HXGBF - Hexagon: Update After 2 Months Of Mostly Negative RoR I Still Say 'Buy'

2023-10-18 21:23:00 ET

Summary

- Hexagon's share price has become attractive, allowing for a 16.5% annualized rate of return through a covered call buy-write strategy.

- The company has seen a decline in its premium due to increasing costs, but its solid earnings growth history suggests potential upside.

- Hexagon's growth in key segments and contract wins indicate a positive long-term thesis, despite short-term challenges in certain markets.

Dear readers/followers,

I did not expect that I 2023 would be able to "BUY" Hexagon (HXGBY) at an actually attractive share price, and go long in my portfolio. But this is exactly what has happened. Through a combination of attractively-priced Puts and Calls, I have been able to trade both the downside and the upside of this company, but I recently added a non-trivial position of the company tied to a covered call buy-write, which ensures a 16.5% annualized rate of return until mid-next year unless the company falls below a very unlikely (based on my estimates) level.

I've also been adding common shares to my corporate portfolio, now that the company has seen some decline that's actually made those prices attractive for the first time in a very long time.

Previously, Calling Hexagon a "BUY" has been possible only if you assume significant EPS and continued margin expansion, which may be possible, but perhaps in my opinion underestimates some of the more structural challenges facing not only Hexagon but the entire industry.

Hexagon very rarely shows bad or negative trends in their earnings - but it does happen, and I also expect it to happen more going forward - but this doesn't mean that the company isn't an interesting investment here.

Let's look at the upside now that we're 6% lower than my last article, which you can find here.

Hexagon - One of the few companies I "BUY" at a premium

2Q23 was the catalyst for the downturn that declined the company's premium by a significant amount. Despite strong organic growth of 8%, 84% cash conversion, 66% adjusted gross margins, and almost 30% operating margins, the company still fell - so I would say that the decline was overdone. It's also why I decided to go deeper with new option contracts and even added common shares when the company hit 98 SEK/share not long ago.

Including the last article, the company is now down more than 15% - and this, being a value investor, is obviously something I welcome.

Why is the company down, as I see it?

The increased cost of debt and increased manufacturing/wage/service/ transport/overall inflation has been the "broad-stroke" reason for why companies are losing the premiums they have been holding for more or less the entire period that we've had low interest rates.

I would put relevance to the results, not to the short report by short-seller Viceroy, which I view as not relevant to the long-term thesis - or really anything relevant. Hexagon has already officially dismissed the short-seller allegation, and I've covered this in detail in my previous articles on Hexagon.

The short of it, with regards to that report, is that I share the company's view that they've gotten their facts completely wrong.

While interest rates and cost of debt have the inevitable result of impacting a company's margins, unless we're talking about a company with zero debt (and even then, cost increases are very relevant), we already know that the markets have a strong tendency towards overreaction, both on the negative and positive side of the spectrum.

The latest set of quarterly results in no way invalidates the longer-term positive thesis for the company. Growth both in the top and bottom line was found in GES, including the attractive Geosystems and A&P areas. The headwind for the quarter, and for the company at this time, was development in the Infrastructure, Positioning, and safety segment, which followed the overall macro development of the market and fell by nearly double-digits.

With continued contract wins across the world though, I view such trends as limited in their scope. Worth mentioning in this context is a contract with a global leader (name undisclosed) in the semiconductor industry, with over 100,000 employees and 50,000 external contractors.

Obviously, Hexagon with its history also has plans for improving current trends. We're talking about a new efficiency program that's set to save over €150M, annualizing €160-€170M over the next few years, with a full run rate from early 2025. Hexagon is in the process of cutting offices and facilities by 25% company-wide. As with most businesses, automation is the name of the game, and the net beneficiaries of these trends will be company shareholders - such as us.

Going forward, there are a few things to keep an eye on even with Hexagon trading at below 100 SEK/share. Given its exposure to Asia, the Chinese real estate and infrastructure market has the potential to be a result drag for a long time. Hexagon is obviously trying to offset these negative trends with sectors that are booming - in this case such as mining and VR/AR - but whenever you're shifting sectors, this is a long and somewhat volatile process.

Blaming just China doesn't really work either. The European construction market isn't much better, nor is the US one. Middle East and APAC-ex China is better here.

My initial reaction going into 2Q23 and now that we're deep in 3Q23 was to be thrilled at the downturn for the company. I remain in this position now, and I've also expanded my position in Hexagon. The company's growth in key segments like GES is to me, proof that the company will continue to grow in segments even while others are going down.

Hexagon is down due to increasing costs. That's it (as I see it). This makes it no different than any other company that is facing revaluation of its premium and upside due to increasing costs of debt, manufacturing, services, and inflation, which makes it a case about company quality and potential upside.

And thankfully, that potential upside is significant here.

Let me show you what we can expect from Hexagon for the next 1-2 years based on the current valuation.

Hexagon - The upside is now over 15% per year.

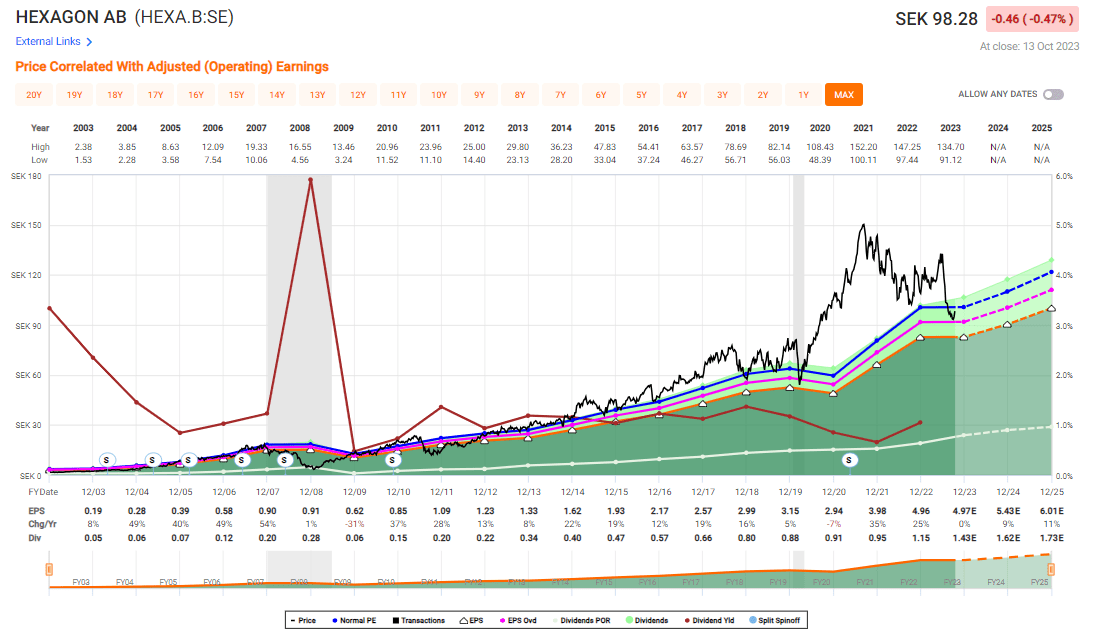

So, first of all, the premium. I consider the premium valid for this company given the absolutely solid earnings growth history, which you can see below.

{kind=link}

F.A.S.T Graphs Hexagon upside (F.A.S.T graphs)

This is an average EPS growth rate of 16% per year for the past 20 years - and even with the current trends, expecting no growth in 2023E, we're still with a company with a solid EPS growth trend with no forecast misses on a 2-year forward basis, with beating those forecasts more than 15% of the time.

That being said, you can see how premiumized the company has been for many years here. We need to discount it somewhat because over 140 SEK for Hexagon is a ridiculous price and not one I intend to pay.

In my last article, I gave the company a 103 SEK/share PT. This represents a forward price target of no more than 17.5x P/E. And even to that valuation, we have a significant upside. Likely the premium I would consider valid is a range between 17-21x P/E, not the 26.2x P/E we've seen on a 5-year average. The upside to that 21x P/E is now just around 15% annualized, which is why the company is such a great "BUY" here.

Unless you think the company is worth only 15x P/E or below any sort of premium, Hexagon becomes a buy here. Given its market-leading position, I cannot see myself giving the company any less than a 17-20x P/E premium. The company is a low-yielder, which needs to be kept in consideration - but nonetheless offers a good combination of excellent potential capital appreciation and some dividends.

S&P Global analysts follow Hexagon and give the company an average of 85 SEK to 140 SEK, with a mean target of 110 SEK/share. I go slightly below this target. Most analysts don't yet believe the "bottom is in". I can see this perspective as being at least somewhat valid, which is why my primary entry into Hexagon is still an option, both on the long and on the CSP side if the company declines to low enough levels. This is the advantage of options - you're able to dictate your prices, and going back to last fall in 2022 when I started incorporating options into my strategy, most of my "plays" (93.5%) have turned out as I expected, meaning out of the money - and over half of those that ended up going ITM are companies that I've kept long-term.

Hexagon is a perfect candidate for this sort of play. That's why primarily, I would still look at going the CSP or the Covered-Call Buy-write strategy, aiming for that 15% annualized RoR on a 4-12 month basis. It's been my experience that it's easier to get 15% on covered calls than on cash-secured puts, but I always check both.

The common shares have some appeal - but I would still say that given the company's potential to drop lower in the short term, the options play is still the stronger and safer way to go here.

Because of that, I give the company the following thesis here as of October of 2023.

Thesis

- Hexagon is perhaps the most attractive positioning industrial/software company in the world. at the right price, this company becomes a must-have, and one you do not look "back" on until it's excessively overvalued. This company is extremely well-capitalized, attractively managed, and has expertise in future-proof global industries with a high upside.

- The trends in October of 2023 have now seen the company recover from what I view as overvaluation - and I am maintaining my rating of "BUY" for the company here - though it comes with caveats, and I would be careful about investing the "wrong way" here, which is why I would go the options way above the common share investments here.

- My PT for the company is preferably double digits but at 103 SEK/share, I'm moving to "BUY" due to the reasons mentioned above

Remember, I'm all about

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company is now at a good enough position to offer a double-digit upside, which makes it a "BUY" in my book - though there are better ways still of entering this investment at a good price.

For further details see:

Hexagon: Update After 2 Months Of Mostly Negative RoR, I Still Say 'Buy'