HIBB - Hibbett: Vulnerabilities In An Uncertain Retail Landscape

2023-09-20 16:00:36 ET

Summary

- Hibbett's business model is attractive, but it faces threats from e-commerce and low-cost producers. We believe its competitive position is deteriorating.

- The company has experienced declining sales and margin erosion due to current economic conditions, as its target demographic is overly exposed.

- Despite appearing attractively priced, Hibbett's trading multiple is primed to expand through a decline in profitability.

Investment thesis

Our current investment thesis is:

- Hibbett's ( HIBB ) business model is attractive, with a strong market share developed through a focus on key demographics. We see the rise of e-commerce and low-cost producers as a key threat to its position.

- The business has faced declining comparable sales and margin erosion in recent quarters, as current economic conditions disproportionately harm the business.

- Despite the business looking attractively priced, we suspect its trading multiple will expand as EBITDA declines, closing the gap.

Company description

Hibbett, headquartered in Birmingham, Alabama, is a leading athletic-inspired fashion retailer with a focus on footwear, apparel, and equipment. The company operates primarily in small and mid-sized markets across the United States through its physical stores and e-commerce platform. Hibbett's target customer base includes individuals interested in sports, fitness, and active lifestyles.

Share price

Hibbett's share price performance has been poor during the last decade, losing over 10% of its value while impressive gains have been made by the wider market. The struggles are a reflection of difficulties with improving its financial results.

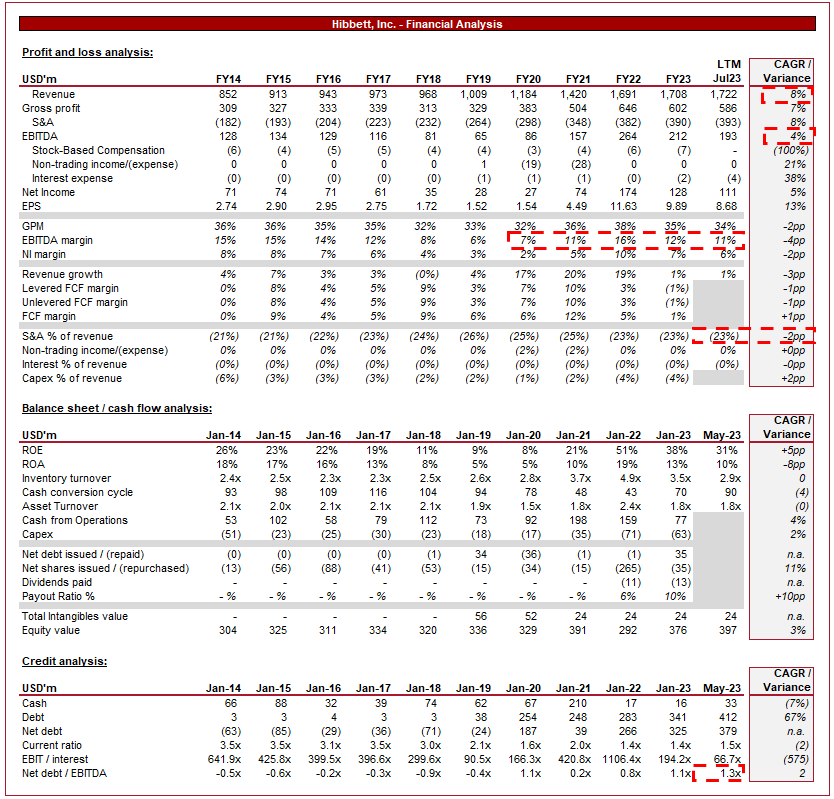

Financial analysis

Hibbett Financials (Capital IQ)

{kind=link}

Presented above are Hibbett's financial results.

Revenue & Commercial Factors

Hibbett's revenue has grown well despite the share price performance, with a CAGR of 8% into LTM April '23. Growth has been incredibly consistent, with only a flat year in FY18.

Business Model

Hibbett operates as a specialty retailer, focusing on athletic footwear, apparel, equipment, and accessories. The company's niche approach allows it to cater to a specific customer segment and specialize in the offering, with a broad product range and the development of a brand synonymous with sports.

Further, Hibbett specifically targets small and mid-sized markets, seeking to cater to underserved individuals outside of major cities. The benefit of this is reduced competition, allowing for greater market share capture. In conjunction with this, Hibbett aims to be an active part of the local communities it serves through partnerships and sponsorships, deepening its ties to its target through on-the-ground marketing.

Hibbett has good relationships with the leading sports and national brands, providing them access to markets not easily represented by their other leading retailers. Once again, this ties the value of Hibbett to its market position.

The company prioritizes providing an engaging in-store experience. The company has invested in staff training, visual merchandising, and a wide range of products contribute to offering a unique shopping experience. Supporting this is the development of its e-commerce platform, enabling customers to shop online and access a broader product assortment. This has allowed the business to develop an omnichannel approach, a critical development in the industry given the threats e-commerce-only businesses offer.

Further, the company takes a "clustered expansion" approach to developing its physical footprint. Hibbett seeks to open new stores within close proximity of existing locations. From an operational perspective, this allows for efficient logistics and local marketing. Commercially, this allows the business to develop its expertise in markets that are known to be lucrative. As the following illustrates, the business has a strong national presence.

{kind=link}

Finally, Hibbett offers a loyalty program, allowing customers to earn rewards and discounts based on their purchases and engagement. Many B2C businesses have experimented with these schemes in the last decade, finding success where customer sales can be recurring. Although we do not believe the apparel industry is best positioned for this, Hibbett's broad range of products improves the optionality of this.

Apparel Industry

The apparel industry has been impacted by a number of trends, which on a net basis, we feel has degraded the competitive position of Hibbett. These factors are a primary reason for its decline in margins.

During the last several years, we have seen an increasing number of businesses with supply chains in the Far East conducting heavy marketing to take market share. With a lack of physical presence, they have been able to undercut the market. This has contributed to a significant increase in competition, contributing to further discounting.

Additionally, the rise of e-commerce has contributed to increased competition for traditional retailers, as consumers now have far more choices and are able to hunt for discounts. This point specifically has degraded Hibbett's strong position in its existing market, softening its ability to achieve comparable store growth.

Offsetting these factors in recent years has been the growing interest in fitness and sports, contributing to a rise in the demand for athletic apparel that is flexible for different lifestyles. This increasingly means fashionable, which many of the brands it stocks (such as Nike ( NKE )) have responded to. This trend looks to be driven by a fundamental shift in societal views on health and well-being.

Competitive Positioning

Our views are that Hibbett's competitive position revolves around the following factors:

- Local Focus. Hibbett's community-focused approach resonates well with consumers who value local businesses and personalized shopping experiences. The company's business model is centered on this key advantage, as it should allow for strong relationships with suppliers to continue as some face a reduction in allocation (Such as Foot Locker ( FL )).

- E-Commerce Expansion. Hibbett's investment in its online platform is critical to maintaining its competitive positioning in the face of new entrants within the industry. When packaged with its strong store footprint and its loyalty scheme, we believe Hibbett offers a compelling package.

- Market Expansion. Although there could be the impression its local approach restricts store growth, thus far the business has been able to grow healthily, with 18 new stores in the last 2 quarters. This will support overall top-line performance (up 2% in the L26W YoY).

Economic & External Consideration

Current economic conditions represent a key risk to the business, with high inflation and elevated rates contributing to a decline in discretionary spending as consumers protect finances. Hibbett's key demographic is overly exposed to the impact of this, implying the business will suffer to a greater degree.

As the following illustrates, the home affordability index has hit a decade low (and is below 100 for the first time in this period), suggesting consumers are struggling with living expenses, leaving little for discretionary living spending. Having enjoyed the spending associated with Covid-19 payments, Hibbett now looks exposed.

In the most recent quarter, Hibbett experienced a (7.3)% decline in comparable sales, with revenue trending down QoQ. This illustrates the struggles the business has faced, with no real evidence to imply this is slowing. Further compounding this is increased investment in promotional activity, contributing to margin erosion.

Net Sales (Hibbett)

The only positive we observe is that shrink has not had a material impact on GM %. This has been a major talking point in recent years, with many of its peers struggling with the issues. This is potential due to its community approach and strong customer service, dissuading the behavior.

Margins

The major financial issue Hibbett has faced is the decline in margins, with EBITDA-M falling from 15% in FY14 to 11% in LTM April '23. This has meant, despite consistent revenue growth, EBITDA declined every year between FY14 and FY19. Only the post-pandemic boost has brought the business back to a reasonable level.

This does raise a serious concern that as revenue continues to soften, which we expect to be the case, margins will also fall. We consider this to be a bigger risk to the long-term success of the business than near-term revenue issues.

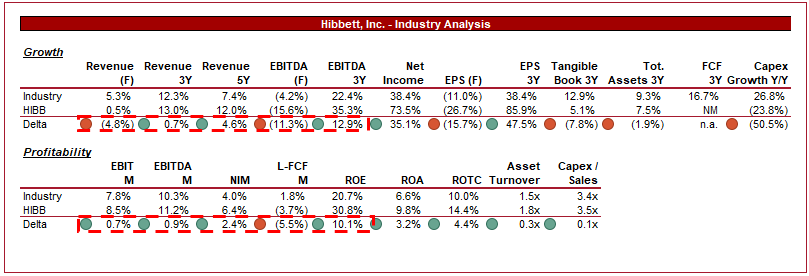

Industry analysis

Specialty Stores Stocks (Seeking Alpha)

{kind=link}

Presented above is a comparison of Hibbett's growth and profitability to the Average of its industry, as defined by Seeking Alpha (22 companies).

Hibbett performs moderately well compared to the peer group. The company's growth has been strong despite the decline in the LTM period, allowing for outperformance across both profitability and revenue. This is attributable to the strong performance post-pandemic.

Further, the company's margins are slightly above average, although our concerns around deterioration suggest Hibbett could fall below the average in the coming 12-24 months.

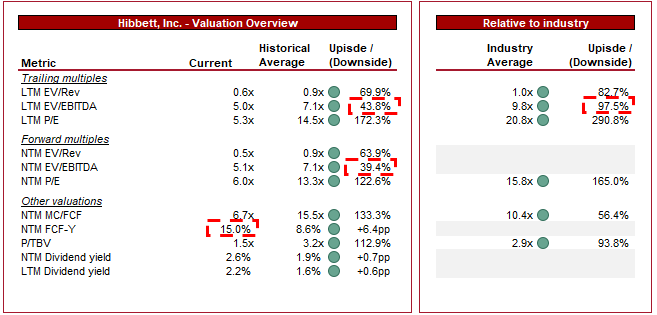

Valuation

{kind=link}

Hibbett is currently trading at 5x LTM EBITDA and 5x NTM EBITDA. This is a discount to its historical average.

Our view is that Hibbett's performance is currently elevated relative to its historical average but, on a normalized level, is likely in line. We purposely do not mention this in connection with its multiple because the margin uncertainty means the discount to its historical average is deceiving. It's very likely this multiple will expand as profitability and sales fall, contributing to the discount rapidly shrinking. This is a similar case for its delta to the industry average, as on paper a 97.5% discount looks incredibly attractive.

We believe the margin and sales risk is far too high. It was only in FY20 that Hibbett had an EBITDA-M of 7%. At this level, its LTM EBITDA multiple would be 7.6x, an unjustifiable premium to its historical level.

Final thoughts

Hibbett is a solid retailer that has carved out market share by targeting a particular demographic. We believe its competitive position is healthy but has certainly declined in recent years, and suspect it will continue to do so. The biggest issue is that comparable growth is poor, and margins are likely to follow suit. With no reason for positive price action, we suggest patience.

For further details see:

Hibbett: Vulnerabilities In An Uncertain Retail Landscape