ADC - High Annualized Upside From Agree Realty At A Low Valuation

2023-08-29 00:01:12 ET

Summary

- Agree Realty is a solid investment with a 5-year total shareholder return of 73.8% and an annualized return on investment of 12.3% since its 1994 IPO.

- ADC has a strong balance sheet with no significant maturities until 2028, and a net debt to recurring EBITDA that has not exceeded 5.0x since 2020.

- Despite modest growth projections, ADC is considered a safe, long-term investment with a well-covered monthly dividend, and a potential upside of at least 10%.

Dear subscribers,

Two of my by far largest REIT positions today are found in two monthly-paying companies. Both are what I would consider "cheap" for what they offer investors. Both of them are investment-grade rated or above (high IG). Both have yields over 4%, which makes them appealing even in the light of CDs and other more risk-free investments.

However, I maintain that both Realty Income ( O ) and the other REIT I have here are very, very solid investments.

The company I am talking about is Agree Realty ( ADC ). In many ways, it can be considered a "smaller brother" to O, but without some of the risk profile, scale, and international diversification that O has. These are obviously both advantages and disadvantages, as it's not uncommon to see for companies like this.

In this article, I'll show you why over 3% of my private and 3.9% of my commercial portfolio is invested in ADC.

Agree Realty - Monthly paychecks are very nice.

Monthly paychecks are something I actively look for. Not because I'm laser-focused on only dividends, but because in my experience, companies that do deliver monthly dividends, but above all are well-managed , tend to outperform the market.

This is true for Agree Realty as well.

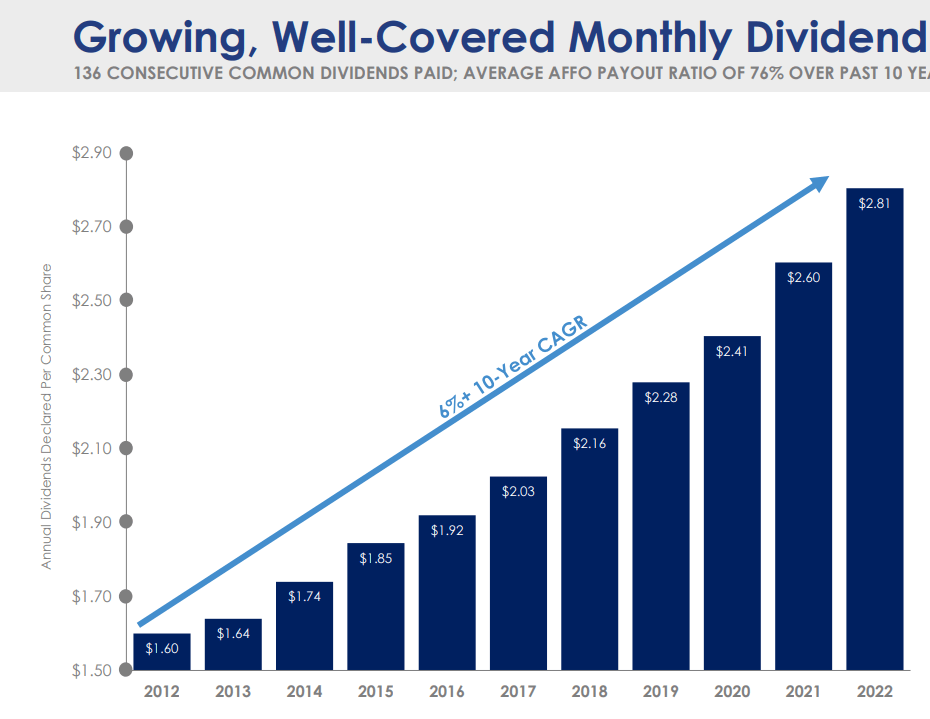

The company has delivered a 5-year TSR of 73.8%. That means you could only have invested in ADC, and you'd have outperformed the market. The annualized RoR since the 1994 IPO is 12.3% - again, a beat. And the company has compounded a 6.1% dividend increase for the past decade or so.

There are a lot of things to like about ADC.

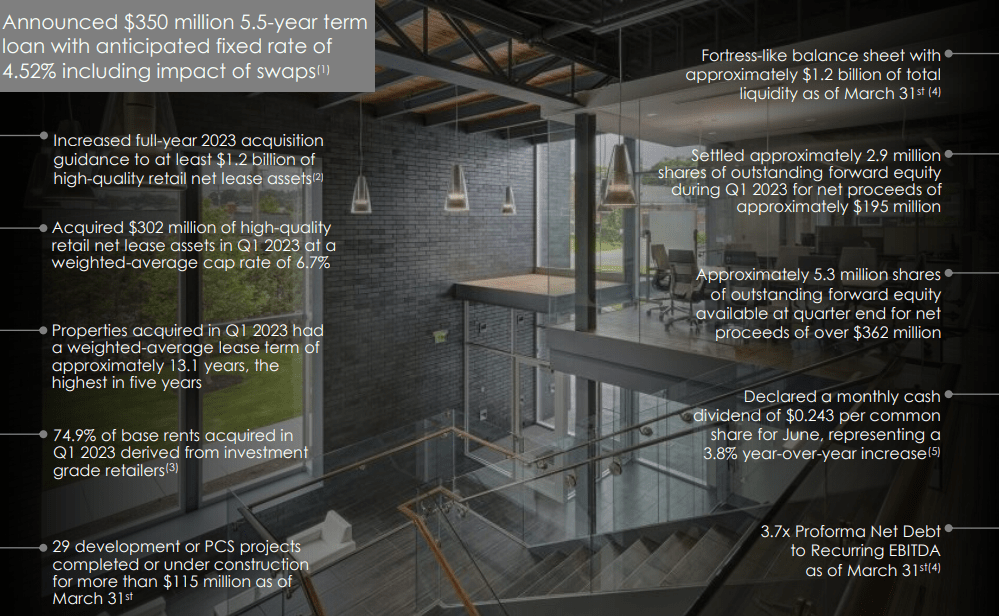

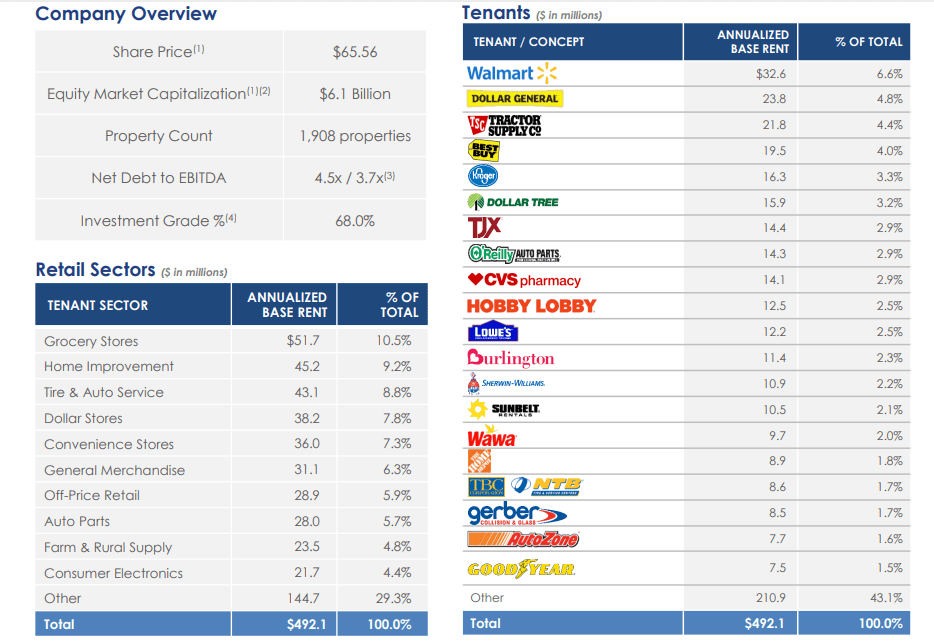

From its BBB rating to its 4.4%+ yield paid out on a monthly basis, to the fact that it has no overexposure or large exposure to any experiential, cyclical industry. The company has "age" - it's been around since the early '70s, owns over 1,900 properties, and its later-year highlights include a whole slew of attractive qualities that showcase that "Yes, Agree Realty is doing very well indeed".

{kind=link}

I want you to note that sub-4x net debt to Recurring EBITDA (even if it's proforma), because that's one of the better ratings in the entire sector - and certainly in triple-net. The company has the sort of operating portfolio of assets that would be the envy of any other REIT. Over 10% groceries, and almost 10% home improvement, with other sectors being either resilient, immune to, or part of the e-commerce trend.

{kind=link}

over 65% of company tenants are investment-grade, with only 16% at sub-investment grade rating. 87% of the company's tenants are what are known as national industry leaders, with less than 2% of the company's portfolio being franchise-based restaurants like Burger King, Taco Bell, or Wendy's. Not saying these are in any way bad - but Lowe's ( LOW ) is obviously better.

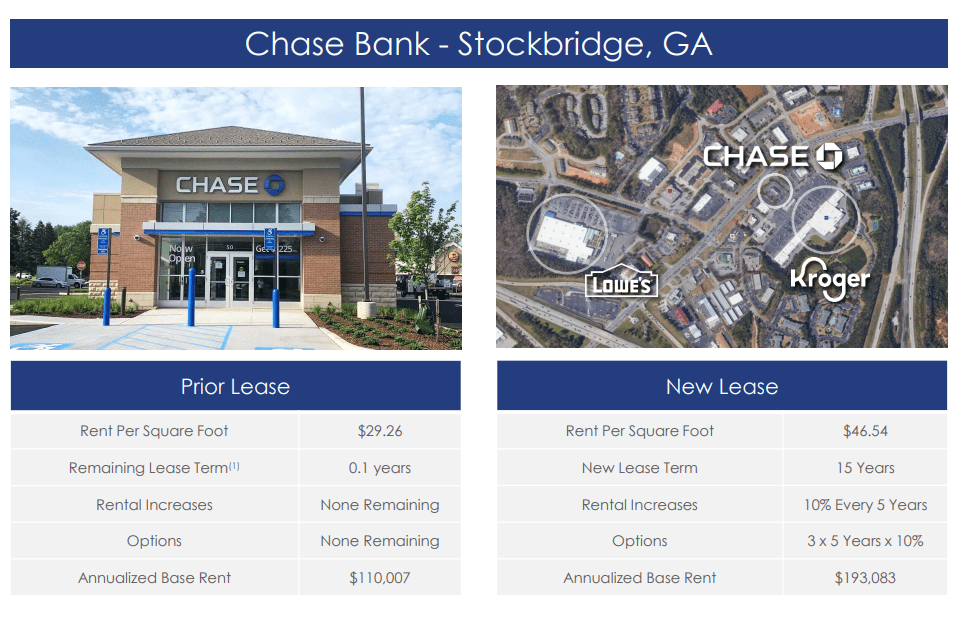

The company also has a growing number of ground leases at 12.1% of ABR, with over 11 years of WALT - most of the ground lease tenants are home improvement, pharmacy similar businesses. I'm happy also to see the very low exposure to pharmacies such as CVS - as I perhaps see these as some of the riskier plays as things currently stand. Ground lease value creation is something attractive to be aware of in these respects, and an example can be found here.

{kind=link}

Different REITs have had different foci on investments for the past few years. What exactly has ADC been focused on, then, that makes it such a good prospect in my eyes?

Well, the company's focus on omnichannel, e-commerce-resistant clients preferably with a recession resistance to the business strategy is what I value here. The company also completely avoids any private equity partners- or sponsorships in terms of retailers, which would muddle the risk/reward ratios. Obviously, ADC wants strong real estate fundamentals and good buildings, but any REIT that at this time focuses on C- or D-class properties has no place even on my survey list.

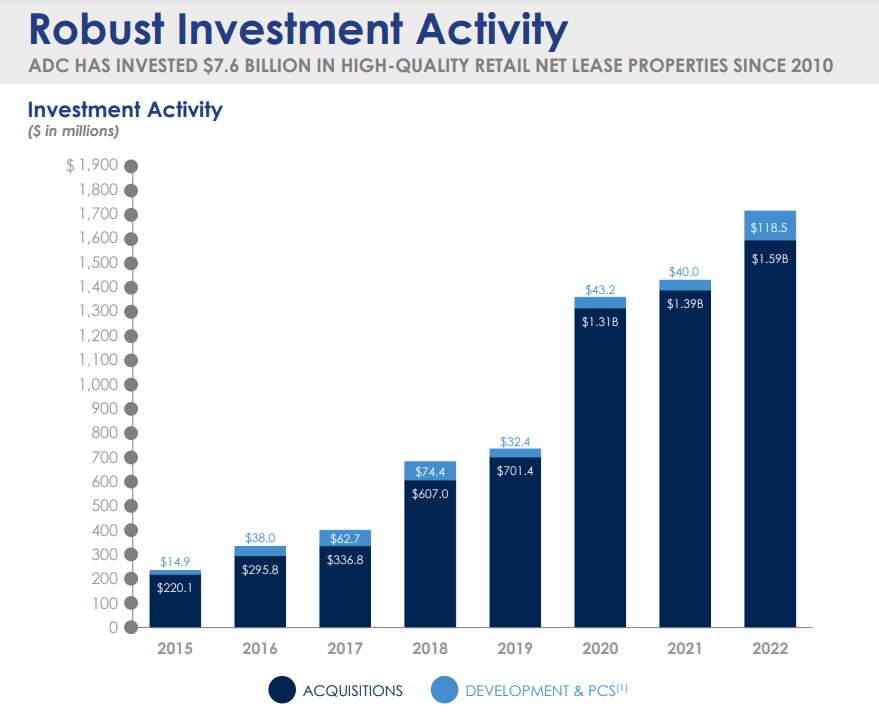

The fact that the company has been able to acquire nearly $6B since only 2018, our of $60B reviewed at a "movement percentage" of 10% means that not only is there still room in this market for high-quality movers/players like ADC, but that they're also very selective. Despite the current chaos in RE, there is a lively and robust investment activity underlying the current market - it's Acquisition-heavy, as opposed to development, but it's significant nonetheless, and it's been increasing all the way to 2022.

{kind=link}

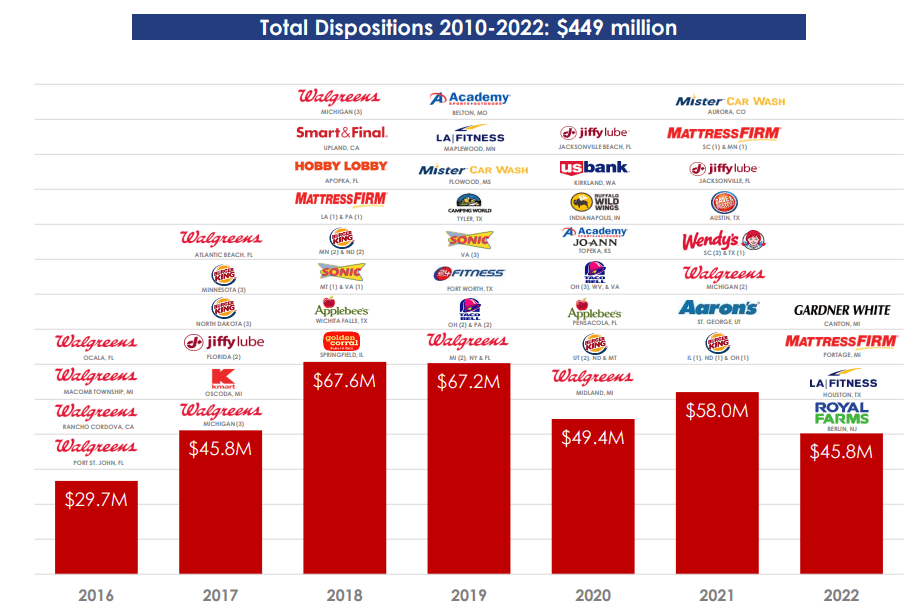

As with any quality REIT, ADC works actively in recycling, divesting and disposing where necessary - and while it's been acquiring, it's also been disposing of almost $500M since 2010 and up to 2022. What I find interesting in their disposals is that ADC seems to have been one of the very early players to target disposals of Walgreens ( WBA ). Even far earlier than before I went negative on the company. I can't help but believe that the company saw what happened to WBA, and acted accordingly - which is very impressive. I also like their continued disposals of franchised locations/brands, as these are less safe compared to, say a Lowe's.

{kind=link}

The company's fundamentals in terms of its balance sheet are absolutely ironclad. No maturities worth mentioning are actually happening until 2028. Okay, so if you include two $50M unsecured ones, there's one in -25 and one in -27, but beyond that, everything is 2028 and beyond. That's one of the best debt ladderings I've seen in REITs and certainly the best in triple-net. The company covers its fixed charges at a rate of 5.1x and has a debt to EV of less than 25%.

Capital markets "love" ADC - this can be seen in its record of being able to provide liquidity for deals, both in the form of unsecured debt and common equity. ADC uses very little preferred equity and almost no secured debt whatsoever.

Its net debt/recurring EBITDA has not once since 2020 and these troubles began, gone above 5.0x - and obviously, that monthly-paid dividend is extremely well-covered with room to grow going forward.

{kind=link}

The picture that I want to leave you with in this article is that ADC is one of the best triple-net lease REITs that there is and that they, like O, have a monthly paid dividend. If you like recurring income, if you like safe income, if you like stability, you should like ADC.

Will investing in ADC make you "rich"?

I would say no, that is not the purpose of ADC.

While over time the company may indeed give you a 100%+ TSR inclusive of dividends, this will likely take a decade or more, and even a 100% TSR isn't really the difference between rags and riches. ADC doesn't turn $10,000 investments into $100,000 easily.

What the company does is safeguard your capital, providing you with a good dividend - a worthy dividend - while also giving you the strong possibility for a good amount of capital appreciation.

As we move into higher interest rates, the company's cost increases, and more lack of opportunities can obviously translate into a much lower-than-historical annual FFO growth rate - and this is where the main risks to these investments lie.

Let me show you.

Agree Realty - Plenty to like, but growth is modest or not there.

Any REIT currently in this space is going to be having some trouble growing. To be clear - when I say modest growth, ADC is still going to be growing its FFO. It's just going to do so at rates of 1-4% instead of 5-8%. You're going to see that dividends continue to rise, that's what I believe, but there are going to be some "jaws" closing where the increases need to be lower because the underlying growth in FFO isn't going to be able to keep up - eventually.

That does not make the company a poor investment - just one with more of an eye towards the long-term and conservative.

While I often present you with companies that may offer 100-300% RoR in 2-5 years, and I do invest 30-50% of my portfolio in such investments, the bulk of my portfolio is invested in companies that continue to churn out or mint cash.

That's how I secure my income - among other things.

And Agree Realty is one of those businesses.

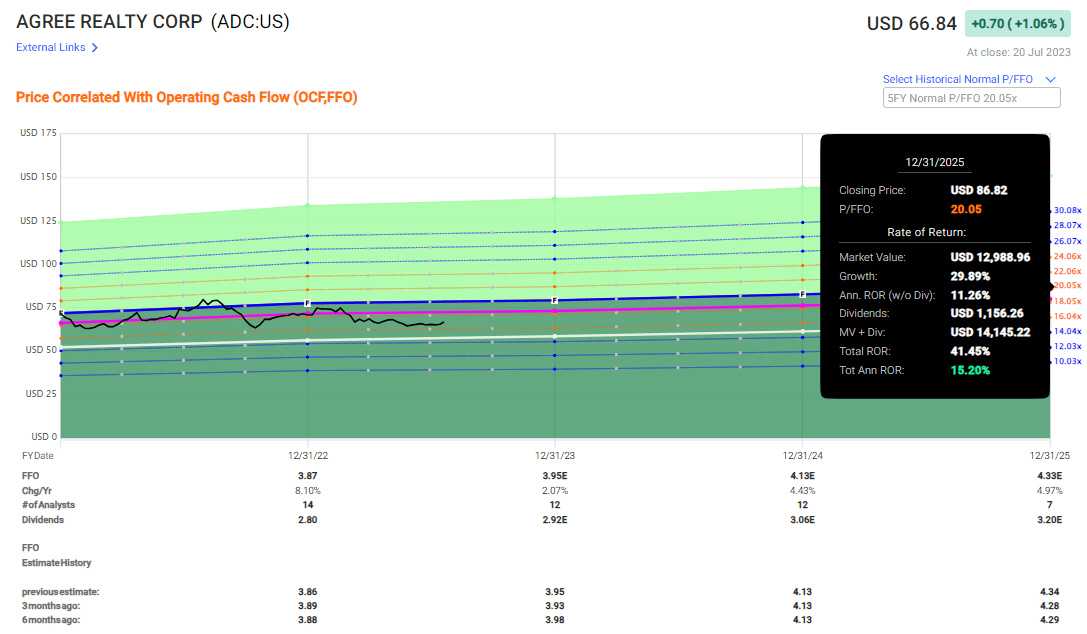

First off, it's my firm stance that ADC deserves a premium. If you don't agree with that stance, you may see a downside here. The quality and the safety of this REITs cash flow means that I consider 18-20x P/FFO to be valid here as I see the company able to pay that dividend through thick and thin - and in this case, the income is one of the primary things I'm looking for.

If 20x P/FFO is valid, then this upside to 2025E is valid.

{kind=link}

And whenever someone tells me that I can invest $1,000 at a 15%+ annual upside while getting monthly paychecks on my money at investment-grade safety while basing this on some of the most recession-resistant operations in the nation, my response is; "Take my money".

It doesn't need to be fancier than this. You could combine ADC and O into two monthly-paying income streams and not buy anything else , and while I say that you might be overexposed, I wouldn't say that these two companies run any sort of risk of fundamental decline. Your income would be safe. I know a colleague of mine who has done exactly this - 29% of his capital is in O, 20% is in ADC, and he's outperforming most of his peers in RoR.

ADC has the sort of crystal forecast clarity that comes with near clairvoyance. Analysts don't miss negatively - ever. Not with a 1 or 2-year basis, not with a 10-20% margin of error, not for the last decade. Not one single negative miss has been recorded on par with this company that's outside a margin of error. There's a very high degree of conviction and clarity here, no matter how the share price moves.

This is a "set-and-forget" sort of stock.

Analysts aside from us give the company a valuation range starting at around $70/share from S&P Global. So you see, 13 analysts are already saying that ADC is trading below the lowest possible PT they would give it.

They go up to $81/share, with an average of $76/share. 12 out of 13 analysts have either a "BUY" or "Outperform" rating here (Source: S&P Global), and these ratings largely mirror the stance we hold here at iREIT on Alpha.

Agree Realty is a "BUY" for me here. And despite my already-outsized exposure, I'm looking to potentially "BUY" more ADC here. It's too good a company not to buy - too good a company not to have in your portfolio, as essentially your own little monthly "cash printer".

Thesis

-

Agree Realty is, next to O, one of the most qualitative investments around in the entire REIT space. While there are many opportunities that do provide a higher, realistic upside, there are very few that offer risk-free-beating dividend yields with the potential for a reversal at such safety. ADC is a monthly dividend payer with a great future - and I keep pushing cash to work here.

-

ADC makes up a substantial amount of my conservative investment portfolio - both the private and the corporate one I run. It's also one of my highest "ratings" out there when it becomes cheap.

-

Agree Realty has a PT of at least $75/share, giving it an upside of at least 10% here, and potentially more.

-

Agree Realty is a "BUY".

Remember, I'm all about :1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

-

This company is overall qualitative.

-

This company is fundamentally safe/conservative & well-run.

-

This company pays a well-covered dividend.

-

This company is currently cheap.

-

This company has a realistic upside based on earnings growth or multiple expansion/reversion.

This company fulfills every single one of my investment criteria barring cheapness - I'm at a "BUY".

For further details see:

High Annualized Upside From Agree Realty At A Low Valuation