CCI - High Yield Blue-Chip REITs On Sale: Realty Income And Crown Castle

2023-06-29 08:00:00 ET

Summary

- REITs have been pummeled over the past year and a half due to rising interest rates.

- As a result, there are some very attractive blue chip REITs selling at compellingly discounted levels at the moment.

- We take a look at CCI and O as two high yielding opportunities that also offer compelling long-term growth potential alongside very strong business models and management teams.

With interest rates rising and increasingly likely to keep rates higher for longer, the interest rate sensitive REIT sector ( VNQ ) has gotten pummeled over the past year and a half:

Some of this sell-off has certainly been justified, given the dramatic pace of interest rate hikes over that period of time:

However, it has also resulted in cases of the baby getting thrown out with the bathwater, as world-class REITs with solid long-term growth prospects have gotten beaten severely along with the lower quality REITs that have much less certainty in their futures.

In this article, we will share two discounted high yield blue chip REITs that are buys during the current dip.

#1. Crown Castle Stock ( CCI )

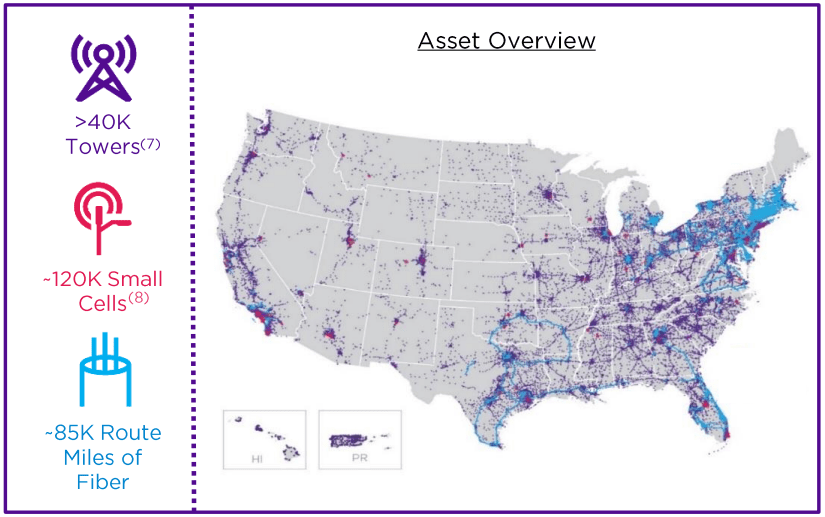

CCI is a blue-chip telecom REIT that owns a well-diversified portfolio of over 40,000 towers, 120,000 small cells, and 85,000 route miles of fiber that makes it an important player in the ongoing 5G deployment across the United States.

CCI Asset Overview (Investor Presentation)

{kind=link}

Moreover, it gives the company a lengthy growth runway to continue driving strong dividend growth for many years to come. In addition to the growth profile, CCI also generates dependable cash flows thanks to a six-year weighted average remaining tenant contract term with $39 billion in remaining contracted tenant receivables.

Keep in mind that this is not just a charismatic investment pitch from management, but the company's track record demonstrates the merit of its business model. It has generated very robust dividend growth that has more than tripled that of VNQ since CCI went public. Moreover, CCI has also generated significantly superior total returns to VNQ over the course of CCI's publicly traded lifespan.

Moving forward, CCI still has tremendous growth potential thanks in large part to its small cell opportunity (with estimates that this opportunity will experience a 15-30% CAGR through 2025) alongside its core tower business that also still has solid growth potential.

However, in the near term (~2 years), the company is projecting that dividend growth will slow from its high single digit CAGR of recent years to a low single digit rate. The reason for this is because CCI is facing a major cash flow headwind from cancelled leases resulting from T-Mobile ( TMUS ) acquiring Sprint. That said, management believes that they will still be able to grow their dividend at a 7-8% CAGR over the long-term as their small cell business ramps and CCI replaces the cash flow lost from the TMUS-Sprint merger and consolidation.

We are optimistic that CCI should be able to reaccelerate their dividend growth in 2025 and beyond thanks to:

- Their strong track record of dividend growth

- Their strong current position in the small cell business and robust growth momentum there.

- Their strong, investment grade balance sheet with an 8-year weighted average term to maturity with only very minor debt maturities in 2023 and 2024, a 3.7% weighted average interest rate, and 91% fixed rate debt exposure.

- Their reasonable 82% expected payout ratio for 2023.

Given that their valuation has become so attractive after the recent sell-off, CCI does not even need to reach its target dividend growth rate in order to deliver attractive total returns. Its current NTM dividend yield is a very attractive 5.7%, meaning that a mere 4.3% CAGR is needed moving forward to deliver 10% annualized total returns assuming no further changes in dividend yield. On top of that, analyst consensus NAV per share is $170.40, indicating that the current share price is priced at a ~35% discount to the underlying private market value of the portfolio. Moreover, its EV/EBITDA, P/FFO, and P/AFFO are all trading at clear discounts to historical averages:

| Metric |

| Current |

| 5-Year Average |

| P/NAV |

| 0.65x |

| 0.86x |

| EV/EBITDA |

| 17.22x |

| 23.30x |

| P/FFO |

| 14.46x |

| 23.37x |

| P/AFFO |

| 14.63x |

| 22.71x |

| Dividend Yield |

| 5.72% |

| 3.61% |

As a result, CCI falls into the Strong Buy category with a pretty clear path to double-digit long-term annualized total returns.

#2. Realty Income Stock ( O )

O is a leading triple net lease REIT that benefits from the safety and stability that comes from the business model as well as its very large and well-diversified portfolio. With its 12,492 properties and 1,259 tenants diversified across 84 industries, O is well diversified against struggles in any single property, tenant, or sector.

O Portfolio (Investor Presentation)

{kind=link}

Moreover, ~91% of its ABR comes from recession resistant and/or e-commerce resistant tenants, along with ~41% of ABR from investment-grade tenants. This makes it an even safer bet in the face of a potential economic downturn.

O has grown its portfolio to such a massive size over the course of several decades thanks to a very simple strategy of issuing shares opportunistically at premiums to NAV and combining it with long-term fixed low rate debt to generate steadily growing cash flow and dividends per share alongside increasing scale and diversification benefits. The results speak for themselves:

On top of that, O has grown its dividend every year for over a quarter century, making it a Dividend Aristocrat ( NOBL ) while also generating positive earnings per share growth in 26 out of 27 years as a publicly traded company with median AFFO per share growth of 5% since 1996.

Moving forward, O's dividend is unlikely to exceed a mid-single digit CAGR, but with a current NTM yield of 5.1% and its stock trading at a deep discount to recent historical averages, it does not need to generate much growth to deliver attractive risk-adjusted returns.

We feel confident that O will be able to generate a 3-5% Dividend per share CAGR for the foreseeable future for the following reasons:

- O has a stellar A- rated balance sheet that gives it a cost of capital advantage relative to many of its peers, thereby fueling more durable per share cash flow growth. Moreover, its well-laddered debt maturities, 5.9 year weighted average term to maturity for its notes and bonds, and a low percentage (10%) of floating rate debt, it should face minimal headwinds from higher interest rates and continue to enjoy access to competitively priced debt.

- While its stock is clearly trading at a discount to its historical norms, it still trades at a slight premium to NAV (1.03x), meaning that it can continue to issue equity to fuel accretive growth via acquisitions.

- Its very defensive business model and contractual rent bumps in its portfolio should drive stable performance and organic growth.

- Management has proven itself adept at finding new ways to grow accretively as the company has gotten larger while also delivering impressively consistent and strong dividend growth.

- The 2023E payout ratio looks quite reasonable at 73.8%, giving it plenty of room to continue growing its dividend even in years where cash flow per share may not be significant.

- Wall Street analysts are also confident that O can continue to churn out steady dividend growth in the coming years, forecasting a dividend per share CAGR of 4.1% through 2027.

O will also likely see valuation multiple expansion in the coming years given that its valuation multiples are so heavily discounted relative to their recent history:

| Metric |

| Current |

| 5-Year Average |

| P/NAV |

| 1.03x |

| 1.24x |

| EV/EBITDA |

| 16.22x |

| 19.34x |

| P/FFO |

| 14.43x |

| 18.42x |

| P/AFFO |

| 14.90x |

| 18.47x |

| Dividend Yield |

| 5.12% |

| 4.37% |

As a result, O looks like a strong candidate to deliver 9-12% annualized total returns with pretty low risk, making it an attractive Buy at current levels.

Investor Takeaway

While REITs have been pummeled and interest rates appear likely to remain higher for longer, CCI and O are two blue chip stocks that currently offer high yields and have attractive growth potential along with fairly low risk profiles. They are also trading at steep discounts to their historical averages, giving them substantial repricing potential, especially if interest rates fall in the future.

As a result, we rate CCI a Strong Buy and O a low risk Buy at the moment and think they are worth buying on the current dip.

For further details see:

High Yield Blue-Chip REITs On Sale: Realty Income And Crown Castle