HXGBF - Hexagon - Short-Seller Response And Good Entry Position - 'Buy'

2023-09-04 20:55:08 ET

Summary

- Hexagon has experienced a drop in share price due to a short-selling report.

- I do not believe the claims of fraud made by the short sellers, and consider the report flawed on more than one point. In this article, I go through errors.

- The drop in share price presents a potential entry point for investors in Hexagon. I continue to view it as a "BUY" here.

Dear readers/followers,

Since my last article on the company, Hexagon ( OTCPK:HXGBF ) (HXGBY) has been the target of a short-seller report that caused a very welcome drop in share price. Some of you have also contacted me and asked what I thought about this short report, and whether it somehow changes my thesis for Hexagon. While my buy-writes are nowhere close to materializing to where I would keep my shares, the report, and the following trends caused some interest in the company - and so, I'll be updating things here and giving you my opinion on the short report.

As you may know, if you follow my work, short-term trends don't really interest me. Unless there is a fundamental change in the outlook, negative trends only serve to make a stock more interesting to me.

The short version of my response to Viceroy is that I don't believe there to be any validity to the claims of fraud that the short sellers are alleging here.

Let's look at what's being said here, and why I believe this marks a potential entry point for Hexagon.

Looking at the company and the most recent trends

My overall thesis for Hexagon is a very positive one. I believe the company has proven, over a long period of time, that it's a capable allocator of capital, a skilled M&Aer, and able to grow its earnings organically. In fact, I view the company as probably one of the most attractive positioning software companies in the world, based on its expertise in some key segments. Peers in this specific industry are very rare, and even during some of the most complex operating environment specifics, this company still manages significant growth.

Hexagon IR (Hexagon IR)

With specifics like an 84% cash conversion, almost 30% EBIT margin and 66% adjusted gross margins , this company is an extremely profitable operator - and the company can prove and report on a quarterly basis the attraction and demand for its products. The latest quarters saw additions from Mineral Resources, Asia Air Survey, Mortenson, NVIDIA ( NVDA ), and others. (Source: Hexagon 2Q23 Report). Results including 8% revenue growth and a net sales increase of 6% together with a growing EBIT of 4% do not exactly spell "negative trends" for this company, even if this is what some would allege.

In this article, as I mentioned, I'm countering some points made by Viceroy. I invested in Hexagon and have researched the company thoroughly. At a good valuation, I believe this is one of the better software investments and industrial companies that can be bought, and I see a potential upside in the double digits.

Now for the report that elicited the article response from me.

In essence, Viceroy is alleging that the company is misrepresenting acquisition (inorganic) growth as organic growth and that the company's M&As actually seem to be underperforming. The exact wording here is:

Management have adopted an aggressive acquisition strategy which has remained largely unchanged for 25 years. Acquisition growth appears to be intentionally misreported as organic growth , which would otherwise rival LVMH. Acquisitions themselves appear to be underperforming en masse .

Aggressive accounting measures and corporate structure decisions put the lipstick on the pig . Dreadful and often non-existent disclosures appear to be a deliberate attempt to keep nosey critics at bay. Not us.

(Source: Viceroy )

Let's first look at who's making the allegations. I don't mind short-selling, in fact, I tend to view short sellers as they are viewed by fictional characters in the TV show "Billions". White blood cells detect danger and disease. If I've made the mistake of investing in a fraudulent or flawed company, then I'd want anyone who was competent or able to point this out to actually do so - and as quickly as possible.

But Viceroy research is far from the most capable or believable short seller out there, I believe. What makes me say this?

Because capable short sellers know where their limits are. They don't get fined for their accusal - which Viceroy has been ( Source ). They typically don't cross regulators, again which Viceroy has done, according to this same source.

The allegations made by the short sellers are very serious - but also very easy to, as I see it, disprove. Any company that's misrepresenting growth as Viceroy is alleging Hexagon to be doing would not be able to showcase a 16%+ annual EPS growth rate for the past 20 years - which Hexagon has, and which is set to continue going forward as well.

The company alleged that interim and annual report numbers were incorrect - and I've been through both the Viceroy report and the Hexagon response. My view is that Hexagon's response is correct. Furthermore, I argue that Viceroy doesn't seem to understand IFRS how it impacts related party transactions, and what, under IFRS, constitutes a related party. Overall, the report seems riddled with a lack of understanding of local laws and regulations.

One of the points made was the change of auditors back in 2021 - this was a mandated change by EU law by the EU Audit directive/regulation. There is a mandatory rotation of both audit firms and individual lead auditors at clearly defined time periods.

I've encountered Viceroy and their reports before - when they were looking at Swedish company SBB, they did a report there as well, and while the errors seemed not to be as clear there, there was a similar implication of complete lack of understanding of basic local/European practice.

The simple fact is that the allegations that Viceroy puts forward, would, as I see it, not be possible without severe manipulation of accounting. I see no such indications in the company's annual reports, and if there are mistakes, I believe that such mistakes are in the process of being cleared up - and if there were major ones, we'd have heard about it over a month after the fact.

As an example point, Viceroy in its reporting applies an EV/Sales multiple to annual acquisition proceeds to reach its "structure" or overall growth for around 15 individual acquisitions in the period. Using such a basic multiple for such a complex number of transactions and sizes is incredibly precise in order to calculate the contribution to growth from these transactions.

The viceroy also made multiple simple mistakes, either not reading or downright ignoring public disclosures of revenues or making very simple currency errors. This includes not being able to differentiate between Millions of Euros and MCNY (ZG Technologies, 2017-2022 M&As), not recognizing when a company was already 50%+ owned by Hexagon and fully consolidated , and so forth.

There are more examples. The company's rebuttal found here goes through some of these points, as well as many, many more.

But the simple and very obvious and inarguably amateurish mistakes put into question, as I see it, just what investment professionals (which I hope they do employ) work in finding short-selling targets and doing the work upon them.

Swedish companies, unfortunately, do not engage in legal responses to such reports - though with regards to the question if the company would have a case to make here, that's above my head.

The facts seem obvious to me, at least. So the question when it comes to how this impacts the long-term thesis for Hexagon, is that it doesn't - not negatively.

No, the change is positive - and to a very large degree.

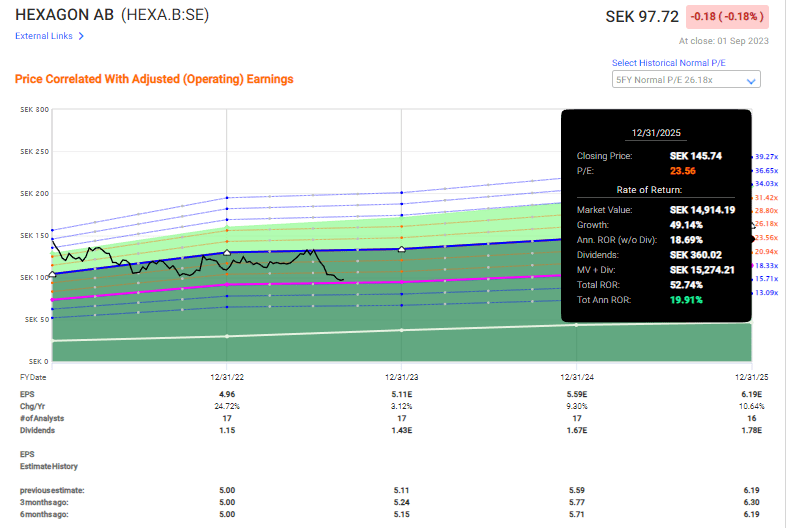

As a result of the short report, Hexagon is trading down more than 10% in a short time. The company has gone from above 24x P/E to below 20x P/E in only a few weeks, which the company hasn't been since COVID-19.

In my last article, I made it clear that the reason the company dropped after 2Q was in part at least, increasing costs for the company. Over the past 8 years, the company has reduced its WC as a percentage of sales from almost 20% down to less than 5-6%, but in the last two quarters, it's trended up, to where it now stands over 7.5%.

But the downturn for Hexagon is a positive one - both the earnings-induced downturn but also the short-seller downturn. It enables us to seriously invest in Hexagon at a very attractive price.

Let's look at current valuation trends.

Hexagon - 2Q23 and short-selling have made a realistic upside above 15% possible.

In my last article, you had to go to 26x P/E to find an annualized upside of above 15%. It's now possible to see almost 20% annually by forecasting the company to only 23.5x P/E. At 20x, the company upside is still 14%.

{kind=link}

F.A.S.T. Graphs Hexagon Upside (F.A.S.T. Graphs)

So, this decline has really improved our profitability in this investment. Analysts following Hexagon have not changed their targets for the business. It's still at an average of 103-107 SEK/share (Source: S&P Global).

I secured a buy-write at 85 SEK with a superb overall upside last I wrote about the company and when the drop began. Now I could either go for a deeper buy-write, or an even better upside, or buy the common shares.

I moved to "BUY" in my last article. I'm reiterating that "BUY" now, is even stronger than before. The short report allegations have no merit as I see it, and for this reason, I give you my updated this as follows for the company.

Thesis

- Hexagon is perhaps the most attractive positioning industrial/software company in the world. at the right price, this company becomes a must-have, and one you do not look "back" on until it's excessively overvalued. This company is extremely well-capitalized, attractively managed, and has expertise in future-proof global industries with a high upside.

- The trends in July of 2023 have now seen the company recover from what I view as overvaluation - and I am changing my rating to "BUY" for the company here - though it comes with caveats, and I would be careful about investing the "wrong way" here.

- My PT for the company is preferably double digits but at 103 SEK/share, I'm moving to "BUY" due to the reasons mentioned above

- Following the short-selling report, I doubled down on my previous share price, completely unchanged, and now say that the company has a significant upside of over 15% to a forward P/E of over 18-19x, but below 24x P/E.

Remember, I'm all about

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company is now at a good enough position to offer a double-digit upside, which makes it a "BUY" in my book - though there are better ways still of entering this investment at a good price.

For further details see:

Hexagon - Short-Seller Response And Good Entry Position - 'Buy'