HT - Hersha Hospitality: Big Selloff Creates Opportunity

2023-03-27 21:35:16 ET

Summary

- Since the beginning of the month, Hersha has sold off from $8.60/share to the current price of $6.15, despite hotel booking trends improving.

- Last year, Hersha sold off 9 of their 33 hotels, reducing net debt from $1.1 billion at year-end 2021 to just $405.2 million currently.

- Recent STR data shows business travel recovering and urban hotels posting large year-over-year gains in RevPAR. In the latest week, NYC RevPAR was up 36% year over year.

- Hersha is in a unique position to capitalize on this valuation discrepancy with a net cash balance of $225 million versus a market capitalization of $285 million.

Hersha Hospitality Trust ( HT ) is a Hotel REIT that went through an interesting recapitalization last year. It sold off 9 of its 33 hotels at good prices, and as a result was able to substantially deleverage, reducing net debt from $1.1 billion at year end 2021 to just $405.2 million at year end 2022.

This, along with a significant recovery in hotel performance, was well received by the market. After being above $11 are recently as August, shares have recently plunged from above $9 in February to $6 now. I believe this is due to a combination of forced selling from Hersha being removed from the S&P600 SmallCap index, as well as broader market concerns in the entire REIT sector. As one of the least leveraged hotel REITS, I think these concerns with Hersha are not just overblown, but wrong.

Capitalization + Valuation

At year-end 2022, Hersha's capitalization was the following:

- Net Debt: $405 million

- Preferred Shares: 14.7 million @ $25/share = $367.6 million

- Diluted Common Units: 46.4 million @ $6.15/share = $285 million

Total Capitalization: $1.057 billion

The $1.057 billion in total capitalization, divided by the "number of keys" (3,507) implies a current valuation of $301,600 per key.

The sale of the Urban Select Portfolio of 7 hotels was done at $360,000 per key.

The most recent sale of two recent West Coast properties were done at $455,000 per key. In the press release, Hersha stated that

The valuation of these two assets is yet another confirmation of the public-to-private market valuation gap for our portfolio, and we believe pricing on these two assets is more representative of the remaining portfolio than prior dispositions.”

Theoretically, if Hersha went forward and liquidated its entire Hotel portfolio at $455,000 per key, it would generate $1.6 billion. Eliminating all debt and Preferred shares would cost $773 million, leaving $827 million. This compares very favorable against a current market cap of $285 million and would imply an equity value around $17.90/share. Even dropping this number to $400,000/key implies an equity value of $14/share.

The new CEO spoke extensively about the NAV gap in the most recent conference call 5 weeks ago (and this was with the stock at $9, mind you)

Our management team has worked diligently to right size our balance sheet and to close the significant NAV gap that persists for our portfolio. We still believe that we traded in an outsized discount to our private market value and are extremely sensitive to any capital allocation decisions that would impact our NAV or leverage as a trade off to growth.

Considering the large inside ownership in Hersha, I believe this is credible.

Hersha has $225 million in cash versus a current market capitalization of $285 million. Hersha does not have a current repurchase authorization (it expired in December 2020) but they have repurchased significant amounts of shares in the past. I would not be surprised to see a repurchase authorization announcement in the coming weeks, especially if operating performance remains strong. Park Hotels ( PK ) repurchased shares in Q4 because of this same valuation gap, despite having much higher leverage.

I would expect the shares to jump 10%+ on any repurchase announcement, if it happens.

Leverage

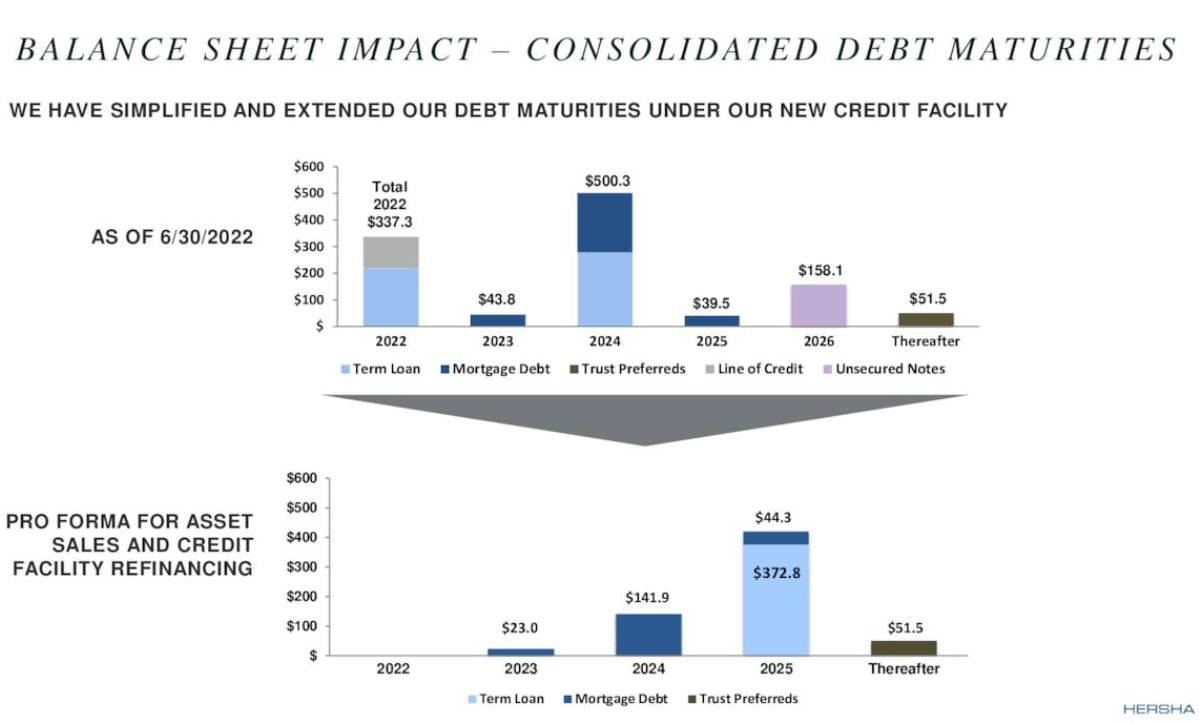

One of the reasons I like Hersha here is because they've significantly deleveraged and have minimal near-term financing risk.

At year-end 2022, they had $225 million net cash on the balance sheet versus $630 million in gross debt. If they chose, they could pay off the upcoming 2023 and 2024 mortgage maturities in cash, leaving the next maturity of their term loan in 2025.

{kind=link}

If we believe the recent large drop off in intermediate term interest rate expectations, that is a big positive for Hersha as well.

Recent Hotel Trends

Hersha had positive comments on current quarter booking trends during their Q4 Conference Call

Our January results were very encouraging with our comparable portfolio RevPAR ahead of January 2019 by approximately 4%. And month to date, our February RevPAR is ahead of February 2019 by 5.5%.

Since that call, i ndustry data reported by STR , Inc, have been extremely strong, particularly in Hersha's key markets, let by strong occupancy gains in Washington, D.C. (+12.1% to 67.6%), New York City (+10.9% to 78.3%) and Boston (+9.6% to 65.4%.)

Hersha Hotels List (Hersha Investor Presentation)

This resulted in year over year RevPAR growth Washington, D.C. (+50.2% to US$124), Boston (+39.0% to US$123), and NYC (+32.7% to US$181).

The strength discussed on the call only seems to have accelerated in March.

So why the steep drop in price?

Despite the industry recovering, why has Hersha dropped so significantly recently?

One key reason was that Hersha was just removed from the S&P SmallCap 600. For those that have read my work, you know that uneconomic forced selling is one of my favorite ways to find undervalued companies.

Another was just a messy last few weeks with the banking crisis where anything not tech got sold indiscriminately, coupled with a partial fundamentally driven sell-off in the commercial real estate sector. Neither of these really means much to Hersha or other hotel REITs, and I think there is a very strong chance this trend reverses over the next few months.

Conclusion

Unlike some other hotel REITS, I consider the leverage at Hersha to be under control. Some of their debt is floating rate, so the recent bond market action pricing in future cuts will be a help, if they materialize.

I believe the hotel recovery is real, and that urban hotels will lead the gains. The last week, STR had overall RevPar up 120.8% versus the same week in 2019, with NYC RevPAR up 36% year over year.

I think there is a very high chance HT exceeds the top end of their Q1 guidance of 4-8 cents of FFO for Q1 and projects a healthy Q2 FFO, as we're heading into the strongest seasonal part of the year for hotels.

Beyond this, Hersha has a net cash balance $225 million versus a market capitalization of $285 million. The money from the two hotels they just sold could repurchase half of the outstanding common shares. Hersha has the cash available to take advantage of this, and seeing a repurchase authorization in the near future would not surprise me.

I think Hersha stock is a solid buy at these levels, and could recover back to $8+ quickly.

For further details see:

Hersha Hospitality: Big Selloff Creates Opportunity