HRTX - Heron Therapeutics Gets Back On Track

2023-12-29 15:14:25 ET

Summary

- HRTX's Zynrelef sales are back on track, with potential for significant growth pending approval of a supplemental New Drug Application.

- Aponvie sales have been underwhelming thus far and probably won't contribute much to HRTX's revenues in the near term.

- HRTX's financials show a net loss in Q3'23, but the completion of restructuring brings optimism for future profitability.

In July, I wrote about Heron Therapeutics ( HRTX ) noting that restructuring could bring about a new dawn for the company. I rated HRTX a buy based on the potential of its recently launched Aponvie, the potential for Zynrelef sales growth, and the company's push towards profitability with restructuring and new management. This article takes a look at where those drugs stand now, and the company's updated financials.

Figure 1: Year-to-date trading of HRTX, Q3'23 earnings have brought the stock well off the lows.

Zynrelef back on track, Aponvie doesn't excite

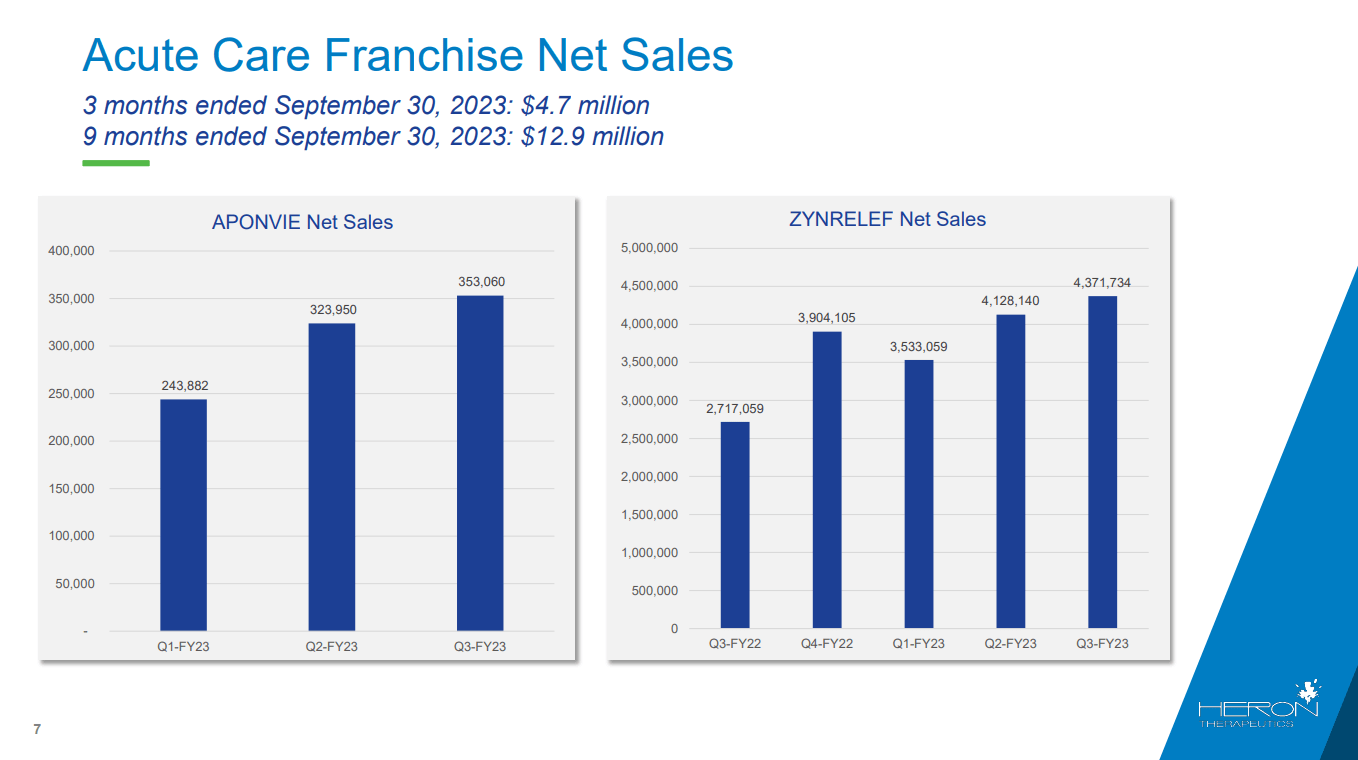

In my July article on HRTX, I noted a dip in quarterly net sales of Zynrelef (bupivacaine/meloxicam injection for post-surgical pain) in Q2'23 to $3.5M. With Q2'23 ($4.1M) and Q3'23 ( $4.4M ) net sales resuming a growth trend for HRTX, one of the main potential drivers of revenue growth is back on track.

Figure 2: Aponvie and Zynrelef net sales by quarter. (HRTX Q3'23 earnings call presentation.)

{kind=link}

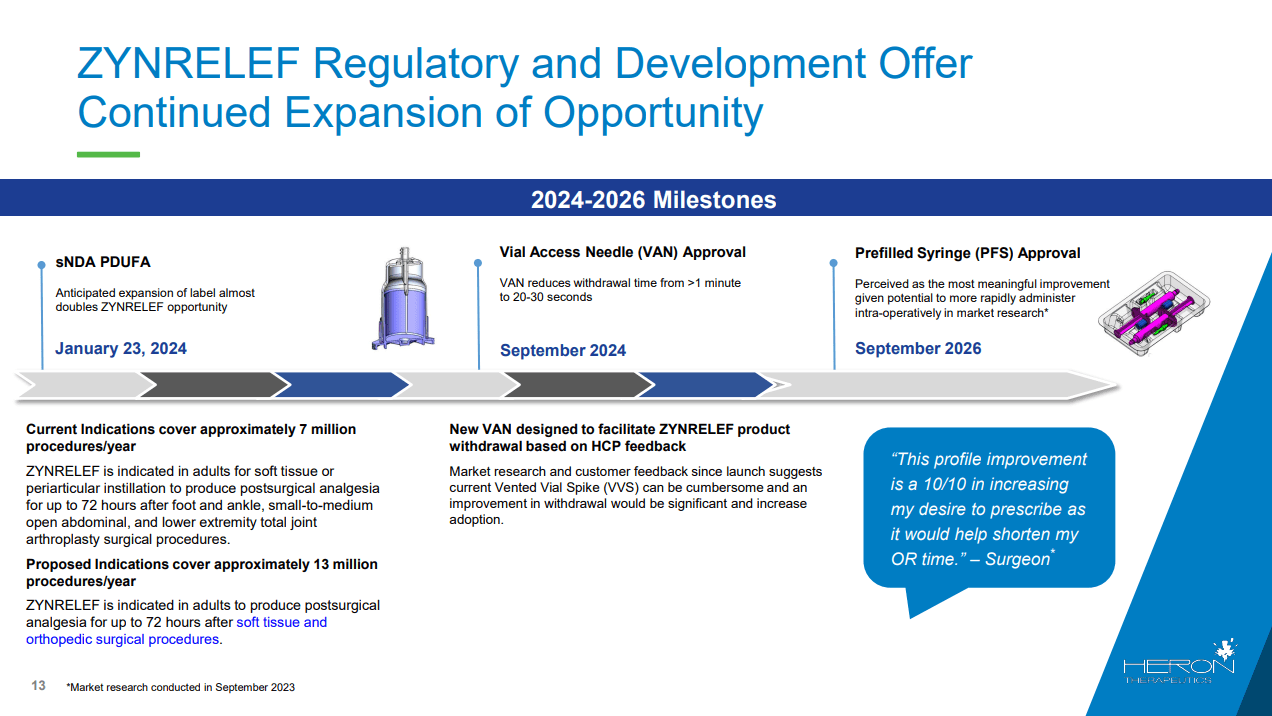

Of course, a more substantial growth in revenue, perhaps a doubling, remains tied to approval of HRTX's supplemental New Drug Application (sNDA). If approved, that sNDA would allow for Zynrelef to be used in almost twice as many surgical procedures and so we could see Zynrelef brining in about $8M a quarter. The sNDA has a Prescription Drug User Fee Act (PDUFA) goal date of January 23, 2024, and so provides a near-term catalyst for HRTX.

Beyond the sNDA, HRTX still has the potential to make Zynrelef easier to use, with a vial access needle, and eventually a pre-filled syringe. HRTX currently expects to launch the vial access needle in Q3'24, but has to first submit a Prior Approval Supplement, which it plans to do in early 2024, according to its Q3'23 earnings release.

Figure 3: Zynrelef sNDA, vial access needle and prefilled syringe. (HRTX Q3'23 earnings call presentation.)

{kind=link}

Regarding Aponvie (aprepitant emulsion for post-operative nausea and vomiting), while the drug only became available in March, the first few quarters of sales don't impress. I can't see that the drug will be adding meaningful revenues to HRTX's top line in the near-term. There are a few slides in HRTX's Q3'23 earnings call presentation showing growth in the number of accounts ordering Aponvie, including beyond the end of Q3'23. For example, there were 156 ordering accounts as of October, compared to 145 in September, up from just 18 in March when the drug launched. Perhaps then we can expect growth in Q4'23 relative to Q3'23, but nothing groundbreaking.

Financial Overview

HRTX reported net product sales of $31.4M in Q3'23; $23.3M coming from Cinvanti, $3.4M from Sustol, $0.3M from Aponvie and $4.4M from Zynrelef. R&D expenses were $13.6M in Q3'23, G&A expenses were $11.6M and S&M expenses were $13.0M. HRTX reported a net loss of $25M for Q3'23, although these numbers were influenced by a one-time inventory write off of $7.5M and $4.1M in severance and reorganization costs as HRTX nears completion of its restructuring. Indeed, Q3'23 earnings produced a bottom in the stock which has now rallied.

In just six months of initiating our corporate restructuring plan, I am pleased to announce its near completion. The enhanced clarity in our sales projections and operational visibility brings optimism for our path to profitability.

Craig Collard, CEO, HRTX, Q3'23 earnings press release .

Regarding those sales projections, HRTX is currently guiding to full year 2023 net product sales of $123M-$125M, whereas full year 2024 net product sales of $138M-$158M. The bottom end of that 2024 guidance would represent just 11% growth from 2023, which isn't that impressive for a company with a newly launched drug (Aponvie) and an expanding label on another drug (Zynrelef). At the same time, the oncology care franchise (Sustol and Cinvanti) bring in most of the revenues, and HRTX is only guiding for 3%-5% growth in 2024 relative to 2023.

HRTX finished Q3'23 with $77.4M in cash, cash equivalents and short-term investments. HRTX drew $25M under a new loan agreement with Hercules Capital which HRTX entered on August 9, 2023. As such, there is $24M of non-current notes payable on the balance sheet as of September 30, 2023.

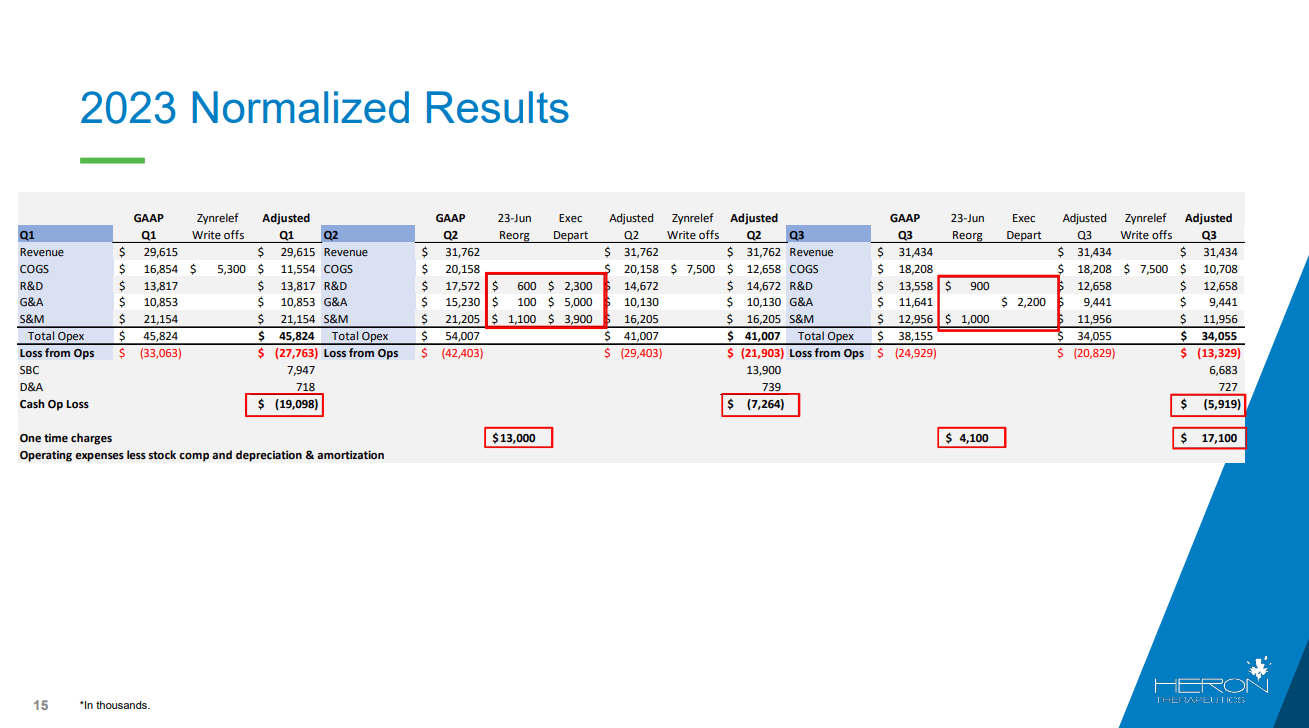

HRTX believes the company has sufficient capital as is to achieve profitability, which would mean further dilution from an offering wouldn't be required. Indeed, the company's goal seems possible. Firstly, HRTX is guiding towards completing 2023 with at least $65M in cash, cash equivalents and short-term investments and has the ability to draw a further $25M under the Hercules loan agreement. Secondly, HRTX provides a table in its Q3'23 earnings presentation noting adjusted loss from operations of $13.3M when removing the Zynrelef write-off of $7.5M and $4.4M worth of costs associated with reorganization and executive departures. Taking out non-cash items of $6.7M of stock-based compensation and $0.7M of depreciation and amortization, HRTX arrives at an adjusted cash operating loss of $5.9M for Q3'23.

Figure 4: Normalized results by quarter, adjusting for one-time charges, Zynrelef write offs and non-cash items. (HRTX Q3'23 earnings call presentation.)

{kind=link}

You can see on the slide that our operation loss after excluding stock compensation and depreciation and amortization and the previously mentioned one-time charges our overall operating cash burn decreased from $19 million in Q1 2023 to $7.2 million in Q2 2023 and $6 million in Q3 2023.

Ira Durate, Executive Vice President, CFO, HRTX, Q3'23 earnings call .

Now the adjustments certainly do a lot of heavy lifting in making HRTX's loss appear to narrow, but I think HRTX's guidance of no future large Zynrelef write-offs is likely to be correct, and the major restructuring costs should be out of the way as the restructuring is "near completion." With an operating cash burn of $6M in the most recent quarter (notwithstanding the aforementioned adjustments), down from $7.2M in Q2'23 and $19.1M in Q1'23, revenues continuing to grow and margins increasing, HRTX could indeed reach profitability without needing to raise again.

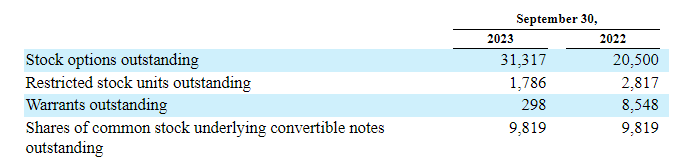

HRTX also has a further $149.4M worth of non-current convertible notes payable on the balance sheet, but these convertible notes only bear interest at 1.5% per annum, so aren't costing HRTX much right now, and have a conversion rate of 65.4620 shares per $1000 of notes (equivalent to a conversion price of $15.276 per share). Those convertible notes come from a May 2021 private placement with the $15.276 conversion price representing a 13% premium to HRTX's share price at the time. If all $150M worth of notes were converted today at the initial conversion rate of 65.4620 shares per $1000 of notes, it would result in 9,819,300 shares of dilution to HRTX's shares outstanding. Right now 10M shares of HRTX is worth about $16.7M, so it seems HRTX ended up getting a very good deal with the convertible notes, unless the stock rallies substantially between now and their maturity on May 26, 2026.

There were 150,072,640 shares of HRTX's common stock outstanding on November 10, 2023, giving the company a market cap of $250.6M. There were also a further 31,316,981 options outstanding at September 30, 2023, with a weighted-average exercise price of $8.88 per share.

Figure 5: Screenshot of table outlining outstanding options, shares associated with convertible notes, RSUs and warrants. (HRTX 10-Q)

{kind=link}

Rating

The low end of HRTX's 2024 guidance for net product sales ($138M) has the company trading at 1.8 forward sales. I think the potential for the Zynrelef sNDA to be approved, which I expect, serves as a near-term catalyst for the company. Further, the company is nearing the completion of restructuring, and not expecting additional inventory write-offs should help narrow the net loss, proving the company is on the way to profitability in the future. Considering these factors, I rate HRTX a buy.

Risks

Firstly, an obvious risk to the thesis is that if the Zynrelef sNDA isn't approved, the company will be reliant on underlying sales growth in the currently approved surgeries, and eventually in September 2024, the vial access needle could help sales.

A second risk is that beyond Zynrelef, while sales of the oncology franchise drugs, Sustol and Cinvanti aren't the main growth drivers, they bring in more net product sales in absolute terms. As such even if HRTX is only guiding the oncology franchise to grow by 3-5% in 2024 a few percentage points of underperformance there could offset gains in Zynrelef sales.

Lastly, HRTX's products can and do come under threat from potential generic competition which results in patent infringement suits. HRTX previously noted a favorable outcome in the Markman hearing from its case against Fresenius Kabi, who seek to launch a generic Cinvanti. HRTX's 10-Q notes a five day bench trial scheduled for June 24, 2024, which at least allows the company to get to the Zynrelef PDUFA date first.

For further details see:

Heron Therapeutics Gets Back On Track