WST - High Quality Dividend Growth Near 52-Week Lows: Qualcomm Is Quality

Summary

- A watchlist of the highest quality dividend growth companies is filtered by proximity to 52-week lows.

- 3M Company, Microsoft, and Qualcomm all appear attractively valued based on Historical and Future fair valuations coupled with analyst estimates.

- Qualcomm has an exciting strategy with high growth potential, has an attractive valuation, and could make an excellent investment, especially for long-term dividend growth investors.

Introduction and Background

In preparation for an early retirement in potentially the next 5-10 years, I am in the process of converting part of my 401k holdings, which for many years I have held in mutual funds, into individual dividend growth stocks. These will be partially replacing the US equity portions of my holdings. I will continue to hold mutual funds in bonds and international equity for overall diversification. I will average into this change over a period of time, so that each month or so I will be looking for attractively valued dividend growth stocks to convert to.

As part of my retirement planning, I may use the 72(t) rule to access funds in my 401k penalty-free, early. My employer also allows me to access 401k funds at age 55 penalty free. I feel like the income stream from dividends will be a more predictable source of funding, especially if I need to adhere to the restrictions of the 72(t) substantially equal periodic payments. My overall portfolio weightings from a diversification perspective will not change, but the US equity portion of the portfolio will include substantial dividend paying individual stocks.

I have been managing a dividend growth sub-portfolio for almost a decade. I have refined my process over time, but fundamentally, I maintain a watchlist of the highest quality dividend growth stocks, and regularly update their valuations such that I can have confidence in paying fair value or below, thereby also maximizing my income. It also happens that over the past decade, my actively managed dividend growth portfolio has outperformed the passive mutual funds, while also providing recurring income, which the mutual funds do not.

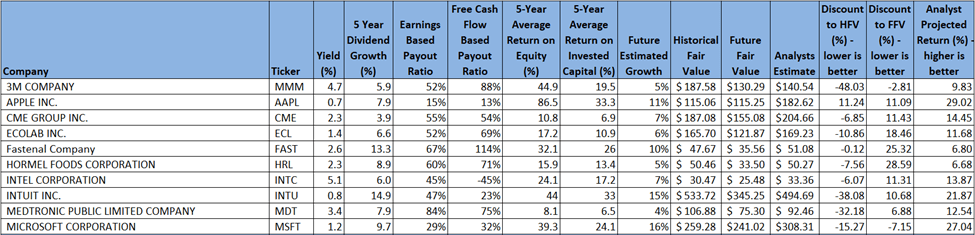

One of my favorite, first-pass screens is to look for those stocks on my watchlist that are trading close to their 52-week lows. For this exercise, I decided to filter my watchlist by companies that have recently reported earnings and that are trading at less than 30% of their 52-week range (52-week low being 0% and 52-week high being 100%).

Using this first pass criteria, we will be looking at the following list of companies:

Finbox, Seeking Alpha, Author's Analysis Finbox, Seeking Alpha, Author's Analysis

{kind=link}

{kind=link}

Fair Value Estimation

As I've described in previous articles, I like to calculate a fair value in two ways, using a Historical fair value estimation, and a Future fair value estimation. The Historical Fair Value is simply based on historical valuations. I compare 5-year average: dividend yield, P/E ratio, Shiller P/E ratio, P/Book, and P/FCF to the current values and calculate a composite value based on the historical averages. This gives an estimate of the value assuming the stock continues to perform as it has historically. I also want to understand how the stock is likely to perform in the future so utilize the Finbox fair value calculated from their modeling, a Cap10 valuation model, FCF Payback Time valuation model, and 10-year earnings rate of return valuation model to determine a composite Future Fair Value estimate.

I also gather a composite target price from multiple analysts including Reuters, Morningstar, Value Line, Finbox, Morgan Stanley, and Argus. I like to see how the current price compares to analyst estimates as another data point, and as somewhat of a sanity check to my own estimates.

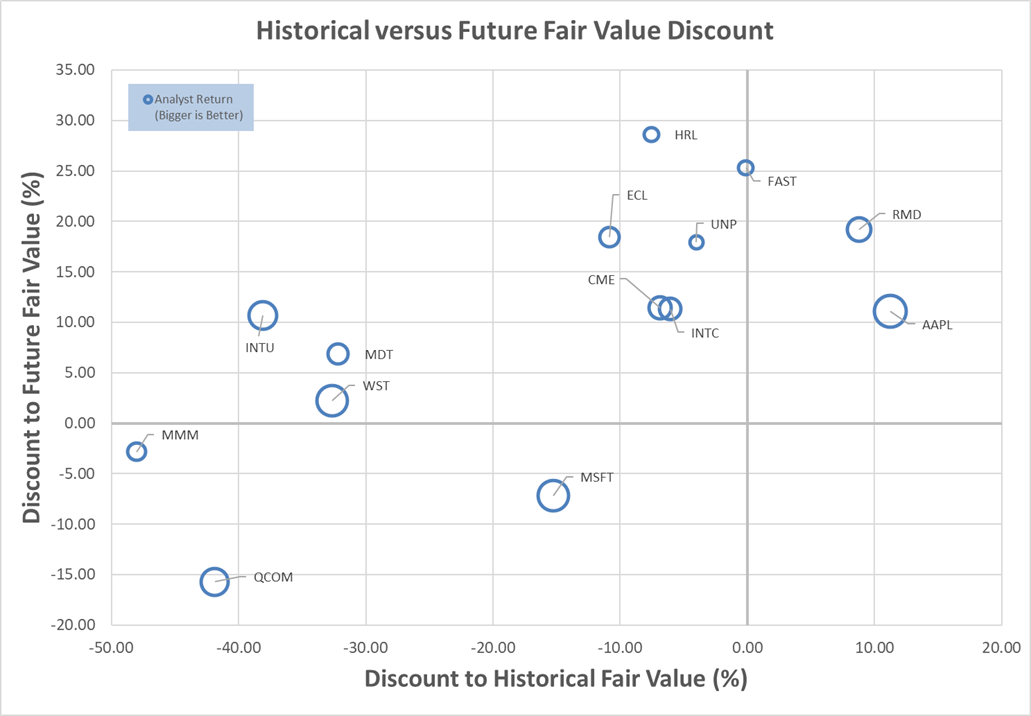

Plotting three variables on one plot is tricky but using a bubble plot allows us to visualize three variables by plotting the Historical fair value versus the Future Fair Value on a standard x-y chart, and then use bubbles to represent the size of discount relative to analyst estimates.

Author calculation of Historical and Future Fair Value, analyst estimates

{kind=link}

This chart is insightful once you understand how to interpret it. What we are looking for are stocks that are trading at a discount to both the Historical Fair Value and the Future Fair Value. So, those stocks that are farther to the left, and farther to the bottom, are potentially the stocks trading at the largest discount to fair value. This would be the bottom left quadrant of the graph. Additionally, those stocks with the biggest bubbles are the stocks that are trading at the largest discount to analyst estimates, so in theory, stocks in the lower left quadrant that also have large bubbles, should be very decent candidates for investment.

Digging into this chart suggests that Qualcomm ( QCOM ), 3M Company ( MMM ), and Microsoft ( MSFT ) are attractively valued from a Historical and Future Fair Value perspective.

I currently own all these stocks and believe that each could be an excellent candidate for further investigation, and potential investment, especially for long-term investors.

In the spirit of full disclosure, I have very recently added to my positions in both Microsoft and Qualcomm. I am really excited to invest in both of these companies, and believe that long-term, they will be exceptional investments, especially considering the present opportunity to buy them at attractive valuations.

My last article was an in-depth look at Microsoft, and I still believe it is very relevant. You can read it here .

In my last article, I suggested I should probably have written about Qualcomm, since, at the time, it also looked to be attractively valued. Well, let's do that this time.

Qualcomm Preliminary Analysis

I like to start simple when analyzing companies. Qualcomm has a 5-year average Return on Equity of 73% and Return on Invested Capital of 25%. The recent figures are even higher at 93% and 43% respectively. These are absolutely excellent values, and do not suggest any kind of degradation. One yellow flag is that RoE is approximately double RoIC, which could mean that the company is using excess debt to juice RoE. However, with both values being so high, this still looks very attractive. We will examine the debt story later in the article. Morningstar's Narrow Moat and Standard capital management ratings are ok. I do wonder if they are giving Qualcomm enough credit for the strong IP that they have in critical components, as opposed to lumping them in with other commodity component suppliers. It is this strong IP that has created some challenges and risks to their business model over time, due to its near monopolistic control over key components. Qualcomm is currently 4-star rated at Morningstar, suggesting it could be undervalued. Now, looking at the dividend, Qualcomm's 26% Earnings-based payout ratio and 50% Free Cash Flow-based payout ratios suggest the dividend is very comfortably covered and sustainable. The 5-year dividend growth rate of close to 6% is slightly lower than I like to see, but the starting yield around 2.6% helps offset the lower growth. With my estimated growth rate for Qualcomm being well above the dividend growth rate, I feel this is a very safe, attractive investment option for the dividend growth investor.

Finally, for our preliminary assessment, let's look at the Seeking Alpha Ratings Summary and Factor Grades.

Seeking Alpha Seeking Alpha

First, from a ratings summary perspective, SA Authors and analysts have strong buy ratings in place for Qualcomm. Looking at the factor grades, Qualcomm's valuation and profitability scores look attractive, and the growth and momentum scores are above average. It scores poorly on the number of recent revisions, which have all been downward. This suggests to me that we may be fighting momentum and short-term challenges, but long-term, I believe this is still a strong candidate for long-term investment.

Qualcomm Strategy

A key part of long-term investing is ensuring that a company's strategy is solid over the long term, and that the company is executing well against that strategy. Qualcomm has some excellent material to help us quickly understand the strategy and progress. The most recent earnings report here , and the recent automotive investor day presentations here , here , and here , are some excellent resources. Let's hit some highlights.

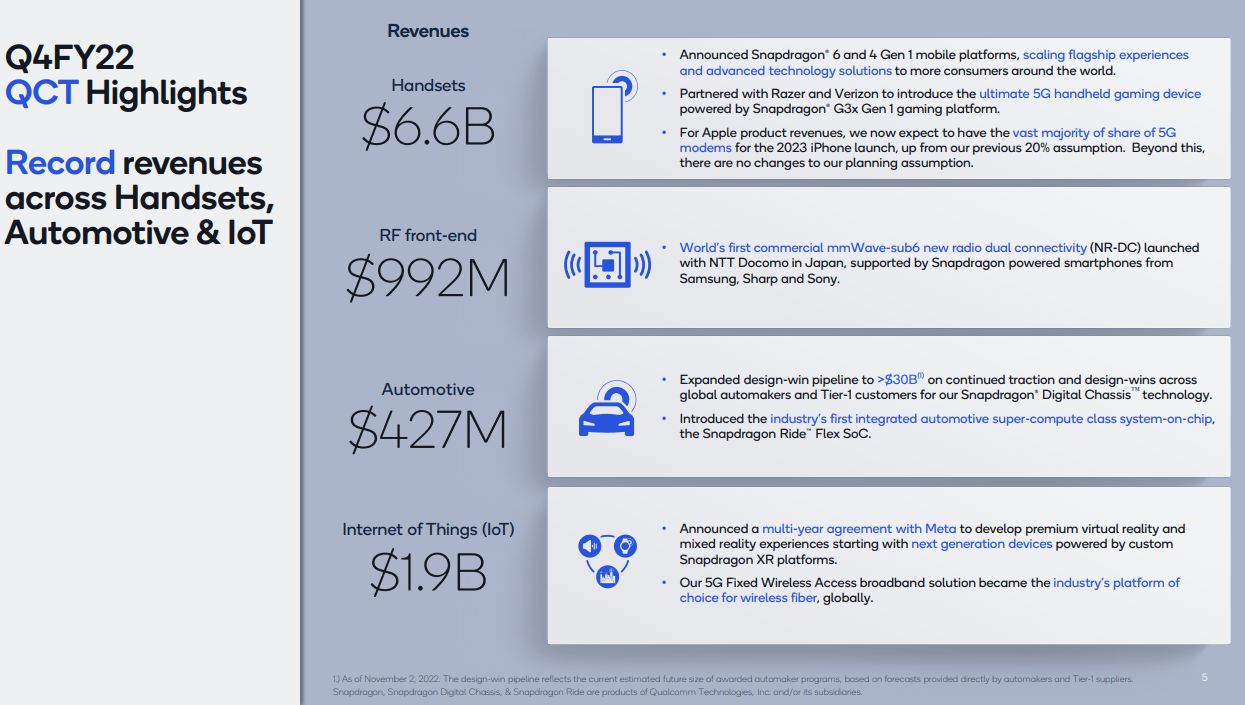

{kind=link}

The split out of revenue for Full Year 2022 shows how important the handset business is to Qualcomm. Handset processors and modems are two very important components in this business, and both have come under attack in past years. At this point though, Qualcomm's superior technology has been able to overcome some of the desire to change to alternative supply. A big result was the recent win of the majority of the 5g modem business for the new Apple (AAPL) iPhone lineup, which was somewhat of a surprise based on Apple's very public desire to move to alternate suppliers.

{kind=link}

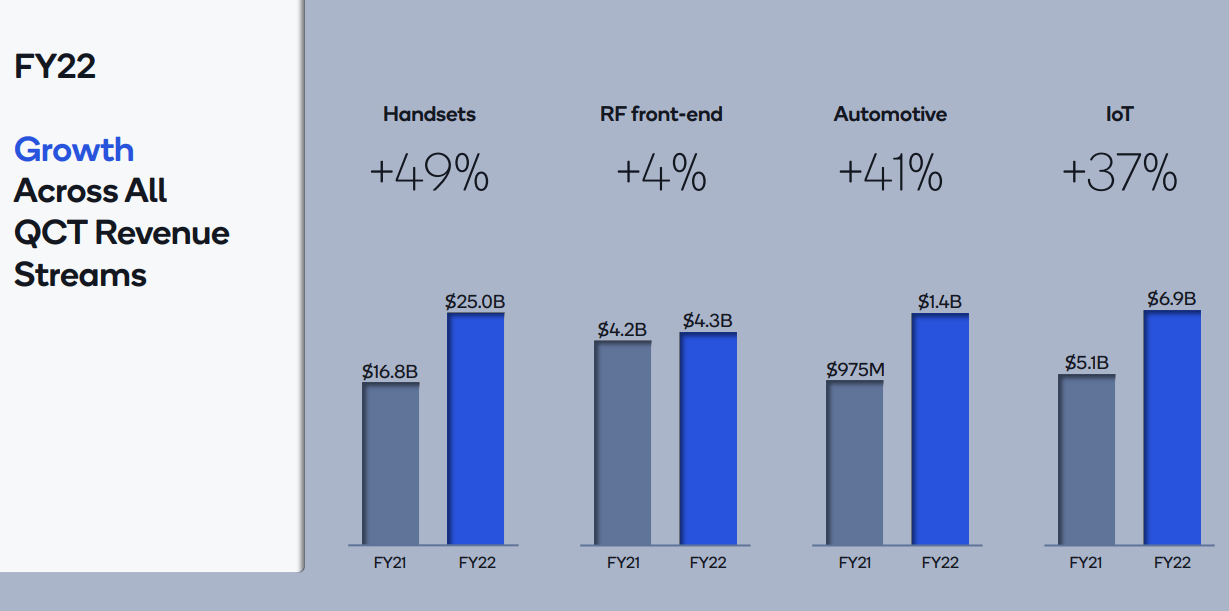

One of the exciting aspects of Qualcomm is that it looks like several of their business segments continue to experience strong growth. The fact that the handset revenue stream grew as much as it did, when it is a relatively mature market, is exciting. The Internet of Things revenue stream growth is also exciting, and there are many fascinating product opportunities that should help in the future. Starting in 2023, Qualcomm is planning to consolidate RF front-end into the other segments.

The three remaining segments will have a rather amazing Total Addressable Market in the next decade.

Qualcomm Automotive Investor Day 2022

{kind=link}

For me, one of the opportunities that appears the most exciting is Automotive. In 2022, it was the smallest segment, and yet when we look at future growth potential, it is amazing.

{kind=link}

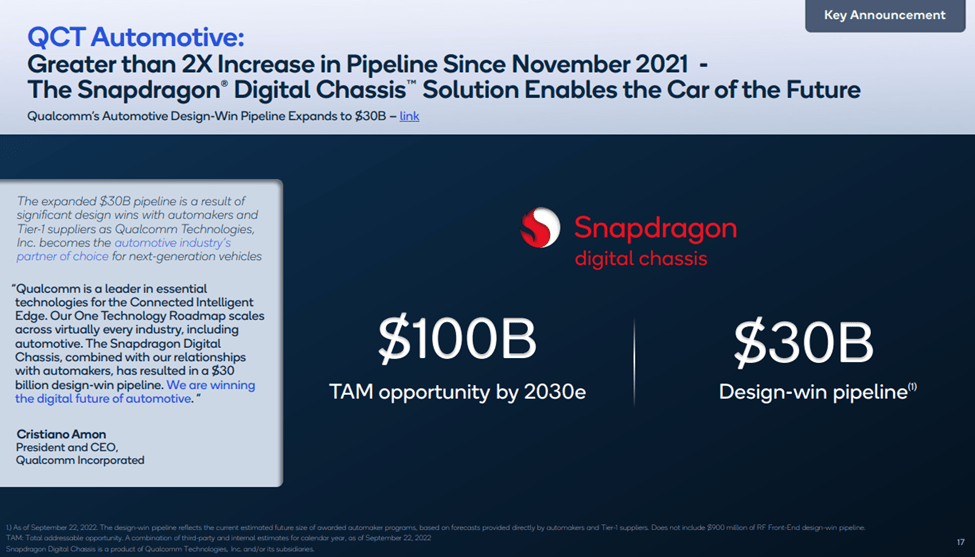

Considering that Automotive is currently $427M for Qualcomm, and they are projecting that the Total Addressable Market by 2030 is $100B, but more importantly, have an actual pipeline that they believe could allow them to win $30B of that seems too good to be true.

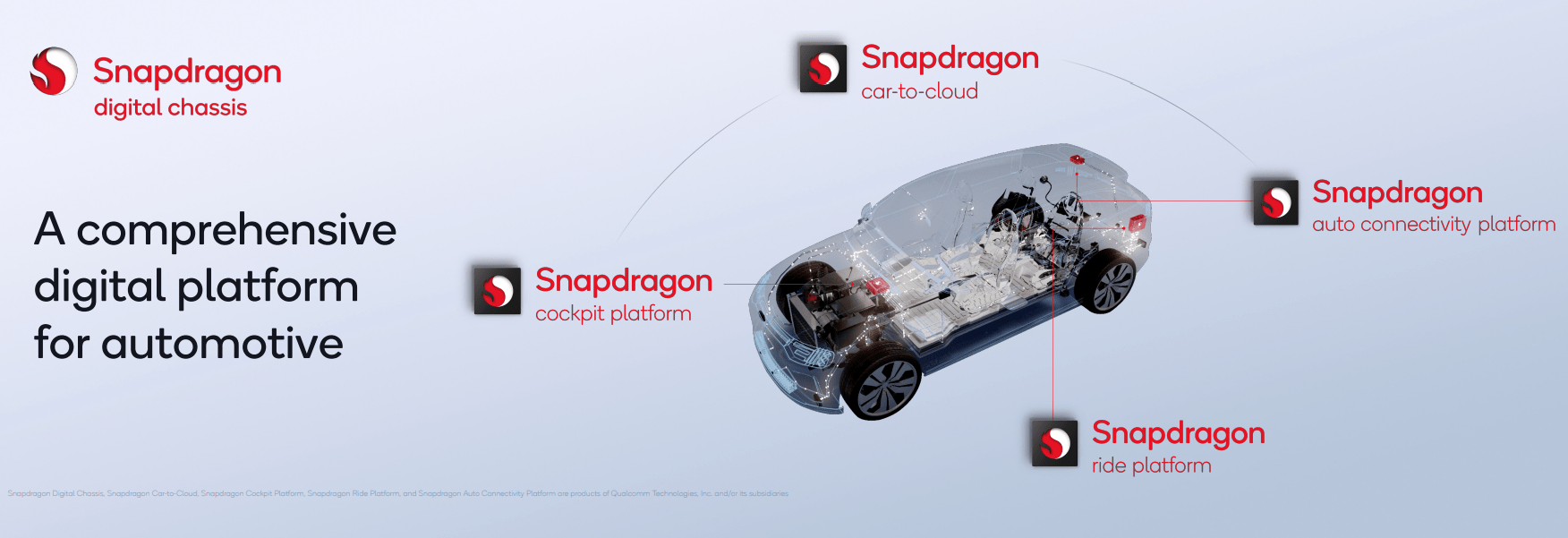

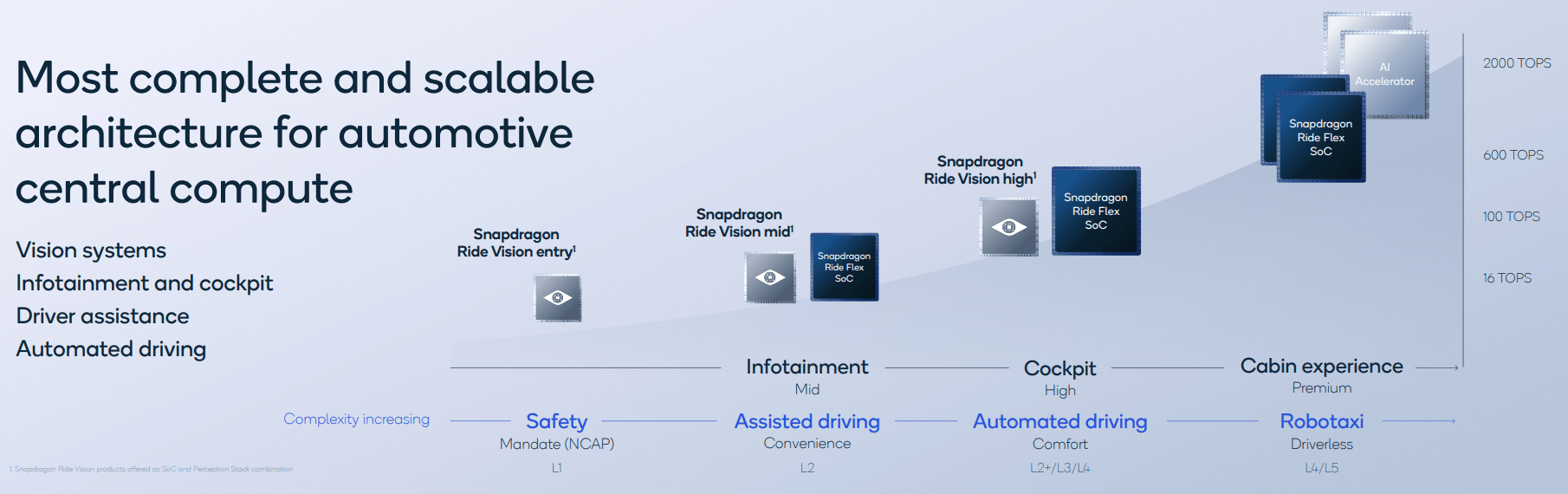

They are taking a very comprehensive approach though, providing full platform solutions with their Snapdragon architecture.

Qualcomm Automotive Investor Day 2022

{kind=link}

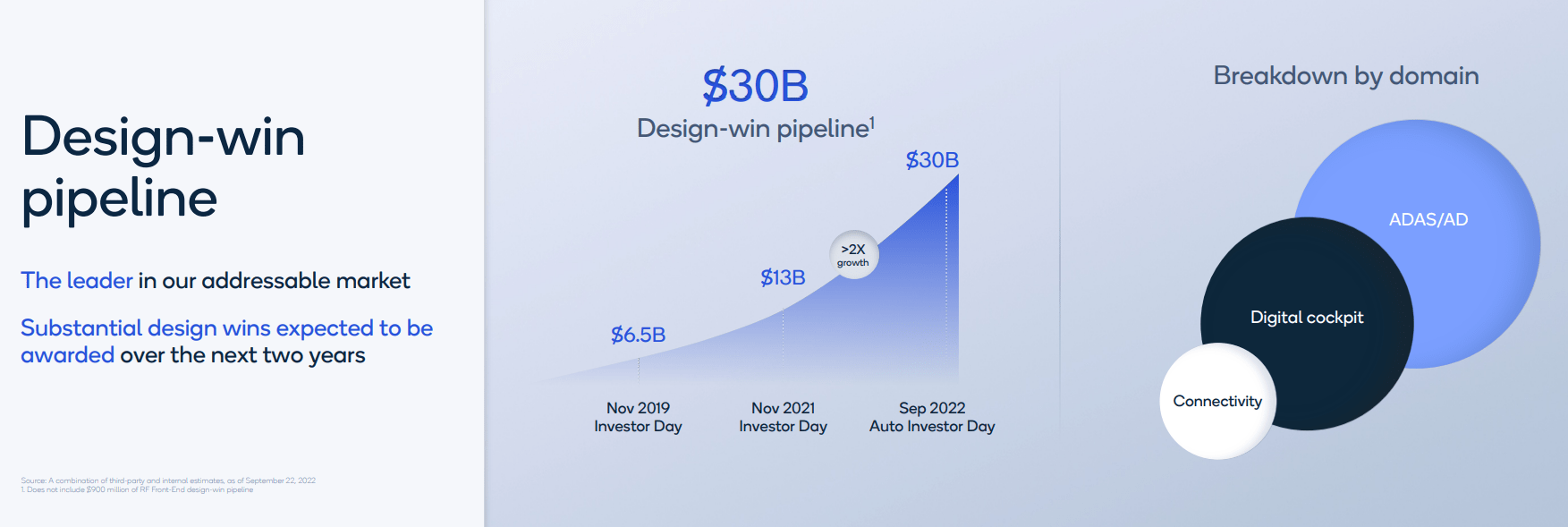

The amount of the Total Addressable Market that they think they will be able to address also continues to increase, and they have a leadership position. The growth in the Design-win pipeline shows the exciting potential, and the alignment of the Qualcomm strategy to the market direction.

Qualcomm Automotive Investor Day 2022

{kind=link}

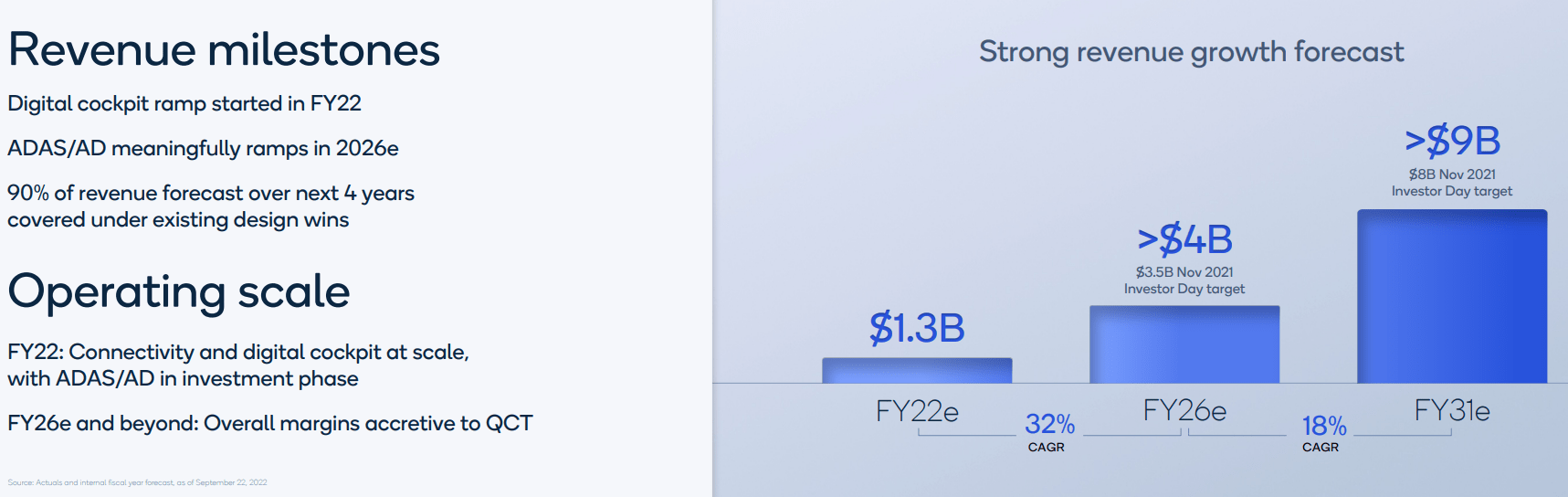

The projected revenue growth associated with this growth in opportunity and pipeline wins looks potentially conservative, but still very attractive.

Qualcomm Automotive Investor Day 2022

{kind=link}

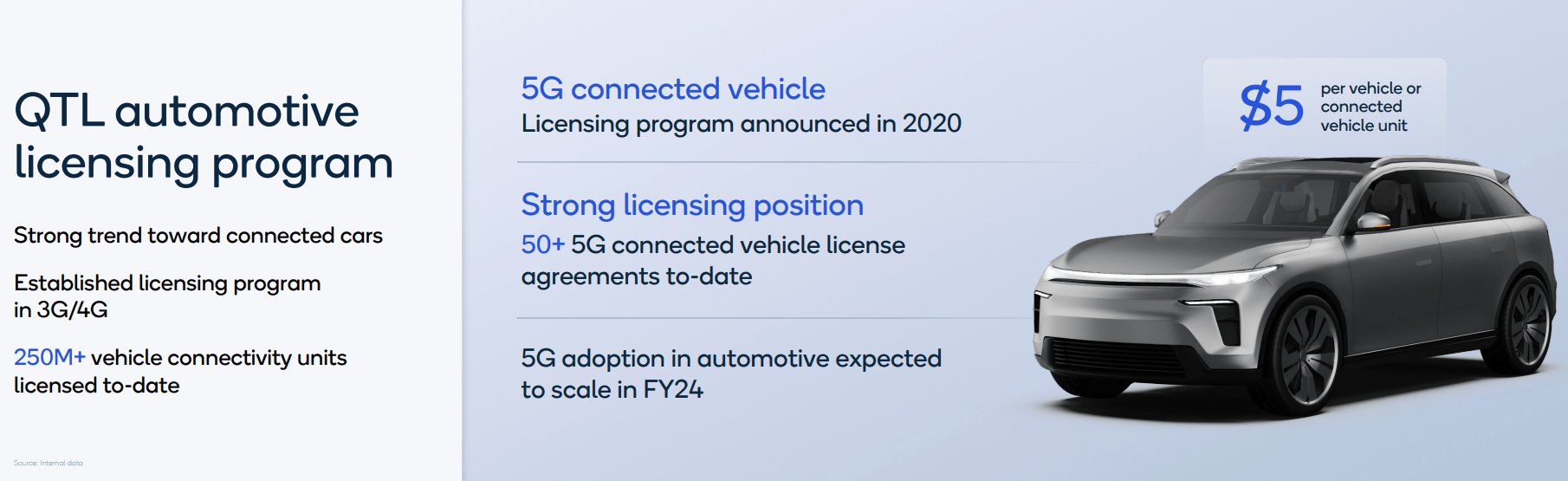

Another aspect of the automotive strategy that is exciting is the licensing opportunity. Even if Qualcomm doesn't win all of the architecture supply opportunity, because of their strong IP position, they will likely still have licensing revenue from the majority of connected assets. Today that is worth around $5 per connected vehicle.

Qualcomm Automotive Investor Day 2022

{kind=link}

Additionally, I like to see that the Qualcomm architecture is somewhat future proof. There are a lot of obstacles to overcome to get to fully autonomous vehicles, however, I believe that semi-autonomous features, especially as they improve safety, are a given. Qualcomm's architecture and technology support all these scenarios.

Qualcomm Automotive Investor Day 2022

{kind=link}

After this brief dive into the Qualcomm strategy, I remain very excited about future prospects. Qualcomm is a leader in their areas of technology, with strong IP protection and licensing to capitalize. They also have multiple value-streams investing for the future, and most indications are that they are positioned to remain a leader. Furthermore, the Total Addressable Markets for the markets that they aim to serve appear to have significant growth potential well into the future. I am excited about Qualcomm's strategy and the progress they are making with that strategy. I want to own a piece of that.

Qualcomm Historical Valuation Analysis

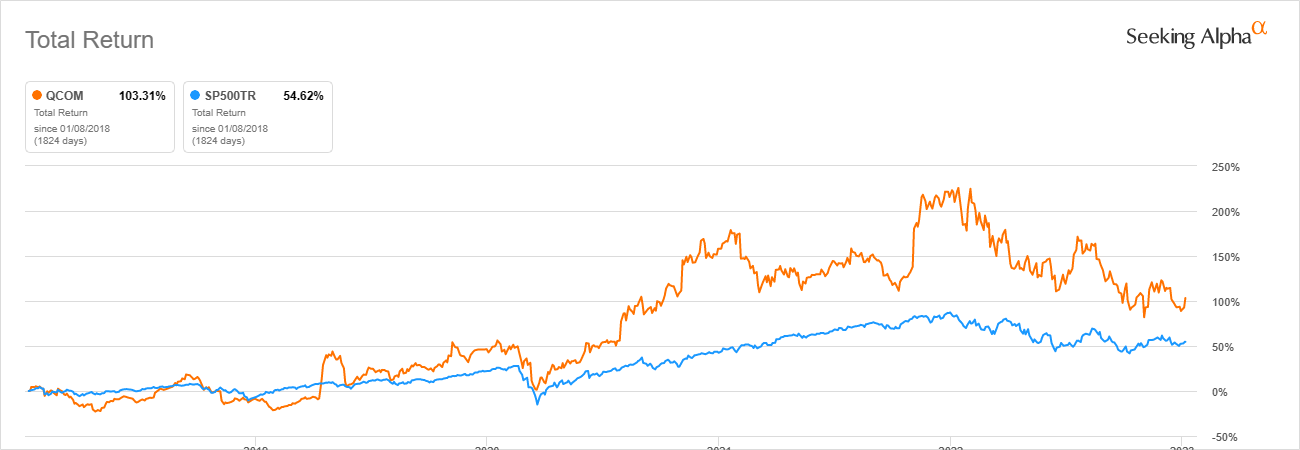

Since I am replacing a diversified, broad market US Equity mutual fund partially with Qualcomm, let's start by seeing how that return compares over time to the S&P 500, not that history is a guarantee of future results, but it is still something I like to consider.

{kind=link}

We can see over the past 5 years that Qualcomm has significantly outperformed the S&P 500. Some of the challenges and lawsuits of the past that challenged Qualcomm's performance seem to be behind them, and the recent performance has been very strong. Considering the potential valuation currently, there is a good possibility that outperformance can continue.

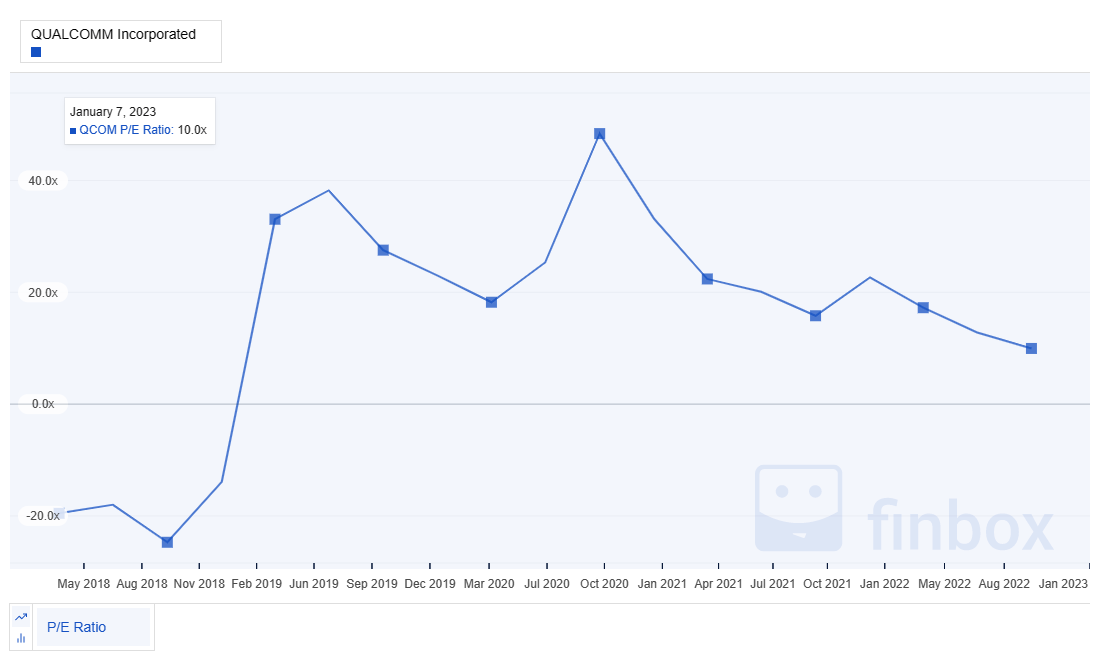

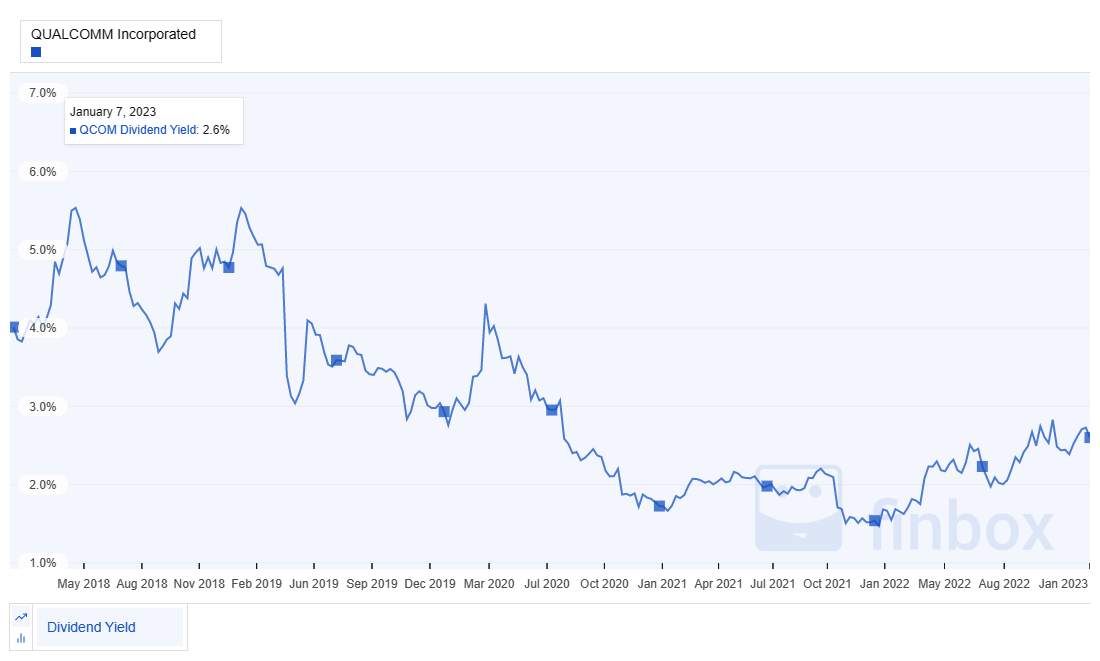

Outperformance in the past is one thing, but maybe that outperformance was just due to valuation multiples. That's why valuation is important. To know if we should consider investment, we want to be sure we are buying fundamentals, not just exuberance. Two of my favorite initial indicators of valuation are P/E and yield.

{kind=link}

{kind=link}

Ignoring the earlier years when Qualcomm was facing some litigation issues, Qualcomm's P/E ratio of 10 looks pretty attractive by itself, especially for a growing company, but also looks attractive historically when compared to its 5 year average of around 16.5. Yield is also a nice indicator for dividend paying stocks. The current yield around 2.6% is still below the 5-year average of 3.1% but is trending higher. We also likely need to ignore some of the earlier years when the licensing business model was really being brought into question, and there was significant customer satisfaction, leading to higher investment risk assessment.

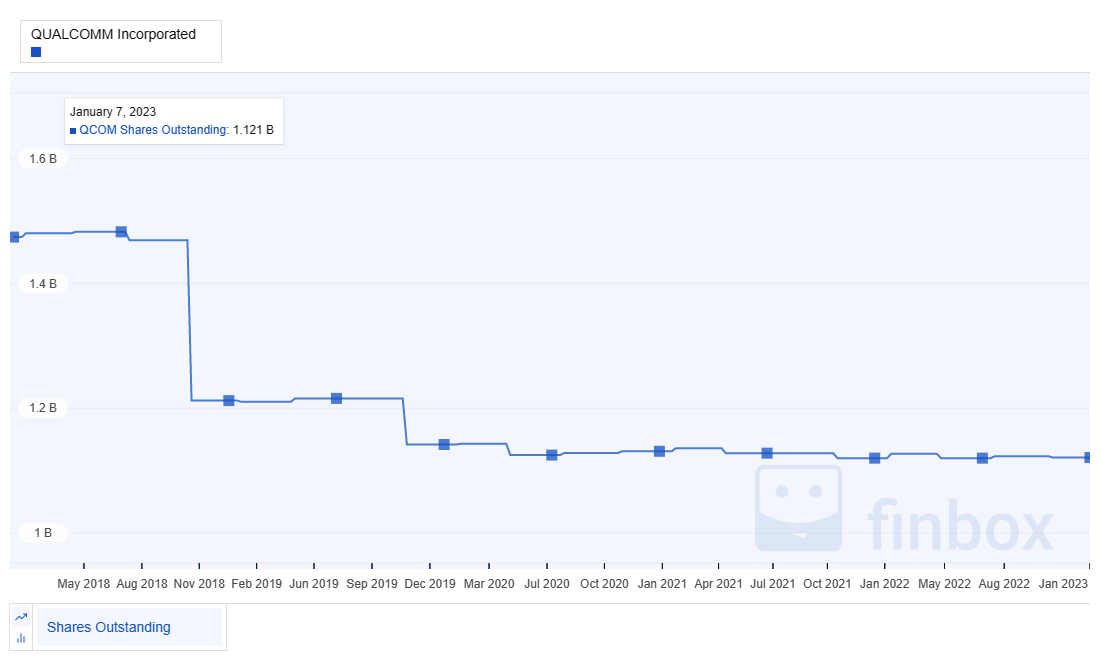

A key part of the Total Shareholder Return includes stock buybacks, which are also important to dividend growth sustainability. Qualcomm has slowed down on share repurchases as of late, but they are still slightly more than offsetting equity based compensation, thereby avoiding shareholder dilution. This isn't overly positive but is also not a big negative.

{kind=link}

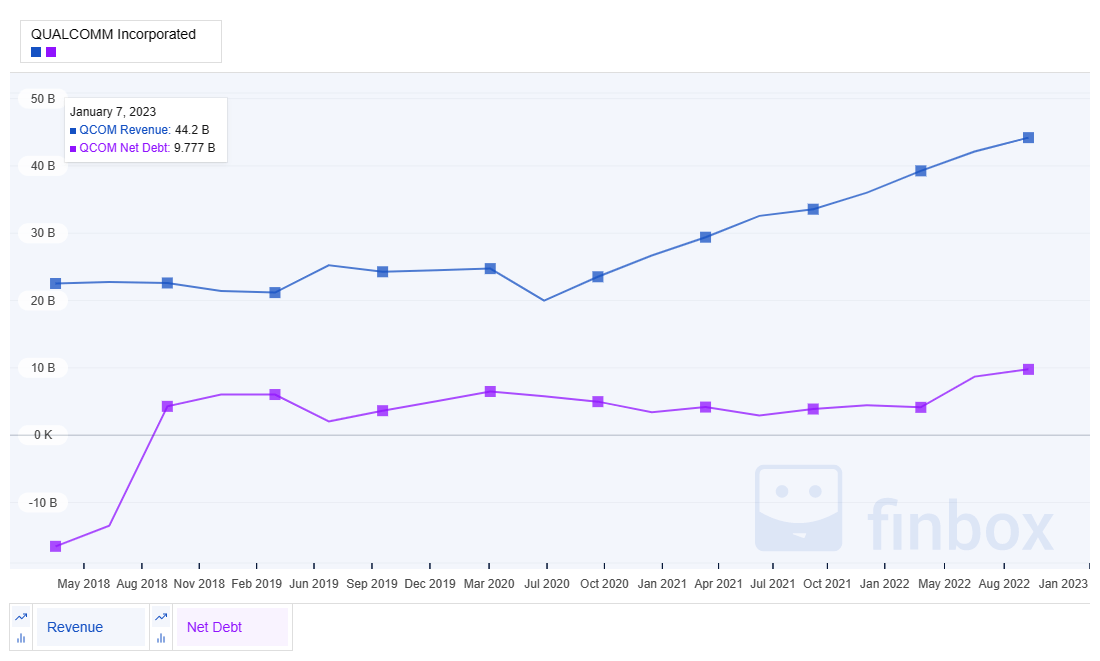

We pointed out earlier from the RoE and RoIC that Qualcomm may be using debt to increase Return on Equity. Looking at their revenue versus net debt shows that Qualcomm has been increasing debt slowly over time, however, it appears revenue has increased more quickly than debt. With an A S&P credit rating, they are still a very financially strong company.

{kind=link}

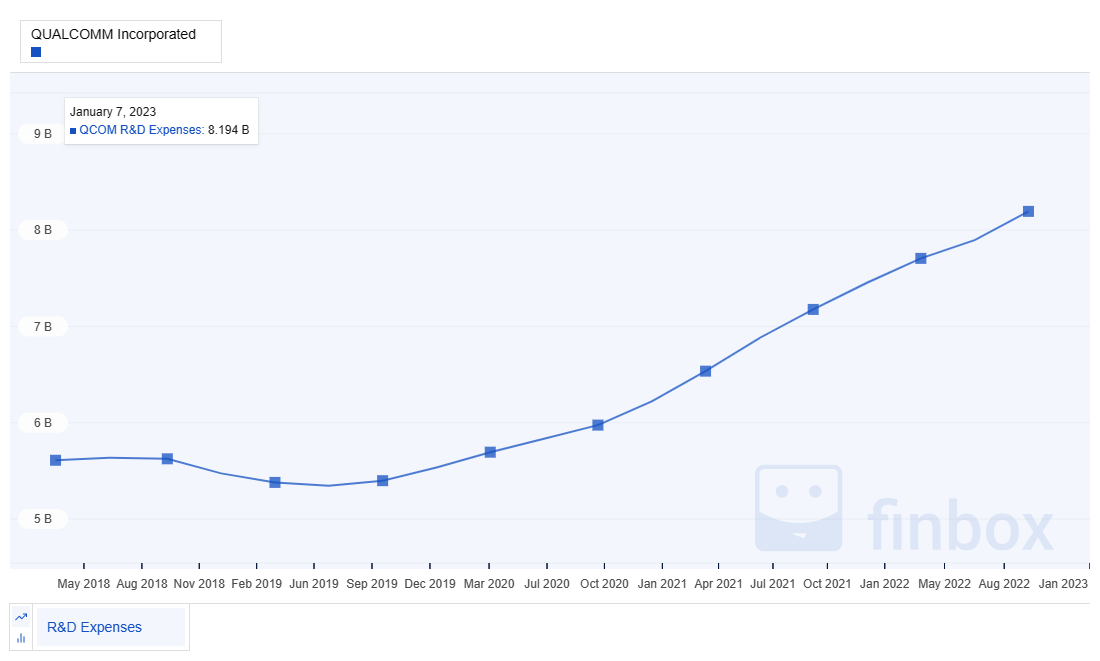

In order to take advantage of the strong growth opportunities for their product lines, Qualcomm has had to increase investments significantly. As long as the revenue growth continues to compound at the rates that it has, this is likely to be a very good investment, long term, but this is something that will need to be watched. If returns start to decline, it could be indicative that the markets they are investing in are becoming more competitive, leading to lower margins and opportunity.

{kind=link}

Qualcomm has been paying a growing dividend for almost 20 years. Their growth has been solid and sustainable. The 7.5% recent dividend growth is just above the average 5-year dividend growth of around 5.5%.

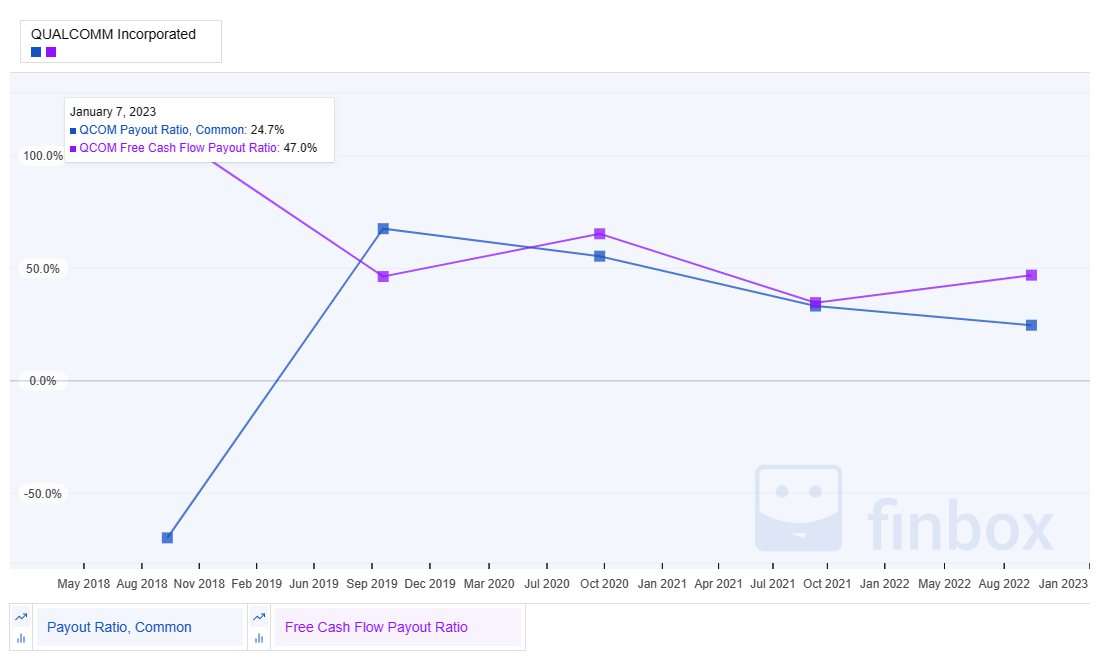

Obviously, dividend growth doesn't do any good if the growth is not sustainable. In this case, Qualcomm's earnings and free cash flow-based payout ratios have remained consistent. This is another indication that the long-term dividend payout and growth should be sustainable. With payout ratios of 25% based on earnings, and 50% based on free cash flow, there is a lot of margin to protect the dividend.

{kind=link}

Based on these various indicators of valuation based on historical perspective, Qualcomm appears to be fairly, if not under-valued, especially considering the potential future growth opportunities.

Qualcomm Future Valuation Analysis

Because we want our dividends to grow in the future, not just the past, we need confidence that the results the company has already achieved will likely continue.

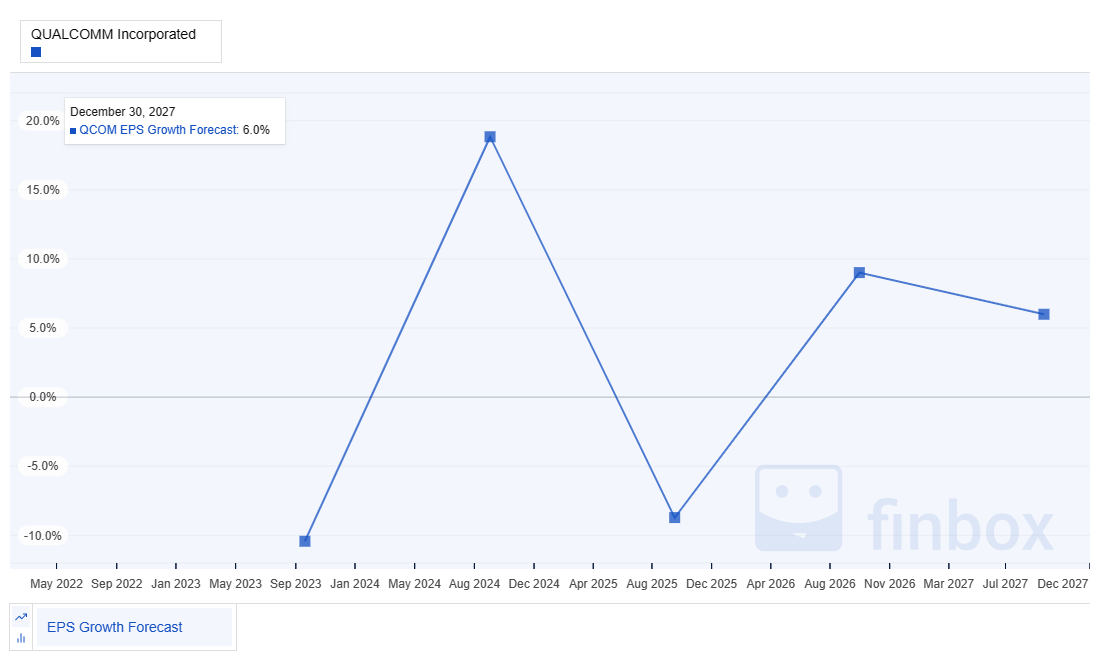

Looking at future Earnings Per Share projections, we can start to see why maybe Qualcomm appears to be undervalued currently. The projections suggest a bumpy ride in the next few years. Now, long term, bumpy investments can still be good investments, if the core business doesn't degrade during the process, but in the short term, it can take the investor for a roller-coaster ride. I do like to look at it another way though, if those bumps result in decreases in stock price, but the fundamental business is still sound and ultimately growing, it can create some great opportunities to buy and compound dividend growth through re-investment.

{kind=link}

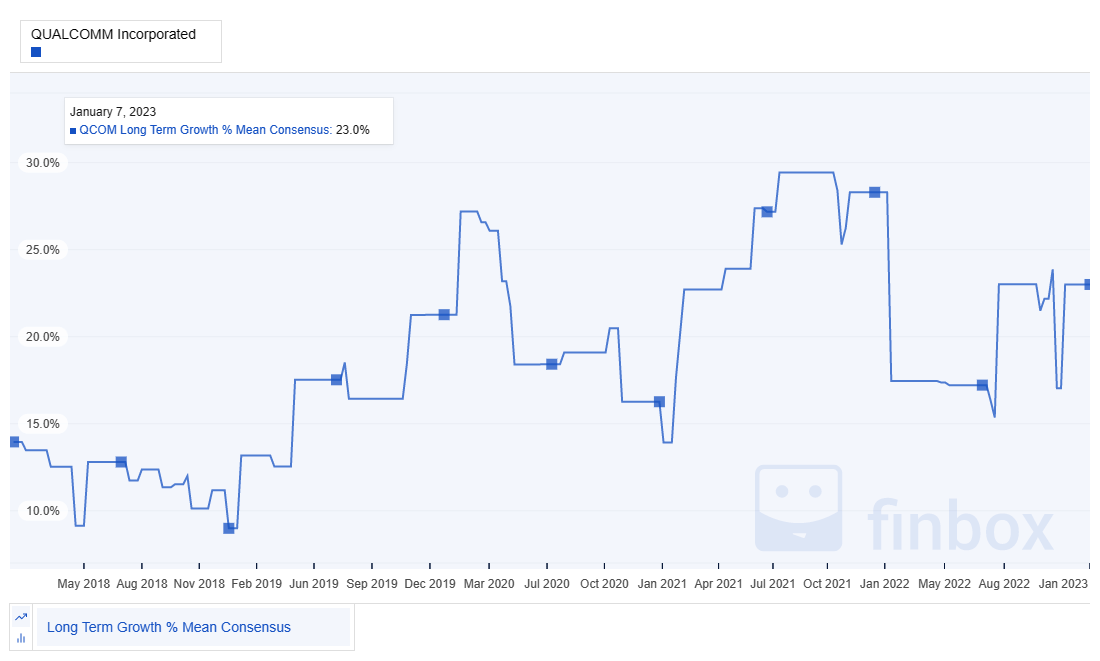

Growth is one of the hardest things to predict in investing, otherwise, investing would be much simpler. As we discussed, future growth projects some turbulence. In the case of growth, I do like to look at historical growth estimates. In the case of Qualcomm, generally growth projections have been well above 10%.

{kind=link}

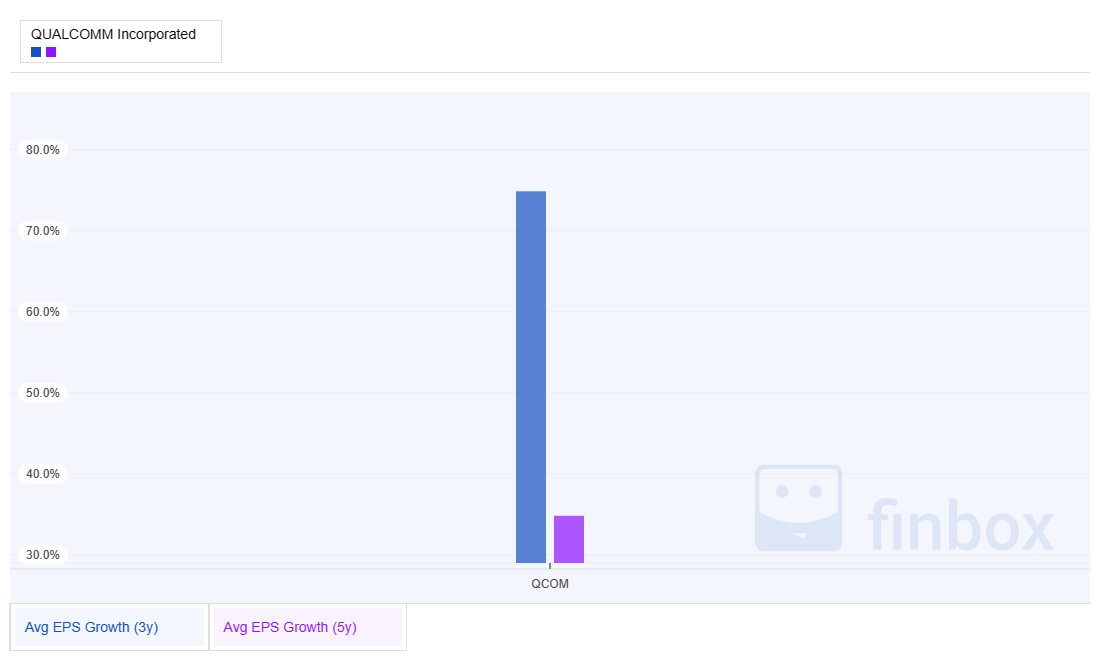

My own estimate for Qualcomm's forward growth is around 16%. I derive this from a combination of various growth projections and growth models. Based on the results of the strategy study, I don't feel like this is completely unrealistic, though it could be optimistic shorter-term. Qualcomm's recent EPS growth has been well above this number.

{kind=link}

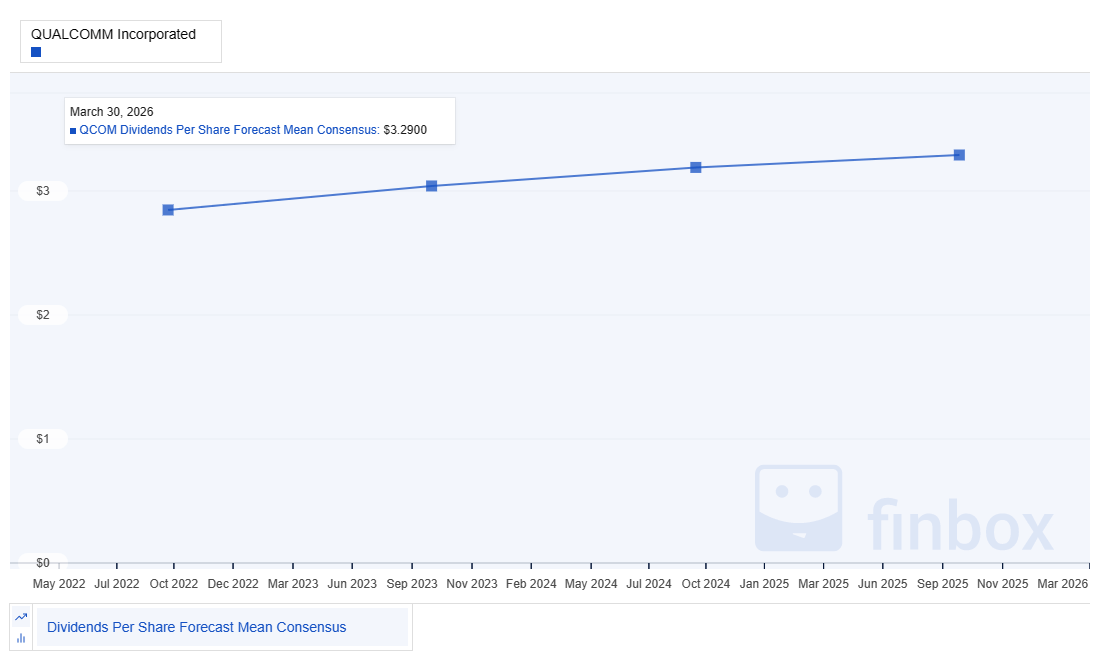

For a dividend growth investor, understanding future dividend growth potential is also important, especially in as much as it is sustainable. Here are the long-term dividend growth projections for Qualcomm. The forecast growth looks very consistent. At least for the next few years, it seems likely that Qualcomm will continue solid, if not especially high, dividend growth.

{kind=link}

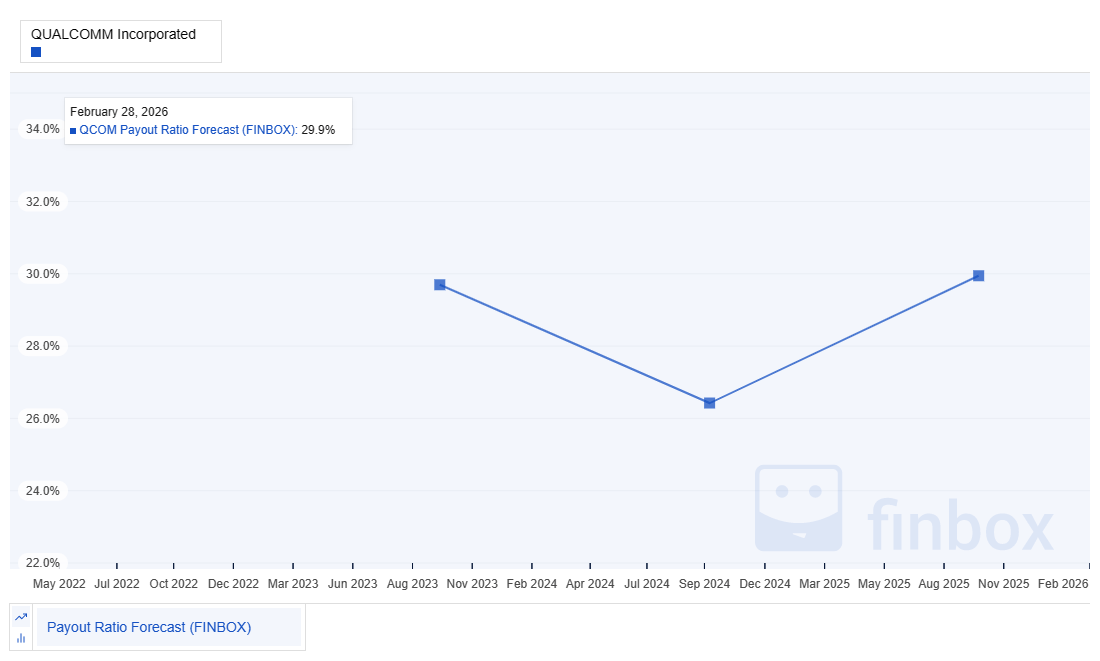

Based on this forecast, and what we've seen already as far as earnings growth and projected dividends, it shouldn't come as a surprise that the earnings payout ratio is also forecast to be well controlled for the near future. The low levels of the payout ratio forecast suggest there will be room for incremental investment back into the business, increased dividend payouts beyond the forecasts, or incremental share buy-backs. All of these are positive for the investor looking for sustained dividend growth.

{kind=link}

As already covered, the growth in expected revenue for the next several years is one of the questions that is likely leading to the lower current valuation. However, it should provide for financial stability and dividend security.

{kind=link}

Qualcomm Risk

Let's be honest, you can do a lot worse than Qualcomm from a risk perspective. The S&P credit rating of A, Moody's credit rating of A2, and A+ Value Line Financial Strength rating all attest to the quality of this company.

That aside, there are a few risks to discuss. Qualcomm still relies heavily on the licensing of its IP for a lot of its revenue. These licensing arrangements in the past have led to lawsuits by customers and competitors for unfair business practices and have also made them a target for IP infringement lawsuits, as well as disruption to their technologies. At this point, it appears that Qualcomm has been able to maintain a sufficient competitive advantage to overcome some of this dissatisfaction and has also taken extra measures to improve relationships with key customers. The high technology markets that they play in provide some barrier to entry, but the high margins and market growth potential also invite more competition and disruption.

For the dividend growth investor, Qualcomm appears very safe. Based on Seeking Alpha's dividend grades, it doesn't get much better.

Seeking Alpha

I also like to look at short-term risk indicators for any new investments, with Short Interest being one key indicator for me that I might be missing something that others might know.

Seeking Alpha

Based on the very low short interest currently in Qualcomm, this would not make me hesitate to initiate or add to my position in this quality company.

Summary

As I stated at the beginning of the article, I recently put my money where my mouth is and added to my position in Qualcomm. I have held Qualcomm since 2015. It has not always been the most stable investment for me, and has even downright scared me a few times, but overall, it has been a very good total return and dividend growth investment for me. I am especially excited about the growth in the Total Addressable Market for the products that they are developing, the evidence of strong competitive advantage I see in many of their recent business wins, with some customers even coming back to them after swearing them off, and I believe Qualcomm is very well positioned moving into the future, especially with growth in the Internet of Things and Automotive segments.

As part of the analysis, 3M and Microsoft were also identified as being attractively valued from a Historical and Future Fair Value perspective. Many of us are likely aware of the ear protection and PFAS risks that are currently unsettling 3M. I have a large position in 3M and plan to hold but will likely not add at this time. On the other hand, I am very bullish on Microsoft, and frankly can't believe it is still on sale, allowing me to recently add even more. Please read my recent article, which is still very relevant, to see my thoughts, here .

For further details see:

High Quality Dividend Growth Near 52-Week Lows: Qualcomm Is Quality