NWL - High Yield Means High Risk: 3 Stocks With Serious Warning Signs

2023-03-29 12:30:09 ET

Summary

- Equities with high yields can mean high risk. When markets fall, especially in a high-interest rate environment, the risk on high-yielding stocks may be even greater.

- This article highlights three stocks with high yields that have poor overall metrics, posing many quant warning signals, intensified amid the banking crisis and interest rate climb.

- Notably, REITs and the real estate sector, despite portfolio diversification and typical inflation-beating income streams, should be viewed with caution when their yields are abnormally high.

- Despite offering tremendous yields and trading at discounts, investors should be on high alert when stocks display very large yields, as high yields are often a tell-tale of risk.

- SA’s quant ratings, dividend grades, and tools help to quickly display what stocks are at risk.

Investing in Stocks for Income: Treasuries or High Yield?

Over the last few years, we’ve witnessed a pandemic, economic corrections, tech and banking crashes, crypto scandals, and a real estate market that’s soared and flattened. When considering ways to hedge against inflation, some of the most apparent methods involve diversification. Finding investments that pay income to naturally offset a drop in portfolio gains and to offset drops in currency that result in decreased purchasing power leads many to think of high yield.

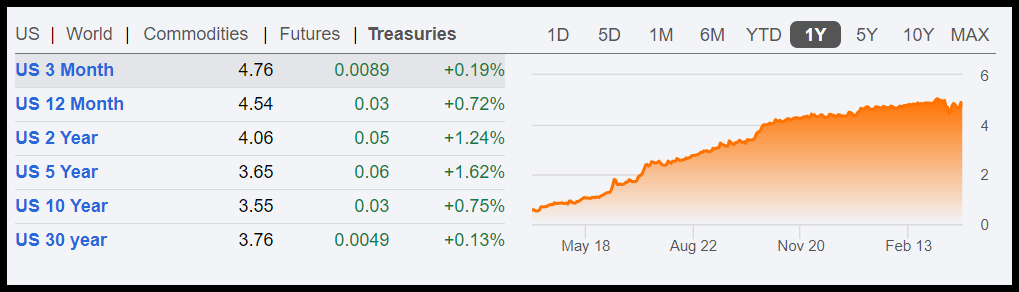

U.S. Treasuries Are On a One-Year Rally

{kind=link}

Especially as today’s interest rate poses the biggest risks, the price of T-Bills and Treasuries backed by the U.S. government offering 4% to 5% makes stocks once considered high yielding less attractive to investors. Why accept the risk of equities when I can receive a guaranteed 4.76%, as showcased above? And if you’re an investor with a higher risk threshold and considering low-quality equities, in today’s environment with the current rate and terms the government offers, I’d rather buy bonds - less risk involved. Then when you factor in the higher cost of capital that corporations are now exposed to due to higher interest rates, their ability to maintain dividend payouts and high yields comes into question and reduces confidence. In a slowing environment, where companies are experiencing earnings misses and dwindling profits, the likelihood of a dividend cut increases, particularly for low-quality companies that already lack profits. Focusing on profitable companies with solid growth and fundamentals can help a portfolio stand the test of time. With cash no longer king as purchasing power falls and inflation eats away at profits, companies holding high cash levels should quickly review their cash management policies. With confidence in the economy and the banking system deteriorating quickly on the heels of Silicon Valley Bank’s demise , I’m highlighting three high-yielding stocks that may look good on the surface and come at excellent valuations. But they also come at high risk with dwindling cash for operations, lacking growth and profitability, and notably, SA Quant showcases their inferior Factor Grades and Quant Ratings.

3 Stocks with High Yields to Avoid

The below screen showcases tremendous yields, but each stock’s financials and overall fundamentals are lacking, putting them at high risk of poor performance. Although each stock’s yield appears strong, this payout is relative to its share price and does not mean the company is doing well. Investors must dig deeper into a stock’s fundamentals and should not rely solely on yield to judge an investment. I’ve often said that not all dividend and high-yielding stocks are equal, so let's dive into the three stocks.

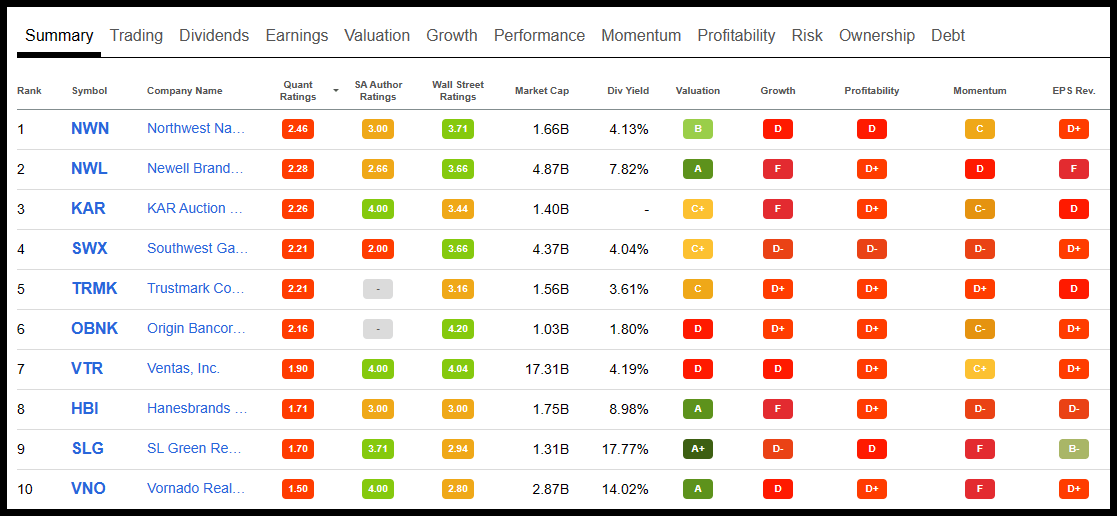

10 High Yield High-Risk Stocks

{kind=link}

1. Newell Brands Inc. ( NWL )

-

Market Capitalization: $4.87B

-

Quant Rating: Sell

-

Dividend Yield ((FWD)) (as of 3/28): 7.82%

-

Quant Sector Ranking (as of 3/28): 426 out of 537

-

Quant Industry Ranking (as of 3/28): 1 out of 3

Offering over 100 brands in Housewares and Specialties, Newell Brands designs, manufactures, and distributes popular products like Rubbermaid, Yankee Candle, Mr. Coffee, and many more. While this consumer discretionary stock may offer the beloved brands used in everyday living, its poor performance has been met by headwinds that include rising costs, declining demand, debt, and a negative outlook resulting in its cut to junk rating by S&P Global Ratings, as detailed in a Seeking Alpha news report :

“S&P believes Newell Brands is not committed to a financial policy that supports an investment-grade rating because it prioritized shareholder returns over debt reduction. In addition, the ratings agency believes NWL cannot materially reduce its current short-term debt balance in 2023 and 2024 because of the projected $200M of discretionary cash flow generation in total over the two-year period. Adding to the burden, S&P said NWL will likely have to refinance some maturities or borrow to repay them, which will likely increase its debt levels and interest burden, which could put pressure on its ability to meet its interest coverage covenant of 3.5X.”

{kind=link}

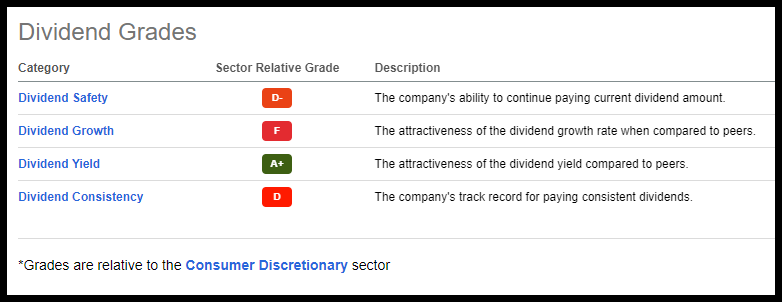

The company has admitted to increases in debt due to management’s decision regarding capital allocation and a challenging macroeconomic environment. Although the company has an excellent 7.82% dividend yield, its dividend safety, dividend growth, and consistency are lacking. While Newell’s commitment to paying its sizable dividend of $400M annually despite negative cash flow may appeal to some, whether it stands the test of time given management’s decision-making coupled with bearish momentum could result in its demise.

NWL Stock Momentum and Valuation

Newell Brands is -12% YTD and -46% over the last year. Its price performance is on a gradual quarterly decline relative to its sector peers. Billionaire American Financer Carl Icahn has opted to trim his stake in the stock. Icahn, who once owned an estimated 8.17%, is thought to have lost nearly 55% of his estimated purchase price of $866M. News of the sale resulted in a fall in the stock on a longer-term bearish trend.

NWL's Momentum is on a quarterly decline compared to sector peers

NWL's Momentum is on a quarterly decline compared to sector peers (SA Premium)

The stock’s 200-day moving average has been falling, along with its momentum, as evidenced above. Despite the stock trading at a great discount – one of the few attractive metrics – its trailing P/E ratio of 25.04x comes at a 72% premium compared to sector peers. However, its other underlying Valuation Grades , especially dividend yield, are positive. Still, they are not enough to offset the remaining Factor Grades, which offer up strong indicators that the attractiveness of the company’s dividend yield, growth, and ability to continue paying a dividend may not stand the test of time.

Newell Brands Factor Grades

Newell Brands Factor Grades (SA Premium)

NWL Growth And Profitability

Seeking Alpha’s Factor Grades rate investment characteristics on a sector-relative basis. valuation aside, Newell Brands' grades are dismal, as showcased above. Lacking growth and profitability, 11 analysts have revised estimates down, with zero upward FY1 revisions in the last 90 days. Although Newell Brands’ fourth quarter EPS of $0.16 beat by $0.05 and revenue of $2.29B beat by $56.35M, the company's growth has lacked, as indicated by its ‘F’ grade for growth. The Consumer Discretionary sector ( XLY ) is one of the top-performing sectors YTD. Meanwhile, NWL’s declining growth is evidenced by a forward revenue growth of -5.66% compared to the sector median of 7.2%, and EPS FWD Long term growth ((3-5Y CAGR)) is -0.65% versus the sector of 12%.

NWL Stock Growth Grade (SA Premium)

Compared to its Core sales one year ago, which experienced 12.5% growth, Newell has seen a 3.4% decline. To restructure and improve cash flow and gross margins, the company has reduced many SKUs, eliminated nearly 13% of the office positions from its cost-cutting plan called Project Phoenix, and hopes to focus on delivering its successful brands through e-commerce and its omnichannel prowess. Adding another devastating blow, Newell Brands CEO Ravi Saligram announced his retirement from the company.

“It has been a distinct honor leading Newell Brands over the last several years, and I am inspired by our talented employees who are passionate, resilient, and courageous… I am confident that they are committed to making Project Phoenix and our new Segment-based operating model a major success.”

The CEO may not be the only retiring aspect of this company. Along with its dividend, my following two stocks are REITs, feeling the pressure of high interest, an economic slowdown, and a banking crisis that puts their high yield at high risk.

High Yield High-Risk REITs

Chief Investment Officer of the Syz Group hit the nail on the head when he wrote :

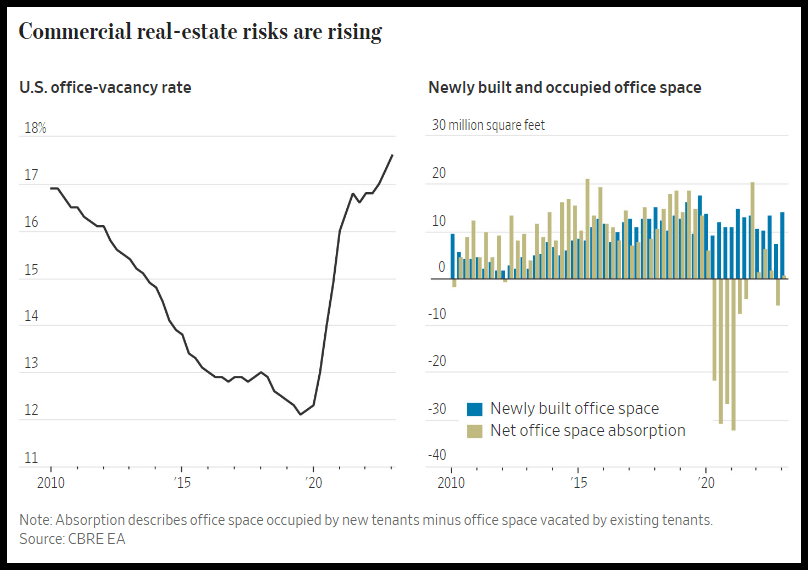

“Vacant office space in the US is at its highest level ever of 18.7%. No rent is being paid on 1/5th of all US office space. Meanwhile, $46 billion of variable rate office debt will mature and need to be rolled this year. Will we see a wave of defaults on commercial real estate loans?”

With the U.S.’s highest proportion of vacant office space ever, landlords are becoming the biggest losers.

Highest % Office Vacancy in U.S. Chart (Joe Consorti, Bloomberg)

{kind=link}

The pandemic didn’t just highlight aspects within supply chains that could make or break investment opportunities. Investors took advantage of record-low interest rates. But as rates have surged, real estate and commercial property loans feel the pressures intensified by the banking crisis.

{kind=link}

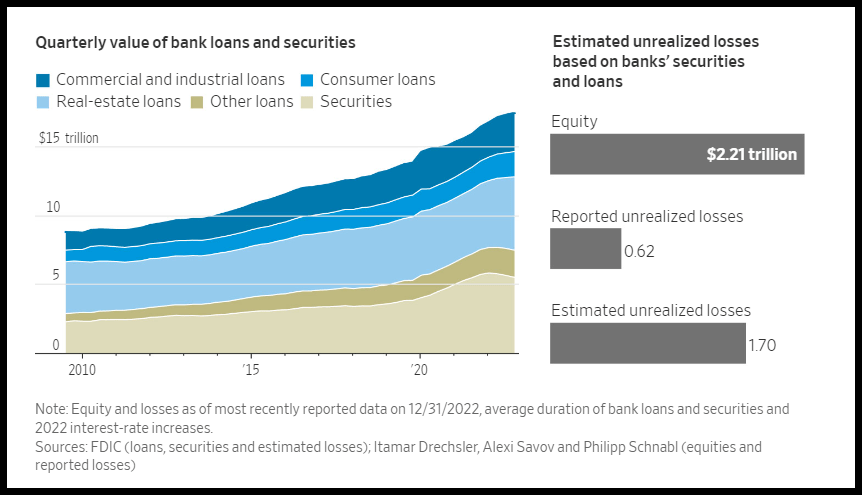

Not only did banks take on $2.8 trillion in deposits at the end of 2022 and invest in mortgage-backed securities, but with rising interest rates, they also may be forced to sell holdings at a loss. Stepping in, the Fed offers loans at pennies on the dollar, adding pressure to real estate companies like the two REITs I’ve picked that are already at high risk of performing badly. Although a recent study published by the NAIOP Research Foundation highlights the economic contributions of new commercial spaces, many of the losses we’re seeing by the sudden collapse of banks like Silicon Valley Bank involve the unrealized losses on lender balance sheets from mortgage- and asset-backed securities, pressuring landlords who have already scaled back, are experiencing a high degree of vacancies on the heels of employees working remote and vacant office spaces. Case in point SLG and VNO.

2. SL Green Realty Corp. ( SLG )

-

Market Capitalization: $1.33B

-

P/FFO [FWD]: 3.79

-

Quant Rating: Sell

-

Dividend Yield [FWD] (as of 3/28): 15.75%

-

Quant Sector Ranking (as of 3/28): 157 out of 178

-

Quant Industry Ranking (as of 3/28): 17 out of 22

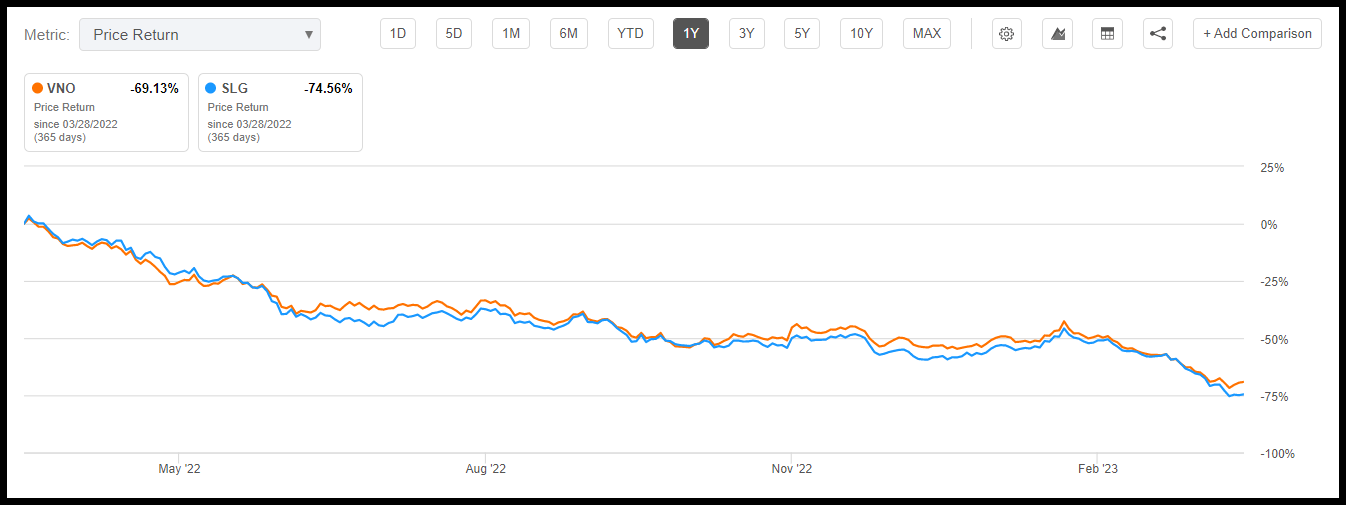

New York City’s largest owner of office real estate, SL Green Realty Corp., is a REIT focused on acquiring and managing Manhattan commercial properties. New York City remains a shadow of its life before the pandemic, with many individuals still working remotely. With 88 buildings totaling 38.2M square feet, SLG, while undervalued, is facing headwinds amid refinancing risks as its debt matures. Higher interest rates and the fallout of banks are putting pressure on SLG, whose $2.2B in 2023/24 debt maturities will result in higher-than-expected costs. SLG and its competitor Vornado Realty Trust ( VNO ) are highly leveraged, posing potential detrimental effects on the companies as interest rates have crushed common equity. Year-to-date, both REITs are down more than 30%, and over the last year, they’ve been crushed as they continue their downtrend, as highlighted in their dismal momentum.

VNO & SLG 1-Yr Price Decline

{kind=link}

3. Vornado Realty Trust

-

Market Capitalization: $2.91B

-

P/FFO [FWD]: 5.34

-

Quant Rating: Strong Sell

-

Dividend Yield [FWD] (as of 3/28): 10.58%

-

Quant Sector Ranking (as of 3/28): 161 out of 178

-

Quant Industry Ranking (as of 3/28): 19 out of 22

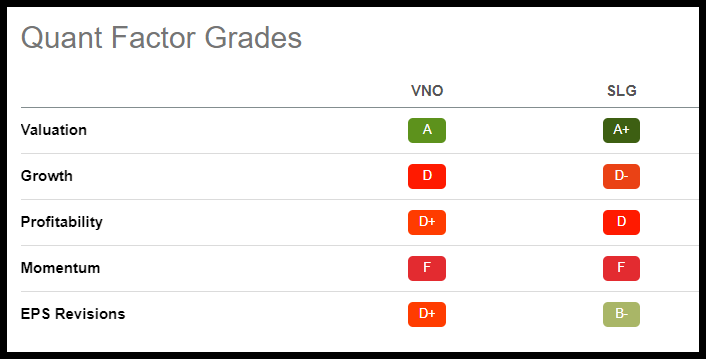

Also focused on commercial office space in Manhattan, Vornado Realty Trust offers premier assets in Chicago and San Francisco, managing over 23 million square feet of LEED-certified buildings. Despite both SLG and Vornado’s deep discounts and high yields, their overall metrics are unattractive, as displayed by their Factor Grades.

VNO and SLG Factor Grades

{kind=link}

Although their four-year average yields are each above 7%, both stocks have poor dividend growth and uncertain dividend safety. Housed primarily in NYC, a diversified business epicenter should make these two REITs seem like a slam dunk. But as the pandemic paved the way for remote work and the Fed began raising rates to tame inflation, the lease decline is adding to an already challenging environment. When you factor in that office REITs typically buy office buildings through bank loans, given the banking debacles we’ve seen lately, Binary Tree Analytics outlines the scenario well, noting that higher interest rates can have dual impacts.

-

Higher rates drive lower valuations for office properties, thus making the asset side of SLG (and VNO) less valuable.

-

Higher rates will be responsible for higher financing costs, making SL Green (and VNO) less profitable unless it sells buildings.

-

Both stocks are highly leveraged, and in the event of refinance/exit, there could be difficulties and impacts on common equity.

Where shareholders appreciate a steady income stream, the commercial real estate risks are mounting, especially amid banks’ exposure. As stated by FDIC Chairman Martin Gruenberg:

“The combination of lower operating income generated by office properties and a higher cost of financing, if they persist, would be expected to reduce valuations for these properties over time. This is an area of ongoing supervisory attention.”

{kind=link}

With profitability falling, analysts are revising their estimates for both stocks. In the last 90 days, VNO and SLG received 11 FFO FY1 downward revisions on the heels of their EPS misses. In recent downgrades after underwhelming reports, Vornado cut its dividend by 29% following fourth quarter earnings. FFO of $0.72 per share was 11% lower than its $0.81 2021 Q4 adjusted FFO. In a similar action, SLG cut its dividend by 13% following lackluster Q4 earnings. SL Green’s FFO of $1.46 per share was 4% lower than its 2021 Q4 results. Both companies anticipate a disproportionate impact from high-interest rates, given their leverage capital structures, falling occupancy rates, and dampening rent growth. Hybrid work disruption has also negatively impacted office real estate, as the national vacancy rate for office spaces in Q1 of 2022 was reported as high as 17.5%. These headwinds pose significant risks to VNO and SLG, whose high yield does not compensate for the company's challenges. Even when a stock is discounted, lacking overall collective metrics, especially growth and profits, can result in lowered guidance and bad performance. Consider avoiding stocks with high yield and high risk.

Conclusion

Investors want the best stocks when markets rise or fall, and buying high-yield stocks should allow them to thrive in both environments. Be on alert for dividend stocks with high yields that also are high risk . Just because a stock pays dividends does not mean it will not sacrifice quality and growth. Each of my three stock picks is at high risk of performing poorly.

Possessing characteristics historically associated with poor future stock performance, NWL, SLG, and VNO have poor one-year price performance with negative double digits. Their growth and profitability metrics are dismal, and professional analysts are handily revising down on EPS revisions. Where the yields for these stocks should provide investors with a steady income stream, they're risky options in a highly volatile market. If yield is what you want, consider our Top Yield Monsters , "strong buy-rated" or our Top Dividend Stocks , which possess strong dividend safety grades and scorecards. Stocks with great dividend yields and excellent cash for operations help to ensure these stocks remain upward.

For further details see:

High Yield Means High Risk: 3 Stocks With Serious Warning Signs