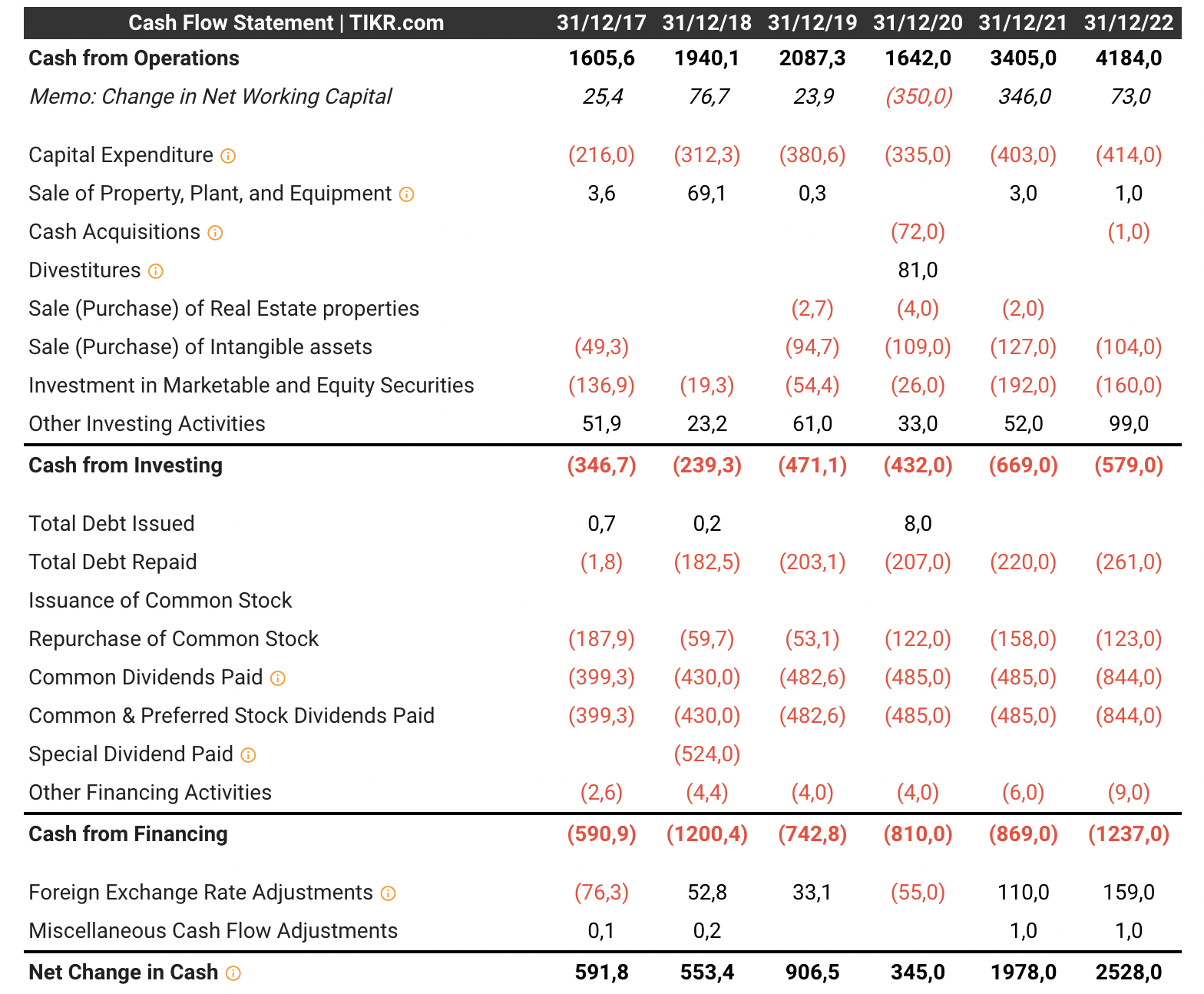

Another thing at which Hermès is superb at is everything related to capital allocation. The company has effectively identified growth opportunities and has expanded its production capacity to meet customer requirements whilst maintaining quality of its products, and in addition it has been very disciplined with shareholder remuneration policies such as dividends and share repurchases. The company has wisely modulated share repurchases being sensitive to valuation and has also increased remuneration to shareholders via an increasing dividend policy. These two points clearly transmit serenity and a reasonable and sensible approach towards what a disciplined capital allocation policy should be.

Hermès' capital allocation policy (Tikr.com)

{kind=link}

The aforementioned points can be seen in the previous table, where the reader can see where Hermès has allocated capital over the last 5 years.

Valuation

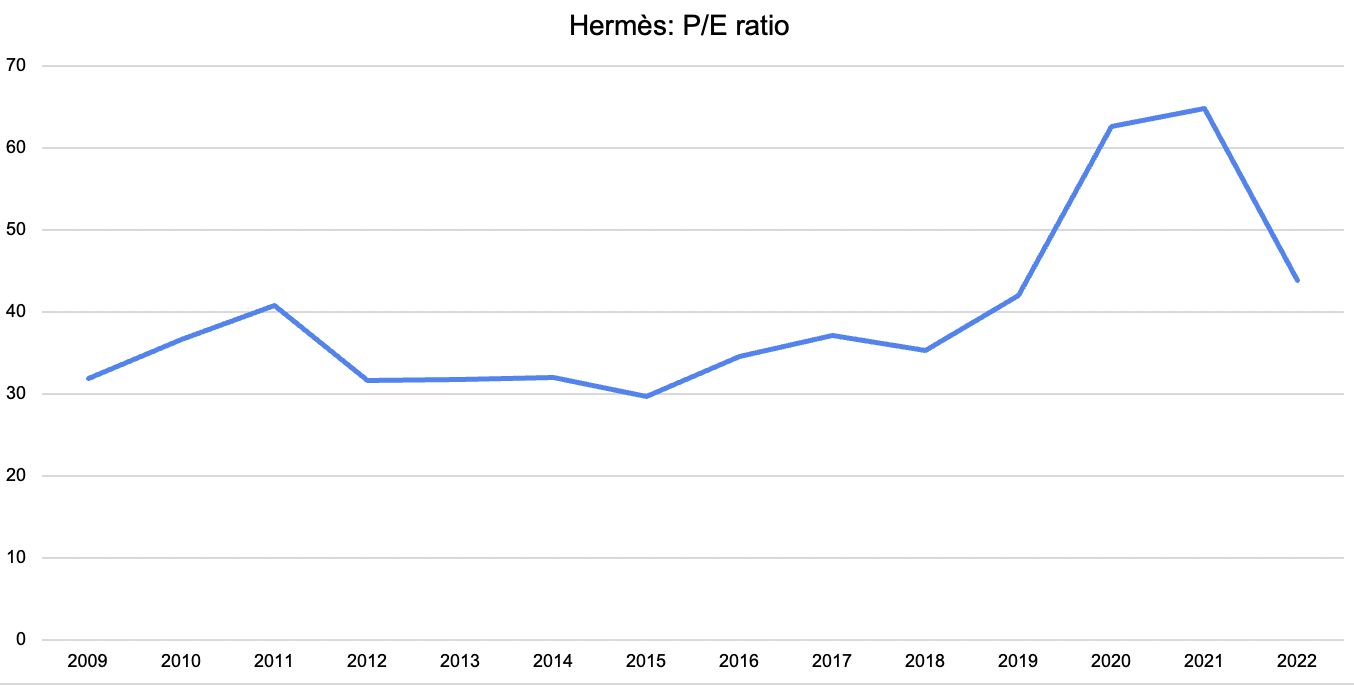

Determining the value of a company is often a hard task for investors. Misguided by the wrongly used concept of margin of safety, many believe that they must buy undervalued businesses to generate excess returns compared to the market. This may be true sometimes, but I believe that it is better to buy extraordinary businesses at decent prices than decent businesses at extraordinary prices. Currently there is too much focus on ratios such as P/E, whilst other important concepts such as terminal risk and business culture tend to be generally disregarded and not looked upon. Something of the sort happens with Hermès when people don't simply look at it because "it has a really high P/E ratio".

{kind=link}

The graph above shows the evolution of the P/E of the company over the last 13 years. In this long time period, the company never really dropped below 30x its earnings. The average investor would have argued that the company has never been cheap. The earnings yield at which it was trading was around 3% on average, a pretty low number compared to the rest of the market. Even though the company was never "cheap" according to pure value investors, its earnings per share increased at a rate of 21% in this period, whilst shares appreciated in price 24%. Looking only at the P/E ratio would have made you lose the opportunity of multiplying your investment by 16.4 times on 13 years. If this example is not enough to show that P/E ratios are not all that matters, I invite the readers to provide me with a counterexample or more solid arguments on why we should only assess valuation based on an arbitrary number.

Valuation is more than looking at a number called P/E ratio because it is a dynamic process, not a static one. Businesses change and hence value changes with them. Terminal value is always what matters most. Because the vast majority of value that the companies will generate is in the future, and hence investors must evaluate whether this is at threat.

Since Hermès' reinvestment rate is on average around 15-20% of its operating cash flow and its return on capital (since it doesn't use any debt) is around 40%, we can estimate growth in earnings in the range of 8% in the long term. Based on the recent half year results that the company has presented, I believe that this estimates will be a bit conservative, but this can be a margin of safety to consider. In this conservative scenario, where margins would stay around 38%, terminal growth around 5% and a return rate of 10%, a DCF yields a value of approximately €1400 per share. In a more optimistic situation where growth could be sustained in the coming years at 10-12% and margins around 40% (maintaining the same terminal growth rate and return rate) the value would be close to €1600. A normal valuation range to get returns in the low teens for the long term would be around €1400-1600. Current price implies higher expected growth than this model and would yield in IRR of 8%, a number below my long term goal of achieving returns higher than 10% in the long term.

For further details see:

Hermes: Why I Think It's The Best Company In The World