HXGBF - Hexagon: An Appealing Play On Sensor And Automation But Expensive

2023-04-28 11:37:40 ET

Summary

- In this article, I'm going to be reviewing Swedish business Hexagon AB. It's the first SA article on the company. It's in a very interesting niche and may offer value.

- I mainly approach this company through the use of options at this time - but should the valuation drop below a certain level, I will go in more seriously.

- In this article, we'll review the company from a higher, but also a more granular level as we delve into the business.

Dear readers/subscribers,

By the time I'm finished with this article, I'm willing to wager that you'll be interested in Hexagon AB (HXGBF). Why do I think that? Because this is a very interesting company - and it does something pretty rare. Hexagon does have peers, but most of those peers have an incomparable mix. It's a software industrial/automation business, but in subsegments and niches, you do not often see.

So, let's not waste any time and start presenting Hexagon here. The company has been around since 1992, has annual revenues of around 35B SEK, and employs over 20,000 people across a multitude of subsidiaries around the globe.

Let's see what Hexagon may offer you.

Hexagon - Reviewing a positioning business

Hexagon AB is a Swedish conglomerate owning a number of subsidiaries. This is a bit of a "sleeper" stock. Usually, if someone tells me that they know Hexagon, my reaction is that "oh, they really know the market pretty well." Because people who only skim the surface of the market usually have no idea what this company is.

Hexagon is dual-listed, with a B-share listing on the Stockholm Stock Exchange, but with a secondary listing on the SWX Swiss exchange. That's your first clue. Swedish businesses, or any business in Europe don't just list on SWX for no reason.

So what does Hexagon do, exactly?

Hexagon is in the business of Geospatial Solutions, or GES as well as Industrial enterprise solutions. In these two segments, the company combines its expertise in sensors , specifically location sensors, including things like laser scanners, airborne cameras, UAVs, mapping technologies, and macro/micro-positioning. Essentially, if you have the need for incredible precision when positioning something, Hexagon is a partner you probably work with.

The segments here are huge, and the products are diverse. We're talking about everything from GPS systems, laser search systems, sensors, and the software to go with the sensors. End markets include everything from infrastructure, and geographical information systems when it comes to macro, while micro products are used in the automotive and aerospace industries, energy, medicine, and design industry. Things like Wind power wouldn't work without the technology Hexagon provides.

{kind=link}

When it comes to the world moving away from Fossil fuels, Hexagon plays an absolutely major role in this development. Through its technology, Hexagon enables data-driven solutions that enable companies to move efficiently into the new world.

Hexagon actually breaks, in part, one of my fundamental rules of investing. That of understanding what you buy. I understand that Hexagon is a company that leverages data, and has a market leadership in two core technologies that allow customers to realize the full potential of data - Positioning, Design/Simulation, Location Intelligence, Autonomous tech, and Reality Capture. By having technology leadership in these areas, the company has put itself in a position where many customers have difficulty operating efficiently without them.

{kind=link}

However, and to be clear, some of what Hexagon does - and I've had someone with a Ph.D explain this to me, goes above my head. The company uses proprietary technology, specifically a platform called Xalt, to facilitate efficient collaboration and streamline processes - tailored to the industry or segment where the customer operates.

Hexagon IR (Hexagon IR)

Some of you might be a bit questioned at such a description of a company. After all, it sounds like a mix or version of a modern "growth" business like Palantir ( PLTR ) - but this is very far from the truth.

Hexagon is a proven, profitable, sector-leading business. It has averaged 8-12% average revenue growth per year, 5-7% of which is purely organic and the rest from accreditive M&A's, which the company does expertly. The company also operates at a 30% adjusted operating profit margin.

The company is an extremely predictable grower. It's also a 97th-percentile gross margin company in the entire hardware industry and operates at a net margin of close to 20%. That's, again, at the 93rd percentile in a peer group that includes business like Keyence Corp. The closest relevant peers that could be argued to be on the same level is something like Garmin ( GRMN ), but even Garmin, as much as I love the business and its products, does only a smidgeon of what Hexagon does. Hexagon is the 2nd-largest business by market cap in its industry on the planet.

And, whenever in doubt about a company, trust the math first.

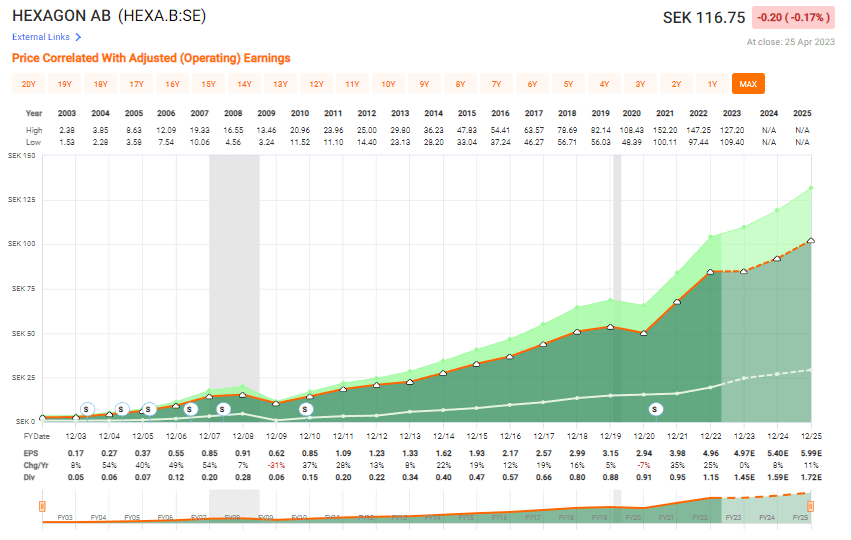

Well, the math for Hexagon on a 20-year basis isn't just good, it's averaged superb growth rates, with only 2 negative years during those 20.

Hexagon EPS 20-year (F.A.S.T Graphs)

{kind=link}

This comes to a 17% growth rate on average per year. Again, the math here speaks for itself. If you invested in Hexagon back in -03, you would have averaged an annual RoR of 23.7%, or a total of 7,464.05% with dividends since 2003.

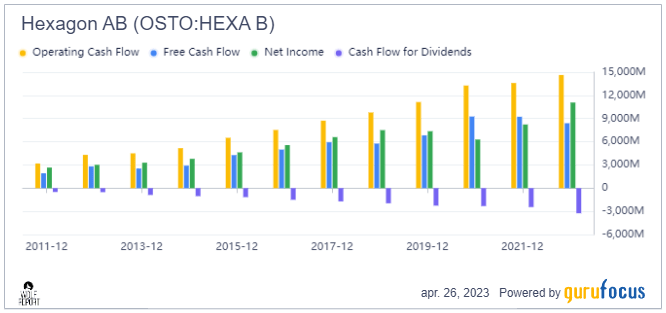

So, let me state this clearly; Hexagon AB is a superb business, and it's proven this through multiple ups and downs. It does not have much debt - less than 25% at debt/cap. It has one of the better fundamentals I've ever seen in this industry, and it's growing revenues at a good rate. Moreover, it's one of the most profitable businesses in this entire space, from gross, to operating, to net margins. Its cash flow trends could serve as a staircase.

Hexagon cash flows (GuruFocus)

{kind=link}

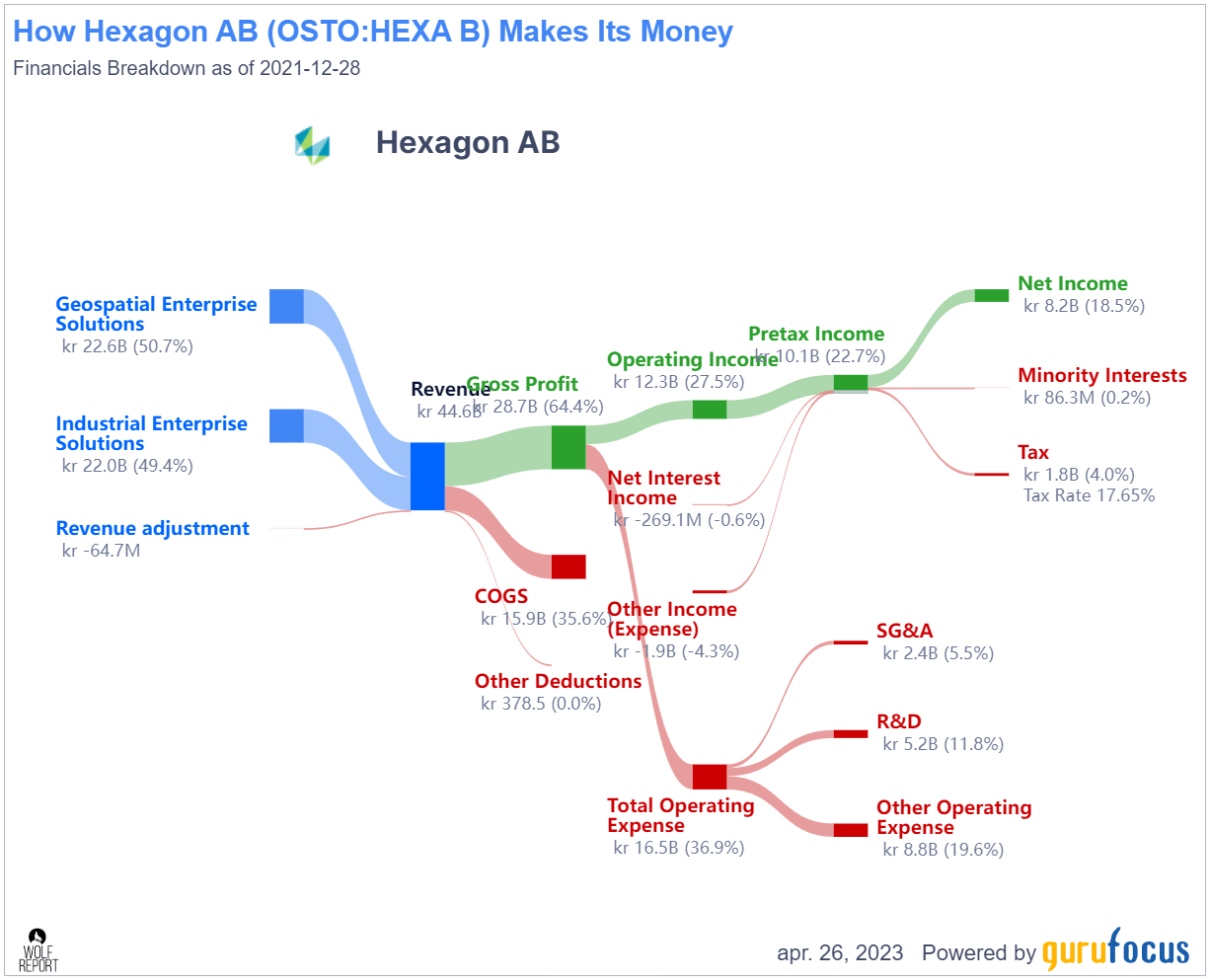

The way it earns its money, including 2022, is very clear. Compared to other businesses in the space and hardware overall, it has its cost structures under very good control.

Hexagon AB Rev/net (GuruFocus)

{kind=link}

Aside from the fact that actually understanding what it really is Hexagon does, aside from the generally "helping customers use data", the secondary drawback to this investment is its income from dividends. Hexagon is an extremely low-yielding company. Even now, in decline from its highs, it yields barely 1.15%.

Hexagon won't make you rich from dividend income - but it can certainly make you rich over longer periods of time. Hexagon is paying out around 25-35% of net, which in the segment comes to a very conservative target.

Overall, the company's operations are conducted by over 300 subsidiaries across 50 countries. Hexagon manages the group on a high level, but many of the subsidiaries operate rather independently. Despite challenges, 2022 results showed impressive growth and margin expansion.

{kind=link}

Hexagon's recent 1Q23 mostly confirmed the strong quality and potential upside, even with the current price. The company showcased strong momentum with an 8% top-line growth - also margin improvements on the gross side, as well on the operating side , despite the overall challenging current macro. On an adjusted basis, the company can now boast 67% gross margin, nearly 30% operating margin, and a cash conversion of 66% - as in how much of the cash flow is converted into net profit. 66% is impressively high for such a company. Companies can have very similar operating cash flow or cash flows overall, but very different net incomes. Conversion is one of the things I look at.

For the quarter, the IES segment especially showcased very strong trends.

{kind=link}

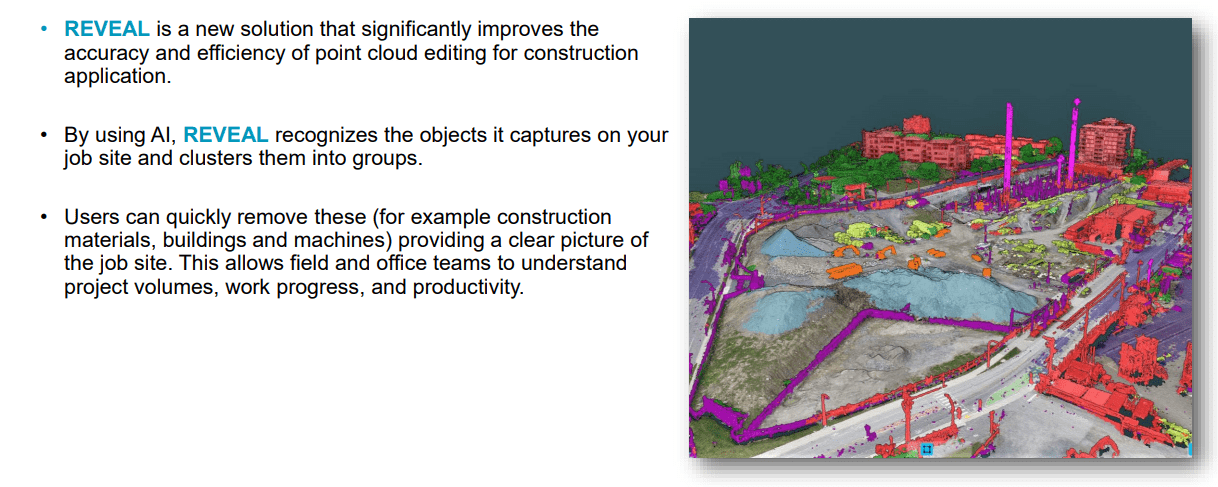

Some relevant news during the quarter. The company recently released its REVEAL system - an AI-solution for heavy construction.

{kind=link}

In other news, the company also launched its new smart city visual positioning systems, allowing users to connect to VR/AR and overall digital technology using 5G technology with unmatched accuracy. Hexagon also had several new program wins during the quarter, including a city in Georgia, BMW ( OTCPK:BMWYY ), And a Saudi Arabian governmental center, Transdev Australia and others. In short, the company's products are still highly in demand, and there is little sign that Hexagon is really slowing down to any particular degree.

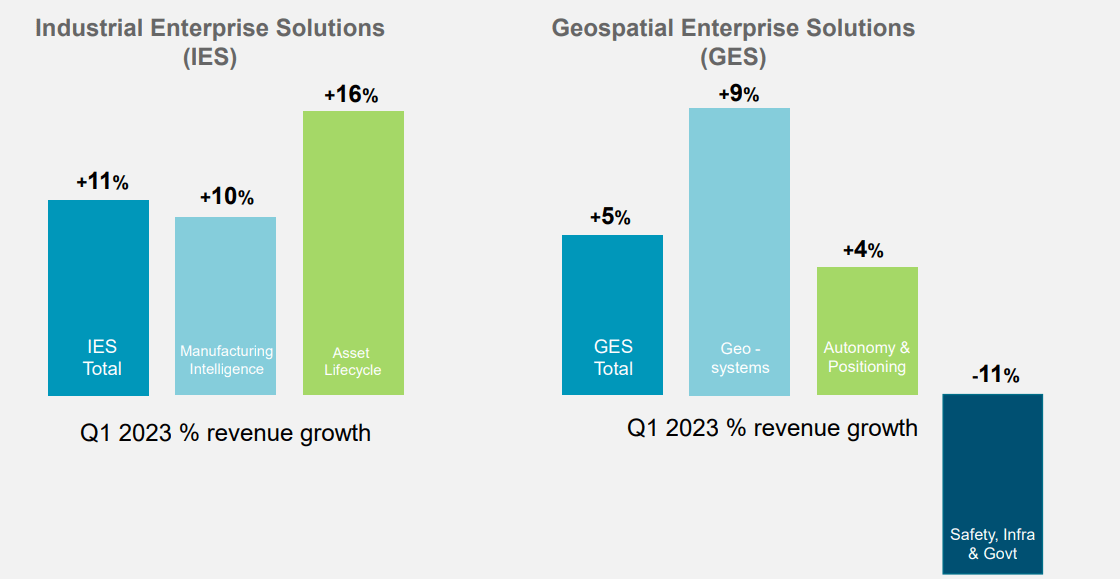

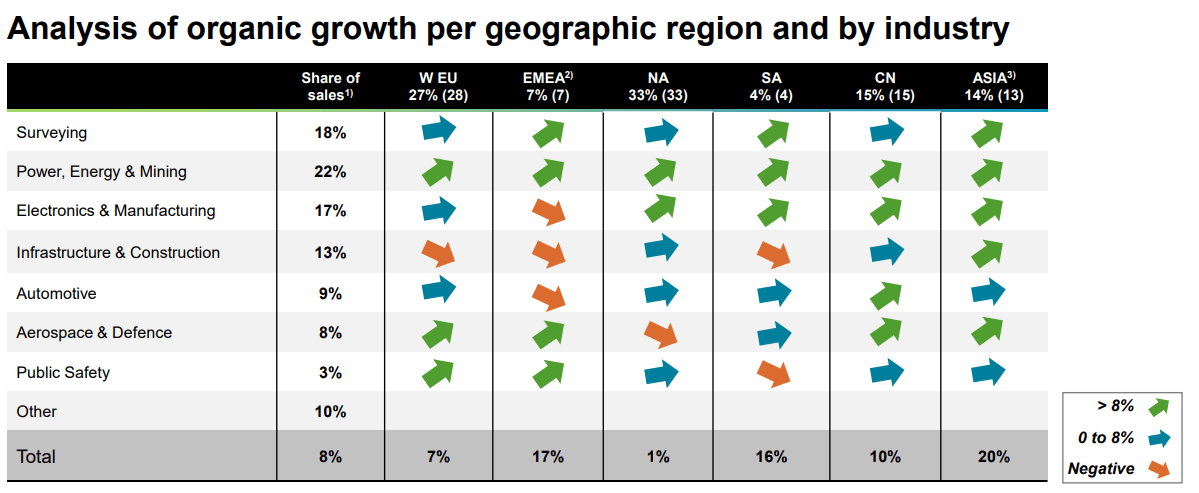

This is the current results in segments following Q1.

{kind=link}

Not much negative in the mix that isn't weighed up by positives. The company remains a seasonal business. If you dig down, you'll notice that 2Q and 4Q tend to be strong, 1Q and 3Q tend to be weak. Despite ongoing challenges, Hexagon is already inching close to its 2026E operating margin target of 30%. I see little reason why the company would fail to achieve this.

The company has exposure to cyclical segments like automotive and Aerospace, but it's overall usually a very well-diversified business - and something like surveying isn't exposed to the same ups and downs as some of the more cyclical segments. The main risks many investors see in Hexagon are exposures to some more cyclical geographies like China and other parts of the emerging markets across the world. For the time being, for instance, while China is a dud for the company, non-Chinese markets like the Philippines, Vietnam, Malaysia, and other regions are actually massively positive for Hexagon.

Outside of the automotive and aerospace sectors, the company is also exposed to the CapEx cycle trends of the consumer electronics space, with upcycles seeing impressive demands for products, with downcycles mellowing that demand. However, given the diverse nature of its mix, I would say that beyond world-shaping events like the GFC or the COVID-19 trends, true downturns in Hexagon are very rare, as evidenced by its 20-year EPS trends.

The second problem with Hexagon at this particular time is simple.

It's not exactly cheap.

Hexagon valuation

So, it shouldn't come as a massive surprise to you that a quality company like Hexagon is rarely, if ever, cheap. A reverse DCF gives us a quick indication, given the predictability of its business, where an 8-12% EPS growth rate "should" put its fair value. Based on an 8-12% growth period, and a 6-8% in the terminal period (and I use very high targets here to make a point, don't worry), the implied FV with a discount rate of 10% comes to around 92 SEK/share, with a current stock price of over 116 SEK. That's where the problems begin. Hexagon over a 10-year period usually trades at a premium of 23-27x P/E and currently is at around 23.5x normalized, expecting a growth rate of exactly 0% for this year, due to a somewhat compressed CapEx cycle in consumer electronics, continued instability in automotive, and other concerns.

Analyst accuracy here is high. On a 2-year basis with a 20% MoE, FactSet analysts do not miss targets negatively on Hexagon. We have a hit ratio of 83%, or a positive miss ratio (meaning the company beat expectations) 17% of the time.

This gives me high confidence that my own forecasts based on similar scenarios, calling for a relatively flat 2023, followed by a slow ramp-up in 2024-2025E, is a realistic prospect.

However, the low dividend yield means that if you invest here, and even if the company keeps its premium of around 23.5x, you're likely to go home with an RoR of less than 2%.

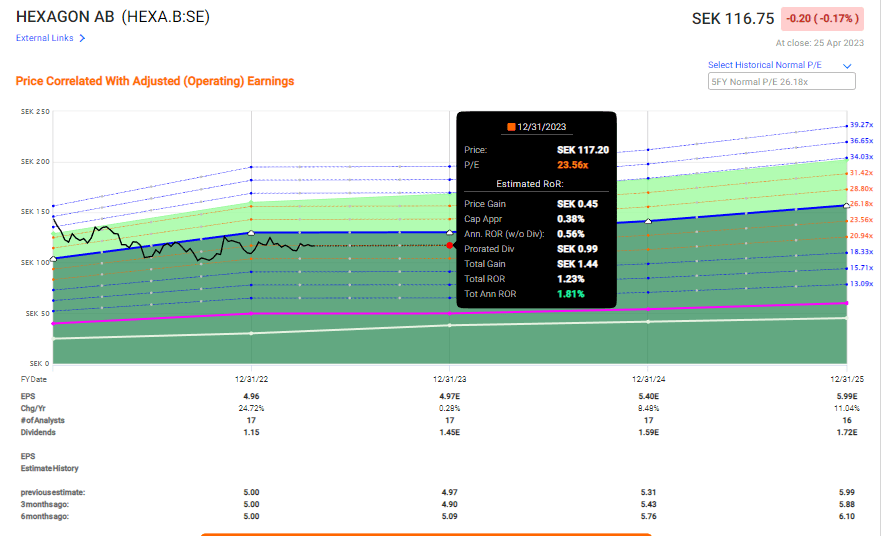

Hexagon Upside (F.A.S.T graphs)

{kind=link}

Longer-term, that upside is also "only" 8.4%. That's less than I would typically be looking for from a company with a less than 1.2% yield. Some other valuation numbers. S&P Global analysts have 16 followings the company, from a range of about 85 SEK to about 133 SEK on the high side, with an average of around 107 SEK. That means they consider the company overvalued around by 4% at this time.

I would put it in a way such as this.

I would prefer not to pay a triple-digit share price for Hexagon. At double digits, the upside here is conservative, for what the company offers, well into double digits per year. 3 analysts are at "BUY" here, with the remaining 13 either at "HOLD", "Underperform" or even "SELL" (one of them).

This translates into multiples as well. The company is at a relatively high sales multiple. 20-year average around 4x, currently around 5.51x. Revenue is typically around 6x, currently at around 6.18x.

Calling Hexagon a "BUY" at this juncture is possible only if you assume significant EPS and continued margin expansion, which may be possible, but perhaps in my opinion underestimates some of the more structural challenges facing not only Hexagon but the entire industry.

Also, and this is me moving into more granular know-how territory, Hexagon typically moves into very weak 1Qs, with 2Qs and 4Qs being strong due to the business seasonality. This means that we're heading straight into the weaker quarter, leaving plenty of potential for a downturn. This is a company I've researched extensively - starting with operations, but also going into valuation and cyclical trading trends.

My main M.O. for investing in Hexagon is related to writing attractively-priced cash-covered put options. This is something I have been doing for over a year. I've never been assigned, and always made around 8-11% in annualized yield on those options. If I do end up being assigned one of these days, it will be at a very attractive price.

For now, I say this to you as my initial thesis for Hexagon.

Thesis

- Hexagon is perhaps the most attractive positioning industrial/software company in the world. at the right price, this company becomes a must-have, and one you do not look "back" on until it's excessively overvalued. This company is extremely well-capitalized, attractively managed, and has expertise in future-proof global industries with a high upside.

- However, it's also very expensively priced and currently trades at least 4-5% overvalued to even a bullish share price.

- My PT for the company is double digits - below 100 SEK - to begin with - and for that reason, I'm at a "HOLD" here.

Remember, I'm all about : 1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company is neither cheap nor has a good enough upside, making it a "HOLD" here.

For further details see:

Hexagon: An Appealing Play On Sensor And Automation, But Expensive