HESM - Hess Midstream Offers Both Safety And An Increasing Dividend

2023-06-02 07:29:52 ET

Summary

- Hess Midstream offers investors a mix of safety and income, with a strong balance sheet profile and downside-protected contracts.

- The company has a free cash flow yield of about 10% based on 2023 projections and pays out a dividend yield of around 8.4%.

- HESM is expected to see solid growth as its parent re-ramps activity in the Bakken.

Hess Midstream ( HESM ) is a midstream gatherer and processor (G&P) that offers investors an intriguing mix of safety and income.

Company Profile

HESM owns an integrated system of oil, gas, and produced water handling assets primarily in the Bakken and Three Forks shale plays in North Dakota. Substantially all its revenue comes from providing midstream services to its parent, oil giant Hess ( HES ). HESM is an Up-C Corp following its conversion from an MLP in 2019.

The company operates in three segments.

Assets – Gathering Business (~50% of EBITDA)

HESM’s Gathering Business, which consists of a system of crude oil, natural gas, and water gathering pipelines that extend nearly 2,200 miles, accounts for approximately 50% of its EBITDA.

On the gas side, it has approximately 1,380 miles of natural gas and NGL gathering pipelines, as well as 410 MMcf/d compression capacity. On the crude side, the company has approximately 560 miles of crude gathering pipelines with 240 MBbl/d of gathering capacity. With 2023 crude gathering guidance of 95-105 MBbl/d, the system has plenty of capacity to handle increased volumes. It has 290 miles of water gathering and disposal pipelines.

Assets – Processing & Storage Business (~40% of EBITDA)

HESM’s Processing & Storage business, which can process up to 500MMcf/d of gas, accounts for approximately 40% of its EBITDA.

The crown jewel of this segment is its Tioga Gas Plant, which has overall plant capacity to 400MMcf/d. The plant also has natural gas liquids ((NGL)) throughput capacity of 80,000 barrels per day and can store approximately 80,000 barrels of NGLs for export via three pipelines and the Tioga Rail Terminal. In addition, the plant has tanks to store approximately 35,000 barrels of propane, 10,000 barrels of butane, and 35,000 barrels of natural gasoline.

Assets – Terminaling and Export (~11% of EBITDA)

The smallest segment for HESM is its Terminaling and Export Business, which generates approximately 11% of its EBITDA. The segment includes a truck and pipeline terminal, a rail terminal and rail cars, and a header system.

Its Ramberg Terminal Facility can receive 130 MBbl/d of crude oil through its crude oil gathering system and another 70 MBbl/d via truck. The facility can redeliver up to approximately 285,000 barrels per day and has storage capacity of about 40,000 barrels. HESM’s Tioga Rail terminal, meanwhile can handle 140 MBbl/d of crude oil and 30 MBbl/d of NGLs. It can also store approximately 290,000 barrels on site.

Contracts (100% fee-based with MVCs)

Nearly 100% of HESM’s revenue comes from fee-based contracts and as such it has minimal direct commodity exposure. The contracts, meanwhile, have CPI escalators that are capped at 3%.

What is unique about HESM’s contracts is that for the first initial phase, the contracts have an annual fee recalculation to maintain a targeted return on capital deployed whereby fees get adjusted for changes in actual and forecasted volume/capex and budgeted OpEx. So basically, the G&P is initially getting a guaranteed return on its growth capex spending.

Meanwhile, HESM also receives minimum volume commitments (MVCs) that get set on a rolling 3-year basis. The MVCs are equal to 80% of Hess’ nominations in each development plan that apply on a three-year rolling basis such that MVCs are set for the three years following the most recent nomination.

Following the initial phase, fees will be based on the average rate over the past three years with the same CPI escalation and MVC methodology in place. The majority of HESM’s contracts will switch to this method in 2024. Fees cannot be changed or reduced once set. These contracts run through year-end 2033, with one gathering subsystem contract ending in 2028.

Opportunities

HESM should continue to see solid growth as its parent re-ramps activity back up in the Bakken and it adds more compression capacity on its systems. The oil giant plans to bring 110 wells online in 2023. Production for Q1 rose to 163,000 BOE/d, and is expected to be between 165,000-170,000 BOE is Q2.

HES claims it has 2,000 future drilling locations that can generate strong financial returns at a $60 per barrel WTI price, giving it 15 years of drilling inventory. Meanwhile, the plan appears for HES to get to 200,000 Boe/d and hold it steady for the next decade.

At a J.P. Morgan conference last year, HES CEO John Hess said:

“We've always said that we were producing 200,000 barrels a day of oil equivalent before COVID will be at 200,000 barrels a day. And I think this year, the guidance is 160 to 165, maybe at the lower end of that number. On average for the year, even though you got the higher number in the fourth quarter. But what this should do is allow us to get to 200,000 barrels a day in 2024. But then we hold it on plateau. We're not going to be adding a fifth rig in the Bakken. The fourth rig is the optimal number for returns, for optimizing inventory, for optimizing free cash flow. So that 200,000 barrels a day will come sooner, and it should extend the plateau at 200,000 barrels a day potentially to the end of the decade.”

Beyond that, HESM should have some opportunities to grow via expanding its water business and capturing more third-party volumes. Right now, 3rd party producers only account for about 10% of its volumes. The company has also shown it’s willing to make accretive acquisitions.

That said, after 2024, HESM could become much more of a financial engineering story. EBITDA growth (2024 consensus is $1.14B) combined with total CapEx potentially falling to around $100 million annually, could see HESM generating free cash flow in excess of $850 million in 2024, or around $300 million after paying out around $2.40 a share in distributions. This type of flexibility can then create a flywheel effect whereby buying back shares or reducing debt creates even greater free cash flow after distributions.

Risks

No stock is risk free, and HESM is no exception.

One the biggest risks is that the G&P was receiving MVC shortfall payments in 2022 and those MVCs will be reduced in 2023. HES reduced the number of rigs on the acreage to only 2 in 2020 and into 2021, which caused production to peak in 2020 at around 193,000 Boe/d and fall to 154,000 Boe/d in 2022.

{kind=link}

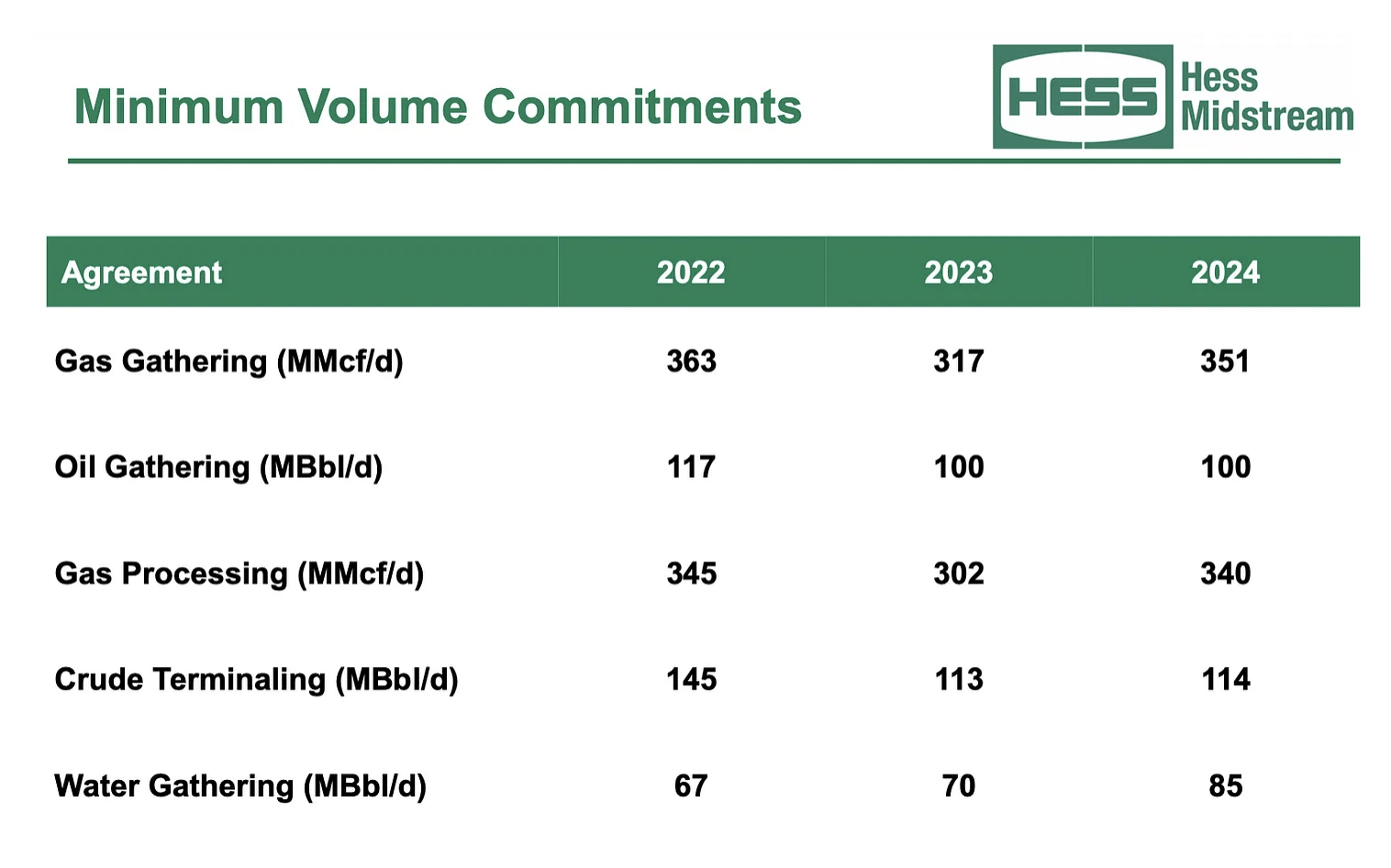

MVCs 2022-24 (Company Presentation )

{kind=link}

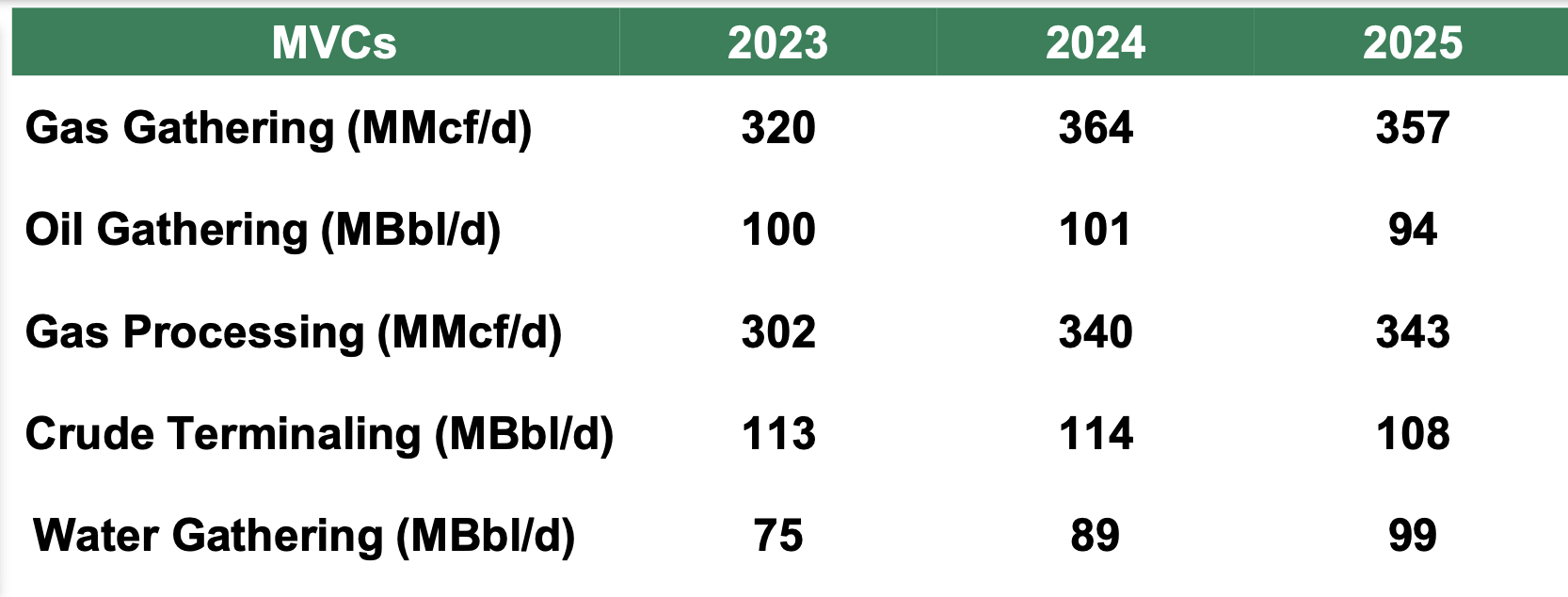

Updated MVCs 2023-25 (Company Presentation )

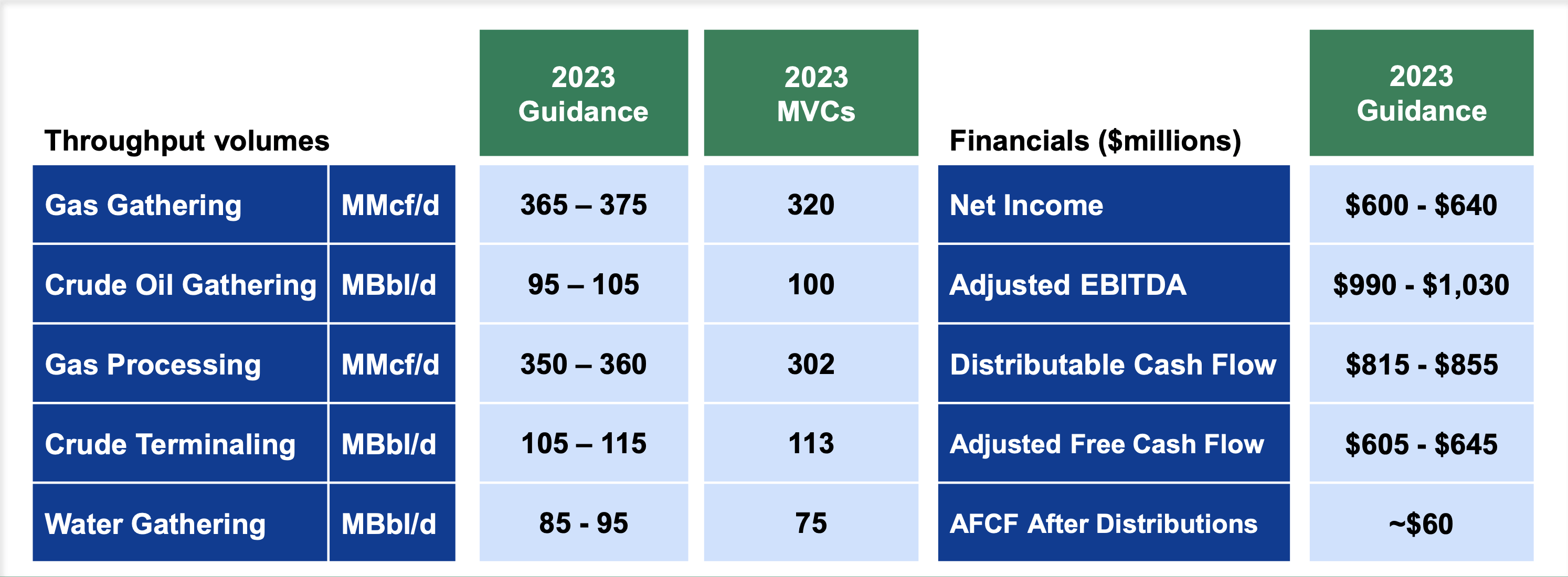

However, the oil giant added a 4th rig to the system in July of 2022, which is expected to help ramp production to approximately 200,000 Boe/d by 2024 and above MVCs in 2023 and 2024. Both gas gathering and processing volumes are forecast to be above 2022 MVC levels, although crude gathering and terminaling will be below.

{kind=link}

Company Presentation

The price of oil is another risk for HESM, despite minimal direct exposure. While a lot of its assets and revenue stem from natural gas, make no mistake, HES is drilling oil wells in the Bakken and HESM’s natural gas revenues come from associated natural gas from this oil drilling. Thus, lower oil prices can lead to less drilling causing lower production, which can negatively impact volumes on its systems. This was obviously seen the past few years, where HES cut back rigs during COVID leading to later production declines. HESM’s MVCs give it some solid protection, but it could still see EBITDA declines.

The dependance on one primary customer is also a risk. On the plus side, HES is one of the strongest oil majors around. However, Guyana, with its $25-35 oil breakeven prices, is its biggest growth driver, not the Bakken. We’ve also seen some upstream-midstream divorces, with some going well and some not. The EQT ( EQT ) – Equitrans ( ETRN ) split has been a clear example of the latter.

HES owns around 40% of HESM, as does GIP. The two firms, however, recently sold shares via a secondary , and HESM has also been buying back shares from the two as well. This is another potential risk that can weigh on shares, as its two large shareholders reduce their positions.

Valuation

Turning to valuation, HESM stock trades at 9.4x the 2023 EBITDA consensus of $1.03 billion. Based on the 2024 EBITDA consensus of $1.14 billion, it is valued at 8.5x.

The stock has a free cash flow yield of about 10% based on 2023 projections calling for $625 million in FCF. And it pays out a dividend yield of ~8.4%. It plans to grow its distribution 5% annually at least through 2024.

The company was leveraged 3x at the end of Q1. It anticipated getting to under 2.5x leverage by the end of 2025.

Conclusion

An investment in HESM isn’t going to make you rich. However, for investors looking for a relatively safe, high-yield investment, HESM fits the bill.

The G&P has a strong balance sheet profile combined with downside protected contracts, strong cash flow, and a solid history of growing its distribution. Meanwhile, the potential financial engineering story is intriguing.

The stock currently yields 8.4% on a run-rate basis, and I’d expect the distribution to continue to steadily grow.

I think most gains will come from distributions, but that investors can also expect some capital appreciation over the next few years. I look at a target of around $33 (about a 9.5x multiple on 2024 estimates), which combined with distributions could give you a return of approximately 40% over a three-year period.

For further details see:

Hess Midstream Offers Both Safety And An Increasing Dividend