HFRO - HFRO: The Fund May Have A Conflict Of Interest But There Is A Lot To Like Here

Summary

- Investors today are desperate for income due to the rising cost of living and HFRO is one potential source of that income.

- The fund is heavily invested in floating-rate securities, which should hold their value better than traditional bonds as interest rates continue to rise.

- The fund may have a conflict of interest with some of its holdings and it appears to have a strange classification for certain asset types.

- The confusion caused by a few of these things is quite disturbing and may explain why the fund has an incredibly large discount to net asset value at the current price.

- The fund is generating substantially more income than it needs to pay the distribution so investors should not have to worry about a cut.

One of the biggest problems facing most Americans today is the incredibly high rate of inflation that has permeated our economy. This has driven up the costs of necessities such as food and energy and forced many people to take on second jobs or enter the gig economy simply to keep themselves and their families fed and clothed. In fact, according to a recent Prudential Pulse survey , approximately 81% of Generation Z members and 77% of Millennials have either pursued or considered pursuing secondary jobs in the gig economy over the past year. Obviously, the working kind of hours that two jobs would require of a person will take a toll on that person’s psyche. Fortunately, as investors, we do not need to go to this extreme as we can make our money work for us. One of the best ways to do that is to invest in a closed-end fund that specializes in the generation of income. These funds provide easy access to a diversified, professionally-managed portfolio that can in many cases deliver a yield that is higher than any of the underlying assets in the fund.

In this article, we will discuss the Highland Income Fund ( HFRO ), which is one fund that can be used as a source of income. As of the time of writing, this fund boasts a fairly impressive 8.79% yield so it certainly meets the yield requirements of most income-focused investors. The fund also trades at an incredibly attractive price today, which may be a consequence of it not being as familiar to many investors as some of the closed-end funds from more famous fund houses. The fund’s lack of attention by no means diminishes its ability to be a good holding for investors, however. Therefore, let us investigate and see if this fund could be a good addition to a portfolio today.

About The Fund

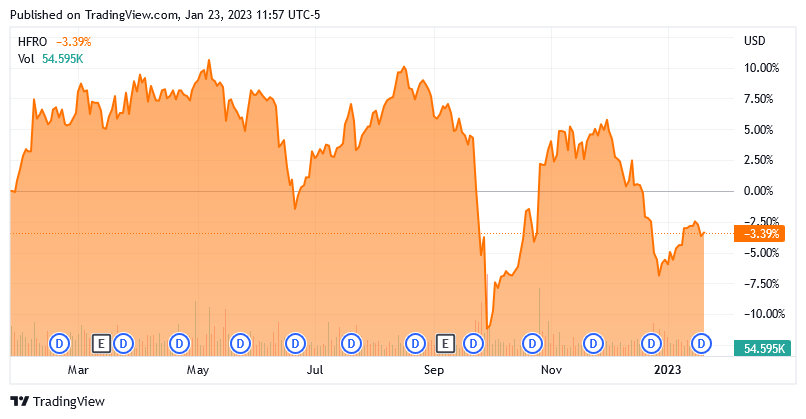

According to the fund’s webpage , the Highland Income Fund has the stated objective of providing its investors with a high level of current income while still attempting to preserve the value of its principal. This is certainly not an unusual objective for a fixed-income fund. In fact, most of them have a stated objective that is pretty similar to this. After all, fixed-income investments are generally considered a reasonably good way to preserve capital since any fixed-income security will return your initial investment at maturity. Unfortunately, bond funds do not always hold their assets to maturity and their price tends to fluctuate based on the value of the bonds in the portfolio. The Highland Income Fund is certainly no different as the fund has declined by 3.39% over the past year:

{kind=link}

This is a much better performance overall than nearly all fixed-income funds have delivered over the period. It is certainly much better than the 10.80% loss that the Bloomberg U.S. Aggregate Bond Index ( AGG ) has delivered over the period. One of the biggest reasons for this is that the Highland Income Fund invests in somewhat different securities from both the index and most other fixed-income closed-end funds.

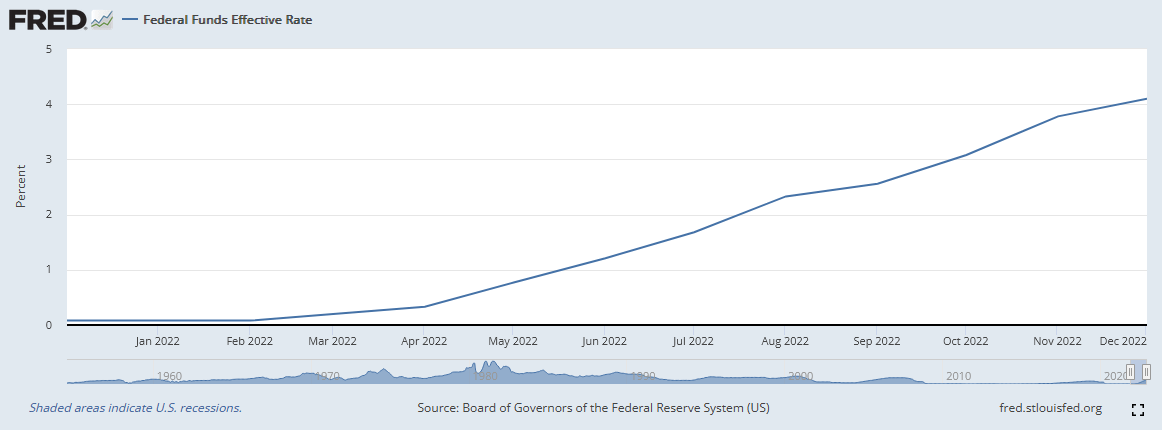

The Highland Income Fund focuses its efforts on investing in floating-rate securities. These are very different than the fixed-rate bonds that most funds invest in. The biggest difference is that the interest rate on these securities increases when a benchmark (usually the federal funds rate or LIBOR) increases. As such, they should hold their value better than traditional bonds during periods of rising rates. This is important today as the Federal Reserve abandoned its zero-interest rate policy back in March 2022 and has been hiking rates ever since in an effort to combat the high inflation that has permeated the United States. We can see this reflected in the federal funds rate, which is the rate at which the nation’s commercial banks lend to each other on an overnight basis:

{kind=link}

As we can clearly see here, the effective federal funds rate climbed from 0.08% a year ago to 4.10% today. This is the biggest cause of the market pressure on fixed-income prices that has been occurring over the past year. The reason for this is that bond prices move inversely to interest rates. In other words, when the federal funds rate goes up, bond prices go down. The reason for this is that newly issued bonds will have a yield that is based on the higher borrowing rate. As such, nobody will buy an existing bond with a lower yield unless the price of that bond goes down so that it delivers the same yield-to-maturity as a newly issued bond with the same characteristics. However, a floating-rate security will have its yield automatically adjusted with the change in interest rates so it does not need its price to decline in order to continue to deliver a competitive yield. As such, we should expect these securities to hold their value fairly well during periods of rising rates. That is exactly what we see with the performance of the fund over the past twelve months.

One of the biggest downsides to floating-rate securities is that they tend to be issued by companies that have a high amount of debt already or have somewhat volatile cash flows. As such, these securities will generally be at a somewhat higher risk of default losses than typical investment-grade bonds. This is something that will undoubtedly concern those investors that are interested in the preservation of principal, which is a category that would include most retirees. As such, it may be a good idea to look at the credit rating of the securities that comprise the portfolio. Here they are:

CEF Connect

This is unfortunately not particularly instructive. As we can see, fully 82.70% of the securities in the portfolio have not been rated by any credit rating agency. As such, we do not know what they are or how risky they may be. We can assume though that these are not investment-grade securities. This is because pretty much any issuer that has a strong enough financial position to qualify for such a rating will pay the money needed to have their securities rated. After all, an investment-grade bond rating will save the issuing company an enormous amount of money over the duration of the bond. Thus, these securities are probably issued by entities that may have some financial issues.

One thing that may be somewhat comforting though is that 72.8% of the securities in the portfolio are secured by real estate:

Fund Fact Sheet

This removes a lot of the risk that we were concerned about in the previous paragraph. This is because of the lien against the real estate that the lender would possess. In short, if the borrower defaults on the loan, then the lender can seize the real estate and sell it off to obtain the money needed to repay the loan. That protection would extend to us as holders of mortgage-backed securities. Thus, while the default risk remains, the probability of loss is greatly reduced because of the ability of the real estate to hold its value over time. Thus, this fund is probably not nearly as risky as the credit ratings of the portfolio securities have led us to believe.

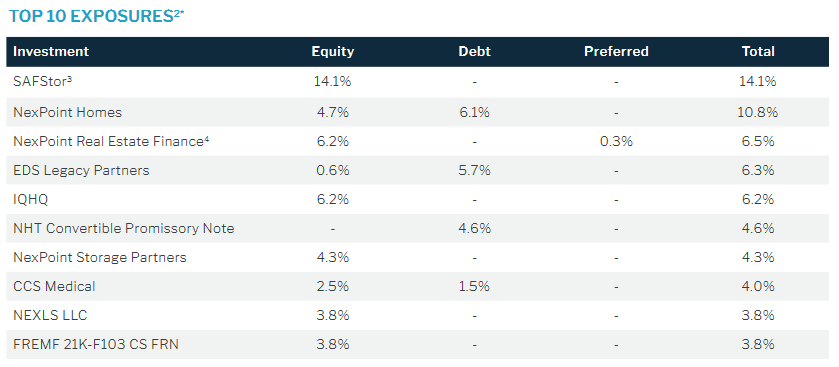

Unfortunately, the fund only has 105 holdings, which is incredibly low for a fixed-income fund. This also increases our risk somewhat because any problems with one of the securities or issuers could cause noticeable impacts on the portfolio. This concern is worsened when we look at the largest positions in the fund:

{kind=link}

Interestingly, the fund's fact sheet states that 14.1% of the portfolio is invested in SAFStor yet only 7.5% of the portfolio is invested in common equity. This is curious as it could be a clear sign that the fund is using a very different definition of common equity than most investors. My first thought is that the fund has some short positions, which is certainly the case. The fund currently holds short positions in Wynn Resorts ( WYNN ) and Texas Instruments ( TXN ). These two positions though only account for 0.8% of the portfolio so they are not nearly large enough to reduce the equity exposure to make each of the two charts make sense. We also cannot consider that the dates are different since both charts come from the exact same recent document. The only thing that I can figure out is that the fund is classifying the common equity of a real estate investment trust as a real estate security as opposed to common equity. The overall lack of transparency here is very disturbing though and I will admit that it makes me very cautious about investing money here.

As we can quickly see, the fund has a few outsized positions with SAFStor, NexPoint Homes, and NexPoint Real Estate Finance. SAFStor is one of the largest developers of self-storage facilities in the United States, which was acquired by NexPoint Storage Partners last month. NexPoint Homes is a real estate investment trust that purchases single-family homes and then rents them out to tenants. Thus, a very substantial portion of this fund’s assets is invested in entities that are affiliated with NexPoint. As the Highland Income Fund is also managed by NexPoint, there are certainly some conflicts of interest here. Basically, the closed-end fund appears to be a vehicle that is used by NexPoint to finance some of its own operations. Admittedly, there are some third-party assets in the fund so it is not exclusively a NexPoint financing vehicle. It is important to keep the conflict of interest in mind before making an investment in the fund as the fund’s investments have the same management as the fund itself. With that said, if you trust NexPoint, this could be a good way to gain exposure to some of their alternative investments without needing to be an accredited investor. Personally, though, I would rather be invested in a fund that is somewhat more diversified across companies and management teams.

Leverage

Earlier in this article, I stated that closed-end funds such as the Highland Income Fund have the ability to utilize certain strategies that allow them to deliver a higher yield than any of the underlying assets possess. One of these strategies is the use of leverage. Basically, the Highland Income Fund is borrowing money and then using those borrowed funds to purchase floating-rate fixed-income securities. As long as the purchased securities have a higher yield than the interest rate that the fund has to pay on the borrowings, the strategy works pretty well to boost the overall yield of the portfolio. As the fund can borrow at institutional rates, which are significantly lower than retail rates, this will usually be the case.

However, the use of debt is a double-edged sword. This is because leverage boosts both gains and losses. Thus, we need to ensure that the fund is not employing too much leverage since that would expose us to too much risk. I generally like to see a fund’s leverage be under a third of its assets for this reason. Fortunately, that is the case with the Highland Income Fund. As of the time of writing, the fund’s levered assets only comprise 12.40% of its portfolio. This is a pretty low leverage ratio for a fixed-income fund and in fact, the fund could probably boost the leverage a bit in order to increase its yield. However, for the most part, the fund is striking a reasonable balance between risk and reward.

Distribution Analysis

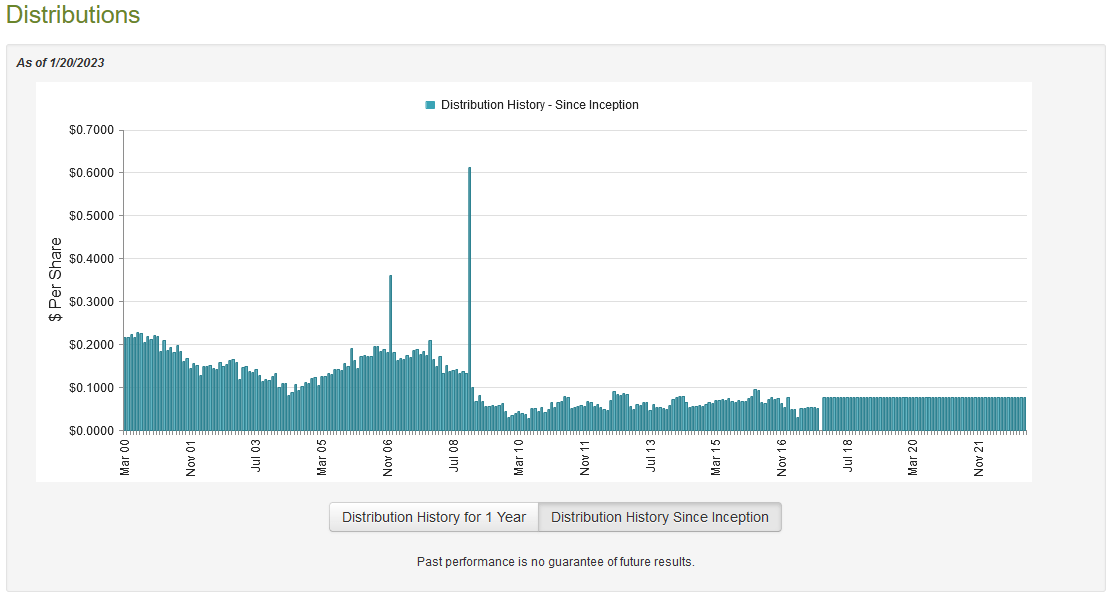

As stated earlier in this article, the primary objective of the Highland Income Fund is to provide a high level of current income for its investors. In order to achieve this, the fund invests in a number of fixed-income securities that have fairly high yields themselves, especially in today’s climate, and applies leverage to boost the yield even further. As such, we might assume that the fund has a respectably high distribution yield. This is certainly the case as the Highland Income Fund pays a monthly distribution of $0.077 per share ($0.924 per share annually), which gives it an 8.79% yield at the current price. The fund has been remarkably consistent about this payout since December of 2017, although it tended to vary a great deal prior to that date:

{kind=link}

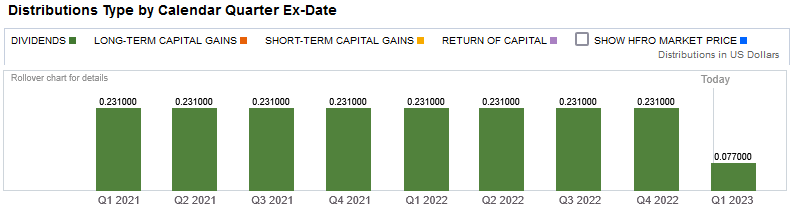

The fund’s recent track record will likely appeal to those investors that are looking for a safe and secure source of income that they can use to pay their bills and finance their lifestyles. This fits well with our general reason for being interested in a fund like this in the first place. These same risk-averse investors will also likely appreciate the fact that the fund’s distributions consist entirely of dividend income, with no return of capital component:

{kind=link}

The reason that this can be comforting is that dividend income is by far the most sustainable source of distribution money for the fund. This is because dividends are paid directly from the dividends or interest payments that the fund receives from the assets in its portfolio. A return of capital distribution can be a sign that the fund is returning the investors’ own money back to them, which is obviously not sustainable over an extended period. A capital gains distribution requires that the fund’s management consistently generate large enough capital gains to cover the distribution, which may not be possible in certain market conditions. We seemingly do not have to worry about any of that here. However, as I have pointed out in the past, it is possible for these distributions to be misclassified. As such, we still want to investigate exactly how the fund is financing its payouts and determine how sustainable they are likely to be.

Unfortunately, we do not have an especially recent document to consult for that purpose. The fund’s most recent financial report corresponds to the six-month period that ended on June 30, 2022. As such, it will not include any information about the fund’s performance over the past half-year. However, the Federal Reserve switched to a hawkish monetary policy in March, which is an event that caused devastation in the bond market. We will clearly be able to see how well this fund handled that event through this report. During the six-month period, the Highland Income Fund received a total of $56,153,903 in dividends and $6,899,477 in interest from the investments in its portfolio. It is admittedly quite curious that a fixed-income fund would receive so much more in dividends than in interest so it seems likely that a lot of the real estate securities in the portfolio are taxed in a somewhat atypical way. Regardless, the fund had a total income of $62,839,343 after we net in some money received from other sources and net out some dividends that the fund received from a partnership (which is classified as a return of capital). The fund paid its expenses out of this amount, which left it with $56,180,232 available for the shareholders. This was far more than the fund needed to cover the $31,578,404 that it actually paid in distributions over the period. In fact, the difference was such that we can expect the fund to pay out a special dividend at some point if its income over the second half of the year was anywhere close to this figure, as seems likely. Overall, shareholders should not have to be concerned about the fund’s ability to maintain its distribution as it is easily generating enough money to do so solely through its net investment income.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the Highland Income Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all of the fund’s assets minus any outstanding debt. It is therefore the amount that the investors would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a situation implies that we are buying the fund’s assets for less than they are actually worth. This is certainly the case with this fund today. As of January 20, 2023 (the most recent date for which data is available as of the time of writing), the Highland Income Fund had a net asset value of $14.51 per share but the shares only trade for $10.52 per share. This gives the fund’s shares an enormous 27.50% discount to the net asset value at the current price. This is not as attractive as the 28.12% discount that the shares have averaged over the past month but frankly, it is still a large enough discount to make the fund’s shares very attractive today.

Conclusion

In conclusion, the Highland Income Fund certainly does not have a huge following but it is a very good fund for income investors. The biggest risk here is that the fund is intrinsically linked to NexPoint and appears to be acting as a funding vehicle for many of the broader company’s real estate projects. With that said, many of the fund’s assets are backed by real estate and so have the security that comes with that. As long as you are comfortable with the potential conflict of interest, there is a lot to like here as the fund’s distribution appears to be very sustainable and its shares are trading at an incredibly attractive valuation. Overall, it may be worth considering as an addition to an income-focused portfolio.

For further details see:

HFRO: The Fund May Have A Conflict Of Interest But There Is A Lot To Like Here