LNC - High Yielding Lincoln National Corporation Looks Favorable Now

2023-04-24 08:15:17 ET

Summary

- 2022 was a rough year for LNC, with unrealized losses impacting the balance sheet and insurance adjustments impacting the P/L.

- 2023 looks to be a "show-me" year, as management seeks to bolster the balance sheet and continue the cost reduction initiative to improve profitability.

- LNC has historically been very generous with the dividends; it is expected that this generosity will continue throughout 2023, with share repurchases remaining paused for the next year.

One company whose stock has fallen on hard times in recent years but is staged for a strong comeback is Lincoln National ( LNC ). LNC, a holding company, through its subsidiaries and businesses, offers life insurance and retirement services to individuals and businesses. With roots going back to 1905 in Fort Wayne, Indiana, the company today operates with four segments : Life Insurance, Annuities, Group Protection and Retirement Plan Services. The Life Insurance segment provides a variety of life insurance products, including term life, single and survivorship versions of indexed universal life insurance, and variable universal life insurance products. The Annuities segment offers variable annuities, fixed annuities and indexed variable annuities. Group Protection provides group non-medical insurance products and services, such as disability, absence management services, term life, dental, vision, accident, illness and hospital indemnity benefits and services to the employer marketplace. Finally, the Retirement Plan Services segment provides employers with a variety of retirement plan products and services, primarily within the defined contribution retirement plan marketplace.

As we will see, the company is battling through a rising interest rate environment, which has put pressure on the financials and the stock price. However, the company has a solid business plan, including a cost reduction initiative, and has been able to increase top line revenues through difficult periods in the past. Investors who are looking for a strong dividend payer and have a longer time horizon may want to check out LNC for their portfolios.

As always, we have to look at where we are to see where we are going. 2022 was a challenging year for the company as it recorded a net loss for the first time since the peak of the financial crisis in 2009. Additionally, revenues declined 2.3% to $18.8 billion, the first decline since 2016.

The decline in revenue was led by a 12% drop in fee income and a 10% drop in net investment income. The fee income declines were led by unlocking within the Life Insurance segment and lower daily variable account values in the Annuities and Retirement Plan Services segments. The net investment income declines were due to lower investment income on alternative investments in the Life Insurance, Group Protection and Retirement Plan Services segments. The company did report strong 8% growth in insurance premiums throughout the businesses.

Expenses increased 23%, which does seem bad, but upon a closer examination, we can see that the Benefits increased 47%, mostly from the Life Insurance segment. Most of this was due to unlocking of secondary guarantee life insurance product reserves.

These reserves are affected by changes in expected future trends of assessments and benefits causing unlocking adjustments to these liabilities.

The other major expense categories, interest credited and commissions, both showed declines of 1.5% and 12%, respectively, from the prior year. I mentioned above the company’s initiative to reduce costs. In late 2021 , the company announced its “Spark Initiative”, which is an expense saving initiative originally designed to generate net recurring benefits of $260 - $300 million annually beginning in 2025. During 2022, the company recognized benefits of $22 million (pre-tax), while in 2023, the company is expecting benefits of $60 - $100 million (pre-tax). The company is still expecting annual benefits of $260 million - $300 million by the end of 2024, which will provide a nice boost to the company’s bottom line should the benefits prevail over the next 18 - 24 months.

Bottom line for 2022, the company lost over $2 billion, or $13.10 per share.

However, on the bright side, the company increased its dividend, yet again, by 5.3% to $1.80 per share.

Management has noted a commitment to the dividend, but the stock repurchases are on hold until they achieve their goal of improving their Risk Based Capital (more on this later).

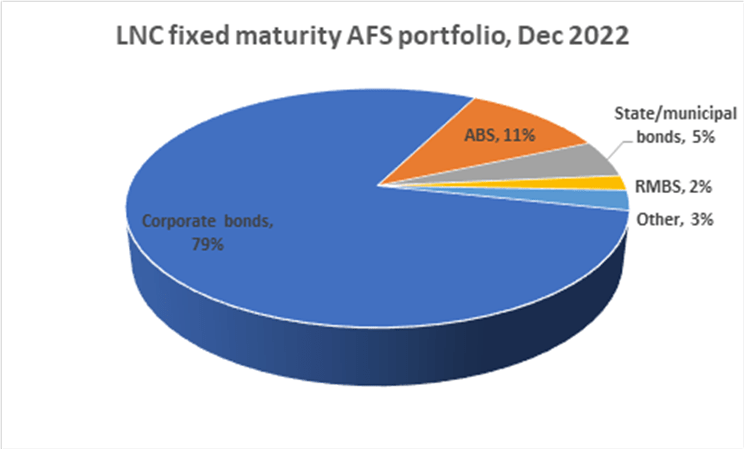

Turning to the balance sheet, we can see some risk, which is another reason why the stock is in the financial penalty box. Total assets shrank 13% from the prior year, mostly due to a 14% decline in available-for-sale (AFS) securities. AFS is comprised of fixed maturity available for sale securities, mortgage loans on real estate, derivatives, equities and other investments.

The $100 billion portfolio is comprised primarily of corporate bonds, asset-backed securities and state/municipal bonds:

{kind=link}

The company reported $13 billion in unrealized losses during the year, mostly from the corporate bond sector. The company did not require an impairment recognized in earnings because they do not intend to sell them, it is more likely than not that they will not have to sell them and the decline in fair value is due to something other than credit loss (i.e. rising interest rates and widening credit spreads). The company expects to recover the entire amortized cost of each security. Additionally, 96% of the fair value of the corporate bond portfolio is rated investment grade.

The next big chunk of unrealized losses, about $1.5 billion, came from the mortgage-backed and asset-backed securities. Losses were primarily because of rising interest rates and widening credit spreads. The company is expected to recover the entire amortized costs of these bonds as well.

The value of the trading securities portfolio declined from $4.5 billion to $3.5 billion during the year. Again, the largest drop was due to corporate bonds, which fell from $2.7 billion to $2.2 billion. The company did recognize a trading loss of $632 million during the year, which was significantly worse than the $51 million loss recognized in 2021.

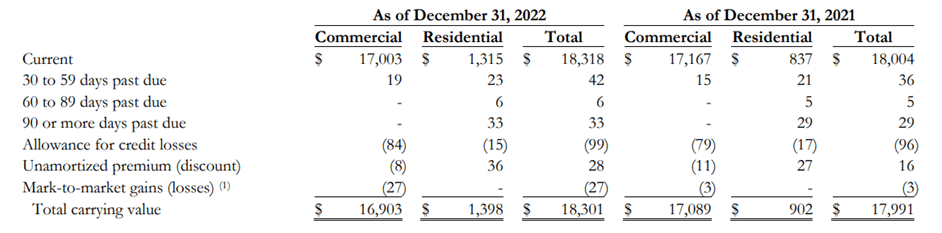

The company holds a fairly significant mortgage loan portfolio, $18 billion at the end of 2022, or 5.5% of total assets. Commercial mortgages of $17 billion, represented 5% of total assets.

{kind=link}

As you can see in the table above, the vast majority of the mortgages are current, with very little past due, and the allowance for credit losses not much different from the previous year. Most of the commercial loans are based in California and Texas, about 36% of total commercial loans. The residential loans are focused on California and New Jersey, about 29% of total residential loans. $34 million of commercial loans were nonperforming at the end of 2022, compared to $30 million at the end of 2021. Commercial real estate is becoming more of a concern to investors. While the working world seems to be getting back to normal pre-Covid conditions, many office buildings remain unfilled or partially filled as employers continue to allow for remote work environments. Furthermore, in some sectors such as tech, layoffs are continuing, putting further pressure on office vacancy rates. Finally, with the banking fiasco of March, it appears that available credit for commercial real estate may be tightening, which would put further strain on this sector. This is an area of concern, but for now, it appears that this sector within the LNC portfolio looks okay.

Looking at the liabilities, excluding the separate account liabilities (which are offset with separate account assets), total liabilities were up slightly. The Other Contract Holder Funds category increased slightly. This represents

account values on Universal Life and Variable UL insurance and investment-type annuity products where account values are equal to deposits plus interest credited less withdrawals, charges and other fees.

During the third quarter of each year, the company conducts its comprehensive review of these assumptions and models to determine if any adjustments are warranted.

Finally, we get to shareholders' equity. Total shareholders’ equity declined to just $4.1 billion ($4.6 billion in the chart) from $20.3 billion at the end of 2021.

The main culprit here? Accumulated Other Comprehensive Income, which declined from $6.4 billion at the end of 2021 to negative $7.7 billion at the end of 2022. The unrealized losses, many of which were described above, are the cause of the major decline in AOCI.

The company was expected to end the year with a risk-based capital ((RBC)) ratio of approximately 383%. The company has established a goal of increasing the RBC to 400%, a level at which management believes to be adequate and sustainable. The company has already taken some steps towards that goal, including the issuance of $1 billion in preferred stock in November 2022. Additionally, the company has paused its share repurchases through at least 2023, and executed a partial hedge on variable universal life insurance products. The company also reported that in the first quarter of 2023, the plan was to reduce the amount of capital supporting new business, with an increased focus on maximizing the return on this capital. Management remains committed to the dividend, however, as explained during the 4 th quarter earnings call :

Just as a reminder, the dividend is under the Board's purview, and we're not going to get ahead of the Board here, but we remain committed to returning capital to shareholders by way of the dividend.

Interesting caveat by the CEO, Ellen Cooper, about the dividend being under the Board’s purview. True, of course, but an interesting comment nonetheless. However, I have to believe that the company will remain committed to the dividend. Furthermore, the company has paused its share repurchases as they rebuild the risk-based capital. Once the company achieves that goal, it would appear that share repurchases would be back on the table.

So what does all this mean for the stock and its viability as an investment? Well, investing comes with risks and the most successful investments are made when the company is on the verge of a rebound in company fortunes and stock sentiment. I think this is one of those situations where the low stock price is the result of a company that has been beaten up, but better days are ahead. The stock has been a terrible investment over the past decade, trading at a recent price of $20.96. It has been as high as $83 back in 2017, with another spike into the $70s during the bull market run in 2021. But, after both occasions, it has lost all those gains and has not been able to gain any traction.

Compared to its peers over the past year, LNC has underperformed by a large margin:

It has been a challenging environment for life insurance companies. The interest rate backdrop certainly has not been favorable:

Rising interest rates have wreaked havoc on the bond portfolios of these companies, particularly LNC. The good news, so far, is the company is taking steps to shore up its capital base. Also, interest rates have retreated from their recent peaks back in March prior to the bank crisis. It is my expectation that the company will report less losses in the first quarter report.

Insurance companies are best looked at through the lens of book value. We can see that book values across the sector have declined in recent months:

The major declines in book value per share began around the same time that interest rates started going up in early 2022. Looking at price to book value, we can see that the premium paid for book value across the sector has declined this year. LNC is trading at about book value.

Lastly, I mentioned above that the dividend appears to be safe for now. The company increased its dividend per share for each of the past 10 years:

The current dividend yield is, not surprisingly given the low share price, quite attractive. If you get rid of the spikes in dividend yield during 2020 and currently, the average dividend yield is really closer to the 2.4% - 3.6% range. At the current dividend, a yield in that range results in a stock price of $50 - $75 per share. That seems aggressive, but it does show the potential for this stock if things start clicking with the company. By comparison, here are the current yields on the peer group:

Really, LNC had an average dividend yield until early this year, when it really popped with the drop in share price. The average among the peer group is about 4%.

Based on the above and my other valuation techniques, I actually think the stock is appropriately priced. 2023 is going to be a "show-me" year for management. I think if they can prove that their expense reduction plan is working, solidify their capital base, and generate some investment gains on their portfolio, all while maintaining the dividend payment, investors will be rewarded. If 2023 ends on a strong note, the company could start entertaining the idea of resuming share repurchases later in 2024, which will provide an additional tailwind for the stock. At these levels, I think a lot of the bad news has been priced in. The interest rate environment appears to be stabilizing, for now. The dividend is very attractive at these levels, with the hope that it can become more in-line with the industry levels. If so, that would provide a great deal of capital appreciation for the stock. Investors who are looking for yield and a relatively safe dividend, finding a spot in your portfolio for LNC stock might be a good move.

For further details see:

High Yielding Lincoln National Corporation Looks Favorable Now