NKE - Hibbett: A Misunderstood Retailer

2023-10-11 08:16:15 ET

Summary

- Hibbett is vastly different from its closest comparables in the market.

- Their focus on underserved communities insulates the company from e-commerce threats and helps build customer loyalty.

- Their digital transformation strategy will garner greater customer LTV.

- Hibbett's largest risk (Nike supply) is now greatly mitigated.

- When looking at normalized earnings and re-rating to comps, the upside at current price levels is excellent.

Executive Summary

I believe Hibbett (HIBB) is a misunderstood retailer that is fundamentally different from what most view as close comparables. Because of this market misunderstanding, I have concluded Hibbett trades well below intrinsic value, providing a high margin of safety and potential upside. This is a great business, with the right management team, and a clear reason the market has mispriced the stock.

Company Overview

Hibbett is an athletic-inspired fashion retailer with 1,148 stores between Hibbett (943), City Gear (189), and Sports Additions (16). City Gear and Hibbett stores look very similar, only differentiated by brand, while Sports Additions are smaller stores focused on footwear. Stores are primarily located in underserved communities at strip centers ( 80% ) and malls ( 20% ). Stores in strip centers are typically located near mass retailers like Walmart to drive foot traffic. All stores look nice & organized inside, comparable to a Foot Locker ( FL ) or Champs ( FL ). Hibbett offers personalized customer service and access to coveted footwear, apparel, and equipment from brands like Nike ( NKE ), Jordan, and Adidas (ADDYY). Currently, there are 11,000 employees, 3,800 full-time, 94% in retail locations. Current EV = $628mm ($554mm Mcap, $33mm cash, $107mm revolver outstanding).

Thesis Points

- New Management Team: Since tenure started in early 2020, the team has been resilient through unprecedented times. Had the greatest 2-year FCF performance in company history, openly identified current inventory problems, mitigated the largest idiosyncratic risk, and returned $374mm to shareholders since the beginning of 2020 (2/3 of current market cap).

- New store openings: Management is focused on opening stores in clustered locations to maximize logistical efficiencies and leverage their understanding of the market. Planning to open 40-50 stores in FY23. Stores in strip centers are typically located next to mass chain retailers like Walmart to drive foot traffic. Great use of capital - historical ROIC = 41%.

- Consumer Base/Underserved Community Focus: Their competitive advantage is serving areas other retailers may not see as lucrative. By understanding their customer base and effectively marketing to them (via their loyalty program, release platform (Raffle), and social media community) they will continue to attract a loyal customer base and receive favorable terms from vendors who otherwise may not be able to serve these areas. According to management, 80%+ of Hibbett customers are debit or non-bank cash customers meaning Hibbett is more insulated from digital competitors. Also, 54% of stores have no competitor within 3 miles and 70% of stores have only 1 competitor within 5 miles.

- Omnichannel: Launched an e-commerce site in 2017 and a mobile app in 2018 to complement the B&M business. The focus is on in-store pick-up to protect margins. The mobile app includes 'Raffle' which is used to manage all new product releases. Raffle offers the chance to win free shoes apart of new releases, big with Sneakerheads, winners pick-up in-store. The loyalty program + Raffle within the mobile app will create sticker/higher LTV customers.

- Macro: Inflationary pressure is causing an array of short-term headwinds (see risks below). Once inflation and inventory levels normalize, gross margins should expand as industry-wide promotional activity stabilizes and the top line will accelerate. Stock down ~30% YTD creates opportunity.

Risks

- Idiosyncratic Risks : The biggest risk to Hibbett's business is Nike pulling their wholesale agreement with them. Nike makes up 69% of sales for Hibbett (which fluctuates historically between 55-70%). In the past 4 years, Nike has ceased 50% of their wholesale relationships and in 2021 accelerated these partnership cancellations due to their focus on consumer direct. I believe there are 4 significant mitigants to this risk (in no particular order):

- Senior Merchandising VP Stephani Smith worked at Nike for 28 years as the VP of sales for Converse and Global VP of Nike SB.

- Launched 2 non-profit charities with Nike in 2023 (SOLE SCHOOL & Fresh Off the Block) funding underserved schools for education & athletic purposes.

- 80%+ of Hibbett's customers are debit or non-bank cash customers so if Nike wants to reach this loyal demo they have to partner with Hibbett.

- Timing, Nike dropped 4 major partners on March 26, 2021, including Macy's, JCP, Urban, and DSW. The fact Hibbett is still around is a good sign.

- Macro: Inflation shrinking their customer's wallets + forcing higher wages for in-store employees. Reduced discretionary spending from general economic worries and student loan repayments coming back online. Sitting on a lot of excess inventory ( +18% YoY ) which has driven higher promotional activity resulting in declining gross margins.

- The macro conditions coupled with Nike fears have created the opportunity I see in the stock today. Assuming these conditions are temporary and focusing on normalized earnings, the discount to true intrinsic value is large.

Financials

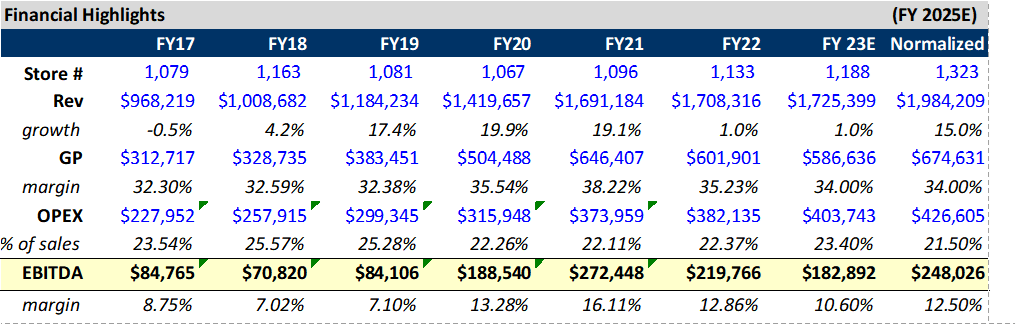

Below I've highlighted my normalized earnings assumptions (2025 expectations), historical ROIC for the business, and my valuation analysis:

Normalized Earnings Assumptions

{kind=link}

I believe Hibbett will reach my normalized earnings target by 2025 due to gross margin recovery, active store growth plans, and operating leverage. At $248mm in EBITDA and assuming $60mm in CAPEX for store additions, relocations, and refurbishing, the normalized FCF yield is 31%. I believe this is excellent for a business with solid long-term growth prospects coupled with a loyal, insulated customer base.

Bears will look at FY17 - FY19 EBITDA margins and debate against normalized EBITDA margins above 10% being unsustainable. To simply refute that argument, remember FY17 - FY19 was the period of digital development in the business which resulted in more promotional activity and development-related costs inhibiting margins. FY06 - FY16 the average EBITDA margin was 14.0%.

Return on Invested Capital

{kind=link}

Hibbett's ROIC has averaged 41.4% since 2006, excluding the overearning periods in 2020 & 2021 due to stimulus. By calculating ROIC as operating income/(net working capital + net fixed assets) this metric gives us an excellent idea of the returns Hibbett gets on new store development.

As management is highly focused on strategic store openings, I believe this ROIC number is protected and will potentially grow into the future. While a disciplined strategy limits total capital expenditure annually, management still expects to spend ~$60mm per year on new stores which is an excellent use of capital.

While Hibbett has a much different target location, Foot Locker operates ~2,800 stores leading me to believe Hibbett still has a significant new store runway.

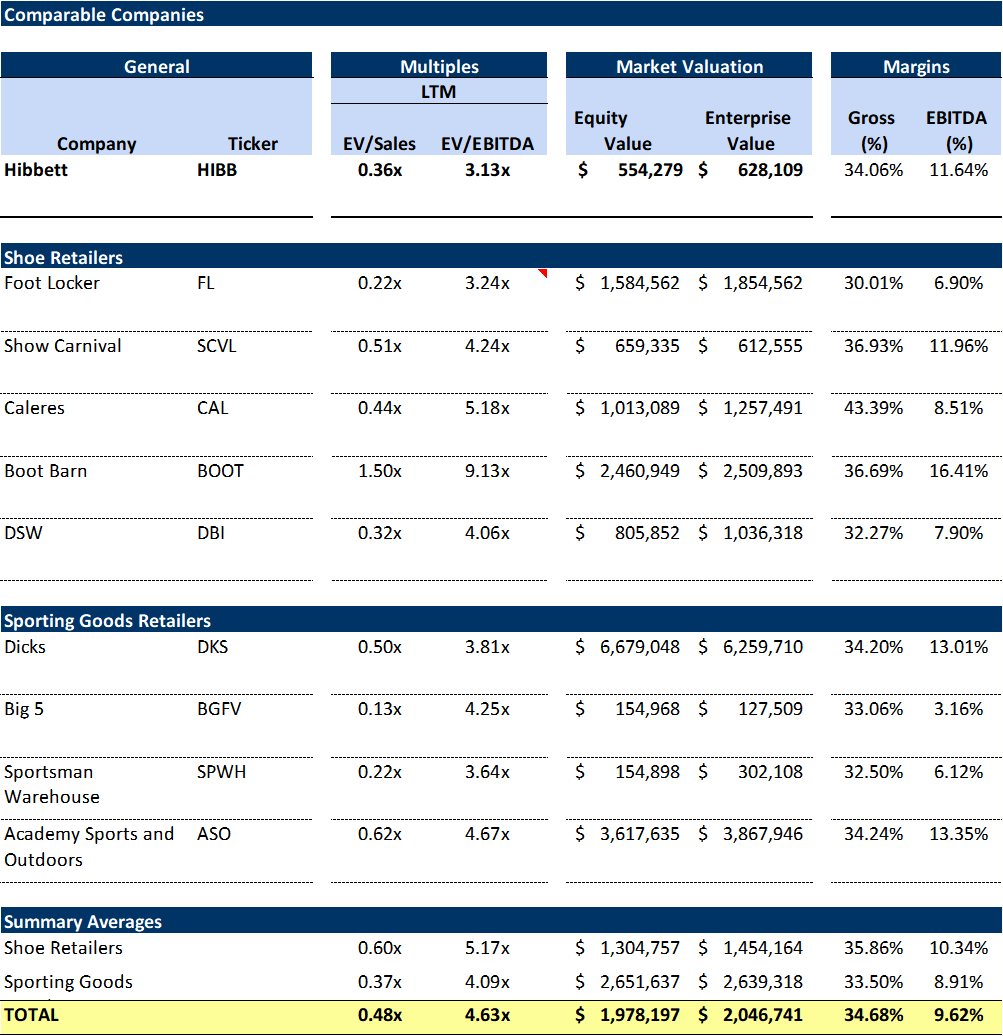

Valuation

{kind=link}

Relative to other shoe retailers, Hibbett trades at a 40% discount, and relative to both shoe retailers and sporting goods stores, a 32% discount. When factoring in historical growth, customer loyalty, customer insulation, and store growth prospects, Hibbett should, at the very least, trade in line with other shoe retailers. Because of this, I believe Hibbett has a significant margin of safety.

Relative to its own history, since 2007 Hibbett's average LTM EV/EBITDA multiple was ~7.0x.

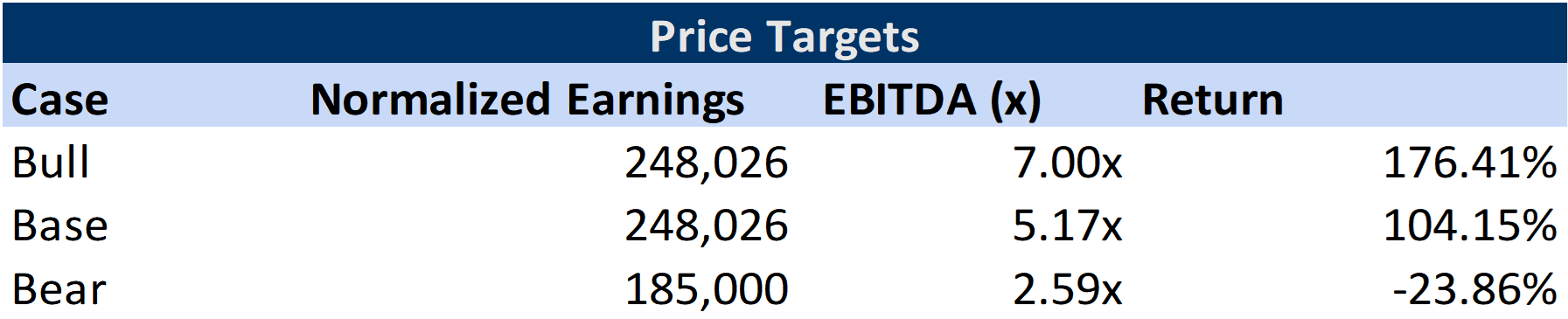

Price Target

Using normalized earnings and re-rating to the current shoe retailer group multiple, my base upside is 104% which I believe is achievable by EOY 2025 (37% CAGR).

{kind=link}

Mike Longo

Mike Longo was appointed as CEO in December 2019 and has methodically built out the management team since then. After running distribution at AutoZone for ~14 years, Longo bought City Gear as a private investment and ran for 13 years before being acquired by Hibbett in 2018. He is an ex-military guy (Army infantry officer - went to West Point then HBS), known for excellent internal goal setting according to other analysts. Regularly visits stores in person (his whole personal Instagram is him with store reps) and stays in touch with suppliers (focused on the right things). Started guiding on store count, revenue growth, GM, SG&A expense, EPS, and CAPEX when he became CEO showing transparency to shareholders. Has struggled with guidance but a lot of that has been a result of a volatile retail environment. Bought $271k worth of stock in May and has returned $374mm to shareholders since becoming CEO.

Summary

Because of Hibbett's strategic focus on underserved communities, they have limited competition and have garnered an extremely loyal customer base who are insulated from e-commerce threats. With total store count well below other comps, the long-term upside for new store growth is plentiful and exciting for shareholders considering their historically high ROIC.

The near-term catalyst is the Q3 print coming out in late November where the market may continue realizing its strength relative to comps (see HIBB vs. FL following Q2's release).

Editor's Note : This article was submitted as part of Seeking Alpha's Best Value Idea investment competition , which runs through October 25. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Hibbett: A Misunderstood Retailer