HFRO - HFRO: Real Estate And Floating Rate Strategy With 9% Yield Can Keep Outperforming

Summary

- HFRO delivered a positive return in 2022 as an outlier to the broader market selloff.

- The fund invests through a unique strategy focusing on real estate and floating-rate instruments.

- We believe the fund can continue delivering positive returns in the current market environment.

The Highland Income Fund ( HFRO ) invests across fixed-income and equity securities with a particular focus on the real estate sector and floating-rate debt instruments. This is a segment that proved to be resilient in 2022 amid rising interest rates despite the challenging economic environment. Indeed, HFRO managed to generate a positive return over the past year, impressively beating various benchmarks as one of the best-performing closed-end funds in its category.

There's a lot to like about HFRO considering its 9% yield and monthly distribution. We see room for further capital appreciation benefitting from a continuation of favorable market tailwinds. While interest rates have stabilized over the last several months, HFRO is well-positioned to benefit from the still elevated rate environment with a path for credit spreads to narrow into an improving macro backdrop going forward. The recent pullback in the fund along with a widening discount to NAV makes HFRO compelling at the current level.

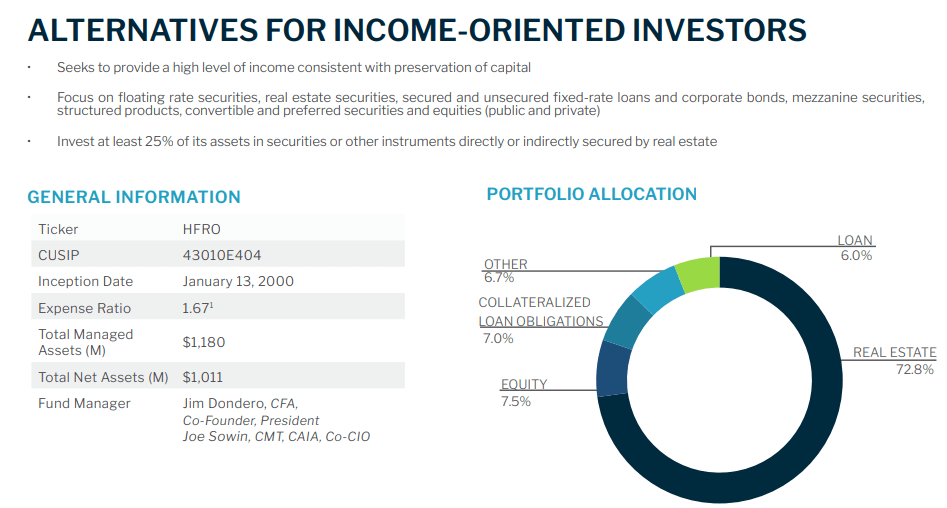

What is the HFRO Fund?

The attraction of HFRO is the fund's allocation strategy into what can be considered alternative investments typically reserved for institutional investors. Keep in mind that the fund is actively managed meaning it's not intended to track any underlying index, and each holding is at the discretion of the investment team at NexPoint Asset Management.

We mentioned the fund's focus on real estate and floating-rate securities. That exposure is comprised of various structures including collateralized loan obligations (CLOs), convertibles, and preferred securities, along with both private and publicly traded equities.

{kind=link}

Within the real estate allocation that represents more than 70% of the fund, the positions are represented by finance companies and REITs. On this point, HFRO invests in some private REITs and others that are separately managed by the same NexPoint group as a wholly owned subsidiary.

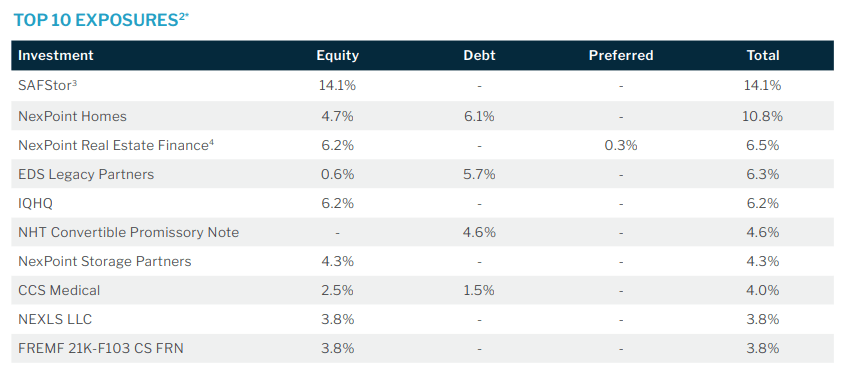

Examples among the top holdings include "NexPoint Homes", a developer of affordable single-family properties. here is also NexPoint Real Estate Finance Inc. ( NREF ) which is a publicly traded mortgage REIT. We also find "NexPoint Storage Partners" which owns and operates a portfolio of storage facilities. The largest current position in "SAFStor" is also an operator of storage facilities that were acquired at the corporate level by NexPointStorage in a transaction announced just this past December.

Going through the portfolio, other major investments include "EDS Legacy Partners", which controls a corporate office development in Plano, Texas. "IQHQ" is a private REIT focusing on life-science real estate developments. There is an overall wide range of real estate investments which is combined with some smaller tactical positions in other unrelated sectors. The fund has also historically used derivatives for hedging purposes resulting in a leverage ratio currently listed at 12%.

The takeaway here is that the HFRO offers exposure to a unique group of assets and investments that are managed to generate a consistent income for fund shareholders.

{kind=link}

HFRO Performance

HFRO technically uses a "leveraged loans" Index as a performance benchmark, but it's clear the actual exposure is more nuanced given the equity positions and REIT holdings. What we can say is that HFRO is doing something right because the numbers speak for themselves.

HFRO has returned 11% at the NAV level on a total return basis, which compares to a 0% return from the Invesco Senior Loan ETF ( BKLN ) as a reference point. The fund was able to buck the trend in both high-yield bonds and broader real estate last year which faced greater volatility. As a CEF benchmark, the PIMCO Corporate & Income Opportunity Fund ( PTY ) is down -7% over the period, while the real-estate-focused Cohen & Steers Total Return Realty Fund ( RFI ) lost -11%.

At the share price level, HFRO is up 5% over the same period with the difference considering its discount to NAV has widened over the period. Nevertheless, the performance spread to the same group of funds is similar.

There are a couple of factors at play that help explain the exceptional year. First, HFRO's exposure to private investments has helped with the returns given their operating and financial trends that are often separate from publicly traded equities. Active management appears to have also played a role in security selection.

We can also bring up a $40 million share buyback program which was completed in Q1 last year. Considering the fund has over $1 billion in assets under management, the repurchases may have modestly supported the shareholder return although it was likely not the primary culprit.

What is more significant is likely the fund's positions in floating-rate instruments as these types of loans adjust in value directly to the changes in rates. This was critical in 2022 into several Fed rate hikes which drove a surge in short-term interest rates. While fixed-rate instruments and the broader bond market as an asset class faced deep losses and historic volatility, the floating-rate components of the portfolio worked as a hedge and may have even added to the NAV appreciation.

This dynamic is connected to the concept of bond duration which reflects a particular instrument's sensitivity to changing interest rates. In other words, the portion of the portfolio in floating rate loans including CLO's helped the portfolio performance by lowering the implied effective duration.

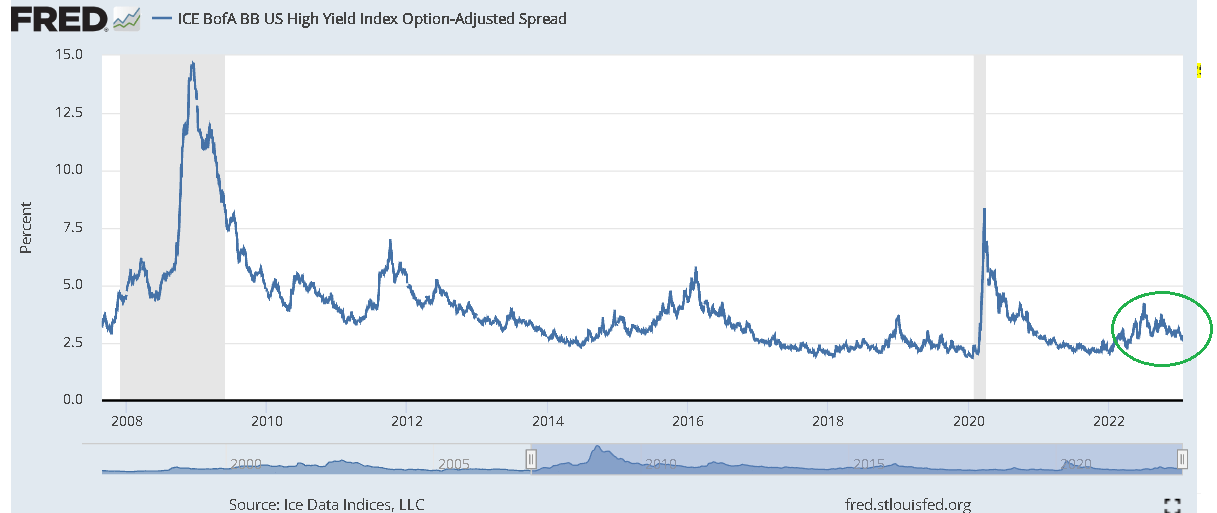

The other fact to consider is the trend in credit spreads. Beyond the headlines over the past year of a slowdown in the housing market and a decline in real estate prices in recent months from their peak, debt securities have been otherwise well-supported without any large-scale defaults that defined previous cycles.

The Fed publishes the index the "ICE BofA BB US High Yield Option-Adjusted Spread" which we can use here as a proxy for credit conditions . The current level has declined over the last several months and is a well-below period of extreme market stress either during the depths of the pandemic or from the financial crisis in 2008.

Notably, the same level of credit spreads is now at the lowest level in nearly 1 year reflecting the latest data on easing inflationary pressures and an expectation for normalizing interest rates. All this can be positive for the NFRO fund strategy going forward.

{kind=link}

What's Next For HFRO?

We're bullish on HFRO with a baseline that the strategy continues to be attractive in the current market environment. While short-term interest rates likely won't have a repeat of 2022 ass the Fed slows its rate hiking policies, outside of a policy reversal to rate cuts or surge in credit spreads, floating rate instruments and CLOs should continue to perform well.

On the real estate side, we're also expecting a stabilization compared to the volatility in 2022. Improving economic sentiment as inflationary pressures ease could be a catalyst for a broader sector recovery. The economic indicators to watch for include resilient labor market trends and corporate earnings to gauge the health of the broader economy.

HFRO trades at an exceptionally wide discount to NAV at -28% which itself has been volatile over the past year. As with the fund performance, part of the dynamic here considers the unique investment portfolio with allocations to private companies and even wholly-owned subsidiaries of NexPoint. By this measure, the market may be assigning a structural discount given the lack of direct control investors in HFRO have as shareholders to the underlying investments along with the nature of some securities including bank loans where daily pricing may be unavailable.

The argument we make is that while a discount is warranted, the level may still be too extreme at this point with room to narrow from here. Any upside to the discount would be incrementally positive to HFRO shareholders.

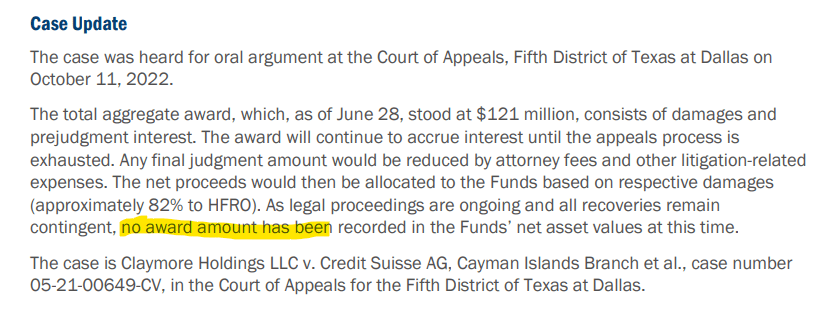

Finally, we can bring up ongoing litigation against "Credit Suisse Securities" where NexPoint is seeking upwards of $121 million as a claim against charges of potential fraud.

The latest update in October simply explained that the group is awaiting a final judgment with HFRO potentially recovering upwards of $103 million which would be accretive to the net asset value. Fellow Seeking Alpha contributor George Spritzer covered the topic at the time. No new developments have been announced at this time. We'd expect the cash to be used for a new buyback authorization.

{kind=link}

Final Thoughts

Overall, our take is that HFRO is a high-quality fund that can work in the context of a broader portfolio for income investors. The expense ratio at 1.67% is consistent with comparable CEFs given the institutional management and particular asset class.

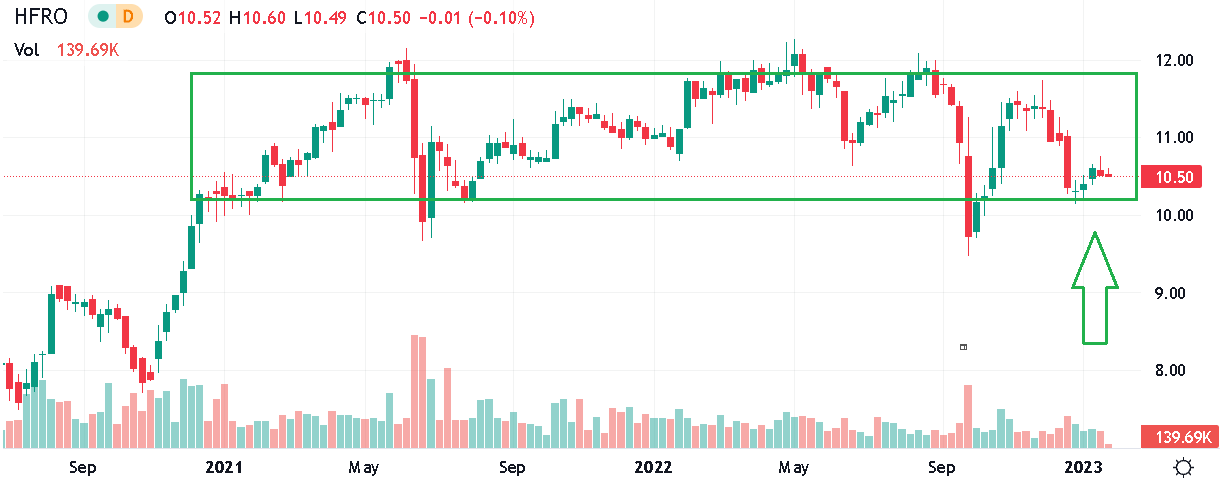

We like the setup in HFRO looking at the share price chart that has traded in a relatively tight range over the past year, excluding the monthly distribution. The opportunity to pick up the fund around $10.50 looks like an attractive entry point in terms of relative value.

On the downside, the main risk would be a deeper deterioration in the economic outlook. While we painted a rosy picture of macro conditions, the inverse taking place between surging unemployment, crashing corporate earnings, and a blowout in credit spread would open the door for a repricing of HFRO lower.

{kind=link}

For further details see:

HFRO: Real Estate And Floating Rate Strategy With 9% Yield Can Keep Outperforming