HESM - Hess Midstream: Growing Value Through Dividend Increases And Share Repurchases

2023-06-22 19:00:55 ET

Summary

- Today’s comments by John Hess at an investor conference support Hess Midstream LP’s long-term prospects.

- Hess Midstream has executed superbly since coming public; we expect that to continue.

- The company has a conservative dividend that is likely to grow and trades at a 7.6% yield.

John Hess, CEO of Hess Corporation ( HES ), stated today at the J.P. Morgan Energy, Power, and Renewables conference that he expects Hess Corp.’s cash flow to grow by 25% per year over the next five years with oil above $75 per barrel. The growth will be driven by production growth from the company’s 30% interest in Guyana’s Stabroek block operated by Exxon Mobil Corporation ( XOM ). The announcement was enough to spare Hess Corp. stock the worst of today’s price declines among E&Ps.

But the comments also delivered a boost to Hess Midstream LP ( HESM ), which gathers and processes all of Hess Corp.’s Bakken oil and gas production. HESM's stock is gaining on a down day for both energy and midstream.

We’ve long held that a risk to HESM is a scenario in which Hess Corp. opts to divest its Bakken acreage. While such a move wouldn’t necessarily lessen the long-term appeal of HESM shares, it would introduce uncertainty about the company’s prospects, which would depend on the acquirer’s development plans. Hess Corp. has used its Bakken acreage as a cash cow, keeping output broadly steady to maximize long-term free cash flow. The strategy is ideal for maintaining steady cash flow growth at HESM. Any change in strategy could change HESM's investment prospects for the worse.

John Hess's commentary implies that Hess Corp.’s Bakken cash flow will continue to be an important part of the company’s operations. We believe the comments reduce the risk of a change in control over at least the next few years. They also suggest that Hess Corp. will see its cash flow grow at a healthy rate even with oil below $75 per barrel, making it more likely that the company keeps its Bakken operations steady, which would benefit HESM.

Hess Corp. claims to have 15 years of profitable locations at its current development rate with WTI at $60 per barrel. Its drilling inventory grows larger at higher oil prices, though it could shrink if it accelerates its pace of Bakken development.

We'd note that Hess Corp. is growing its average annual production rate by 9% in 2023 versus 2022. However, the company's 15-year drilling inventory estimate is based on its 2023 Bakken production volumes. This year's Bakken growth is primarily attributable to an additional Bakken rig that was added last July, so we don’t expect annual production growth via increased drilling activity to remain as elevated going forward.

That said, we do expect continued volume growth for HESM. The combination of Hess Corp. maintaining four rigs on its acreage, its commitment to "zero flaring" on its Bakken properties, and progressively gassier Bakken production are likely to grow HESM’s volumes over at least the next few years. HESM’s system is positioned to support a production increase of 30% from 2022 to 2025. The company is currently constructing two new natural gas processing facilities to accommodate Hess Corp.’s planned growth.

The other, more obvious risk to HESM shareholders is a bout of sustained low oil prices. Once Bakken activity stops generating free cash flow for Hess Corp., it will curtail development. The last time it did so was in 2020, when it dropped its Bakken rig count from six to one in May of that year.

Partially offsetting this risk is HESM’s minimum volume commitments, which cover more than 80% of its revenues through 2025. However, the company could be forced to cut its distribution amid a material decline in drilling activity even with these contractual commitments.

Only a deep global recession that takes oil prices below $60 per barrel for a sustained period would lead Hess Corp. to pare back its Bakken drilling activity. This scenario would pose a risk for nearly every oil and gas equity. We expect crude inventories to draw in the second half of the year, which should be supportive of oil prices and, by extension, Hess Corp.’s drilling activity. We therefore don't expect the company to reduce its drilling activity under anything but the most severe oil market conditions.

Financial Performance Has Been Strong

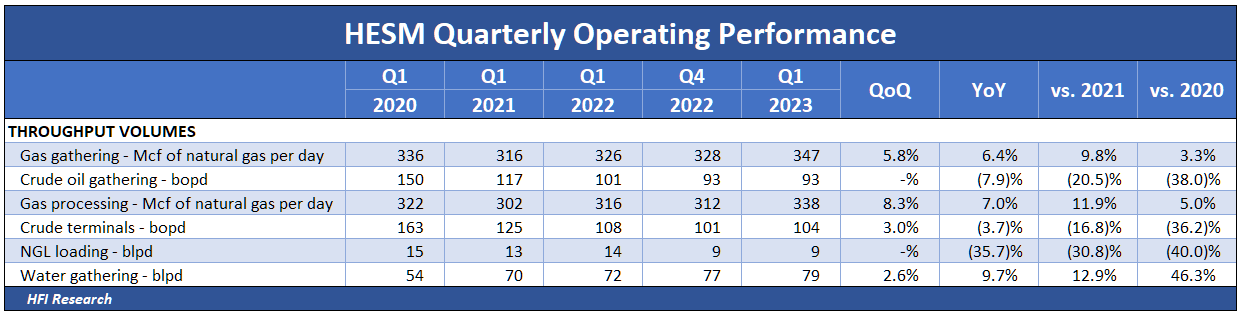

HESM continued its track record of natural gas volume growth in the first quarter. Natural gas volumes have been HESM’s growth engine, with first-quarter gathered volumes coming in 6.4% higher year-over-year and 9.8% above the first quarter of 2021. The growth has come even as crude volumes fell after Hess Corp reduced its rig count in 2020. Natural gas processed volumes rose by 7.0% and 11.9% over the first quarters of 2022 and 2021, respectively.

{kind=link}

During the quarter, HESM continued to reduce its share count by repurchasing $100 million of units held by its sponsors. The share sale increased HESM’s public float to 18.3% of its outstanding shares, which will enhance trading liquidity, reduce share-price volatility, and increase the likelihood that the shares reflect the company's intrinsic value.

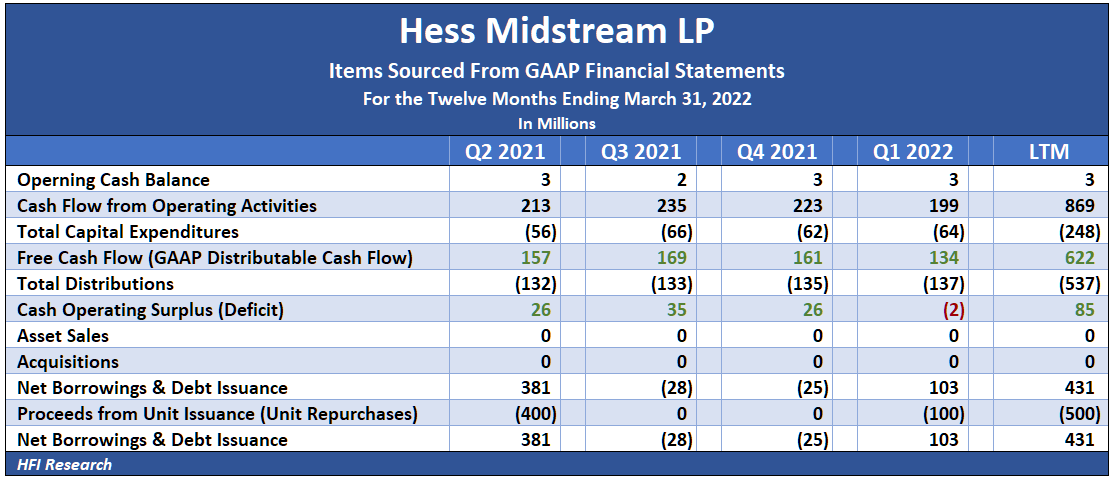

HESM generated a $2 million cash flow deficit during the first quarter, which has been its seasonally weakest quarter over the past few years. The lack of free cash flow required it to borrow on its revolving credit facility to fund its share repurchases. Over the last twelve months, HESM generated an $85 million cash flow surplus. It used the surplus and $431 million of borrowings to repurchase $500 million of shares, as shown in the table below.

{kind=link}

HESM’s increased debt load at the end of the first quarter boosted its leverage ratio from 2.9-times at the end of 2022 to 3.0-times at the end of the first quarter. Even with the increase, HESM’s leverage ratio is the lowest among its G&P peers.

On May 16, HESM's sponsors sold 11.1 million of its shares at $27.00 per share in a secondary offering. While HESM received none of the proceeds of the sale, the shares further increase the float of publicly-traded shares.

Conclusion

Hess Midstream LP is executing operationally and financially. It is likely to register steady cash flow growth in all but the absolute worst oil-market conditions. We expect management to continue to take proactive measures to return capital to shareholders in the form of dividend increases and share repurchases. HESM shares offer the added benefit of being taxed like a corporation, so its shareholders avoid the hassles associated with a K-1.

Hess Midstream LP shares can be bought with confidence that cash flow and dividends per share will increase over the next few years. We believe they're an attractive alternative for any income portfolio.

For further details see:

Hess Midstream: Growing Value Through Dividend Increases And Share Repurchases