HIBB - Hibbett: The Market Is Ignoring A Valuable Asset

2023-08-21 15:06:20 ET

Summary

- Hibbett is currently trading at 6.5x the low point of recently lowered FY2024 EPS guidance.

- This low multiple can be attributed to Hibbett’s declining comparable same-store sales growth, which is occurring while management is maintaining a high level of capital expenditures.

- Additionally, it seems investors are currently not very enthusiastic for small-cap stocks as large-caps are usually deemed safer in times of uncertainty.

- I believe Hibbett's network of stores in underserved communities gives it a valuable asset that will allow its same stores sales to stabilize and return to growth. This should lead to multiple expansions.

- The main risk of this investment thesis is that Hibbett's network of stores might not be as valuable as I believe it is.

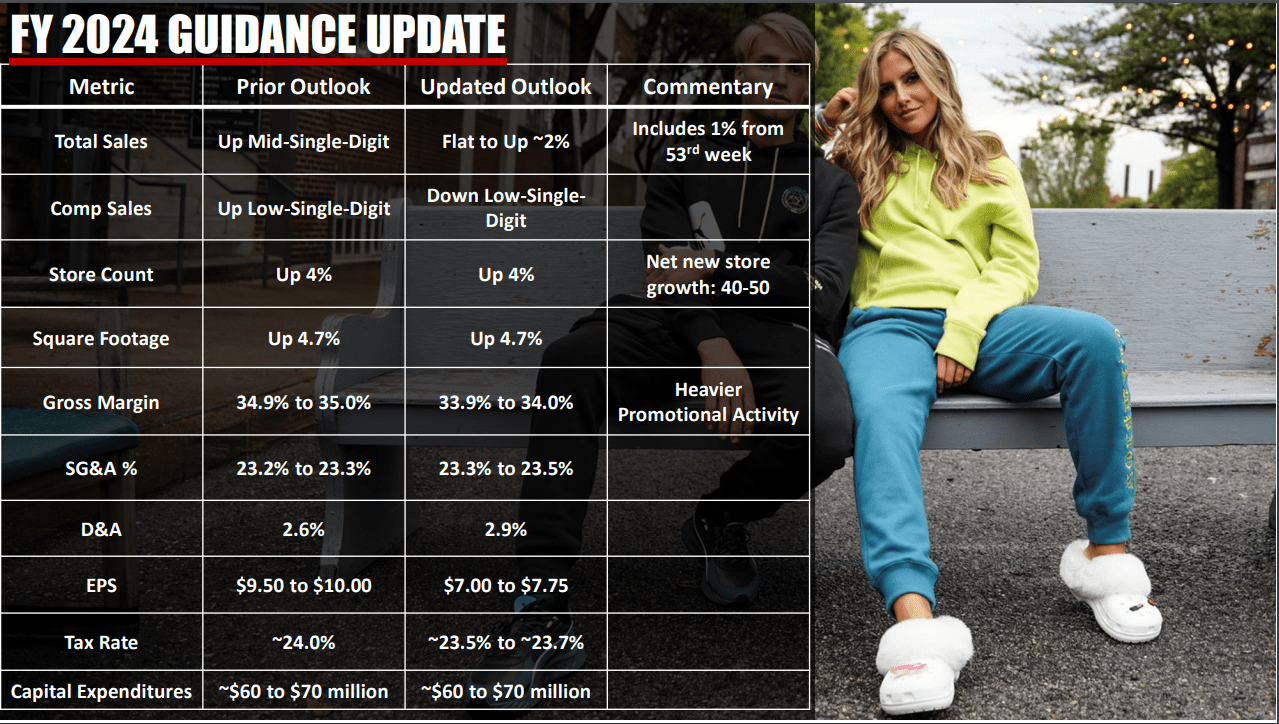

Hibbett, Inc. ( HIBB ) is facing many uncertainties in the next 6-18 months, and investors have responded with a vote of no confidence as its stock is down 35% year to date. This lack of confidence primarily stems from the recent reduction in FY2024 EPS guidance which were announced with Q1 earnings results. This reduction in guidance primarily stems from a higher likelihood of consumer weakness as the year goes on, and the retail industry's dynamics that have led to a surplus of inventory and increased promotional activity.

Hibbett Updated FY2024 Guidance (Q1 Earnings Presentation)

{kind=link}

I would also attribute the decline in the stock to a general distaste from market participants for small and micro-cap stocks, and terminal value fears for the business. So far in 2023 the Russell 2000 has provided investors with a 6.2% return while the S&P 500 has risen 14%. Large caps are generally perceived as safer investments in times of economic turmoil and uncertainty. While economic data has generally been positive so far this year, undertones of general recession fears have been strong and I believe the banking crisis in May caused investors to fear that smaller businesses may run into liquidity issues.

In addition to this lack of enthusiasm for small cap stocks, I think investors are worried about terminal value risks for Hibbett specifically. Prior to the pandemic, Hibbett’s same store sales, margins and ROIC were all trending down. This poor performance led to multiple contraction for the stock which, along with the decline in EPS, caused the stock to decline 75% from its peak in 2014 to its bottom in 2019. This decline stopped in 2020 when EPS almost tripled from the prior year, ROIC returned to where it was in 2014, and same store sales growth began to rise rapidly.

This likely leaves investors questioning whether the return to strength was simply due to fiscal stimulus and pandemic spending habits or if it is from Hibbett strengthening its position in the footwear and apparel industry. The former would put Hibbett back in the declining position it found itself in prior to the pandemic.

What is the correct interpretation of Hibbett's situation? I believe that Hibbett’s brand and logistics network that primarily focuses on underserved areas in the U.S. is a strong asset. The strength of this asset should lead to Hibbett’s revenue, earnings and same store sales growth stabilizing, which would lead to multiple expansion as investors take notice. With this view, I believe Hibbett's stock has 80%+ upside potential within the next 12-24 months and more beyond that. Additionally, I believe that the low multiple and the value of Hibbett’s brand and store network makes it an attractive acquisition. The longer the market chooses to ignore Hibbett the more likely the acquisition scenario becomes in my view.

In this article, I’ll provide an overview of the business and its competitive advantages, an overview of its past financial results, and the assumptions and thought process behind my price target.

Business Overview

Hibbett is an athletic retailer with stores that are primarily located in underserved communities in the U.S. As of the end of Q1 2023, Hibbett operated 1143 stores in 36 states. While the company has a long history, it recently pivoted to focus more on fashion and premium footwear as opposed to commoditized sporting goods. Hibbett has strong relationships with vendors from premium brands due to its status as a trusted brand with a strong logistics and store network in underserved communities.

This is where the competitive advantage lies. Brands such as Nike (NKE), Jordan, Puma, Adidas, Timberland and UGG retain a good relationship with Hibbett because these underserved communities have important customers which they would not be able to reach without large investments in those areas. Rather than use large amounts of capital for this, these brands distribute through Hibbett.

During Hibbett’s 2021 investor day presentation Kandace Turner, Hibbett’s vice president of stores, spoke to the strength of Hibbett’s relationship with Nike:

Footwear is our biggest sales driver and a large portion of that is from one of our key partners, Nike. Our partnership with Nike is fueled by our ability to operate stores in underserved markets. And our ability to bring brand names like Nike to these markets is a driving force for our repeat customers.

For some perspective, the following are stores counts for Hibbett and some competitors in select U.S. states that contain underserved markets.

| Alabama |

| Mississippi |

| Tennessee |

| Texas |

| Hibbett |

| 110 |

| 72 |

| 68 |

| 132 |

| Finish Line |

| 8 |

| 5 |

| 17 |

| 77 |

| Foot Locker |

| 10 |

| 7 |

| 7 |

| 16 |

Ben Knighton, Hibbett’s senior VP of operations, provided some metrics in the 2021 investor day presentation to show the value of this network:

Approximately 70% of our stores have 2 or fewer competitors within a 15-minute drive. And when looking at the total distribution footprint for sneakers and athletically inspired apparel, less than half of these markets have what we would consider true competition for our customer base. Each of these factors underscore the advantage of our positioning in underserved markets.

Regardless of where earnings go over time, this network of stores and the trust the brand has in these communities is a valuable asset. I would be more wary of Hibbett’s terminal value risk if it weren’t for this.

Past Financial Results

Hibbett has had mixed financial results over the last few decades. Earnings and ROIC were trending up from 2010-2014 but were largely declining from 2014 to 2019. This change was primarily driven by changes in same store sales growth.

The following are same store sales growth by fiscal year since 2010:

| 2010 |

| 0.1% |

| 2011 |

| 9.8% |

| 2012 |

| 6.8% |

| 2013 |

| 6.9% |

| 2014 |

| 1.8% |

| 2015 |

| 2.9% |

| 2016 |

| -0.4% |

| 2017 |

| 0.2% |

| 2018 |

| -3.8% |

| 2019 |

| 2.2% |

| 2020 |

| 5.3% |

| 2021 |

| 22.2% |

| 2022 |

| 17.4% |

| 2023E |

| -LSD% |

In FY2010, the economy was starting to return to strength after the financial crisis. From that point through FY2013, Hibbett was growing comparable same store sales at a high rate and the stock followed. The increase in comparable same stores sales in this period was due to increased foot traffic in stores and increased retail prices. From the start of FY2011 to the end of FY2013, Hibbett’s stock rose 150%.

Comparable same store sales began to fall as increases in footwear sales were offset by declines in apparel and equipment. This is when the business began the shift to focus more on premium fashion and footwear brands as opposed to equipment and general apparel. From FY2016 to FY2019 same store comparable sales were stagnant or declining. In this period the stock fell 75-85% depending on the start and end points.

This volatility in comparable same stores sales had a two pronged effect on Hibbett’s stock. First, it had an effect on earnings as the changes in demand led to changes in revenue and margins. Second, it had an effect on the stock's multiple. When same stores sales were growing investors were more bullish on the outlook for the stock and were willing to pay a higher multiple of earnings for it. When same store sales were falling, the opposite was true.

In the 2010-2013 period, the stock consistently traded above 20x trailing EPS. Once same store sales fell, the multiple that investors were willing to pay gradually declined and the stock traded down to a low of 6x trailing EPS in 2017.

Currently, Hibbett is in a period of high earnings relative to its past, but same store sales growth is stagnant/declining. The stock is reflecting this negativity as it is trading 4.5x trailing EPS. If same store sales growth reverses course and begins to rise, the stock’s multiple could expand in a big way.

Forecast

Hibbett’s management lowered FY2024 guidance when they announced Q1 earnings. They are currently guiding for revenue to be flat to up 2%, comparable sales to be down low single digits, and margins to decline. This is all supposed to lead to an EPS range of $7.00 to $7.65 which puts the stock at about 6x the low point of this guidance.

This multiple is obviously low compared to Hibbett’s past multiples as investors don't seem to believe these earnings will hold up over a long period of time. But it also has to do with Hibbett’s plans for maintaining high capital expenditures over the next few years related to more store openings and digital infrastructure. Declining earnings coupled with increasing capital expenditures leads to lower ROIC. These investments may pay dividends in future years, but investors are very impatient these days especially with small cap stocks in my opinion. The lower ROIC expectations are further contributing to the lower earnings multiple.

Management is guiding for $60-70 million in capital expenditures for FY2024 which is in line with capital expenditures in the past two years when earnings were growing. While this plan will reduce cash flow in the near term, it shows management’s confidence in Hibbett’s long term prospects, its new business plan, and the value of its store network.

Management is also showing their confidence with recent open market stock purchases. CEO Mike Longo purchased 7,500 shares recently at around $36 per share and another insider purchased 2,000 shares also at around $36.

My bet for Hibbett is that the value of its network will show itself over the next few years as revenue and earnings stabilize after this period of economic uncertainty. The premium brands will maintain their relationship with Hibbett due to this network and competitors will close down or leave the area as they will have difficulty competing with Hibbett and other online retailers. Once investors see this and once small-cap stocks become more favorable in general, I believe the stock's multiple will rise.

I am estimating EPS of $8.20 in FY2025 based on 3% revenue growth over FY2024 to $1.76 billion, an 8% operating margin, $5.2 million in interest expenses, a 22% tax rate, and 12.7 million fully diluted shares outstanding. Using a 10x EPS multiple, the stock would trade at around $82 for 81% upside from today’s price.

Risks

In the near term, the main risk in this bet is that the economy worsens and same store sales continue to decline. If FY2024 EPS comes in below the low point of guidance, the multiple could fall further as the company loses more credibility than it has already lost, given how often Hibbett's quarterly earnings have come in below expectations in the past few quarters. The trailing EPS multiple fell as low as 3.7x in June and I don’t see why the stock can’t fall to that multiple again especially given the lack of enthusiasm for small cap stocks.

Hibbett will also be releasing Q2 results shortly . Expectations are clearly low given the state of the retail industry and the disappointing Q1 resulted that led to multiple analyst downgrades . Additionally, the percentage of Hibbett's float sold short is 15% so many investors are clearly not expecting much from Q2. However the value I am ascribing to Hibbett's network will remain no matter what Q2 results show. If results are weaker than expected, it could be a chance for investors with longer term time horizons to add to positions.

Longer term, the risk is that the financials trends from before the pandemic continue from here. Those trends were declining same store sales, declining earnings, and declining ROIC. This is how terminal value risk would show itself in Hibbett's financials. Perhaps brick and mortar retail will become irrelevant, or the premium brands will find a way to directly sell and market to the underserved communities that Hibbett focuses on.

A key part of my confidence in this bet is due to the strength of Hibbett’s store network. There are many retailers trading at low to mid-single digit EPS multiples, most of which I don’t want to invest in given some of my doubts about their long term prospects. However I view Hibbett’s store network as a margin of safety due to its potential value to an acquirer.

JD Sports acquired Finish Line in 2018 for $554 million and at the time of the acquisition, Finish Line generated $54 million in pre-tax operating income in the twelve months prior. This means the acquisition was for about 10x operating income.

Finish Line is a valuable brand just as I believe Hibbett is. If Hibbett were acquired for 10x operating income, the sale price would be about $97. I don’t like to invest based on the hopes of an acquisition, but I think this provides a bit of a margin of safety. Even if this acquisition does not happen, Hibbett will “acquire” itself as management continues to repurchase shares at a rapid rate.

In general, if Hibbett's store and logistics network is not as valuable as I think it is, my investment thesis will fall apart.

Final Thoughts

Like many retailers, Hibbett’s stock is trading at a very low multiple of its trailing EPS. This is primarily due to economic uncertainty, declining same store sales growth, declining earnings, and a general lack of enthusiasm for small-cap stocks.

However I think the market is ignoring the value of Hibbett’s store and logistics network in underserved U.S. communities. This network reduces the terminal value risk of the business and provides a margin of safety as it would be a valuable asset for a larger business to acquire, similar to how JD Sports acquired Finish Line in 2018.

As investors gain confidence in Hibbett once same store sales growth and earnings stabilize, I estimate the stock will trade at $82 per share within the next 12-24 months. This estimate is based on FY2025 EPS of $8.20 and a 10x EPS multiple.

The main risk of this thesis is that Hibbett’s store network is not as valuable as I think it is. The value of this network is the backbone of my thesis so it must be strong for my price target estimate to hold up. Given the stock's current multiple, the market is clearly taking the other side of that bet. This is why the risk/reward is favorable in my view.

For further details see:

Hibbett: The Market Is Ignoring A Valuable Asset