HFRO - HFRO: 50% Discount To NAV And 50% Distribution Cut

2024-01-05 08:30:00 ET

Summary

- Highland Opportunities and Income Fund provided an opportunity as it cut its income.

- HFRO fund tanked 16% and widened the discount to NAV to almost 50%.

- We examine the "why" and give you our take.

You can get the thesis right, and you can get it wrong. That's life, and none of us have divine knowledge. You can be excused for being human. But there's no excuse for blind yield chasing with no due diligence. Today, we look at those risk factor identifications, and one of them actually materialized for Highland Opportunities and Income Fund ( HFRO ).

In our previous coverage, we rated the fund a Hold.

Seeking Alpha

We found that there were positives for the fund, including a wide discount and some evidence that some finessing was employed using hedges to stabilize the NAV. We also saw that there were risks, and those kept us out of the "buy zone."

In the "against" category would be the fact that a lot of the fund's investments are not paying dividends themselves and are extremely illiquid. So funding via even the return of capital route may be hard in a protracted downturn. Another strike would be the fact that the fund's top performance came in the field of senior loans. Will we do just as well in real estate? The jury is out on that.

Source: 40% Discount To NAV And A 11.4% Yield

The 50% Solution

It's rare for CEFs to cut the distribution by 50%. This is even more true when you have the fund trading at the widest discount in the space. No one wants to add an exodus at that exact point. But that's what happened. HFRO's explanation was interesting, to say the least:

On January 4, 2024, the Fund declared a regular monthly distribution on its common stock of $0.0385 per share, payable on January 31, 2024, to shareholders of record at the close of business January 24, 2024.

The Fund adjusted the monthly distribution rate to align the distribution with the current portfolio and investment objective.

Additional considerations in the distribution change include:

Sources of distribution - As HFRO's portfolio has shifted its primary focus from bank loans to more diversified investments in real estate and private equity, the sources of distribution have similarly shifted from net investment income to capital gains and return of capital. As such, the monthly distribution payout exceeded the Fund's earn rate for some time, creating an unstainable dynamic that could negatively impact the portfolio if the distribution amount had remained unchanged. The reduction in the monthly distribution amount better reflects the cash flow from interest income and capital gains under HFRO's current portfolio composition and investment strategy. While the distribution change is intended to create a more sustainable monthly distribution level, the Fund may make special distributions as it monetizes certain holdings. Many of these holdings are not income-producing assets and therefore do not support monthly distribution payments. The recent distribution change provides more flexibility in the distribution to reflect the composition of the underlying assets.

Source: HFRO (emphasis ours)

So, in essence, HFRO's risk factor became a real actualized risk as the fund cut to avoid NAV erosion. The fund also cut because they really cannot sell some of these investments on a monthly basis to meet the difference between actual distributions and internally generated income. The market greeted this with all the enthusiasm of a first-trimester morning sickness, cratering the stock to a near 50% discount to its NAV.

Problem With HFRO's Distribution

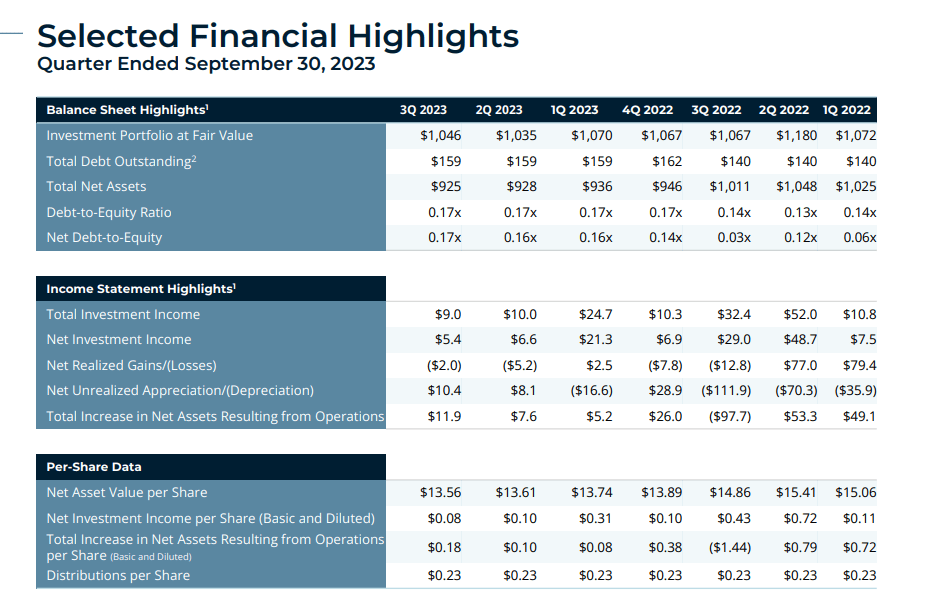

HFRO's selected financial highlights tell the story rather clearly. While the NAV has been firm, net investment income has been nowhere in the ballpark of distributions for the last three quarters.

{kind=link}

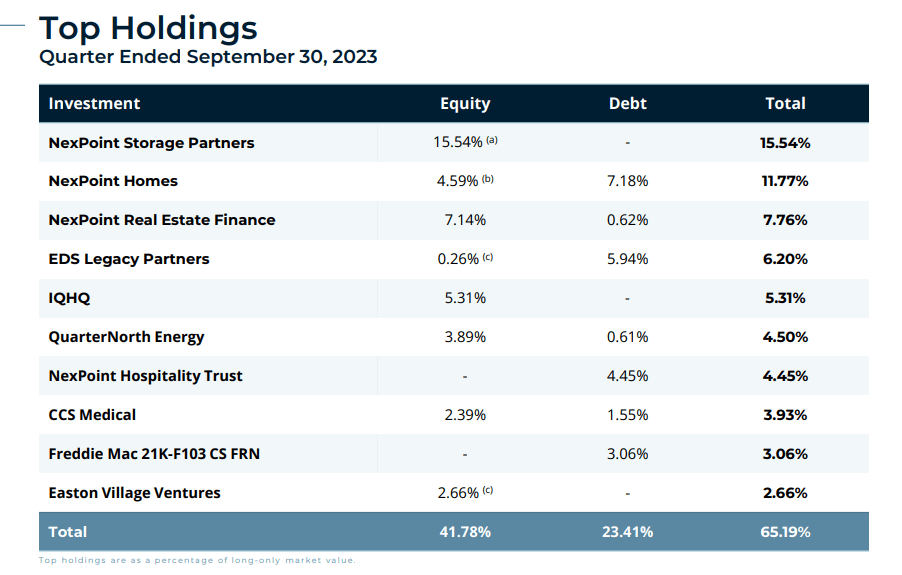

We don't have Q4-2023 results yet, but we suspect it would be the same story. The portfolio breakdown explains the issue. Of the numbers provided, about 10% of the portfolio is what would be considered extremely liquid and providing high income. This would be the sum of the public stocks, loans, bonds and CLOs. Almost 90% of the portfolio is in commercial real estate and private equity.

HFRO Q3-2023 Presentation

With commercial real estate, the debt section is good for income, and so are the public stocks, but the private equity is unlikely to be doling tons of cash. Overall, in the portfolio, we would think about 40% is providing some sort of income. If we assume this is at an 7% weighted rate, that just gets us to about 2.8% on the total portfolio. That's before accounting for any fees. If HFRO continued distributing beyond its income generation, it would likely have to dump its most liquid assets first and then try and market some of these illiquid ones. So the distribution was really at the mercy of the fund manager, and he decided it had to get chopped.

Outlook

The real estate portfolio is definitely on what we would call the "defensive side" and there are very little hotel or development assets in there. Office is also notably absent.

HFRO Q3-2023 Presentation

Self storage, multifamily rental, and single family rental make up similar percentages. If you saw this as a diversified REIT, we're sure many would jump in to make bull arguments. The problem is the sheer illiquidity of these investments and the rather unusual issue of many of them being sponsored by NexPoint.

{kind=link}

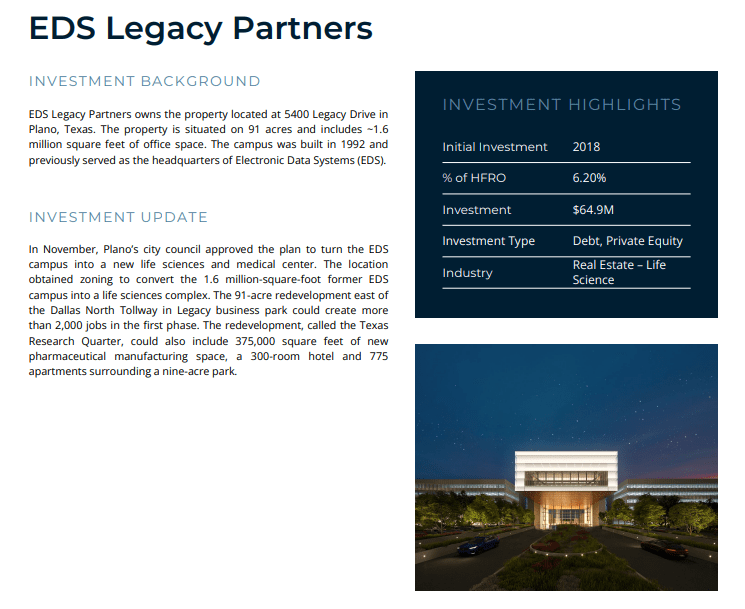

Exiting private investments is hard enough in most cases, but when you have the person in charge sitting in the same office, it might make things more complicated. Even fair value marking might be a bit challenging. To be fair to HFRO, it does go through all its investments in rather nice detail. Here's their largest one and most investors might recognize the name, Jernigan Capital (formerly symbol JCAP).

{kind=link}

That one actually might have some liquidity as it's an active property set producing income. The next one looks like it's locked for a really long time if you read what is being done with the investment.

{kind=link}

Most of the other investments seem fairly illiquid and hard to value. The current price is at a huge discount to the NAV, but the NAV is still extremely subjective. Note that the chart below runs till yesterday's NAV and price.

Data by YCharts

As of today, the discount is about 48% at a price of $6.68. This forms a pretty good margin of safety, and we think it likely works out from a total return perspective. The fund manager is likely to work on lucrative exits and use the cash flow to narrow the discount. This is also mentioned in the press release.

Current and future investment opportunities - Many of the Fund's top holdings represent longer-term, high-conviction investments that tend to be less liquid in nature. The Adviser believes the return profile of the Fund's current investments offers better long-term value for shareholders than liquidating assets to maintain monthly distributions at the previous rate. Further, maintaining a more sustainable monthly distribution better positions HFRO to realize growth-oriented investment opportunities and maximize the value of those opportunities for shareholders.

Initiatives to narrow the discount - The Adviser continues to pursue initiatives to narrow the discount between the Fund's share price and its net asset value - NAV. Reducing the distribution would preserve cash for share repurchases and other initiatives that may help narrow the discount and create value for shareholders.

Additional information on the current portfolio, the Fund's 2023 performance, and the recent distribution change will be addressed on the quarterly call with the portfolio management team on Thursday, February 29, 2024.

Source: HFRO

The environment is also far better than what it was two months back as credit conditions have eased substantially.

It still will require some finesse to exit these investments, and the only way to win the market back would be to demonstrate one or more illiquid asset sales near book value. We're very tempted here and might buy a small speculative position. But the risk factors still keep our rating at a firm "hold" and this won't make it into our Conservative Income Portfolio . There are also better choices in publicly traded REITs with similar discounts, where the exit/liquidation strategy is showing promise . Investors interested in just the income can consider the preferred shares ( HFRO.PR.A ) which are rated A1 by Moody's ( MCO ). They dropped a bit in sympathy, but the lower payout strengthens their position, and the 7.1% stripped yield from an A-rated security is not the worst place you can go.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

HFRO: 50% Discount To NAV And 50% Distribution Cut