HXGBF - Hexagon: Quality Continues To Matter Reiterate Hold

2023-06-23 03:27:23 ET

Summary

- Hexagon is a company I've been reviewing for the second time now - and I believe it's one of the highest-quality stocks out there in the field.

- My current approach is mostly focused on options trading due to the company's unfavorably high valuation.

- I give you my updated price target for the company and show you how I approach this investment from a valuation perspective.

Dear readers,

I wrote my first article on the Swedish company Hexagon ( HXGBF ) back in late April - and I made a wager with you, dear reader. Today I'm going to double down on that wager, and show you why I'm doing more put options as the company, as of today, is slightly dropping.

Let me show you once again why Hexagon, in the long term, is definitely a company that you want to own for the long term. You won't make mountains of dividends from this investment. It won't even make you rich quickly.

But I believe there to be a significant case to be made why this, at the right valuation, could be one of the most attractive players in the entire sector - and why it's a bit of a "hidden" gem because very few people seem to follow or know it - in part due to its subsidiary structure.

Let's review the company's recent trends and results.

Hexagon - More upside but hopefully it'll drop down further

As recently as today, I wrote a set of new cash-secured puts on Hexagon AB. Why did I do this?

Well, for one thing, the company fell slightly - and I was able to secure some not perfect, but decent options. I'm hoping to see a bit of a fall to a share price of about 100 SEK/share, which would open up some possibility for even better returns. But as the company is such an excellent operation, there's also some doubt as to if this will actually materialize.

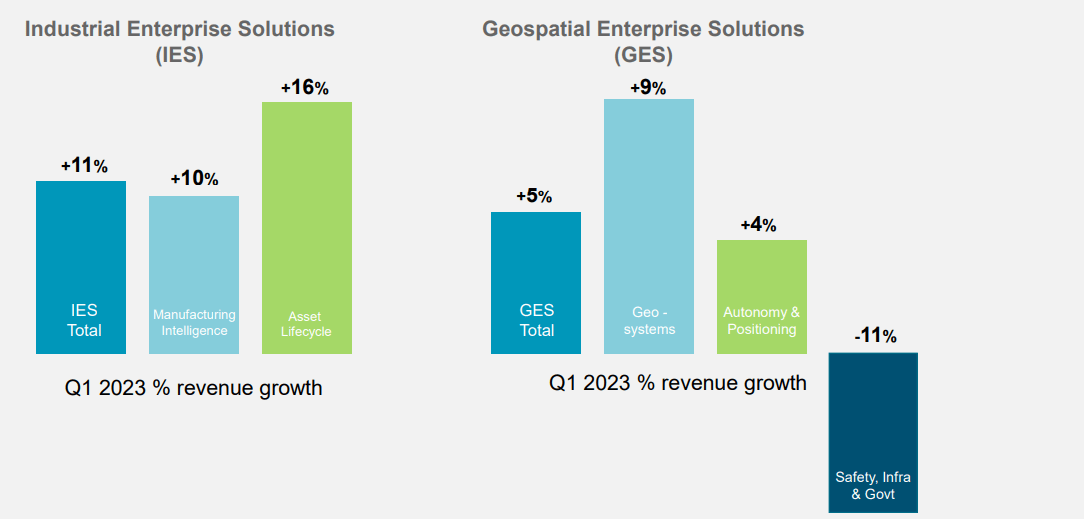

We have 1Q23, and despite the ongoing troubles across the world, the company is reporting strong sales growth of 8% with improvements in gross margins. Not many companies can claim that in this market environment - and to say it's worth highlighting is an understatement.

The company managed 8% organic growth, 66% cash conversion, 67% adjusted gross margins, and almost 30% operating margin while managing 2 acquisitions during the quarter as well.

The company is in IES and GES - or Industrial Enterprise solutions and Geospatial enterprise solutions. While there are subsectors of these sectors that are negative - safety, infrastructure, and government to be precise, there are also the segments that are showing upside - and those are most of them.

{kind=link}

Segment-specific trends, for a second. The GES segment, which is in the areas of surveying, positioning, machine control, mapping, 3d-scanning, and public safety saw significant sales growth and saw a positive impact from FX. Sales splits are attractive - almost 40% each in EMEA and the Americas, with only around 19% from Asia. Sales are primarily surveying and infrastructure, with other sub-sectors in the segment still ripe for growth - only single-digit percentages in most of them. The company is also starting to utilize AI to aid in its heavy construction sectors, which likely will be a major consideration going forward in the next 20-30 years due to the potential there.

{kind=link}

The company's tech is also very much applicable to the telecommunications industry, due to its smart 5G-enabled visual positioning system, as well as the new Digital reality platform.

Projectmate is one of the M&A's the company made in the sector. It brings with it knowledge from a SaaS-based construction management solution, which means that with the company's smart build-platform from HxGN, the company is able to provide a single source for all owners, making sure that project members have access to relevant data from one systems, linking owners to the job sites in actual real-time.

The company continues to win awards as well - the latest one is the Leica BLK360 Imaging laser scanner.

{kind=link}

To say the geosystems are doing well is an understatement. Even in the somewhat downer segment of Safety/infra/gov, the company has had several significant wins, such as BMW (BMWYY), as well as starting to work with various Middle Eastern countries that are growing significantly - such as Saudi Arabia.

{kind=link}

There is, simply put, plenty to like here. The company's sales split is appealingly diverse, even across multiple segments. It's 30-40% each in EMEA and Americas across the world.

The business has some of the best margins that you will find. A close to 30% operating margin turns into an over 20%+ net income margin, which you do not find often. The company also has one of the most impressive ROIC metrics I have seen in this entire sector, and it hasn't turned a negative net of WACC despite a growing cost of capital. Also, the company has successfully kept the SE portion of the assets at a relatively constant percentage, which means that shareholders are still owning a large, more than 50% portion of these assets, despite issuing some 15M shares back in 2021. Revenues have been climbing on par with net income, and this is yet another positive sign.

{kind=link}

Insider trades in this name are very few, and there isn't anyone motivated major shareholder for this business.

It's important to remember though - one of my cardinal rules when doing any investment at all is understanding what it is you're buying, being able to do the calculations yourself, and understanding where you're going. This is easy, or at the very least doable in many businesses. While I can forecast Hexagon and listen to what analysts expect, as well as management, when it comes to what the company actually does in detail, this is outside of the field of my understanding.

Some of what Hexagon does - and I've had someone with a Ph.D. explain this to me, goes above my head. The company uses proprietary technology, specifically a platform called Xalt, to facilitate efficient collaboration and streamline processes - tailored to the industry or segment where the customer operates.

Hexagon IR (Hexagon IR)

The basics are fairly understandable - but the details and how it does it, this is where I am left to having to have faith in company management knowing what they're doing. This is never a good position to be in - because if you do not understand this, it means you can't really understand how someone could do what Hexagon does better than them. This is the one flaw that I am trying to rectify with this particular investment.

To be clear, it's not that I don't understand the business - I just don't understand the details to a high enough degree to where I could confidently state peer appeals or lack thereof, or say when a competitor does something better than this company does.

Hexagon has been a market-beating investment for literally decades. Since 2003, your total RoR would be about 8,355.13% which is more than 2.5x the S&P Global RoR in the same timeframe, or 24.22%.

You cannot argue against this company - not in the long term, and at least not historically. If you had sold during overvaluation, your returns would have been even better. Then you could have taken home about 9,400% RoR, or 28% per year. Your original investment in the company would now be at a YoC of 71% per year , based on a 2003 share price of around 1.60 SEK, and a current dividend of 1.15 SEK.

Find me an investment that give you the same RoR - you won't find many.

That being said, we have a valuation issue - and I'll showcase it to you here.

Hexagon's Valuation - the One problem

The problem remains the company's massive valuation - and this is the reason why even in the most positive of forecasts, I can't do anything but go cash-secured puts here. it's the only way I can get the company for something resembling a fair value. I was able to write some CSPs close to the 100-SEK mark, which is the highest possible PT I'd be willing to buy the company at for the long term. I initially said that I wouldn't want to pay triple digits - and I remain at this stance - but at the same time, it might be an unrealistic overall expectation.

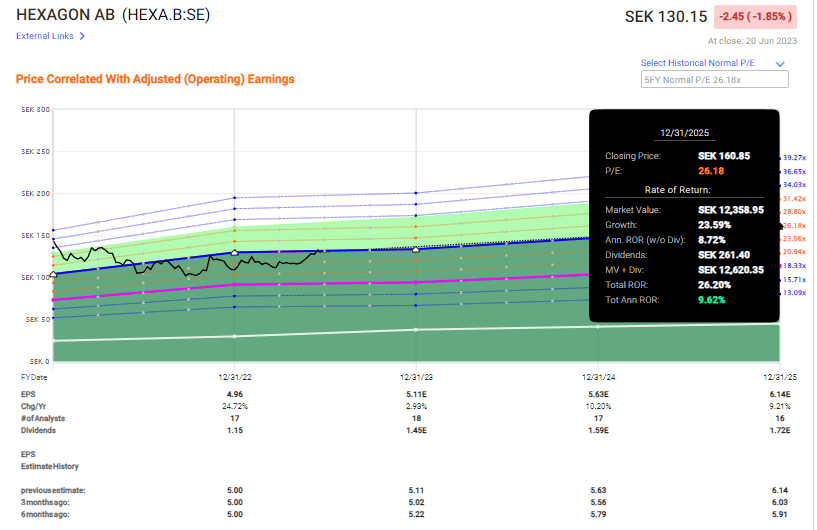

Normalized P/E valuations have the company at more or less the apex of its 5-year average here. The average is 26.18x - the current average weighted is around 25.9x.

This caps our theoretical upside at around 9.6% per year, or 26.2% until 2025E. The only good part about this company is that it tends, outside of extreme highs, to be far more stable than the overall market with a relatively low beta.

{kind=link}

However, at this valuation, I consider it too rich despite some very solid analyst forecast accuracy trends/history, and what I still retain is one of the best performances in the Swedish stock market over the long term.

The yield won't make you rich - for those of us investing now, it's 1%, maybe 1.1% if you're lucky.

Calling Hexagon a "BUY" at this time in June of 2023 is possible only if you assume significant EPS and continued margin expansion, which may be possible, but perhaps in my opinion underestimates some of the more structural challenges facing not only Hexagon but the entire industry. While the company hasn't been facing margin or inflationary pressures the same way, the trends in certain subsectors indicate at the very least the potential for more downward volatility.

If this materializes, you may be in for a period of below-average returns - and that would be less than ideal.

If this company ever becomes cheap, I'll jump on it. Until then, I'd follow the trends that most analysts call relevant here. A quick look at the S&P Global pricing targes from 16 analysts gives us an average from 88 SEK to 130 SEK, with an average of 107 SEK. At 107, I'd be writing CSPs in the 90s for all I was worth to make sure I have the potential to buy it cheap - potentially even buy some common shares.

For now though, only 1 analyst considers Hexagon to be a "BUY". The remaining 15 are at a mix of "HOLD", "Underperform" and even 1 "SELL", which is rare to see.

Thesis

- Hexagon is perhaps the most attractive positioning industrial/software company in the world. at the right price, this company becomes a must-have, and one you do not look "back" on until it's excessively overvalued. This company is extremely well-capitalized, attractively managed, and has expertise in future-proof global industries with a high upside.

- However, it's also very expensively priced and currently trades at least 4-5% overvalued to even a bullish share price.

- The trends in June of 2023 has not made this any easier, and any realistic upside is capped at single digits, as I see it. Single-digit upside isn't what I am looking for in this market, which is why I'm very tepid on the company and choose to go with some options as they become at least somewhat attractive.

- My PT for the company is preferably double digits - below 100 SEK - to begin with - and for that reason, I'm at a "HOLD" here.

Remember, I'm all about

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company is neither cheap nor has a good enough upside, making it a "HOLD" here.

For further details see:

Hexagon: Quality Continues To Matter, Reiterate Hold