TTFNF - HIE: A Term Fund At A Discount

Summary

- HIE is trading at an attractive discount despite the better relative performance over the last year, thanks to its energy exposure.

- A discount for a term fund is something that can be exploited, but we still have some time before the termination date.

- The latest annual report shows us that net investment income has risen, which should help support the monthly distribution to shareholders.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on January 20th, 2023.

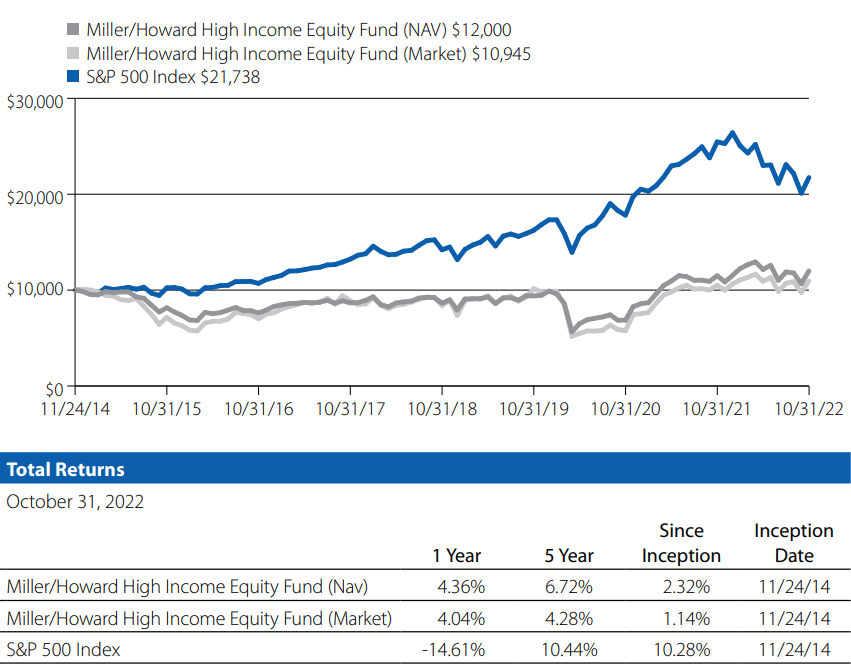

Miller/Howard High Income Equity Fund ( HIE ) finished off 2022 in a relatively strong position with positive results. That was much better than what could be said for most of the rest of the equity and even fixed-income markets. This would be thanks to the heavier energy exposure this fund runs. Other contributors to the fund's better relative performance would be the higher allocations to financials and healthcare while keeping tech positioning very minimal in the portfolio.

Despite the stronger results, this fund continues to trade at an attractive discount. As a term fund, that's one of the most attractive things we can see in this fund structure. As the term date comes closer, there should be a natural decline in the discount, where investors can ultimately realize the difference between the share price and the NAV.

We mostly covered the topic of energy helping the fund previously in November . The last couple of months didn't show much difference from what we saw through most of 2022. Since then, we see that HIE has put up slight gains.

HIE Performance Since Previous Update (Seeking Alpha)

The Basics

- 1-Year Z-score: -0.08

- Discount: 8.17%

- Distribution Yield: 5.79%

- Expense Ratio: 1.92%

- Leverage: 19.10%

- Managed Assets: $228.72 million

- Structure: Term (expected November 24th, 2024)

HIE is classified as a "diversified, closed-end management investment company whose primary objective is to seek a high level of current income with capital appreciation as a secondary objective."

They intend to invest "at least 80% of its total assets in dividend or distribution paying equity securities of US companies and non-US companies traded on US exchanges. The Fund will seek to invest in securities that the Investment Advisor considers to be financially strong with reliable earnings, high dividend or distribution yields, and rising dividend growth. The Fund may invest up to 25% in Master Limited Partnerships ("MLPs"), generally in the energy sector. The Fund intends to engage in an options writing strategy consisting of writing put options on securities already held in its portfolio or securities that are candidates for inclusion in its portfolio. It may also engage in covered call writing strategies, and it may buy put and call options. The Fund may write covered put and call options up to a notional amount of 20% of the Fund's total assets."

The fund's higher expense ratio isn't ideal. That eats away returns that could otherwise be going to shareholders. When including the leverage expenses, the fund shows a total expense ratio of 2.34%.

While the fund carries a moderate amount of leverage, it showed some deleveraging at the end of the last fiscal year. At around a 20% leverage ratio, it certainly wouldn't appear to be a forced deleveraging. This is normally a negative for a fund because it means they could potentially be selling securities at lows. Due to HIE having a relatively successful year, that wouldn't necessarily be a concern.

With rising interest rate costs, lowering leverage isn't necessarily bad. That's because they borrow at a floating rate. At the end of their fiscal year, they averaged an interest rate of 1.74% on their ~$49.3 million balance. At the end of October 31st, 2022, they had borrowings of $44.5 million but were paying an interest rate of 3.89%. Interest rates have only increased further, so we know these costs are rising.

Performance - Attractive Discount

HIE had enjoyed trading at premium levels prior to 2020. During COVID, the fund cut its distribution, and the discount appeared almost immediately. It slowly began to rise to narrow that discount, but it's been essentially hanging out at the 8% level for the last year or so now.

Ycharts

Considering that the fund should liquidate in November 2024, we would presume that the discount should narrow over the next year leading into the term date.

There are two caveats to this, however.

The first would be that the Board can extend the termination date for a year without shareholder approval.

Second, they leave in language that shareholders could vote to extend or shorten the term. Meaning that the Board could very likely bring up the possibility of removing the term structure and switching to perpetual.

This fund came in at a time when the CEF 2.0 wasn't established, so the language is more ambiguous than we see in funds today. CEF 2.0 is just a term to describe funds that launched after 2018, coming to market with term structures and the launch costs being paid for by the fund sponsor.

One of the reasons I'm not too concerned is because institutional ownership in this fund is quite high. In fact, Saba Capital is the largest shareholder at nearly 15.5%, and they are a known CEF activist. If anything, I was hoping they'd be able to get this liquidation party started early, but that hasn't been the case thus far.

All else being equal, if they liquidate as expected and we don't get a black swan event, HIE is likely to provide respectable returns. Buying a term fund heading into liquidation means there is guaranteed alpha because that discount can be realized as opposed to a fund that can continue trading at a discount.

Of course, the other way it could work is if the NAV comes down to meet the share price. Important to note the difference here between guaranteed "alpha" and guaranteed "return." A return is not guaranteed.

I've discussed HIE and what has driven its historical results ad nauseam.

However, here is a quick recap for those that might be new. Over the long term, HIE has underperformed the S&P 500 Index considerably. The primary reason for this is due to the higher energy exposure. That was the portion of their portfolio last year that saw the fund significantly outperform the S&P 500 Index. I wouldn't consider the S&P 500 Index as an appropriate benchmark.

{kind=link}

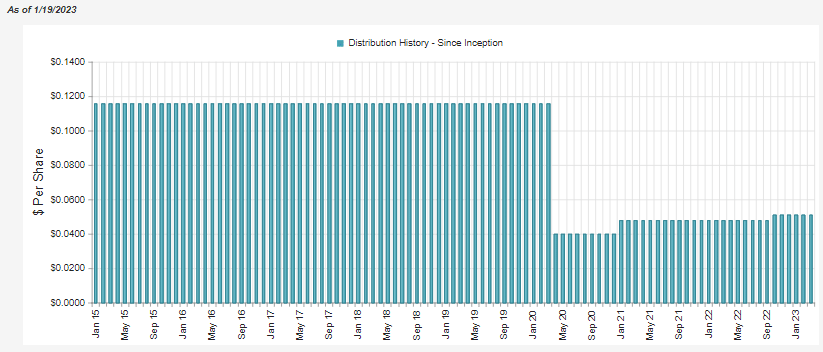

Distribution - NII Going In The Right Direction

As mentioned above, HIE cut its distribution in 2020. Since then, they have been moving it up a bit.

{kind=link}

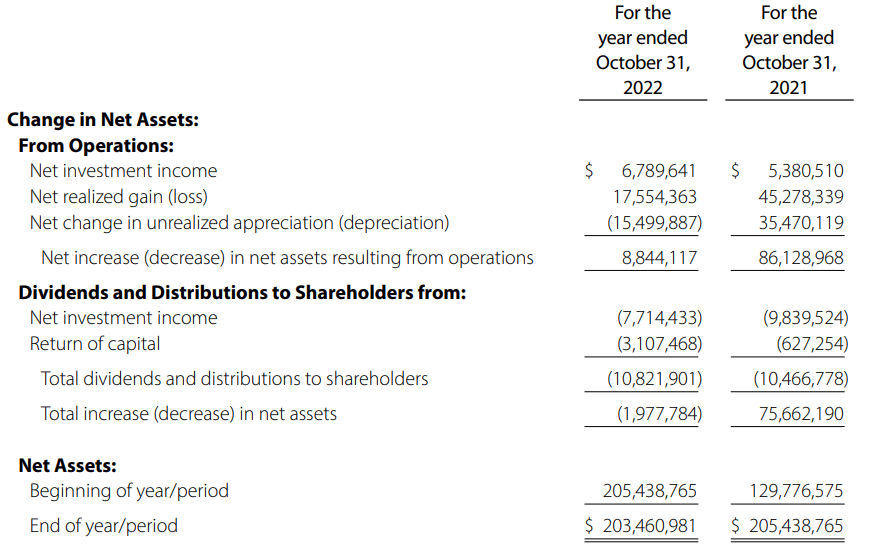

With their latest annual report , we can see that net investment income increased year-over-year. NII is the fund's total investment income minus the fund's expenses. So that means despite the fund's higher leverage expenses, the underlying portfolio is still generating more NII for shareholders. That's a positive as it could mean more distribution increases in the future.

{kind=link}

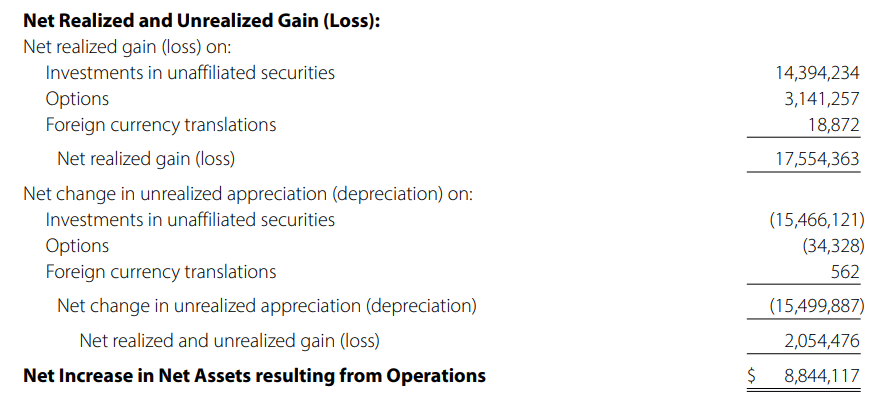

The fund also implements an options writing strategy to generate option premium. That means the fund can generate realized capital gains through that strategy even in a flat or down market. At the end of October, they actually listed zero options positions. However, they provided the breakdown through the year;

We are enhancing the income in the portfolio through the sale of options. For the fiscal annual period ended October 31, 2022, we sold calls on 91 positions, of which 64 expired worthless after we collected the premium, and we had 26 exercised. We bought to close 1 position. Zero positions remained open as of October 31, 2022. Our option positions' notional value represented 0% of total assets as of the end of the period, below the 30% limitation.

In the last year, the fund generated around $3.14 million in options premium.

{kind=link}

That might not seem like much, but adding that to the ~$6.8 million NII reflected above, we see that the distribution to shareholders was almost entirely covered through those means.

Of course, we can't ignore the unrealized appreciation in the portfolio either. When combining that, we see that the fund's net assets did decrease by almost $2 million. However, that was a drop in the bucket compared to fiscal 2021's strong results. At that time, the fund enjoyed even stronger returns as everything rebounded from 2020.

For tax purposes, the fund lists return of capital. This can be both destructive but also good ROC. This is because the fund holds a sizeable allocation to MLPs, and the distributions from those are almost entirely ROC. That gets passed through to the distributions from HIE to the shareholders.

{kind=link}

HIE's Portfolio

One thing that is always worth pointing out for HIE is the fund's turnover rate. They have one manager, and he's a really busy guy because the turnover has been as high as 277%. So the latest fiscal year showing 116% is actually moderate compared to how often this manager usually flips positions. This is important to note because it means the portfolio constantly changes.

Additionally, that can cause the NII the portfolio generates to fluctuate significantly from year-to-year. So while the increase in NII has been nice, it's hard to know exactly what was the underlying portfolio bumping up their distributions or swapping out portfolio positions for higher yielders.

For positioning, at the end of October 31st, 2022, the fund was heavily weighted toward energy positions.

{kind=link}

This is a common theme for this fund; even despite the higher turnover, the fund stays mostly relatively energy focused. That's expected as the fund outlines the high-yield dividend focus sectors and industries. The energy sector and MLPs can be an important piece as they are generally higher-yielding securities.

The largest part of HIE's portfolio is Mount Vernon Liqudi Assets Portfolio, LLC. This private fund "invests in high-quality, short term investments, similar to a money market fund, which can be redeemed daily." Details beyond that are limited, but it seemed to have been earning 3.21% at the end of October. Given its short term focus and if it's invested similarly to a money market fund, the yield should be higher today.

After that, the largest position is another short-term investment. This time it's the Morgan Stanley Institutional Liquidity Fund, which was yielding 2.85% at the time. Again, as rates have risen, the yield here should also be higher. At least, given this, we see that putting capital into the Mount Vernon Fund was more beneficial.

At the same time, these positions were a massive part of the portfolio and were yielding less than the cost of the leverage being employed. Remember, at the end of October, they were paying 3.89%. So the positions here at 32.7% of the portfolio were a net drag on the fund.

These are short-term positions, so this capital could have been invested already. At the same time, we know that isn't the case because the semi-annual report for the end of April 30th, 2022, shows another hefty 27.9% invested in these two short-term plays. Ideally, this should be put to work now that leverage costs are rising.

Finally, though, we see some real positions show up after those two positions. TotalEnergies ADR ( TTE ) shows up at a weighting of 5.52%, and then Energy Transfer ( ET ) comes in at a weighting of 4.71%. These are two well-known energy plays, and we can start to see where HIE gets its significant energy exposure with these combining to be over 10% of the fund's assets.

After that, we see Lamar Advertising ( LAMR ), a name that isn't related to the energy space. Instead, it is a specialized REIT that focuses on leasing out billboards. Quite a unique space to be operating in and not something that would come to mind that could be worth investing in. However, it seems to be heading in the right direction. FFO is estimated to continue rising in the coming years. They cut their dividend in 2020, but it has been rising in the right direction since and is now higher than pre-cut.

{kind=link}

Conclusion

HIE is an interesting name trading at a discount. The discount for this fund is more interesting than usual due to the fund's term structure. There is still some time before the termination date; to be more precise, it is a year and 10 months. However, the discount on term funds tends to start narrowing before the termination date.

All this being said, the heavier energy exposure of this fund means it's riskier in general. The energy sector is cyclical, and the anticipation of a recession in 2023 could cause volatility to increase for the fund.

For further details see:

HIE: A Term Fund At A Discount