ASO - Hibbett: Still A Sporting Good Prospect On A Change In Fortunes

Summary

- Hibbett has done really well as of late, with sales and bottom line results improving markedly.

- This comes after a rough start to the 2022 fiscal year and the future for the business will likely be bright.

- Add in just how cheap shares are, and the company seems to offer additional upside from here.

Economic conditions over the past couple of years have been highly irregular. After recovering from the COVID-19 pandemic, the world was plunged into an inflationary state caused by supply chain issues, largely resulting from the aforementioned pandemic. Most companies have suffered to some degree through this. However, adaptation is important, and one company that has shown impressive signs of adapting to current market conditions is Hibbett (HIBB), an enterprise that sells not only athletic shoes and related products, but also a wide variety of fashion-oriented products. For the data currently available throughout its 2023 fiscal year, it's clear that much of the year proved to be painful for the enterprise. But the most recent data available suggests that the worst is well behind it. Although shares of the company have roared higher in recent months, they do still look attractively priced on an absolute basis, while being perhaps fairly valued compared to similar firms. Because of this all, I believe that a soft 'buy' rating is still appropriate for the business at this time.

The tide is changing

The last article I wrote about Hibbett was published in late September of 2022. At that time, I acknowledged that shares of the company had been hit hard during the general market decline leading up to that point. This was driven in large part also by weakness on both its top and bottom lines. Investors were super pessimistic about the company at that point, even though shares of the company looked incredibly cheap on an absolute basis. This affordability led me to keep the 'buy' rating I had assigned the company previously, a rating that denoted my own expectations that shares should outperform the broader market for the foreseeable future. Since that time, the company has done exceptionally well. Even though the S&P 500 is up a robust 13.1%, shares of Hibbett have generated upside of 38.5%.

{kind=link}

If you look at the data covering the full first nine months of its 2023 fiscal year, you might be perplexed as to why shares are up so much. During that nine-month window, revenue came in at $1.25 billion. That's actually down 4.4% compared to the $1.31 billion reported one year earlier. Interestingly, this decline came even as the number of locations the company had in operation had risen year over year, climbing from 1,086 to 1,126. The big culprit then was a 7.4% plunge in comparable store sales. The real weakness for the company came from a 10.2% plunge in brick-and-mortar comparable store sales. By comparison, e-commerce sales actually grew 11.2%, climbing to 14.9% of the company's overall revenue compared to the 12.8% that they accounted for only one year earlier. This push into e-commerce has been a strategy of the company for some time now, even prior to the COVID-19 pandemic. And frankly, it likely will create additional value for investors moving forward.

On the bottom line, the picture for the company during this time was even worse. Net income plunged from $156.7 million in the first nine months of the company's 2022 fiscal year to $89.6 million the same time of its 2023 fiscal year. Operating cash flow was cut by more than half from $112 million to $52.4 million. Even if we adjust for changes in working capital, the metric would have declined, dropping from $177.3 million to $132.5 million. Also on the decline was EBITDA. Year over year, this metric fell from $230.5 million to $150.1 million.

{kind=link}

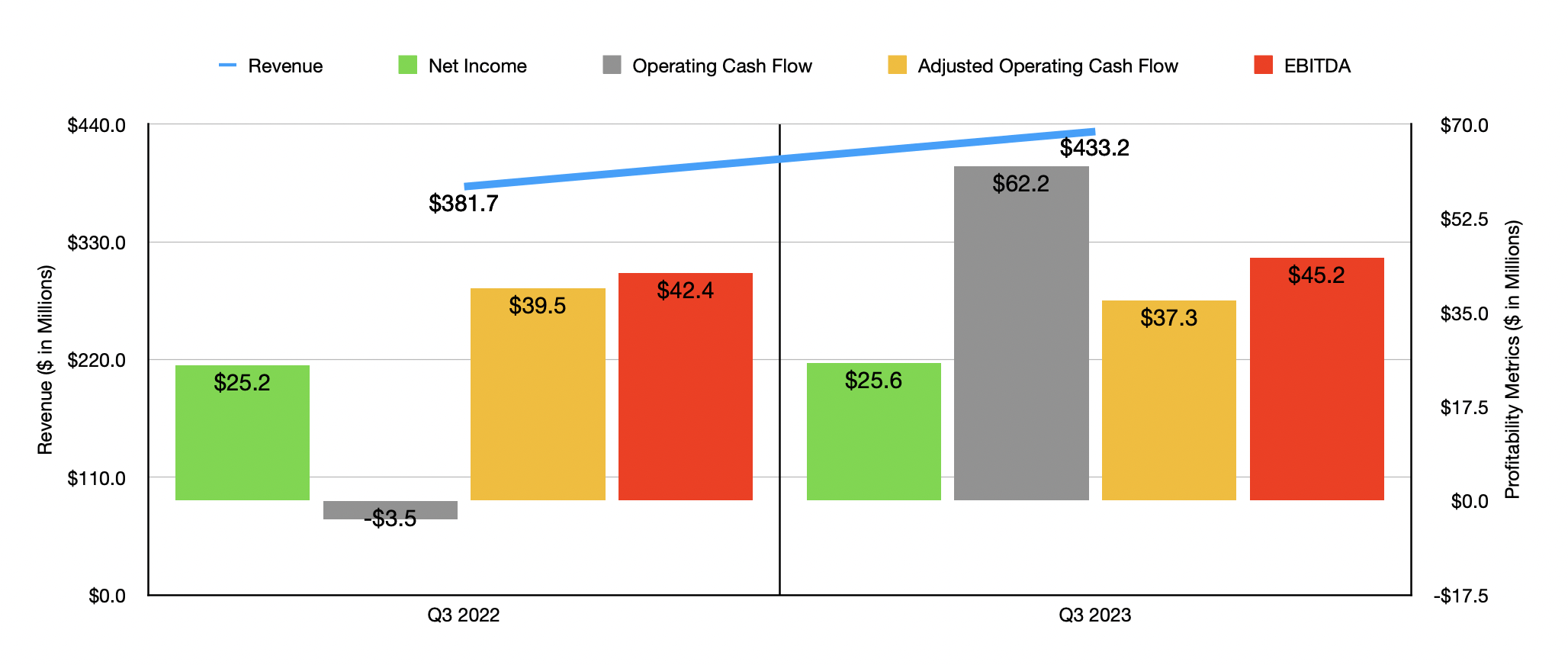

The real magic for the company came in the third quarter on its own. It's only when you look at this data that you come to realize why shares have performed so well in recent months. Revenue during that quarter totaled $433.2 million. That's up 13.5% compared to the $381.7 million reported one year earlier. In addition to benefiting from the aforementioned rise in store count, the company also saw a 9.9% surge in comparable store sales. Management attributed this to a significant improvement in footwear inventory, as well as the shift in focus between footwear and apparel. E-commerce sales skyrocketed 22% during this time. That brought e-commerce penetration to 15% of overall revenue for the quarter.

More likely than not, this trend will continue for the foreseeable future. I say this because the company continues to invest in its digital transformation efforts. In early December of last year, for instance, management announced a strategic investment that it made into both Heady LLC and Heady Digital Products. These investments will help the company accelerate digital transformation efforts, with Heady Providing full-service strategy, design, full stack development, and growth marketing services for Hibbett, while Heady Digital Products will provide omnichannel digital experience management software for Hibbett, as well as other leading brands. This does not mean that the company is going to be ignoring its brick-and-mortar operations. In fact, during the latest quarter, brick-and-mortar sales increased nicely, shooting up 7.9% on a comparable store basis.

Considering the inflationary pressures that Hibbett and similar firms have faced, the business did quite well from a profitability perspective. Net income during this time actually totaled $25.6 million. That's marginally higher than the $25.2 million reported the same time one year earlier. Operating cash flow went from negative $3.5 million to positive $62.2 million. Though if we adjust for changes in working capital, it would have dipped slightly from $39.5 million to $37.3 million. Meanwhile, EBITDA for the business ticked up modestly from $42.4 million to $45.2 million.

For 2023 in its entirety, management has been a bit vague when it comes to guidance. They anticipate total revenue for the company rising at the low single-digit rate, with comparable store sales ranging between flat and being up in the low single digits. This would imply a very strong final quarter for the fiscal year. It should be aided by between 30 and 40 net new stores, with 29 having already been opened as of the end of the third quarter. Earnings per share, meanwhile, should be between $9.75 and $10.50. At the midpoint, that would translate to profits of $134.7 million. No guidance was given for other profitability metrics. But if we annualize results experienced so far, an approach that would be rather conservative considering what the company is likely to report for the final quarter, we would get adjusted operating cash flow of $157.4 million and EBITDA of $164.8 million.

{kind=link}

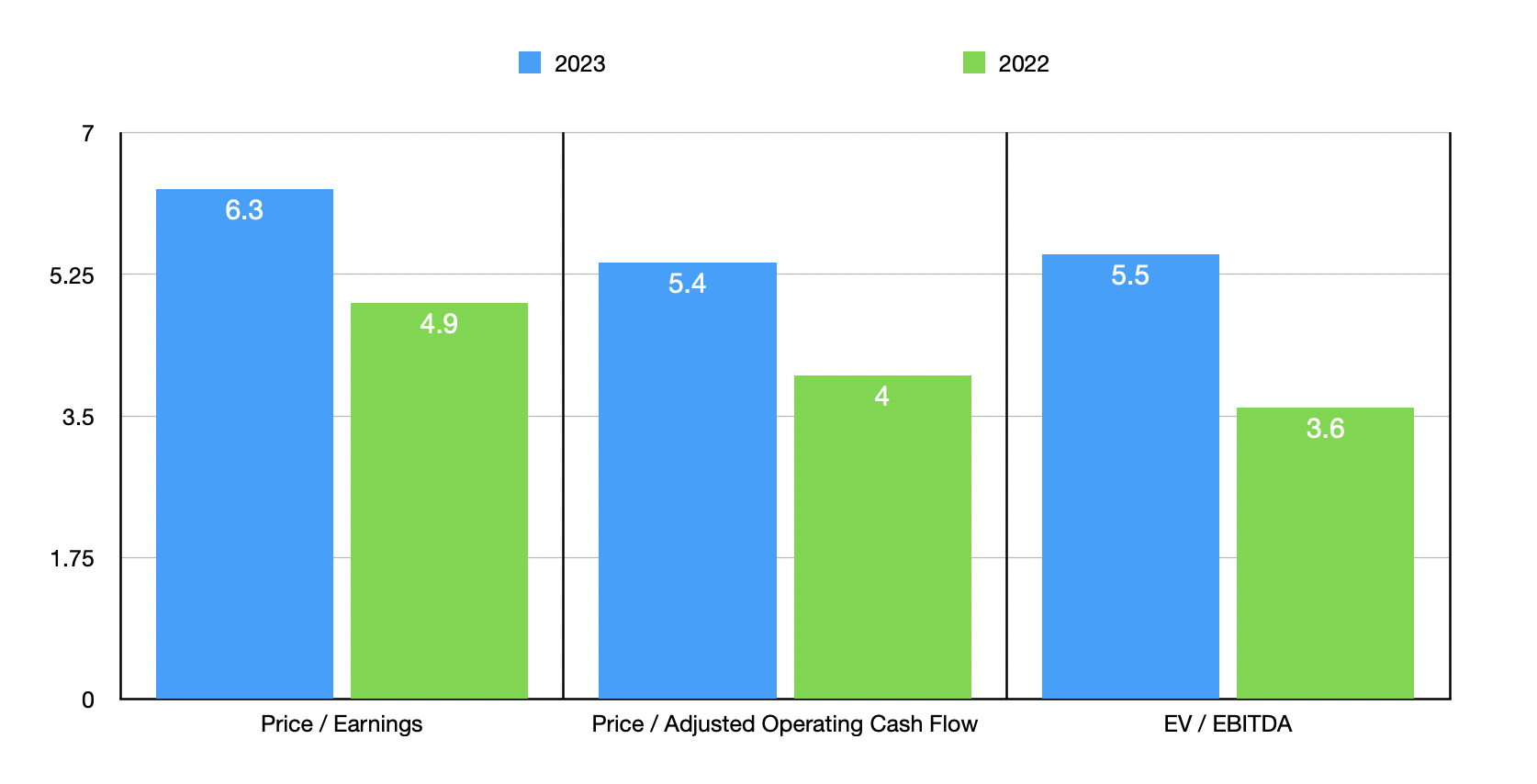

Based on these numbers, Hibbett is trading at a price-to-earnings multiple of 6.3. The price to adjusted operating cash flow multiple should be 5.4, while the EV to EBITDA multiple should come in at 5.5. By comparison, if we were to use the data from 2022, these multiples would be lower at 4.9, 4, and 3.6, respectively. As part of my analysis, I compared the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 4.7 to a high of 11.9. Two of the five firms were cheaper than our prospect. Using the price to operating cash flow approach, the range was from 5 to 123.6, with only one of the five firms being cheaper than Hibbett. And finally, using the EV to EBITDA approach, the range was from 2.6 to 8.1. In this case, three of the five companies were cheaper than our prospect.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Hibbett |

| 6.3 |

| 5.4 |

| 5.5 |

| Dick's Sporting Goods ( DKS ) |

| 11.9 |

| 21.6 |

| 5.9 |

| Big 5 Sporting Goods ( BGFV ) |

| 5.2 |

| 5.0 |

| 2.6 |

| Sportsman's Warehouse Holdings ( SPWH ) |

| 4.7 |

| 5.7 |

| 3.1 |

| Academy Sports and Outdoors ( ASO ) |

| 8.5 |

| 11.1 |

| 5.4 |

| Escalade ( ESCA ) |

| 8.5 |

| 123.6 |

| 8.1 |

Takeaway

Although much of the company's 2023 fiscal year was problematic, Hibbett demonstrated relatively strong results, particularly on the sales side, during the third quarter of its 2023 fiscal year. More likely than not, we will see continued strength for the business in the near term. On an absolute basis, shares of the company look very cheap even though they have risen so much since I last wrote about it. On a relative basis, however, they do look closer to fair value. For those who are drawn to this space, I would say that Hibbett does offer some additional upside from here, enough, at least enough to warrant a soft 'buy' rating at this time.

For further details see:

Hibbett: Still A Sporting Good Prospect On A Change In Fortunes