HXGBY - Hexagon: Upside After Q2 - I Now Say That You Can 'Buy' (Rating Upgrade)

2023-08-01 05:10:36 ET

Summary

- Hexagon's 2Q23 report fell below analyst expectations, leading to a double-digit drop in stock price.

- Despite the decline, the company's overall growth in various segments remains strong, with significant contract wins. Hexagon is launching an efficiency program to reduce costs and increase savings for shareholders.

- I view the company as a "BUY" now, but I wouldn't go into the common share without some safety. I go through my investment approach here.

Dear readers/followers,

Hexagon ( HXGBY ) has been a company I've covered for a few articles at this point, ( Source ) lauding their technology and fundamentals, but viewed the company as a very clear "HOLD" due to the valuation premium inherent to the company.

Previously, Calling Hexagon a "BUY" has been possible only if you assume significant EPS and continued margin expansion, which may be possible, but perhaps in my opinion underestimates some of the more structural challenges facing not only Hexagon but the entire industry. I view this latest quarter as proof that hopes for such positive development were somewhat too high.

Remember, my way of earning money from Hexagon - not much, but some - has been short-term dated cash-secured puts in the '90s. I actually have a short-term CSP with an Aug '18 expiration currently running, with an effective cost basis of 87.90 SEK and an annualized RoR of 15.03% inclusive of fees. This was one of my most successful CSPs in the company ever, and if it does go through, I'll be thrilled.

I doubt it will, however. Instead, let's look at what the company can offer us going forward, and why I view a rating change to be relevant here.

Hexagon - Plenty to like after the drop

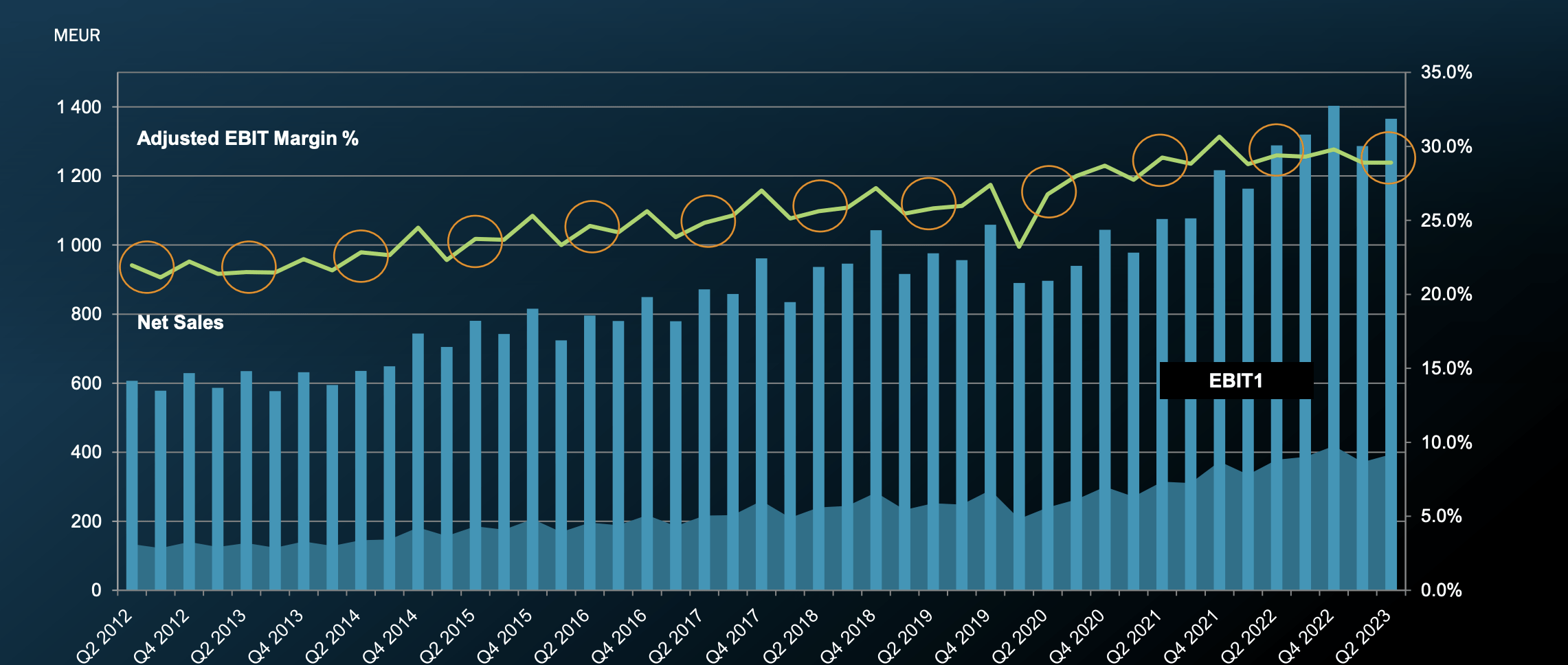

The reason Hexagon dropped was rather simple. The 2Q23 report ( Source ), which came mid-this week, was below analyst expectations. Despite strong organic growth of 8%, 84% cash conversion, 66% adjusted gross margins, and almost 30% operating margins, the company still fell. Some of this fall was sudden, but the fact is that the company has really been declining significantly for the past month or so.

Hexagon 1-month decline (Google Finance)

{kind=link}

Still, the company dropped double-digits - almost 11% during the trading day with the highest turnaround on the entire stock market on that day (the Swedish market).

The reason was simple. A combination of increased interest costs, and lower overall results. It always amazes me how many analysts and investors fail to account for simple things like this. I would put relevance to the results, not to the short report by short-seller Viceroy, which I view as not relevant to the long-term thesis - or really anything relevant. Hexagon has already officially dismissed the short-sellers allegation.

To me, this decline in valuation is a gift from above. I don't see any fundamental weakness in the company that justifies this sort of downturn - and we're slowly getting to a level where we really can consider the company an attractive play, something I've been wanting to do for several years.

{kind=link}

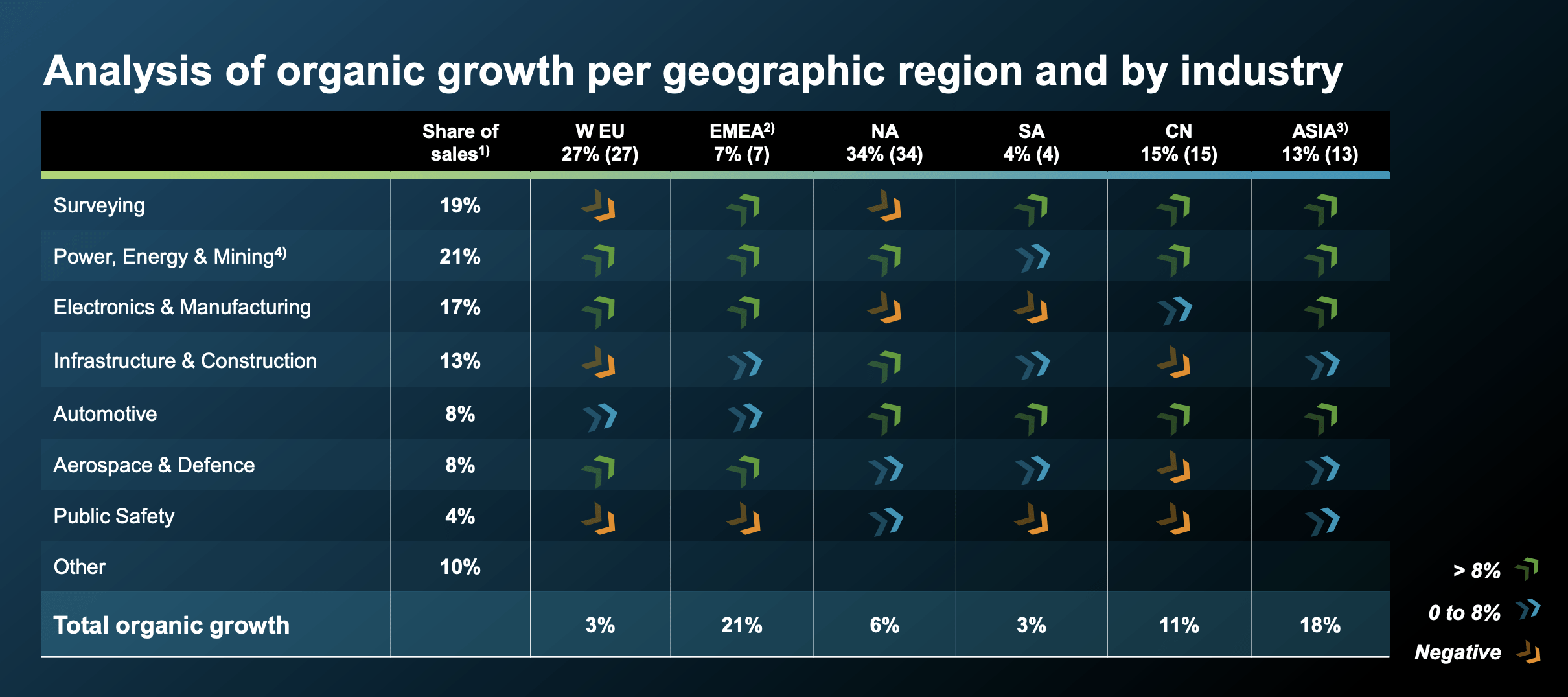

The company's overall growth not only in Manufacturing and Asset Lifecycle intelligence but in the entire GES segments, which includes Geosystems and A&P, was stellar. The literal only negative for the YoY quarter was the development in Safety, infrastructure, and positioning, which fell around 9%.

However, the company keeps winning contracts across the world, and none of them are really small or insignificant.

{kind=link}

The company also won a significant contract with a global leader (name undisclosed) in the semi-industry, with over 100,000 employees and 50,000 external contractors.

In response to increasing costs, the company is launching a new efficiency program, investing €200M during 3Q, but annualizing €160-€170M in savings over the next few years, with a full run rate from early -25. This includes cross-divisional cost savings, technical synergies, rationalizing non-core, and reducing office/facilities by over 25% company-wide, with more automation being introduced in the company. All changes are slated to deliver advantages and profit to shareholders like us.

Remember, the company does have seasonality in profits. And the fact that 2Q was better than expected in organic growth is not atypical, because the company's seasonal pattern has strong 2Q and 4Q.

{kind=link}

In short, the company fell on increasing costs. WC was also part of it. Over the past 8 years, the company has reduced its WC as a percentage of sales from almost 20% down to less than 5-6%, but in the last two quarters, it's trended up, to where it now stands over 7.5%. The company's positive trajectory is far from broken. Gross margins and operating margins are still trending very high - and I don't expect material worsening in the next few quarters here.

But the volatility and some interest expense can cause this sort of reaction in the company implies to us that there was a definite degree of overvaluation in Hexagon and that this normalization was a very positive one.

The things that are now affecting the companies are few. Foremost among them, I would argue is the incremental softness and lower demand related to construction and infrastructure, in particular from China's declining real estate and construction market. The company will be trying to offset this with gains in other sectors, such as mining and various types of reality. Hexagon has already increased its R&D spend towards these sectors for the past few years. Mining also has extremely good current momentum, which is offsetting those drops.

It's not just China that has a softening construction demand either. The same trends can be seen in the US, but also in Europe, especially in Germany. Middle East and APAC demand are better here, ex-the situation in China.

FX doesn't really impact the company much due to how things are structured. the increase in financial net is mostly from the higher interest rates, not FX - so the company is at the very least shielded from these.

I mentioned that the company has responded to the short report - that response was simply this:

Yes, look, I mean, we're coming out of a silent period. We've looked deeply into the report. And for sure, we're going to come back. And we think for us to do so for the sake of analysts and investors that have followed the group for a long time. As I said, we deeply disagree. We think that there's factual inaccuracies and there's allegations that deserve being responded to.

(Source: Paolo Guglielmini, 2Q23 earnings call)

The company has already announced that a more comprehensive response will be coming in the near future. Aside from the mixed appeal coming from the various divisions where essentially one division is weighing up shortcomings from another, I do not see a comprehensive set of forward risks to the negative side.

That's why I am thrilled at this downturn, and why I've been following the company very closely at this time. The underlying cash flow conversion rate is a real positive here because it shows continued strength even when certain markets and segments are declining. Specifically, the growth rate in A&P, with agriculture being a massive driver here (and also why I continue to invest in agri-adjacent or linked businesses, including fertilizer).

Let's look at a valuation for the company and what we can expect going forward here - also, why I'm changing my thesis at this time.

Hexagon Valuation - It's now getting interesting

I've said previously that the valuation where I would start to be interested is at around double digits or close to it. That's where we currently are. At or around the 100-SEK mark is the highest possible valuation that I would buy the common share. That's why my strategy at this time remains to look at both the cash-secured put avenue, as well as the buy-write CC strategy as primary entries into the company.

As I've said previously, and as is indicated on the CSPs I've written on Hexagon - my overall long-term target is a 13-16% annualized rate of return. I don't care much how I get it. I'll do interest rate savings combined with CSPs. I'll do conservative undervalued DGR investments. I'll do higher-yield reversal plays. I'll do buy-write CCs, owning the stock for a year and selling it at a good price (unless it drops to a price that I dictate as attractive). However I get those minimum 13-16%, usually around 15%, RoR, that's what I'll do.

And I want them safely.

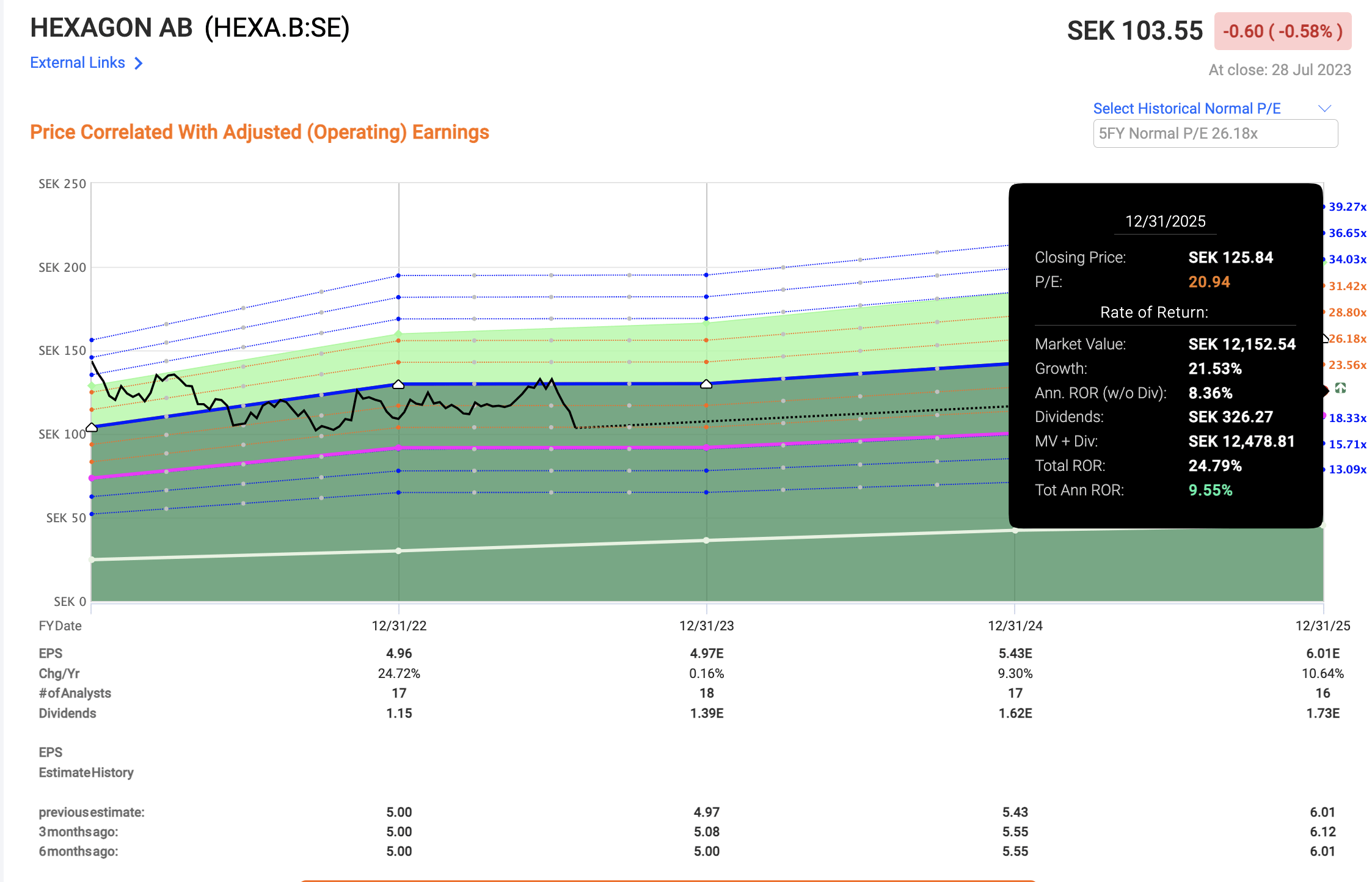

At this time, Hexagon trades at a 20.8x normalized P/E. that's significantly better than when I last wrote about it. The company's fundamentals and my thesis on the business are all the same.

I value Hexagon conservatively. And conservatively, the company is usually at around 20x P/E, which is where it currently is.

A 20-21x P/E upside is around 8-9% annually here, or 21-22% in a few years. These forecasts have high accuracy, so I tend to believe them. Very high accuracy in fact - for a 2-year basis, with a 20% margin of error, analysts have not missed this company in over 10 years, and the company has outperformed expectations 17% of the time. That is a high degree of conviction.

Hexagon Upside ( FAST Graphs )

{kind=link}

However, the problem is an upside. Even estimating it close to 21x, the upside is not double-digit at this price. It's technically good enough for you to "BUY" - and that is indeed why I am raising my target here and going "BUY" for the first time ever on Hexagon on Seeking Alpha.

But this rating comes with a warning.

I'm not currently "BUY"ing the common shares. At least not without safety.

If you can get 9-10% annually at today's price, but I can secure a buy-write CC with a 14-17% return at a strike of 95-100 SEK with a 1-year expiration, this far better encapsulates where I believe the company may realistically go, while meeting my overall investment targets. So I may go long the company via shares, but I'm doing so with an underlying guarantee of only keeping them if they move below my strike price.

Or, I could go with the CSP option - selling cash-secured puts with short- or longer expirations, like the one I gave you early in my article, annualizing 13-16%. That also is an avenue I would be more likely to take because it fulfills my investment targets much better than a single-target upside investment.

So in the end, I say this.

My targets for Hexagon remain the same. I was "right" in my last thesis and rating, holding until now. I'm shifting to "BUY" now, but I'm cautioning against naked buying of common shares without safeties to ensure that you get returns above 13-15%. In today's environment, I no longer think that 7-9% per year is enough, except in very special cases.

So this is my updated thesis on Hexagon AB.

Thesis

- Hexagon is perhaps the most attractive positioning industrial/software company in the world. at the right price, this company becomes a must-have, and one you do not look "back" on until it's excessively overvalued. This company is extremely well-capitalized, attractively managed, and has expertise in future-proof global industries with a high upside.

- The trends in July of 2023 have now seen the company recover from what I view as overvaluation - and I am changing my rating to "BUY" for the company here - though it comes with caveats, and I would be careful about investing the "wrong way" here.

- My PT for the company is preferably double digits but at 103 SEK/share, I'm moving to "BUY" due to the reasons mentioned above

Remember, I'm all about

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company is now at a good enough position to offer a double-digit upside, which makes it a "BUY" in my book - though there are better ways still of entering this investment at a good price.

For further details see:

Hexagon: Upside After Q2 - I Now Say That You Can 'Buy' (Rating Upgrade)