SVC - Hersha Hospitality: A Buyout Is A Good Time To Cash Out

2023-08-29 13:02:15 ET

Summary

- KSL Capital Partners has agreed to acquire Hersha Hospitality Trust in an all-cash deal valuing the company at around $1.4 billion.

- The deal offers significant immediate upside for common shareholders and preferred stockholders.

- Hersha Hospitality Trust has shown an impressive recovery and growth, but recent signs of weakness and asset sales have impacted revenue and profits.

- All things considered, this deal seems like a fine exit for shareholders of the business.

August 28 ended up being a really fascinating day for shareholders and market watchers of hotel operator Hersha Hospitality Trust (HT). Shares of the company spiked, closing up 55.9% at $9.79 after news broke that KSL Capital Partners had agreed to acquire the company in an all-cash deal valuing the firm, on an enterprise value basis, at around $1.4 billion. This obviously has significant ramifications, not only for common shareholders, but also for owners of the three different classes of preferred stock that the company has on the market. While some investors might be disappointed with this development, based on recent performance achieved by the firm, I would argue that this deal is logical and probably gets investors fair value or something close to it.

A straight-forward transaction

On August 28, before the market opened, the management team at Hersha Hospitality Trust announced that the company will be sold to KSL Capital Partners in an all-cash deal valuing the company at $10 per share. This represents a roughly 60% premium over the price that shares traded at immediately before the news broke. Management reports this as translating to an enterprise value of $1.4 billion. From what I can tell, the price isn't quite that high. The number I get is $1.29 billion, which includes net debt, non-controlling interests, and preferred stock, all on top of the common stock. For the purpose of valuing the company, however, I would use the market capitalization I calculated and the enterprise value reported by management.

{kind=link}

Regardless of what the price ends up being, this has a significant impact on common shareholders. Obviously, it does remove any future upside beyond the buyout price. But in exchange, it results in tremendous immediate upside. The same thing is true for shareholders of the preferred stock. These would be the 6.875% Series C Cumulative Redeemable Preferred shares, the 6.50% Series D Cumulative Preferred shares, and the 6.50% Series E Cumulative Redeemable Preferred shares. As you can see in the table above, this resulted in immediate upside for the preferred holders of between 23.8% and 24.5%. Naturally, all distributions payable under these units up to the buyout date will also be honored.

{kind=link}

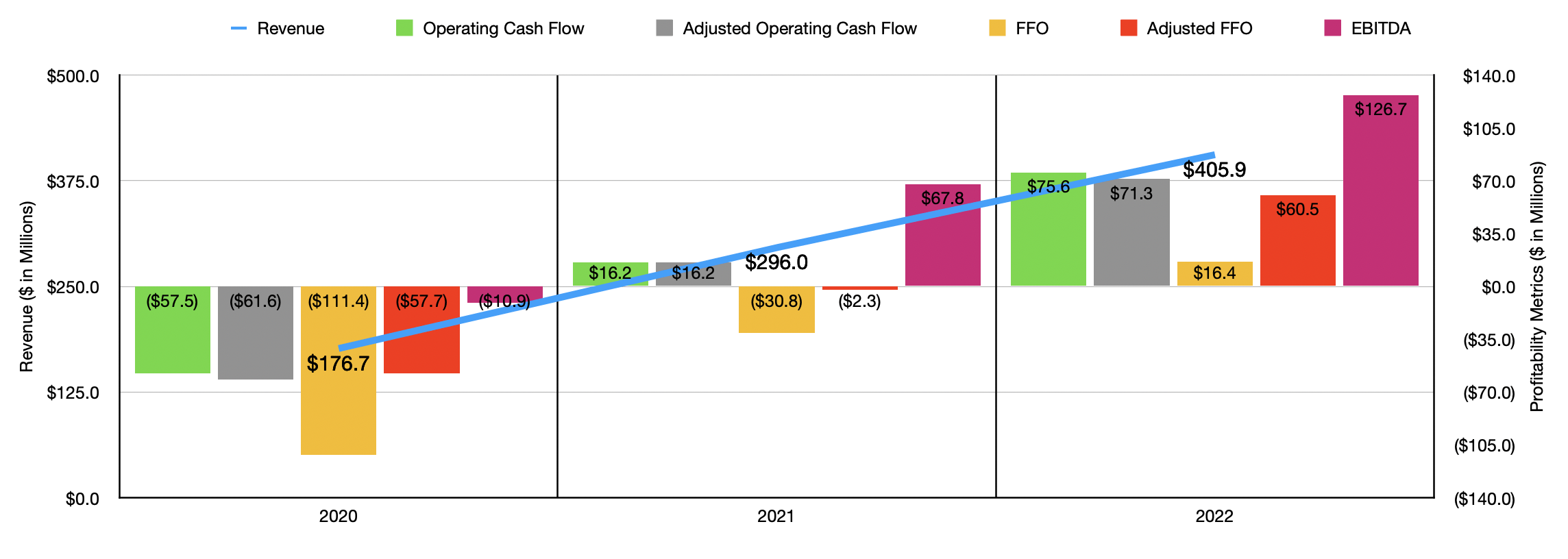

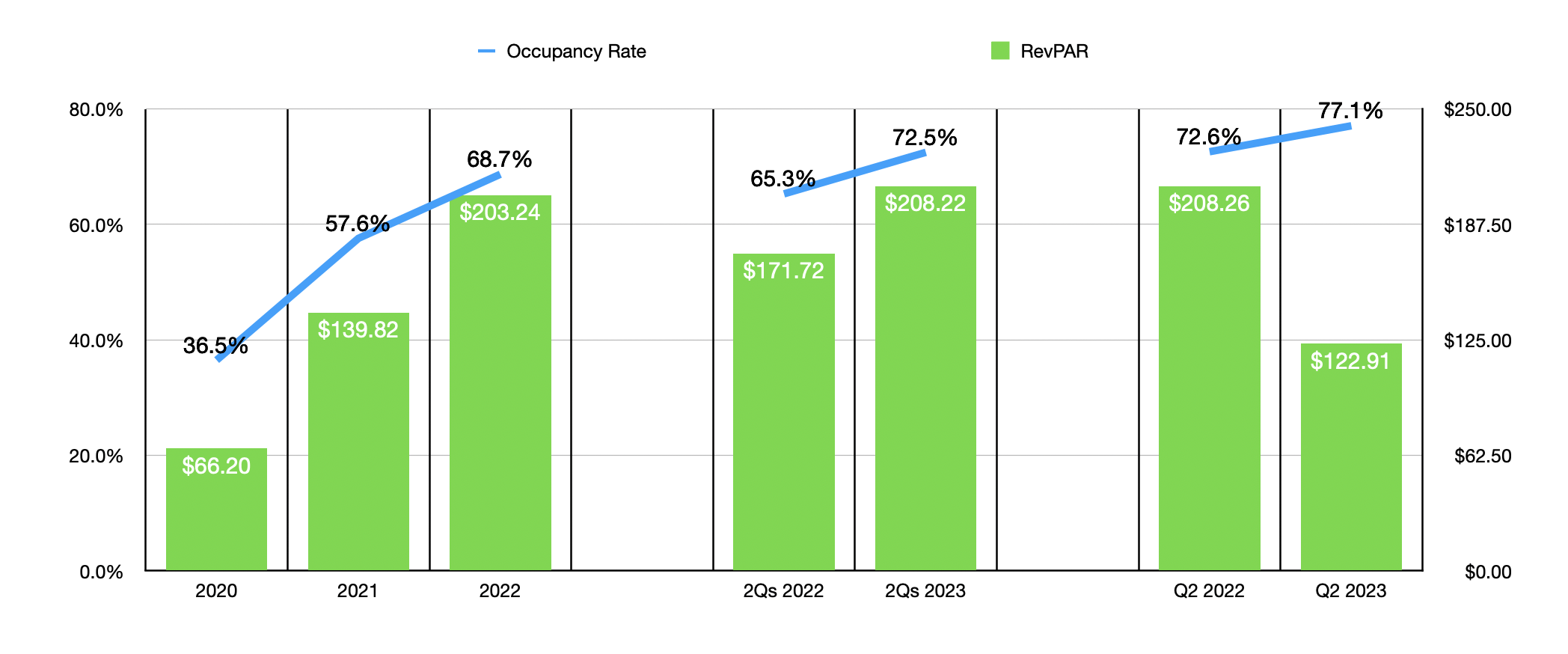

In the past, I was somewhat bullish regarding Hersha Hospitality Trust. This bullishness was driven by the fact that management had been successful in driving the company from the state of pain that it was in during the COVID-19 pandemic to what was an impressive partial recovery. In the chart above, for instance, you can see how the business performed fundamentally over the three years ending in 2022. Revenue, profits, and cash flows, all shot up significantly during this window of time. Even though the company sold off certain assets, this recovery was driven by a surge in the firm's occupancy rate from 36.5% in 2020 to 68.7% in 2022. At that same time, the RevPAR of the business skyrocketed from $66.20 per night to $203.24 per night.

{kind=link}

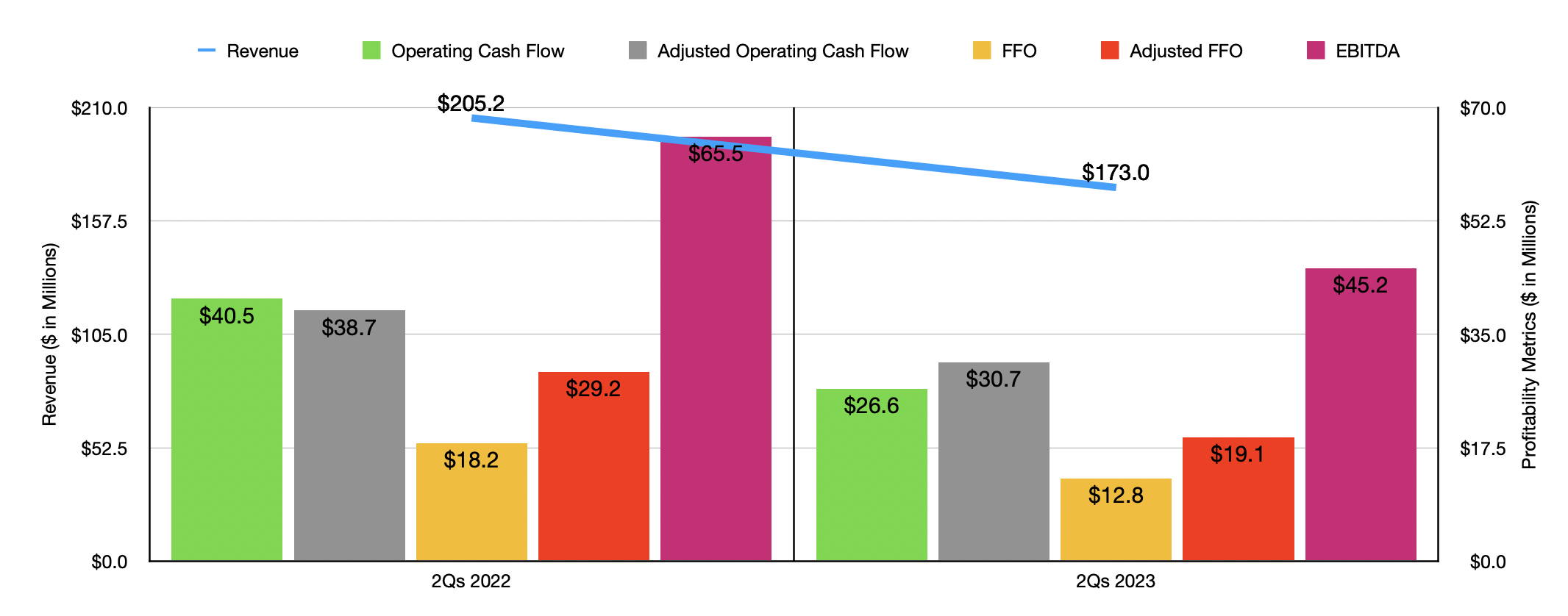

But when it comes to the current fiscal year, some signs of weakness were beginning to emerge. In the first half of the year, for instance, revenue came in at only $173 million. That represents a drop of 15.7% compared to the $205.2 million reported at the same time one year earlier. This occurred even as the occupancy rate to the company shot up from 65.3% to 72.5% and as the RevPAR expanded from $171.72 to $208.22. This might seem odd to some. But the reason why had to do with asset sales. In 2022, for instance, management sold off 10 properties in exchange for $641 million in cash. That cash was used to pay down debt. In the firm's most recent quarterly earnings announcement, it stated that it had paid down another $48 million of debt, debt that bore a weighted average interest rate of 8.46%. That reduction alone should save shareholders $4.1 million in interest per year.

{kind=link}

With the decline in revenue also came a drop in profits. Operating cash flow, for instance, dropped from $40.6 million in the first half of the 2022 fiscal year to $26.6 million the same time this year. If we adjust for changes in working capital, we would get a decline from $38.7 million to $30.7 million. Other profitability metrics worsened also. FFO, or funds from operations, fell from $18.2 million to $12.8 million, while the adjusted figure for it dropped from $29.2 million to $19.1 million. And finally, EBITDA for the business fell from $65.5 million to $45.2 million.

A company undergoing so many changes is difficult to value. And this is because we don't know what the future holds. To see how profitable the firm might be in the future, I was able to take management's guidance for the third quarter of this year and assume that its decline year over year would apply to all future quarters as well relative to what the company achieved last year. This is definitely not a perfect method to use in valuing the company. But it's probably the best approach we have to figuring out how profitable it might be moving forward.

Using this approach, I estimated that the company should generate adjusted operating cash flow of about $58.1 million per annum. But of course, even though it's not typically included in operating cash flow, when determining how valuable common shares are, it is wise to strip out the preferred distributions. This would give us a modified version of cash flow of $33.9 million. Adjusted FFO should be around $49.3 million, while EBITDA should be somewhere around $103.3 million.

{kind=link}

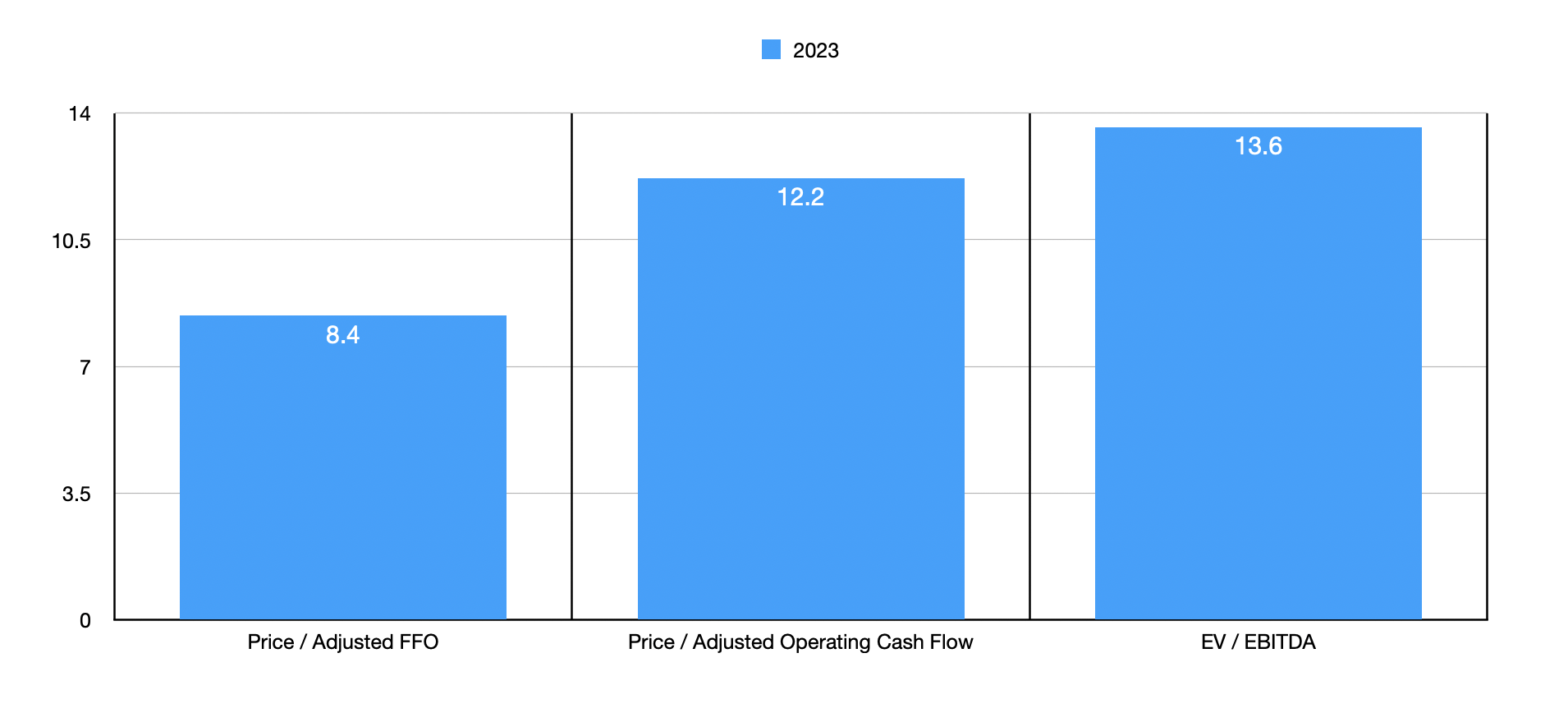

Using these figures, it was easy to value the company. The price to adjusted operating cash flow multiple should be about 12.2. The price to adjusted FFO multiple should be lower at 8.4, while the EV to EBITDA multiple should come in at 13.6. In the table below, I compared the company to five similar firms. I focused only on the operating cash flow and the EBITDA of these companies. In both cases, Hersha Hospitality Trust ended up being the most expensive of the group.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Hersha Hospitality Trust |

| 12.2 |

| 13.6 |

| Braemar Hotels & Resorts ( BHR ) |

| 2.1 |

| 10.0 |

| Chatham Lodging Trust ( CLDT ) |

| 5.6 |

| 9.2 |

| Ashford Hospitality Trust ( AHT ) |

| 2.6 |

| 10.7 |

| Service Properties Trust ( SVC ) |

| 6.1 |

| 9.7 |

| Summit Hotel Properties ( INN ) |

| 3.7 |

| 11.6 |

Takeaway

Based on the valuation data that we have right now, I would make the case that investors in Hersha Hospitality Trust should probably be at least content with this transaction. Relative to similar firms, this does seem to represent a premium. Though, I would argue that shares are still cheap enough to warrant upside if the company were not being purchased in its entirety. This is because, after all, I think that the bulk of the industry is undervalued to some extent. None of this means, however, that shareholders should continue to own their shares of the business. The deal is expected to close sometime in the final quarter of this year. And the upside between where shares are trading now and what they will be purchased for is only 2.1%.

I think the same argument also applies to the preferred units. In the best case, the implied upside from where shares are now is 0.9%, on top of any other distributions coming in the direction of shareholders. And in the worst case, upside, excluding distributions, is only 0.7%. There definitely are better prospects that investors could put their money into during this window of time. So unless you want a modest uptick to your portfolio with a fairly high degree of certainty, with that uptick likely underperforming many investment prospects on the market, I would consider looking elsewhere for opportunities

For further details see:

Hersha Hospitality: A Buyout Is A Good Time To Cash Out