OGN - High Risk High Reward: Why 8.5%-Yielding Organon Could Be Up To 90% Undervalued

2023-12-19 10:22:30 ET

Summary

- Organon's stock has declined 32% since September, making it one of the worst performers in healthcare.

- The company reported mixed financial results, with 1% growth in product sales and a decline in total revenue.

- Organon's biggest challenge is debt reduction, but its strategic focus on cost efficiency and debt reduction could lead to significant returns.

Introduction

It's time to talk about a company I started to cover this year. On September 10, I wrote an article titled 6% Yield And Significantly Undervalued: A Closer Look At Organon .

In that article, I covered the valuation and growth opportunities of the company, which spun off from Merck & Co., Inc. ( MRK ) in 2021.

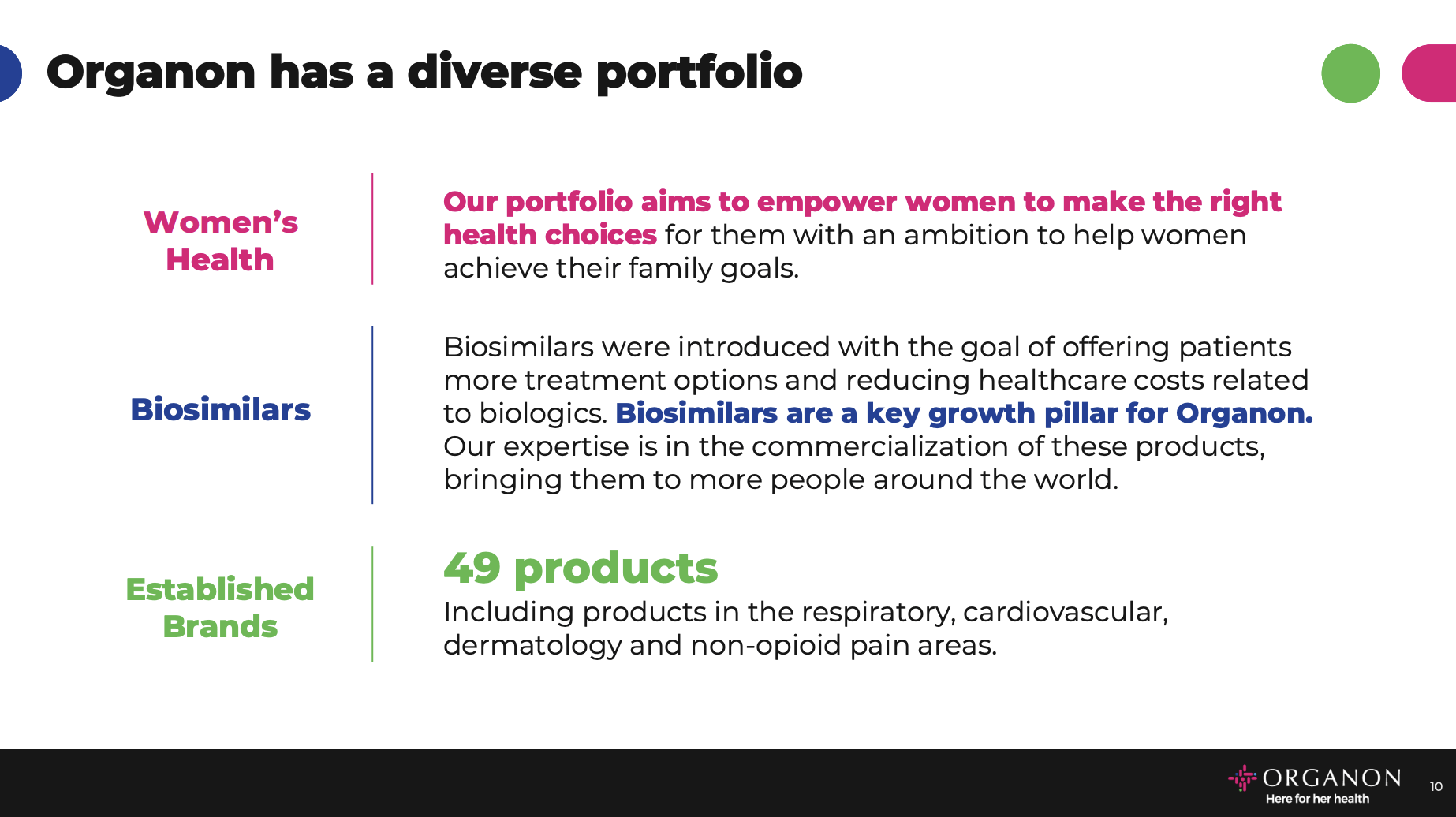

The company, which operates three major segments covering Women's Health, Biosimilars, and Established Brands, has elevated debt levels and a juicy dividend, which investors don't seem to care for until the debt load has been lowered.

{kind=link}

Although Organon & Co. ( OGN ) appeared cheap in September, the stock is down 32% since then, making it one of the worst performers in healthcare.

In this article, I'll elaborate on a few key issues, including the fact that the company remains in a great spot to boost its free cash flow to reduce debt. If it is successful in doing that while growing core products, it will not only be able to protect its dividend, but also grow its dividend down the road, making OGN a highly attractive income play.

Hence, I stick to my bullish view and rate OGN a high-risk, high-potential return income play.

Now, let's dive into the details!

What's Going On At Organon?

Generally speaking, Organon's financial results are mixed, not horrible.

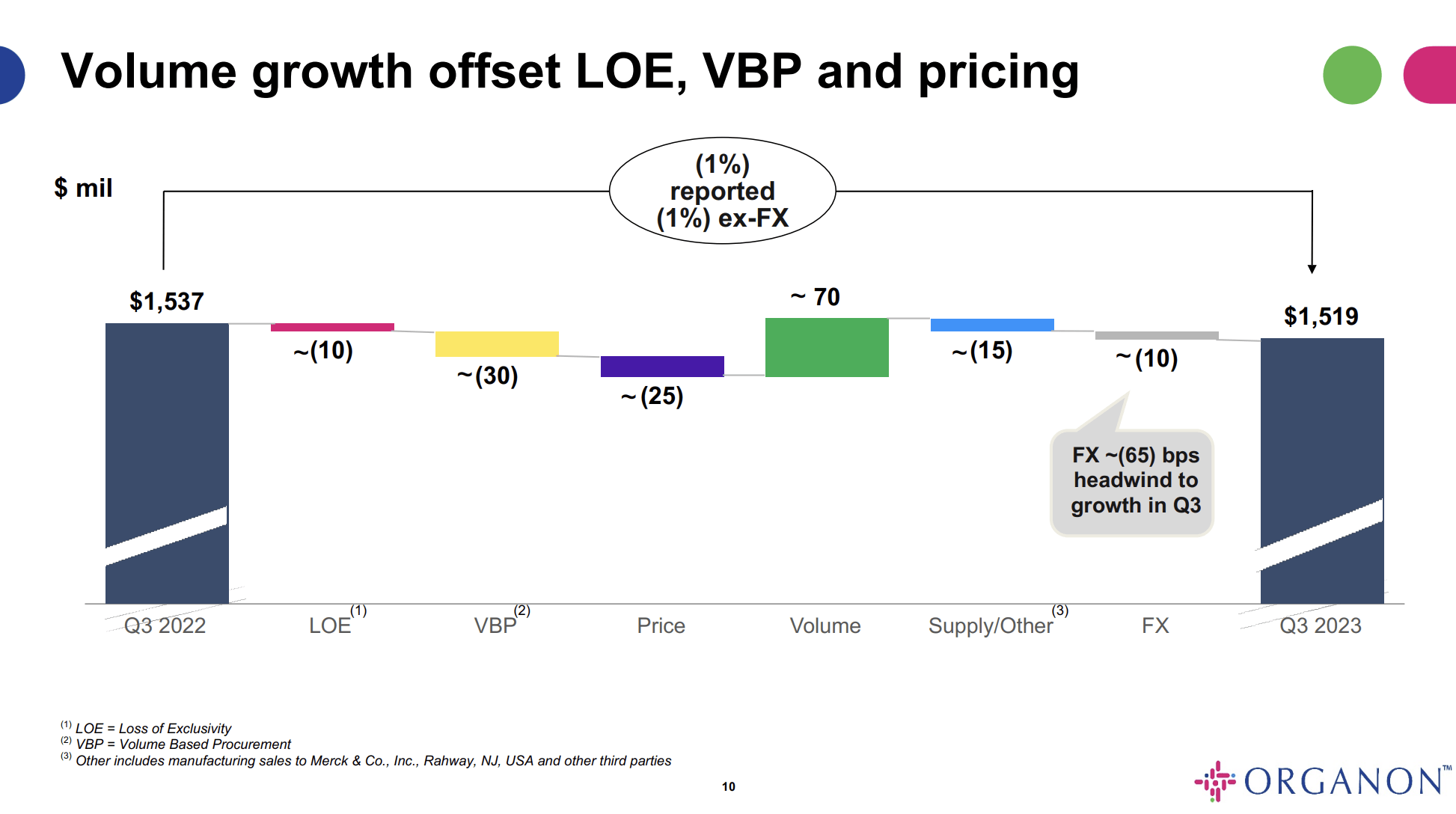

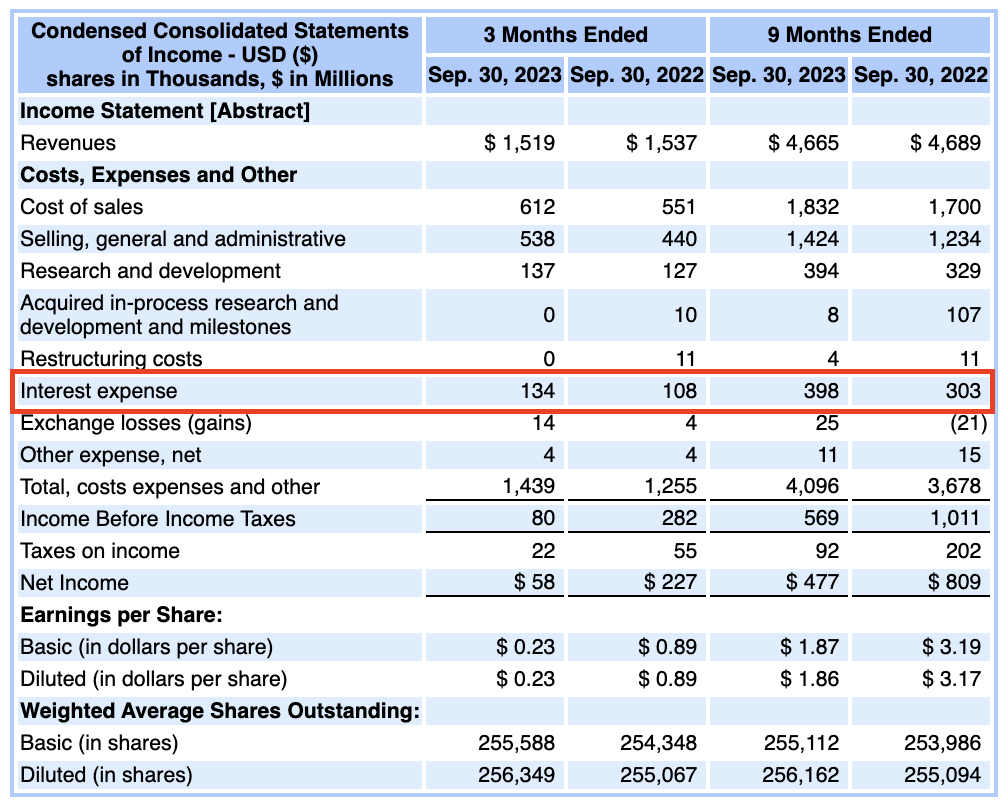

In the third quarter, the company reported a 1% growth in product sales at constant currency, marking the eighth consecutive quarter of product growth.

Total revenue, including lower-margin sales to Merck, declined by 1% at constant currency.

The quarter saw about $70 million of volume growth, primarily from established brands in the LAMERA region and non-VBP products in China.

Biosimilar volumes increased in the U.S., Canada, and Brazil due to volumes from new customers and greater purchasing from existing customers.

{kind=link}

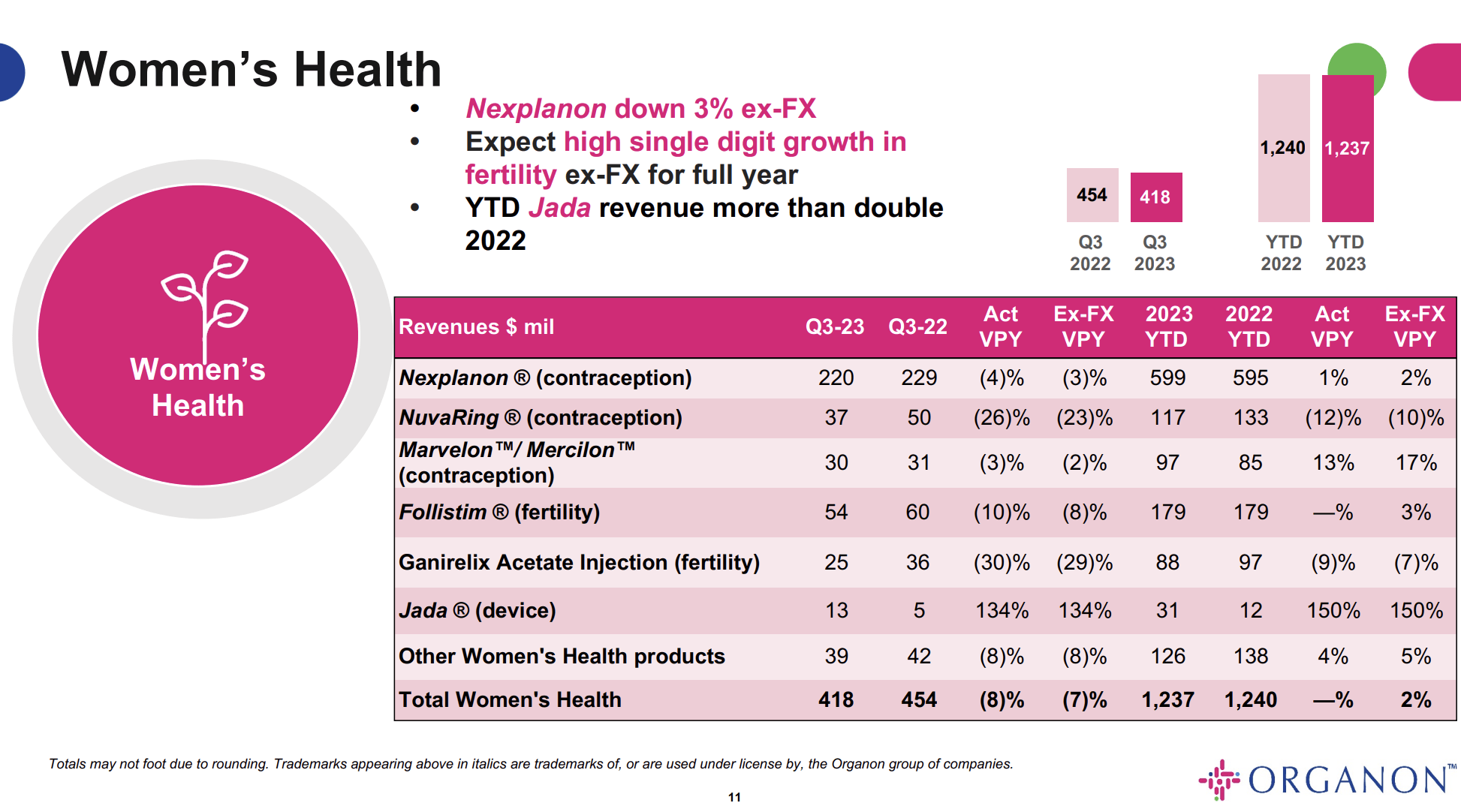

- In the women's health franchise, Nexplanon faced headwinds in 2023, but it's anticipated to return to strong growth in the high single digits next year. Fertility demand is solid, and new products like the Jada device for postpartum hemorrhage and Xaciato are expected to contribute to growth in 2024.

{kind=link}

-

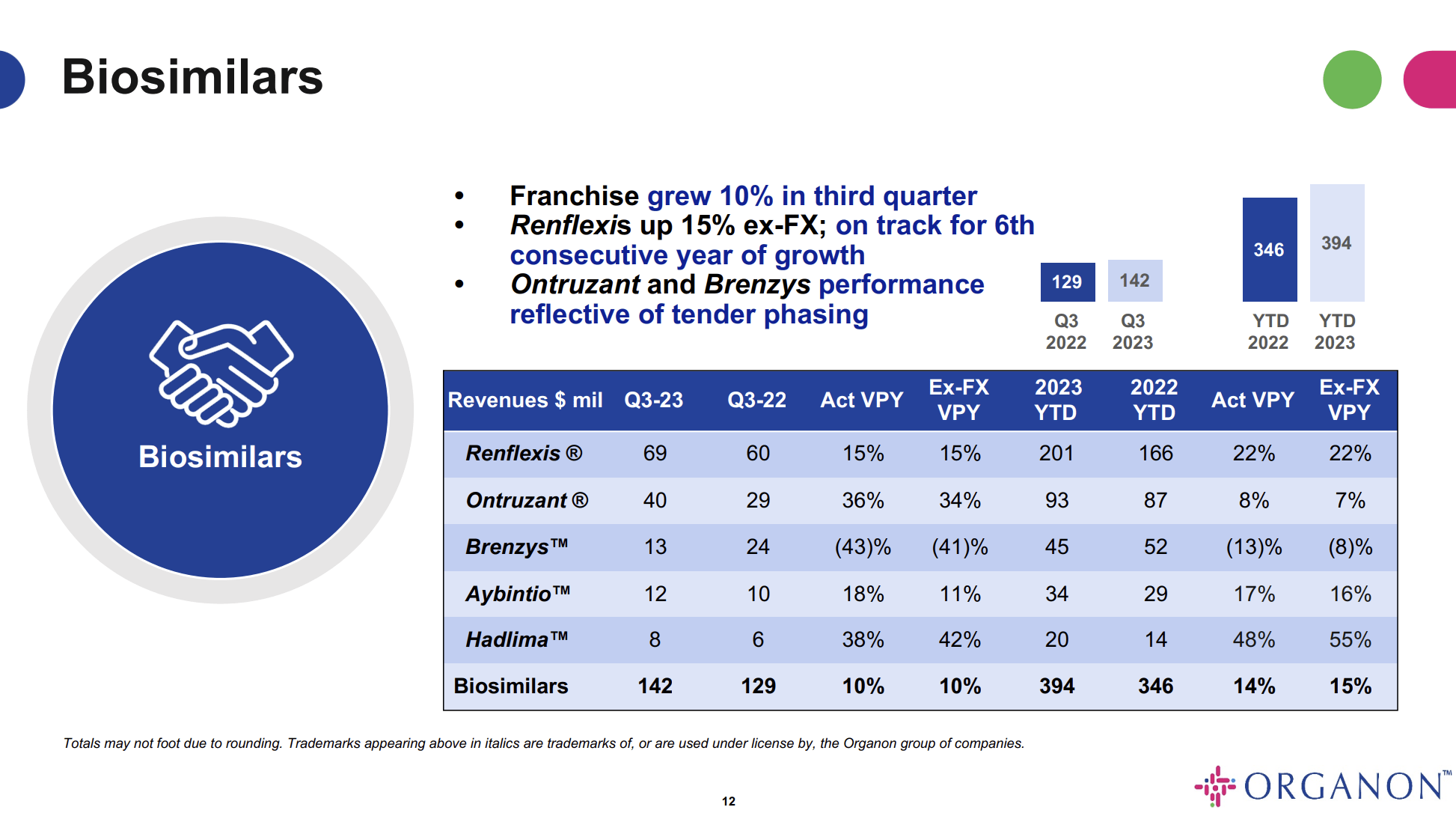

Biosimilars grew 10% ex-FX in the quarter and 15% ex-FX year-to-date. Renflexis showed strong growth, Ontruzant faced competitive dynamics, and Hadlima's global sales expectations for 2023 were revised downward due to slower market formation for HUMIRA biosimilars.

{kind=link}

-

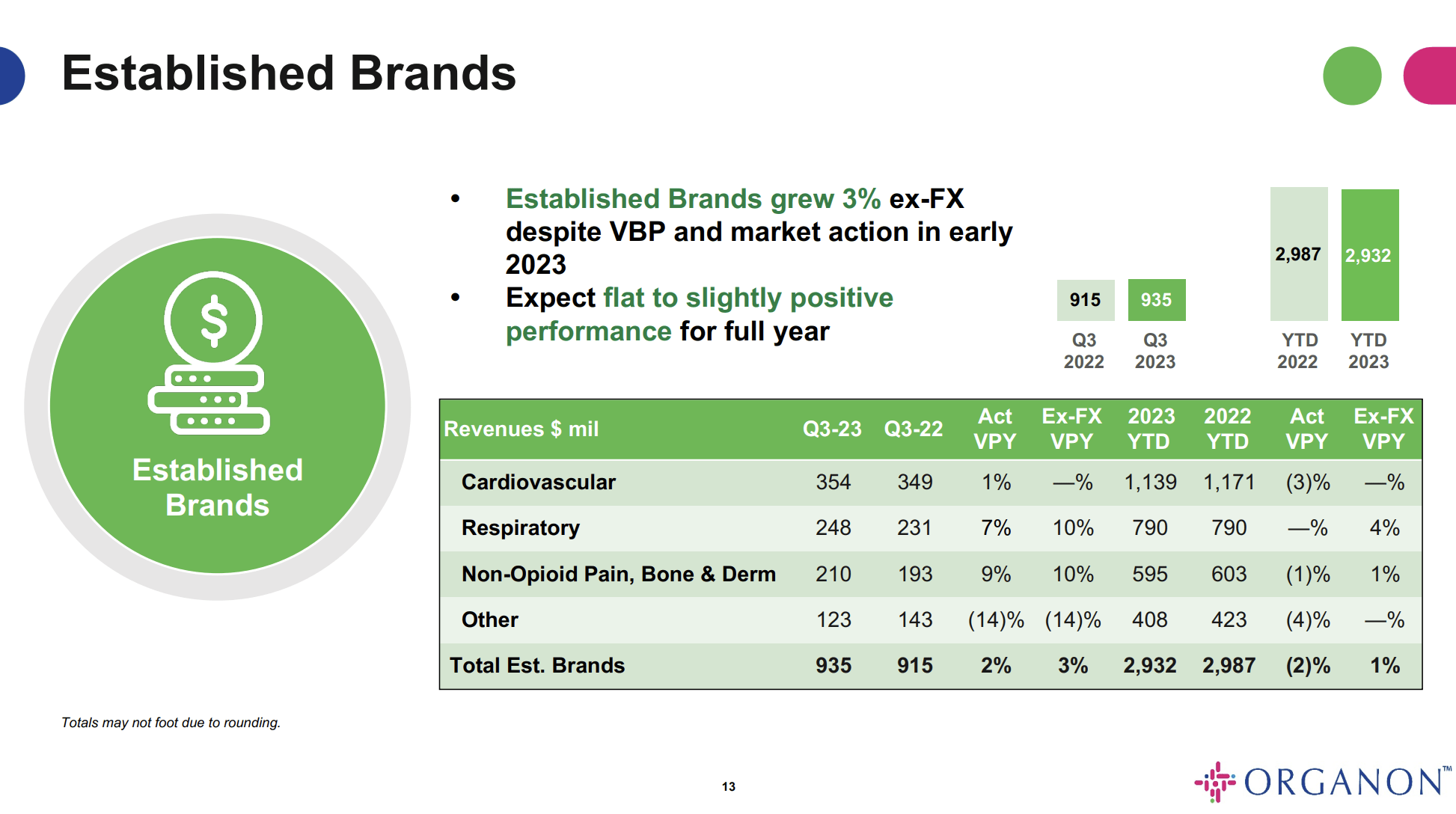

Established brands grew 3% ex-FX in the third quarter and maintained positive territory for the year at 1% growth year-to-date. Despite headwinds, the franchise demonstrated resilience, including challenges in China and market actions at the beginning of the year for injectable steroid products.

{kind=link}

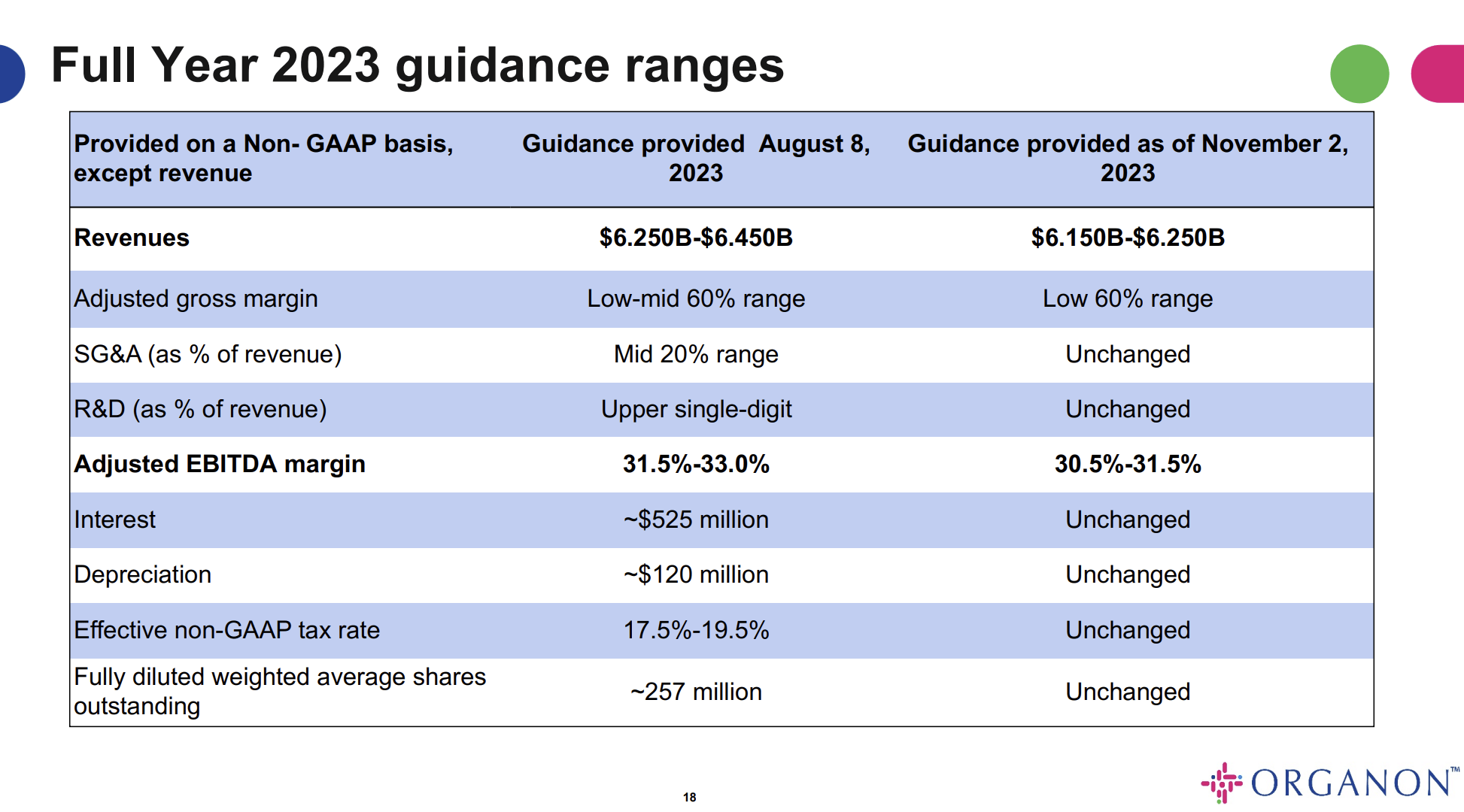

Unfortunately, a big part of the recent stock decline was its poor guidance.

The company downgraded its full-year guidance, including adjusting the revenue guidance range to $6.15 to $6.25 billion, reflecting constant currency growth of 1.6% to 3.3%.

{kind=link}

Several factors contribute to this adjustment (with volume growth being the biggest driver):

- Loss of Exclusivity Impact: The LOE impact has been minimal so far in 2023, and the company expects it to finish similarly. The guidance range for LOE impact was lowered to $10 to $20 million, down from $50 million to $75 million.

- Volume-Based Procurement ("VBP"): The annual impact of VBP is expected to be slightly lower than previously guided in the second quarter. The company is tracking better with both EZETROL and the recent Round 8 implementation.

- Price Erosion: The estimate for potential price erosion is improved to $90 to $100 million, down from $100 to $150 million. The established brand portfolio shows momentum in managing price erosion better than expected.

- Volume Growth Outlook: The outlook for volume growth was lowered, contributing to the revision in revenue guidance. The range is now $370 million to $400 million, about 6% year-on-year growth at the midpoint.

What About Long-Term Shareholder Value?

The biggest issue for OGN is debt reduction.

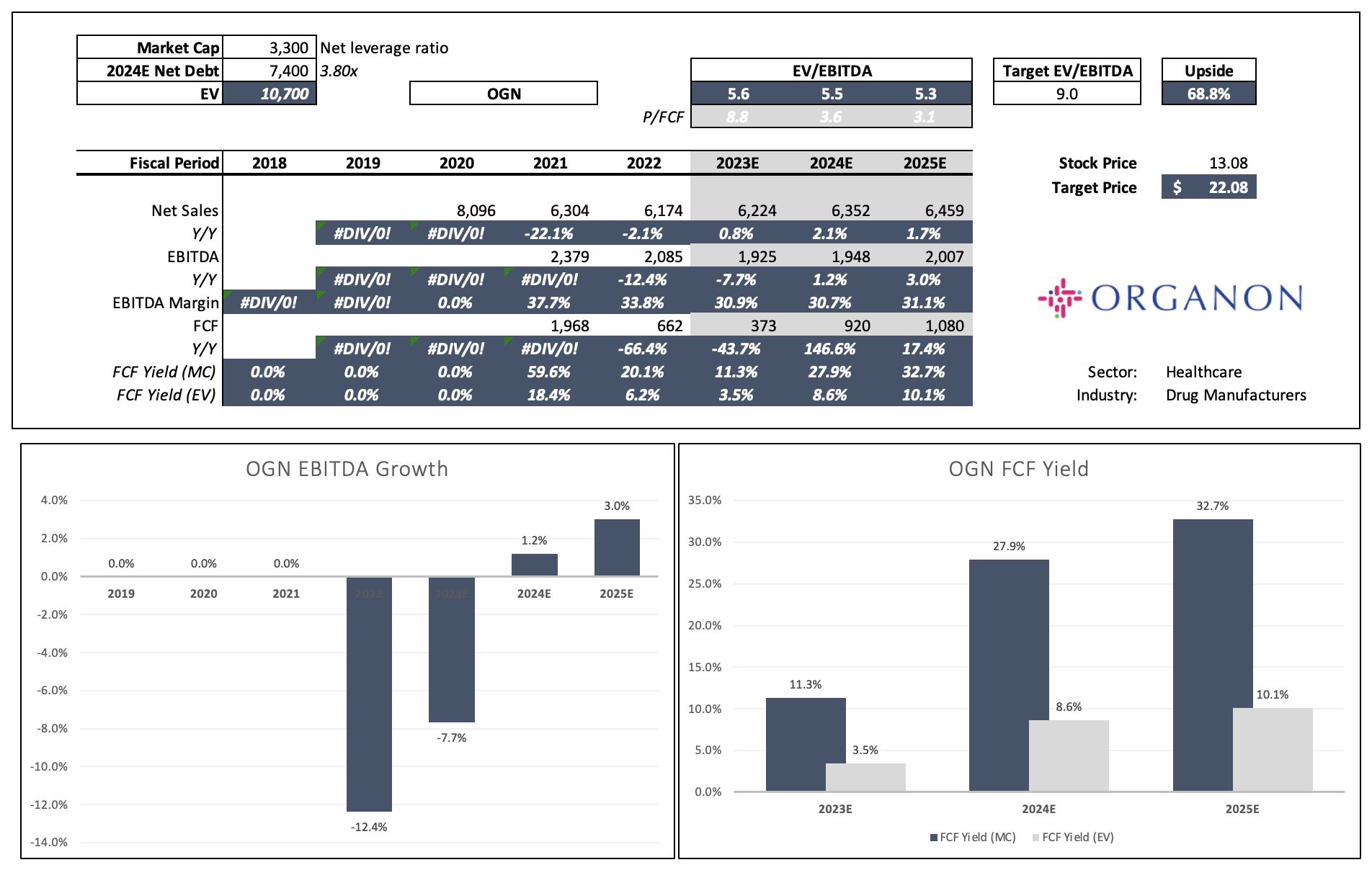

Looking at the overview below, we see that this company, with a market cap of $3.3 billion, has an implied free cash flow yield of roughly 28% using 2028 free cash flow expectations. This may be the highest number I have discussed for any company in 2023.

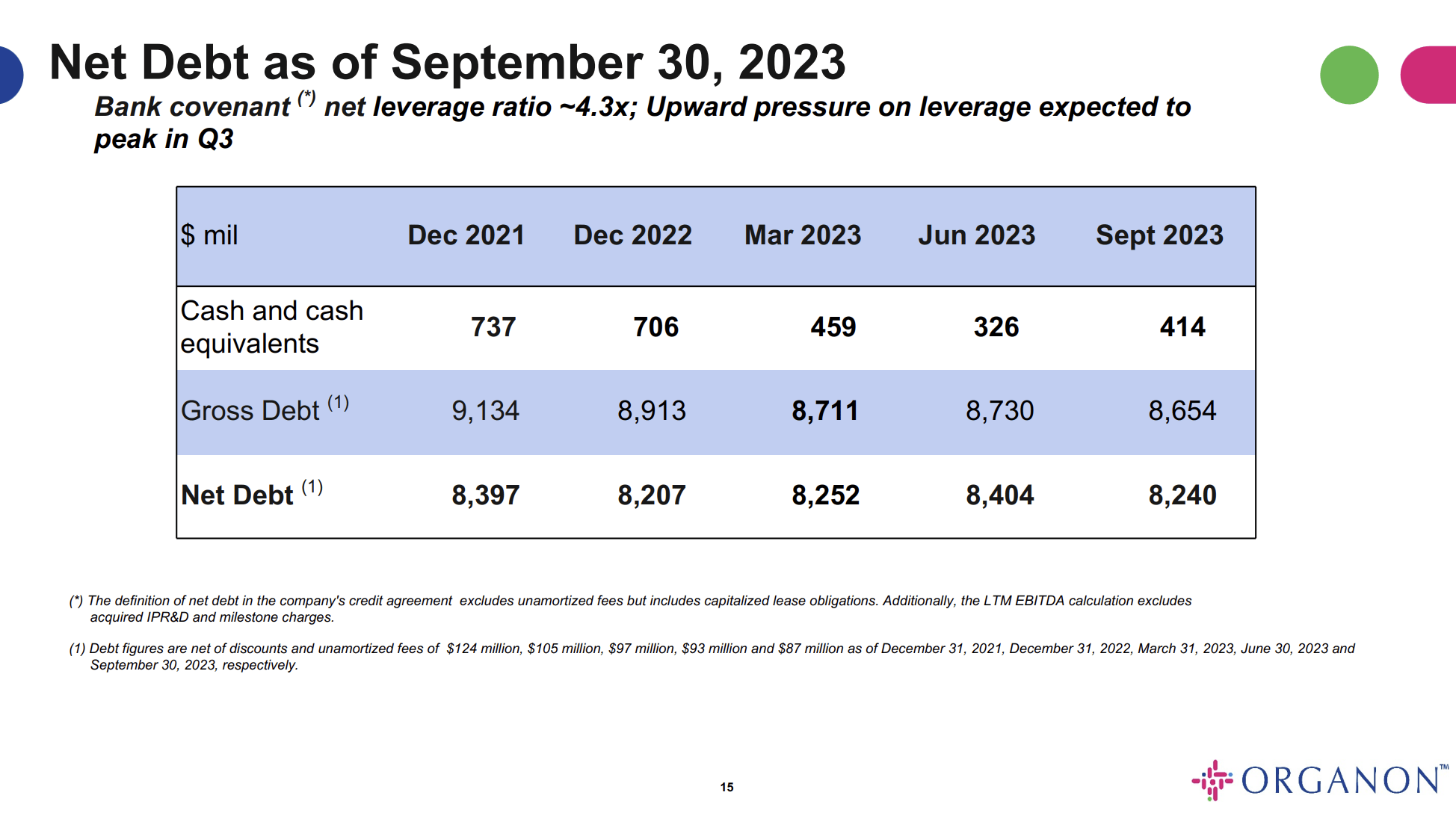

However, the free cash flow yield based on its enterprise value (market cap + net debt) is less than 10%, which shows the massive debt load. Next year, the company is expected to end up with $7.4 billion in net debt, which is more than twice its market cap and 3.8x expected EBITDA.

Leo Nelissen (Based on analyst estimates)

{kind=link}

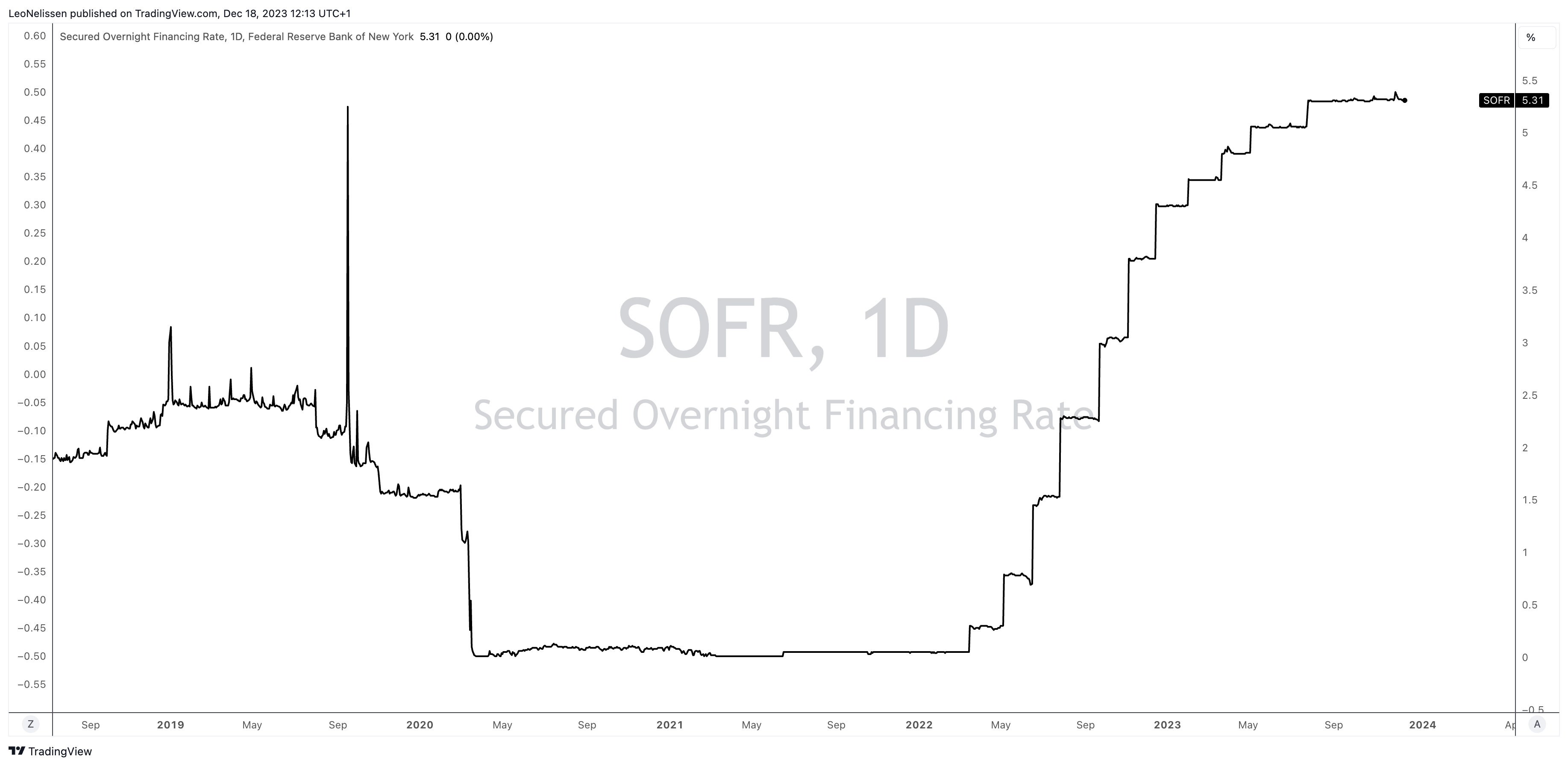

Especially in an environment where SOFR rates (the LIBOR successor) are trading at 5.30%, meaning companies with low credit scores and elevated debt levels will have to borrow at juicy premiums on top of this elevated rate.

{kind=link}

For example, going into this year, the company's Term Loan B credit facility yielded LIBOR + 300 basis points, which would put the current yield above 8.0%!

Hence, in the first nine months of this year, the company spent roughly $400 million in interest, up from $300 million in the prior-year period!

{kind=link}

It has a BB credit rating, which means there are three more steps between its current rating and a BBB- rating, which would lift the company from "junk" to investment grade.

In other words, the company needs to quickly lower net debt without hurting its dividend!

OGN currently pays a $0.28 dividend per share per quarter. This translates to a yield of 8.6%, one of the highest yields on the market.

Technically speaking, this dividend is protected by free cash flow, as its free cash flow yield is close to 30%. The question is how much room this leaves the company to pay down debt.

During the recent Piper Sandler Annual Healthcare Conference, the company outlined a clear and strategic focus on debt reduction during the discussion.

The company's approach involves a better understanding of its cost structure and a commitment to financial efficiency.

The company mentioned that it entered the third year with a deeper comprehension of its real cost structure, moving beyond the initial one-time costs associated with establishing the company.

The plan is to scrutinize operating expenses, aiming for a more leveraged profit and loss statement.

This approach includes a transition from the initial investment phase to a more efficient operational phase.

Organon also underscored the importance of achieving a debt-to-EBITDA ratio below 4x in the upcoming year. Since December 2021, it has lowered net debt from $8.4 billion to $8.2 billion, mainly by reducing gross debt by roughly $500 million.

{kind=link}

As my financial overview showed, analysts believe that OGN can achieve a 3.7x leverage ratio at the end of 2024.

Furthermore, the focus will be on business development instead of M&A, meaning every penny of excess free cash flow will be used to reduce debt.

But nevertheless, as we start to be able to generate more free cash flow, absent anything that's interesting in BD will definitely put it to debt pay down. - Kevin Ali , Organon CEO

As the company is projected to boost free cash flow to more than $1 billion by 2024, I expect the dividend to be (relatively) safe, although I would not rule out a potential cut if management decides that debt reduction isn't going fast enough.

This could be triggered by slower-than-expected growth of key products or similar headwinds.

However, if the company is able to protect its dividend and reduce debt as planned without hurting its core business, it offers tremendous value at these levels.

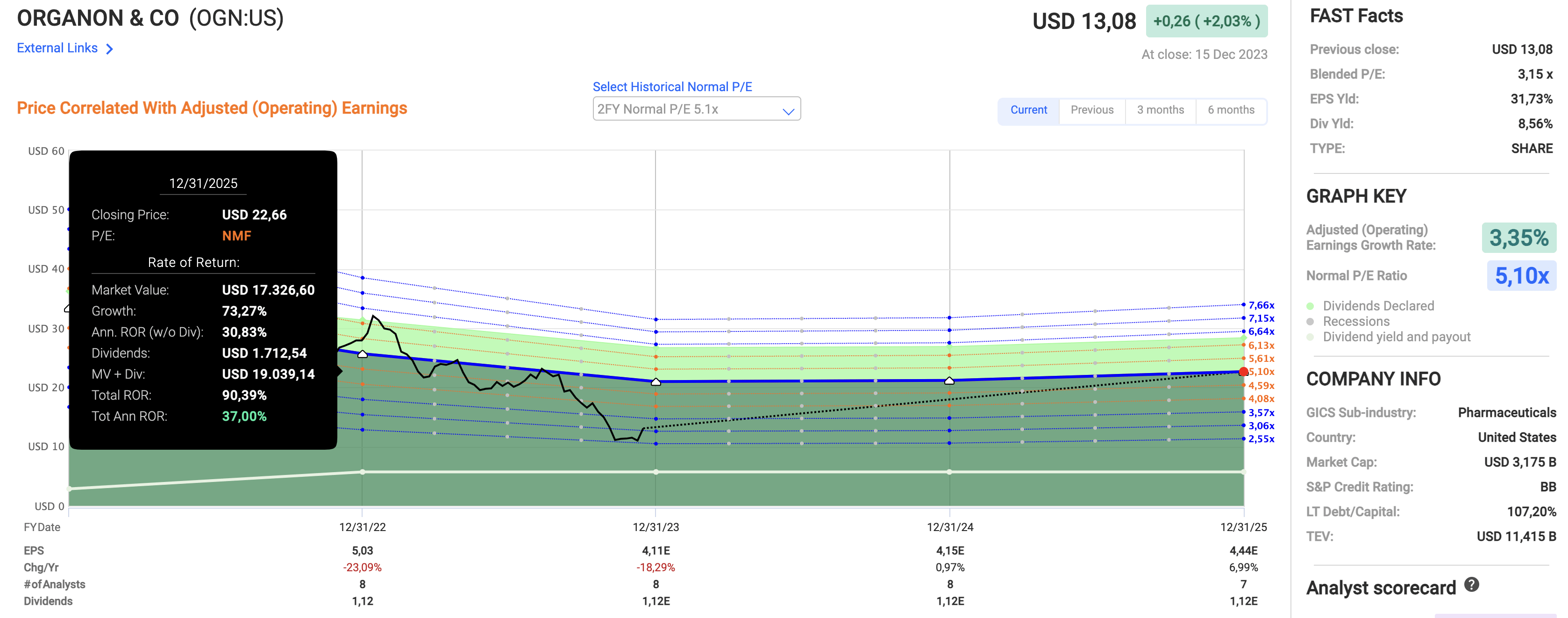

As my analyst estimates table in this article showed, a 9x EBITDA multiple in 2025 would give the stock a fair price of $22.10, which is roughly 70% above the current price.

We find similar numbers when we apply an earnings-per-share multiple of 5.1x.

As we can see in the chart below, OGN shares have traded at a normalized multiple of 5.1x EPS since its spin-off. The current blended P/E ratio is 3.2x.

{kind=link}

This year, EPS is expected to decline by 18%, followed by a recovery of 1% growth in 2024 and 7% growth in 2025.

Including its dividend, the stock could return 37% per year through 2025, which translates to a total return of roughly 90% and a fair price target of $22.70.

Hence, I stick to a Buy rating and believe that OGN is a high-risk healthcare play that could pay off handsomely.

If management can successfully execute its plans, OGN investors could benefit from a high yield, potential capital gains, and future dividend hikes.

Needless to say, risks are elevated, and I would not, under any circumstances, make OGN a big part of any income-focused portfolio, especially since I expect rates to remain elevated.

Takeaway

Despite a recent 32% stock decline and downgraded guidance, I maintain a bullish view of Organon.

The company faces challenges like debt and lowered revenue expectations, but its strategic focus on debt reduction and cost efficiency is commendable.

With a high dividend yield of 8.6% and plans to boost free cash flow, OGN could offer substantial value.

While risks are elevated, successful execution of the debt reduction plan could lead to significant returns.

Hence, I rate OGN a high-risk, high-potential return healthcare play.

For further details see:

High Risk, High Reward: Why 8.5%-Yielding Organon Could Be Up To 90% Undervalued