HESM - Hess Midstream Looks Well Positioned For 2024

2023-10-04 04:23:06 ET

Summary

- Hess Midstream's Q2 EBITDA did not reflect how strong its underlying growth really was.

- The company looks poised to see solid growth over the next couple of years.

- The stock trades at a slight premium to its peers but offers a nice mix of safety and growth, making it a "Buy."

Back in June, I placed a “Buy” rating on Hess Midstream ( HESM ), saying it offered an intriguing mix of safety and income for investors. At the time, I thought the company should see solid growth as its parent, oil giant Hess ( HES ), begin to re-ramp up activity in the Bakken. The stock is about breakeven since then, as is the S&P 500. Let’s catch-up on the name.

Company Profile

As a refresher, HESM operates midstream assets in the Bakken and Three Forks shale plays in North Dakota, serving primarily oil major HES. About 50% of its EBITDA comes from its gathering business, where it gathers natural gas, NGLs, and crude oil. The segment also has water gathering and disposal pipelines.

Approximately 40% of HESM’s EBITDA comes from its Processing & Storage segment, whose assets include processing plants and NGL storage facilities. The rest of the company’s EBITDA comes from its Terminal and Export segment, whose assets include a truck and pipeline terminal, a rail terminal, and a header system.

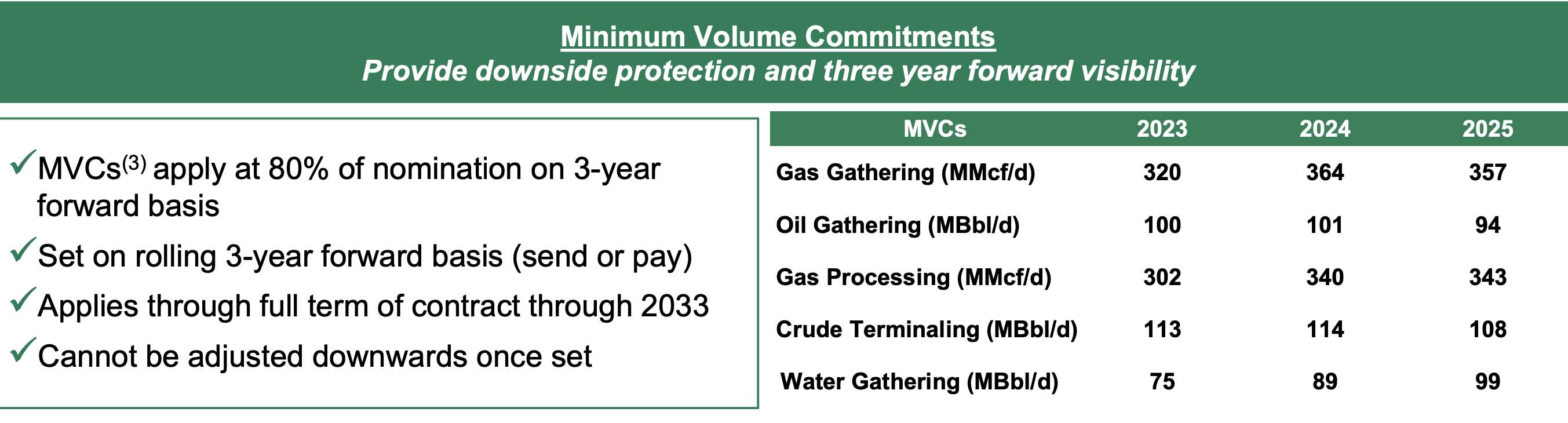

HESM gets virtually all its revenue from fee-based contracts, which generally have CPI escalators that are capped at 3%. The company also get minimum volume commitments (MVCs) that are set on rolling 3-year basis.

{kind=link}

Steady Q2 Performance and Increased Guidance

HESM turned in steady Q2 results, with adjusted EBITDA rising 2% to $248.1 million from $242.6 million a year ago.

Higher interest rates, however, weighed on net income and distributable cash flow ((DCF)). Net income fell nearly -3% to $147.9 million, while DCF was lower by nearly -2% to $202.6 million.

The company paid out a 60.1 cent dividend during the quarter, with a coverage ratio of 1.4x.

Adjusted free cash flow was $154.3 million, as it spent $48.3 million in growth Capex. It had $14.3 million in FCF after dividends for the quarter.

HESM saw its throughput volumes increase across all its products, both year over year and sequentially. Gas gathering volumes jumped 19% year over year to 369 MCF/d, while crude gathering volumes rose 7% to 94 bo/d. Gas processing volumes climbed 23%. Crude terminal volumes rose 16% to 108 bo/d, while water gathering soared 34% to 87 bl/d.

The company ended the quarter with leverage of 3.1x.

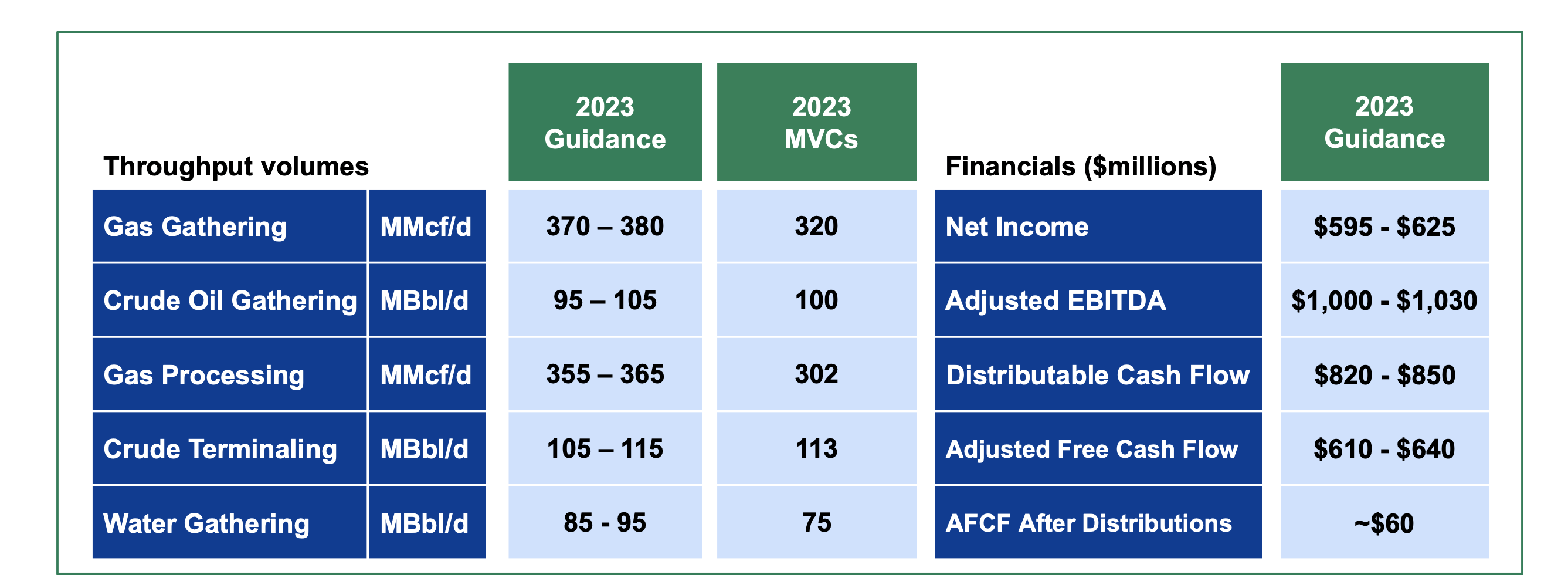

Looking ahead, HESM forecast full-year adjusted EBITDA of between $1.00-1.03 billion, up from a prior outlook of $990 million to $1.03 billion. It is projecting DCF of between $820-850 million versus a previous forecast of $815-855 million. It expects adjusted free cash flow of between $610-640 million compared to prior guidance of $605-645 million. HESM also raised its guidance on throughput volumes for gas gathering and gas processing.

For Q3, the company expects adjusted EBITDA to be between $250-260 million. It anticipates adjusted EBITDA growth to be higher in Q4.

HESM said it will continue to target at least 5% distribution growth through 2025 with a coverage ratio of at least 1.4.x. It projects at least 10% a year growth in net income and Adjusted EBITDA for 2024 and 2025.

{kind=link}

On its Q2 earnings call , COO John Gatling said:

“Hess reported strong second quarter results with the Bakken net production averaging 181,000 barrels of oil equivalent per day, which was above their guidance range of 165,000 to 170,000 barrels of oil equivalent per day. Approximately half of the increase was due to the strong operational and development performance and the remainder from higher production entitlements under Hess' percentage of proceeds or POP contracts. As a reminder, POP volumes do not impact Hess Midstream's throughput volumes or revenues. Hess anticipates Bakken net production will increase to approximately 185,000 barrels of oil equivalent per day in the third quarter, and as a result of expected continued strong performance, raise their full year 2023 Bakken net production guidance by 10,000 barrels of oil equivalent per day to 175,000 to 180,000 barrels of oil equivalent per day. Hess plans to continue to operate a 4-rig drilling program and bring approximately 110 wells online in 2023. Furthermore, Hess continues to forecast Bakken net production to grow to an average of approximately 200,000 barrels of oil equivalent per day in 2025, which implies approximately 10% annualized growth rate in throughput volumes across all Hess Midstream systems from 2023 to 2025. Additionally, Hess expects to hold production at approximately 200,000 barrels of oil equivalent per day for nearly a decade.”

Last month, HESM bought back $100 million units from HES and Global Infrastructure Partners (GIP). The company paid $30.29 per unit. Earlier in August, GIP sold 10 million shares at a price of $28.80 in a secondary offering.

Overall, HESM put up solid Q2 numbers. One thing to note is that EBITDA growth did not keep pace with volume growth and price escalators largely because the company had high MVCs in 2022 that it was below at the time. As such, in Q2 what HESM largely saw was volumes mostly catching up to last year’s MVC levels.

HESM’s MVCs for this year were considerably lower in most categories, outside of water gathering, so it’s been important that the company see the surge in volumes in the 1H, even though it hasn’t led to big jumps in EBITDA or other metrics. However, now that volumes have caught up to 2022 MVC levels and with HES continuing its 4-rig drilling program, expect the HSEM to see nice growth after this year.

Valuation

Turning to valuation, HESM stock trades at 9.3x the 2023 EBITDA consensus of $1.02 billion. Based on the 2024 EBITDA consensus of $1.15 billion, it is valued at 8.3x.

The stock has a free cash flow yield of about 9.6% based on 2023 projections calling for $625 million in FCF. And it pays out a dividend yield of ~8.5%. It expects to raise its dividend 5% annually at least through 2024.

The stock trades at a slight premium to some other mid-sized midstream operators that generally trade between 8-9x 2023 EBITDA.

Conclusion

Given its contracts and ties to oil giant HES, HESM continues to offer a nice mix of safety and growth. HES is committed to increasing its Bakken production over the next couple of years, and with oil prices where they are at, there is no reason to think the oil major will deviate from its plans.

The biggest risk to HESM would be for an oil price collapse that changes HES’ drilling plans, but even then, its contracts (which see MVCs move up nicely next year) would partially protect its EBITDA and cash flow. Higher interest rates are a bit of a drag on cash flows, while GIP and HES selling shares occasionally can be a bit of an overhang.

That said, HESM is one of the safest midstream stocks out there, and it should see nice distribution growth over the next few years. As such, I continue to rate the stock a “Buy.” My target is $33, which is an under 9.5x multiple on 2024 projected EBITDA. Given its contracts and growth prospects, I believe the stock deserves a slight premium to some of its peers.

For further details see:

Hess Midstream Looks Well Positioned For 2024