HT - Hersha Hospitality Trust: Undervalued But Financial Performance A Concern

2023-06-20 01:57:50 ET

Summary

- Hersha Hospitality Trust is a hospitality REIT focused on luxury, upscale, and upper midscale hotels in key markets such as New York City, Boston, Washington D.C., and Philadelphia.

- The company has recently reinstated its dividend and pays a forward dividend yield of 3.30%, with several valuation metrics indicating that the company is undervalued at present.

- However, concerns over the company's financial performance, including a declining AFFO over the past few years, make it a "Hold" for investors seeking better opportunities in the hospitality industry.

Introduction

I have written about several hospitality REITs in the past few months, covering select-service REITs such as Apple Hospitality REIT (NYSE: APLE ) and Summit Hotel Properties (NYSE: INN ) and full-service REITs such as Park Hotels & Resorts (NYSE: PK ) and Host Hotels & Resorts (NASDAQ: HST ).

The focus of this article, Hersha Hospitality Trust ( HT ), is another hospitality REIT. Similar to the latter two hospitality REITs, Hersha Hospitality Trust has a focus on luxury, upscale and upper midscale hotels. In this article, I will evaluate the company to determine if it is an attractive investment.

The Business

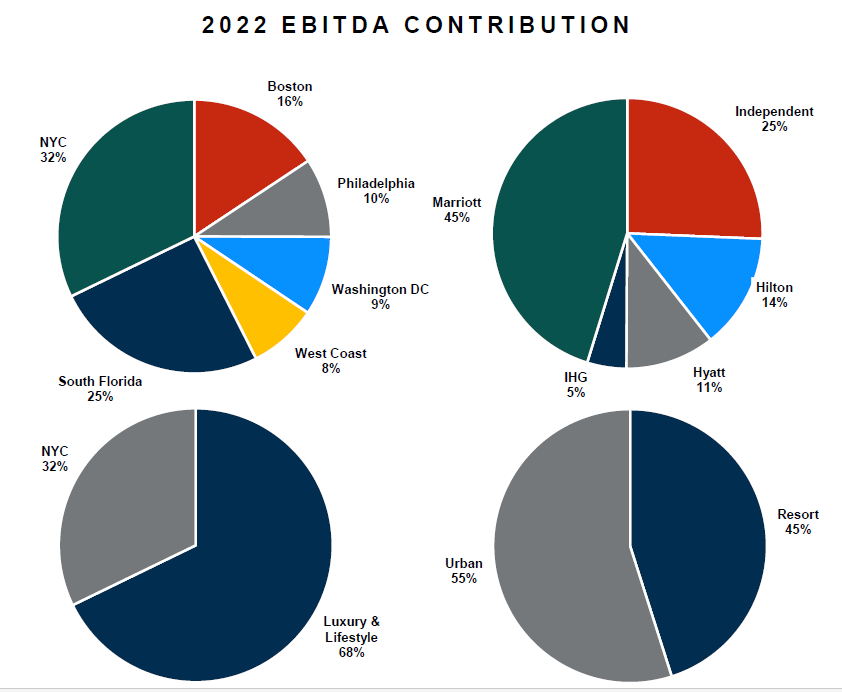

Hersha Hospitality Trust is a hospitality REIT specializing in luxury, upscale and upper midscale hotels. The company has a strategic focus on gateway markets, which are major metropolitan areas which a high population. Such markets include New York City, Boston, Washington D.C. and Philadelphia and they generally have a higher barrier to entry. The company's portfolio comprises hotels affiliated with prominent brands such as Marriott and Hilton. Apart from these brands, the company also has independent boutique hotels in markets with similar characteristics.

As of Q1 2023, the company has a portfolio of 23 hotels with a total of 3,507 rooms. In particular, the company's main focus is on New York City which represents over a third of its hotel portfolio with 8 hotels and approximately 1,300 rooms.

{kind=link}

Q1 2023 Earnings & FY 2023 Outlook

The company's latest earnings are for Q1 2023 , with the Q2 2023 earnings to be announced in early August . Before diving into detail, there are a couple of points to note. Historically, the first quarter has generally been the slowest quarter for the company. It was for this very reason that the company chose to carry out significant renovations across some of its properties during the quarter. While these renovations are expected to enhance the performance of its properties in the future, there was undoubtedly an impact on the company's Q1 earnings.

For Q1 2023, the company's comparable hotel portfolio saw an occupancy of 68% and an average daily rate (ADR) of $268. As a result, the revenue per available room (RevPAR) for the quarter stood at $182. Excluding the properties undergoing renovations, however, the hotel portfolio saw an occupancy of approximately 73% and an ADR of $290, which translates to a RevPAR of $212 - an increase of 11.4% compared to the 2019 figures.

{kind=link}

The company reported a net loss of nearly $15 million, or a loss of $0.38/share, for Q1 2023. In comparison, Q1 2022 saw a much larger loss at $22 million or $0.57/share. However, adjusted funds from operations (AFFO) for Q1 2023 came in at $0.02/share, lower than the $0.07/share recorded in Q1 2022. It is worth noting that Q1 2023 results came in below the company's original forecast , though it has to be said that the renovations had a greater than expected impact on the company.

Looking ahead, the company has projected an AFFO of between $0.39/share and $0.45/share for Q2 2023.

Balance Sheet

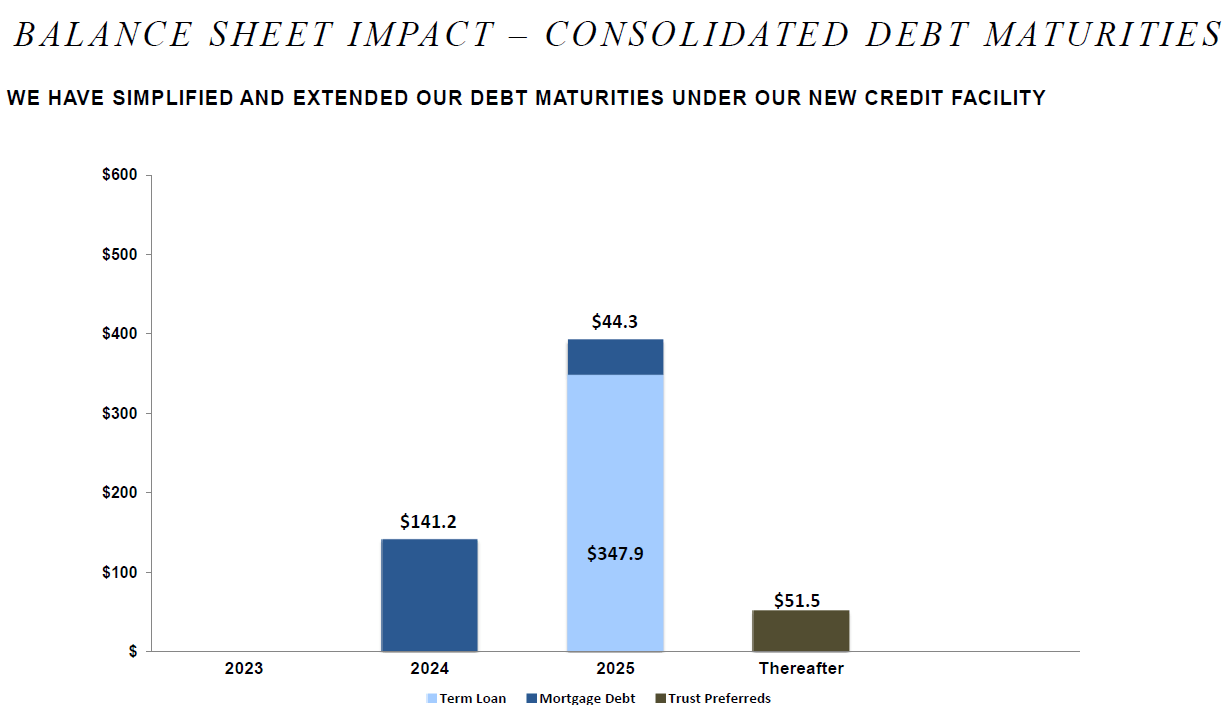

As of May 2023, the company has close to $150 million in cash, with a further $100 million revolving line of credit available to the company if needed. Of course, just knowing the amount of liquidity a company has is insufficient to draw any conclusions. In terms of the company's liabilities, the company has a debt of approximately $585 million, of which none is due this year and only less than a quarter due next year. Coupled together with the liquidity the company has, it ensures the company will be able to manage its obligations at least this year and the next.

It should also be noted that the majority of the company's debt, or 78.5%, is fixed debt. This provides stability and predictability in the company's cash flows and is especially crucial considering that interest rates are expected to remain high for the foreseeable future.

The company has been actively focused on reducing its leverage, with a target of maintaining its a debt to EBITDA ratio of between 3x and 4x. Notably, the company has achieved its objective, with its net debt to EBITDA on a trailing twelve-month basis at the end of Q1 2023 coming in at 3.7x. The company's strong financial position, coupled with its reducing leverage, ensures the company has the financial flexibility to pursue any opportunities which may arise.

{kind=link}

Dividend

Hersha Hospitality Trust, like many other REITs, saw the pandemic impact its dividend payments. Prior to the pandemic, the company had been consistently paying a quarterly dividend, with the latest increase to its dividend coming in 2017 for a quarterly dividend of $0.28/share. However, due to the severe disruption to the hospitality sector, the company suspended its dividend payout after Q1 2020.

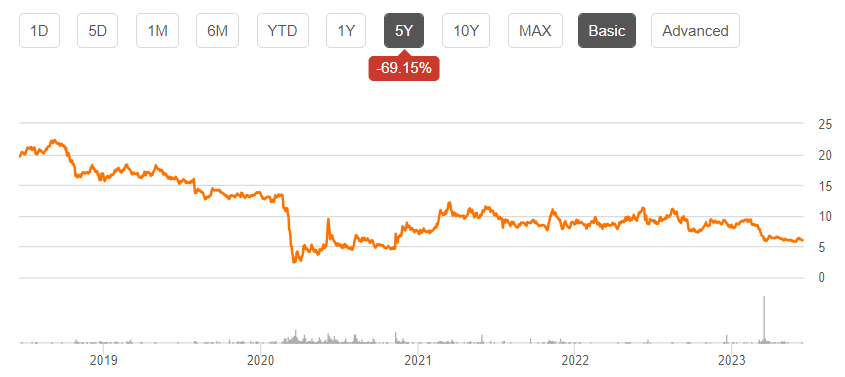

The company reinstated its dividends in Q3 2022, resuming with a quarterly dividend of $0.05/share . This dividend level has been maintained since then, with the upcoming Q2 2023 dividend scheduled to be paid in the middle of next month on 17 July 2023 . With the current share price at $6.06, this gives the company a forward dividend yield of 3.30%. It should be noted that the company paid out a special dividend of $0.50/share last year, which I have not accounted for in my calculations as this is a special dividend and not a recurring one.

To assess the sustainability of the company's dividends, the company's AFFO is a key measure. The company reported an AFFO of $1.30/share for FY 2022, comfortably covering the forward annual dividend of $0.20/share. For the FY 2023, the projected AFFO for Q2 2023 alone is expected to cover the annual dividend even after taking into account the slower performance in Q1 2023. Using the FY 2022 AFFO figures as an estimate, the company's dividends seem quite safe. Even a reinstatement to the previous quarterly dividend of $0.28/share would result in a payout ratio of 86%. While not a low payout ratio, it is still a reasonable figure.

Risks & Considerations

There are, however, several risks that should be taken into consideration. Firstly is the company's geographic concentration. A significant portion of the company's earnings is derived from only a few key markets, with New York City and Boston alone accounting for close to half of the company's FY 2022 EBITDA. Any adverse developments in these markets will have a substantial impact on the company's financial performance.

Concerns regarding the company's recent and historical performance also warrant attention. The projected AFFO for Q2 2023, even at the high end of $0.45/share is still substantially below the Q2 2022 AFFO of $0.56/share. Additionally, even prior to the pandemic, there was a declining trend in the company's AFFO - from FY 2016 to FY 2019, the company's AFFO was $2.40/share, $2.16/share, $2.20/share and $1.94/share. While it might not be reasonable to expect the company to have fully recovered from the pandemic, its FY 2022 AFFO of $1.30/share which remains substantially short of the pre-pandemic figures and the declining trend in its AFFO is a cause for concern.

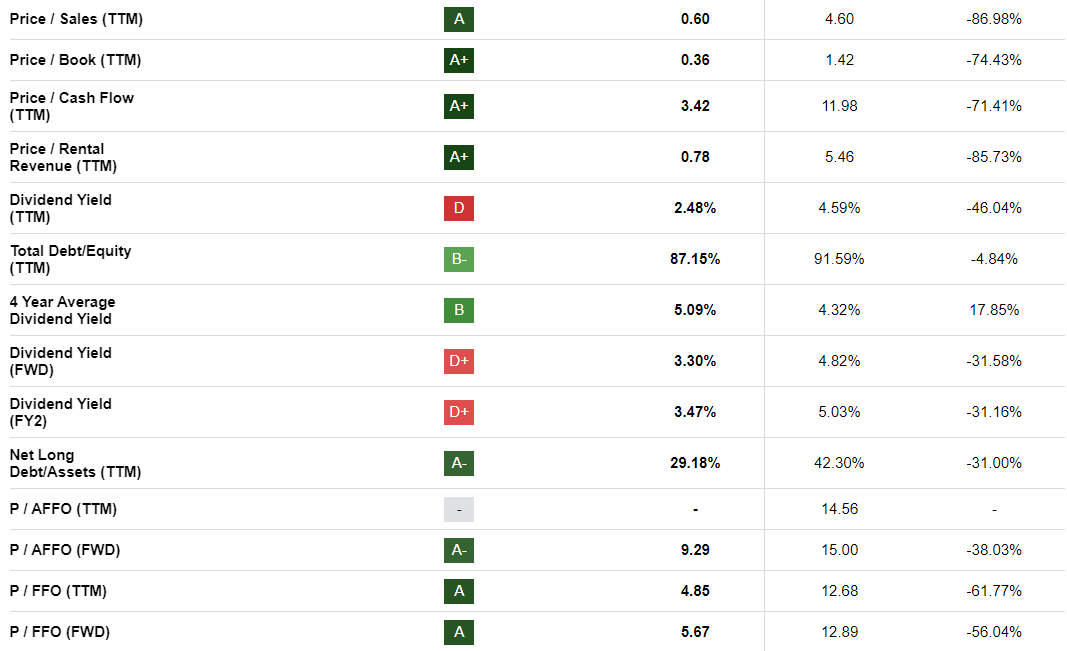

However, it is important to note some caveats to these risks. The company has significant insider ownership, with management holding approximately 20%, which is a positive signal showing management's confidence in the company's prospects. Additionally, various valuation metrics such as the price-to-sales (P/S) ratio, price-to-book (P/B) ratio and forward price-to-adjusted funds from operations (P/AFFO) all suggest that the company is undervalued compared to its peers in the sector. Moreover, the company's share price remains significantly below pre-pandemic levels. Prior to the pandemic, the share price was around $14, more than double the current share price. Hence, there is a compelling case to believe that the company's shares a substantially undervalued.

{kind=link}

{kind=link}

Conclusion

Hersha Hospitality Trust is a hospitality REIT focused on a few key markets. The company has recently reinstated its dividend and pays a forward dividend yield of 3.30%. Several valuation metrics and the company's historical share price all indicate that the company is undervalued at present. The company also has significant insider ownership, which indicates to me that the management has confidence in the company's future prospects. Potential investors may view this as a valuable opportunity, with room for substantial capital appreciation.

However, as I indicated above, I do have concerns over the company's financial performance. It has shown a declining AFFO over the past few years, even before the pandemic. While there isn't any issue with the dividend safety as the payout ratio remains at a comfortable range, the declining performance is still a point of concern for me.

I invest in REITs mainly for the dividend yield, and not for capital growth, though of course, an ideal scenario would be to have both. The company's historical financial performance, coupled with the relatively low dividend yield at 3.30%, means that the company is a "Hold" for me as I believe there are better opportunities out there at present. For investors who would like exposure to the hospitality industry, more specifically the luxury hotels, one example would be Host Hotels & Resorts which I wrote about earlier this month. Though the company pays a slightly lower dividend yield, I view it as a better investment overall due to the stability and safety of the company.

For further details see:

Hersha Hospitality Trust: Undervalued But Financial Performance A Concern