HESM - Hess Midstream Offers A Secure 8% Yield With Possible M&A Upside

2023-11-06 20:59:14 ET

Summary

- Hess Midstream has been a solid performer, with shares rising 8% and paying out an 8% distribution to investors.

- HESM operates a fee-based revenue model, making its dividend secure and attractive for income-seeking investors.

- The acquisition of Hess by Chevron is likely to be positive for Hess Midstream, potentially leading to further upside opportunities.

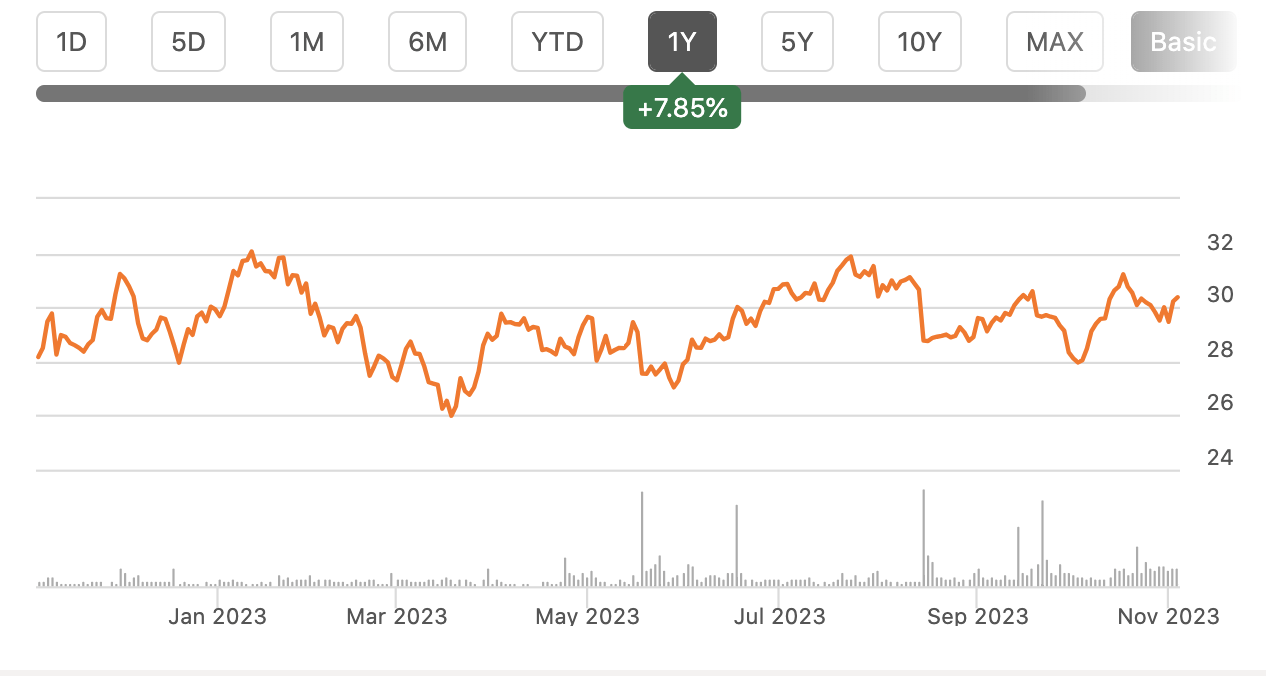

Shares of Hess Midstream ( HESM ) have been a reasonable performer over the past year, rising 8% while also paying out an 8% distribution to investors. Given its strong fee-based revenue, its dividend is quite secure, making this an attractive company for income-seeking investors. Moreover, I believe Chevron's ( CVX ) acquisition of Hess ( HES ) is likely to be positive for HESM. At the worst, it has a larger, even stronger company as a counterparty. Additionally, I believe that in the months after CVX completes its purchase, it will likely seek to acquire HESM, creating further upside opportunities.

{kind=link}

In the company's third quarter , Hess Midstream grew revenue by 9% to $363 million, leading to $0.57 in EPS, a penny ahead of consensus . HES operates an extremely predictable business because it takes essentially no commodity or volume risk, collecting fees for transporting gas and water for Hess and other third-party products.

Its contracts with Hess extend through 2033. 100% of these contracts are fee based. It also negotiates minimum volume commitments ((MVC)) on a three-year basis, which currently extend through 2025. These MVCs amount to about 85% of this year's revenue. They also assume 10% volume growth through 2025. This means that Hess has to pay HESM a minimum fee, even if it ships less through the pipes than the contract.

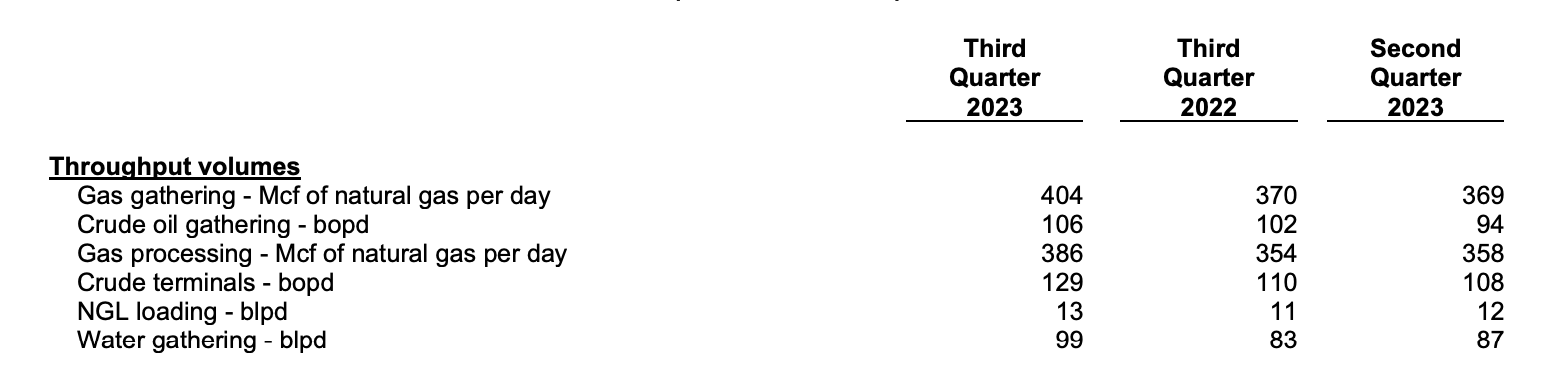

This helps to insulate HESM's income and cash flow from weak production or if Hess were to cut cap-ex due to lower commodity prices. In the quarter, HESM received $2.8 million in MVC shortfall fees or about 0.8% of revenue. This was down substantially from $27 million last year because Hess has been growing its production. In the long-term, it is good to see minimal MVC payments as it suggests producers are healthy, but they do provide quite a bit of stability to cash flow. As you can see below, volumes across HESM's systems improved from last year as Hess has grown production and grown into these commitments. There was 7% gas volume growth, 17% terminalling growth, and 19% water gathering growth.

{kind=link}

The remaining 15% of revenue is protected by cost of service contracts, which have inflation riders to ensure that HESM's initial rate of return is sustained. This is analogous to regulated utilities with approved returns on capital deployed. These agreements mainly relate to water transportation, as well as some gas transportation. The structure of its contracts provides tremendous visibility and stability to HESM's cash flow.

That proved to be true in the quarter. Adjusted EBITDA of $271 million was up from $254 million as higher volumes and inflation-riders provided growth. At the same time, cap-ex has been holding steady at a ~$225 million run-rate, which should continue to be the case over the next two years, leading to free cash flow of $163 million. For MLP investors, distributable cash flow ((DCF)) is key, as this measures cash flow less maintenance cap-ex, which in turn supports the distribution. In the quarter, DCF was $224 million, up from $215 million last year. This provided 1.6x coverage.

HESM targets a 1.4x coverage ratio and 5% dividend growth. Currently, it has a higher coverage ratio, and over the past five years, Hess Midstream has increased its dividend by 12% . Thanks to this strong excess cash flow, it has exceeded dividend growth targets and bought back $1.4 billion of stock over the past three years.

Additionally, its balance sheet is healthy with debt to EBITDA of just 3x, a reasonable level given the stability of its cash flow. With modest growth spending and benefits from rising volumes in contracts, EBITDA and free cash flow should rise 10% over the next two years, which will bring debt to EBITDA down to 2.5x and provide $1 billion of capacity for share buybacks as well as at least 5% distribution growth.

In the seasonally slower Q4, HESM expects EBITDA to be $270 million and free cash flow to be $160 million, essentially stable from Q3. As a result, management raised EBITDA guidance to $1.03 billion from $1-1.03 billion previously. Free cash flow should be about $635 million from $610 million previously. HESM is an MLP with very stable cash flows and solid growth prospects. With an 8% yield and 5-10% annual growth, it can generate medium-term returns in the mid-teens for investors as a stand-alone entity.

In October, Chevron announced it would be acquiring Hess in an all-stock deal, which should close next year. To be clear, Chevron has only agreed to acquire HES; there is no agreement with HESM. It is not known if CVX has discussed a HESM purchase, though it has undoubtedly examined its assets and financial position while doing due diligence on HES. Based on its history and the logic of the HES deal, let me explain why I see a purchase offer as likely after the HES deal closes.

After acquiring Noble Energy, Chevron later acquired its MLP, Noble Energy Midstream Partners, even raising its offer to complete the deal. For a company of Chevron's size, having a small MLP providing infrastructure support to just a small subset of its assets is not necessary and more likely to be a nuisance as it would likely prefer to manage all midstream assets holistically rather than having a subset of acreage and wells tied to a separate set of transportation agreements.

Indeed, part of the rationale of its Hess purchase is to gain scale across key US basins to find synergies and reduce costs. Maintaining separate transportation networks runs entirely counter to this goal. Ultimately, Chevron will want to get approval for and close the Hess deal first, at which point it can pivot to dealing with Hess Midstream, similar to its cadence with Noble. By acquiring Hess, CVX also will acquire its 38% stake in Midstream.

As such, Chevron needs to only buy out the remaining 62%, reducing the purchase price to $4.4 billion at its current valuation. Pro-forma for the Hess transaction, CVX's market capitalization will be over $320 billion, making this purchase under 1.5% of its value, little more than a rounding error, frankly. This is not to say Chevron will pay any price to take out HESM - its management team is very disciplined. That said, paying a 15-20% premium, or $800 million to have the synergy benefits entirely in-house and reduce the distraction of a small outside entity, is likely to be viewed as an accretive decision by CVX management, in my view. That is especially true when the 20% premium for HESM is equal to less than 0.3% of Chevron's own market value.

I view shares as extremely attractive at an 8% yield, given the strong coverage and free cash flow generation. HESM has likely traded at a bit of a discount given its dependence on Hess, but now it will provide services for an even stronger entity. I think shares are attractive at least to a 6% yield, given that 5+% dividend growth is likely, if not conservative. That would provide a 33% upside past $41. Given its strong stand-alone economics, if Chevron seeks to buy HESM next year, I think it will likely have to pay over $40 to win shareholder approval for the purchase. I see significant upside, and in the meantime, investors are paid to wait with that 8% yield. HESM is a compelling buy.

For further details see:

Hess Midstream Offers A Secure 8% Yield With Possible M&A Upside