HFRO - Highland Income Fund: This Controversial CEF Has Become More Shareholder-Friendly

2023-05-30 05:01:23 ET

Summary

- HFRO pays an attractive distribution yield and currently trades at more than a 30% discount to NAV.

- HFRO has been quite controversial in the past, but a new $100 million share repurchase program and reduced expense ratios are more shareholder-friendly.

- The HFRO litigation with Credit Suisse is still ongoing, but it appears the settlement received (if any) will be smaller than originally expected.

- HFRO has announced a name change to Highland Opportunities and Income Fund to reflect the new investment objective to pursue the growth of capital along with income.

Highland Income Logo (Highland fund web site)

(Data below is sourced from the Highland Income Fund website unless otherwise stated.)

Fund History

( HFRO ) is an eclectic closed end fund that invests in a diverse set of asset classes: real estate, CLOs, equity, fixed and floating rate loans.

The fund is quite controversial. It was originally an open-end mutual fund (HFROX) that invested in floating rate loans. In 2017, when it appeared that the fund could win a large award from the Credit Suisse law suit, the fund started to attract a lot of inflows and management got shareholder approval to convert the open-end mutual fund into a closed-end fund- ((HFRO)).

The fund now owns a more eclectic set of assets with a large allocation to real estate investments.

Investment Approach

- The primary objective has been to provide a high level of current income, consistent with preservation of capital. But this will be changing to also include capital growth.

- The fund uses effective leverage of about 13%, but that varies over time based on market conditions.

- Invests at least 25% in assets directly or indirectly secured by real estate.

- Focuses on real estate securities, floating rate securities, secured and unsecured fixed-rate loans and corporate bonds, mezzanine securities, structured products, convertible and preferred securities and equities (public and private)

Some Recent Developments Since My Last HFRO Article

Here is a link to my last HFRO article back in October 2022:

HFRO CEF: An NAV Pop From Credit Suisse Litigation

Some updates since then are:

1) May 16, 2023- HFRO's board approved a sizable share repurchase program. The fund may repurchase up to $100 million in open market transactions over a two year period. This represents around 11% of NAV, and a whopping 16% of market cap.

HFRO currently pays a 10.36% annual distribution yield. If you split the $100 million share repurchases over the next two years, HFRO will return about 8% a year from the share repurchases. So the total returned to shareholders (including the share buybacks) over the next two years will average around 18% a year.

2) May 16, 2023- The HFRO board also approved modifications to the fund's investment objective. Under the modified objective, The Fund will pursue growth of capital along with income. This expands the fund's universe of opportunities. The fund will change its name to "Highland Opportunities and income Fund" to reflect the new investment objective.

3) Update on the Credit Suisse litigation

On February 14, 2023, the Texas Court of Appeals reduced the award to Highland by about $23 million for part of its claim. This was the conclusion of the judge from the legal document:

"In accordance with this Court's opinion of this date, the trial court's award of $23,235,910.61 for appellee Claymore Holdings, LLC's secondary market purchases is REVERSED and judgment is RENDERED that appellee Claymore Holdings, LLC take nothing on its claim.

We REVERSE and REMAND to the trial court for further consideration of prejudgment interest in light of the Court's opinion."

On March 27, 2023, the fund announced an update on the lawsuit. The fund will eventually be providing an estimate of the award (if any):

"On February 14, 2023 the court of appeals issued a ruling related to the damages in the case against Credit Suisse. Right now, we are analyzing opinion and conducting a calculation based on such analysis to determine the remaining value, if any, of the award to the funds. We anticipate providing an update here when this process is complete."

The total aggregate award will consist of damages and prejudgment interest. The award will continue to accrue interest until the appeals process is exhausted. Any final judgment amount would be reduced by attorney fees and other litigation-related expenses.

The net proceeds would then be allocated to two funds based on respective damages (approximately 82% to HFRO and 18% to NXDT).

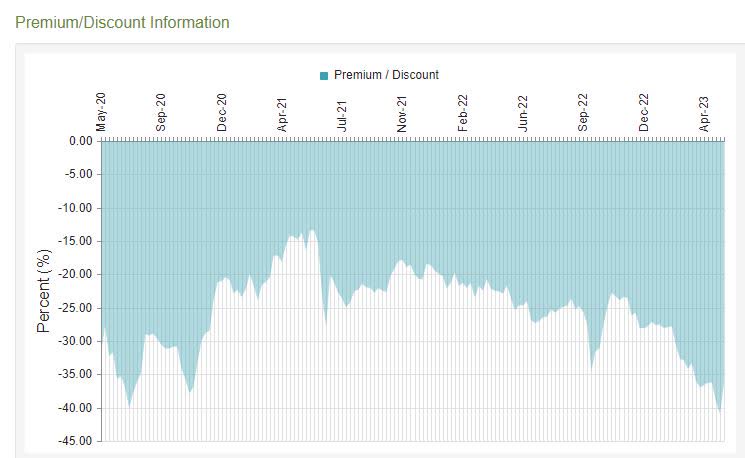

Three Year Discount History for HFRO

{kind=link}

HFRO Three Year Discount History (cefconnect)

Here is the asset allocation breakdown as of March 31, 2023:

Portfolio Allocation Breakdown

| Equity |

| 9.4% |

| Real Estate |

| 71.4% |

| CLOs |

| 6.3% |

| Loans |

| 5.5% |

| Other |

| 7.5% |

Source: HFRO Fund Fact Sheet Q1 2023

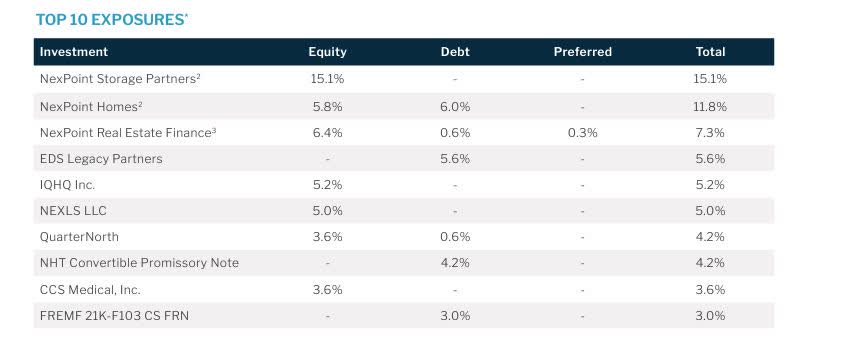

Portfolio- Top 10 Holdings (as of March 31, 2023)

{kind=link}

HFRO Top 10 Holdings (Highland Fund web site)

The Expense Ratio Has been Coming Down

HFRO has a bad reputation with many investors for various reasons, but in some ways the fund has become more shareholder friendly. Along with the share buybacks, I have also noticed a steady decrease in the fund's expense ratio over the last four years. Here are the net investment income and gross operating expenses reported for the last four years as a percentage of net assets.

HFRO: Net investment income and Gross operating expenses

| Year |

| Net investment income |

| Gross operating expenses |

| 2019 |

| 5.93% |

| 3.39% |

| 2020 |

| 4.22% |

| 2.68% |

| 2021 |

| 5.26% |

| 1.67% |

| 2022 |

| 8.98% |

| 1.32% |

Trading Opportunities in HFRO

I have owned a core position in HFRO for several years. But because of big swings in its discount, it has provided some good trading opportunities to add some shares when there is a quick downward move in the price, or to trim some shares when the stock bounces up rapidly. Consider this table of price/discounts for the recent period starting from May 1, 2023:

{kind=link}

HFRO Price/Discount History (cefconnect)

Note that HFRO reached a discount level of 40.21% on May 10, and the discount expanded even further to over 42% on May 11 and stayed above 40% on May 12. This provided a great buying opportunity for active traders who follow the fund closely.

On May 16, HFRO announced their large $100 million share repurchase program, and the discount decreased to around 37%. Then on May 24, there was a bullish article on HFRO from the widely read Contrarian Outlook newsletter which caused another spike in the price and drove the discount down to the current level of around 33%. If you purchased shares during the May 10-May 12 period, you would now have the opportunity to trim a few shares and take some profits off the table.

Fund Performance

The NAV performance of HFRO has been good since 2018 on a relative basis compared to its Morningstar Bank Loan fund peers, but it has been lagging somewhat in 2023 on a year-to-date basis. Now that the Fund's investment objective has formally changed, I would expect Morningstar to assign HFRO to a different fund category in the near future.

Here is the year-by-year total return performance record since 2018 when the fund converted to the closed-end fund format:

| HFRO NAV Performance |

| HFRO Market Performance |

| Bank Loan NAV Performance |

| Rank in Category ((NAV)) |

| 2018 |

| +1.53% |

| -12.15% |

| - 0.47% |

| 7 |

| 2019 |

| +1.48% |

| +4.20% |

| +8.82% |

| 94 |

| 2020 |

| +4.36% |

| -8.38% |

| - 1.26% |

| 1 |

| 2021 |

| 14.76% |

| +16.35% |

| +12.29% |

| 16 |

| 2022 |

| 6.66% |

| + 1.69% |

| - 7.20% |

| 1 |

| YTD |

| - 3.99% |

| -7.53% |

| + 3.64% |

| 100 |

Three Year Annualized Fund Performance

| HFRO Price |

| +14.43% |

| HFRO NAV |

| +10.61% |

| Bank Loan NAV |

| + 8.25% |

Source: Morningstar

Alpha is Generated by High Discount + High Distributions

A good reason to invest in HFRO now is the potential to capture "alpha" from the high discount, NAV boosts from the share repurchases and the potential for an NAV boost from the Credit Suisse litigation proceeds.

The distribution rate of 10.36% along with the 33.2% discount allows investors to capture some alpha by recovering a portion of the discount whenever a distribution is paid out.

When you recover NAV from a fund selling at a 33.2% discount, the percentage gain is 1.00/ 0.668 or about 49.7%. So the alpha generated by the 10.36% distribution is computed as:

(0.1036)*(0.497)=0.0515 or about 5.15% a year.

Note that this is way more than the 1.32% baseline expense ratio.

Potential For Activist Activity

Institutions hold about 36% of the shares.

Here are some opportunistic investors that owned shares in HFRO as of March 31, 2023.

Activist #shares

Thomas J. Herzfeld 2,936,570

Atlas Private Wealth 940,076

Bulldog Investors, LLP 451,627

Advisor Group Holdings 399,688

Matisse Capital 140,000

Highland Income Fund ((HFRO))

- Total investment exposure: $1,050 Million

- Total Common assets: $910 Million

- Annual Distribution (Market) Yield= 10.36%

- Last Regular Quarterly Distribution= $0.077 (Annual= $0.924)

- Fund Baseline Expense ratio: 1.32%

- Discount to NAV= -33.23%

- Effective Leverage: 13.3%

- Average 3 Month Daily Volume (shares)= 250,000 (Source: Yahoo Finance)

- Average Daily Dollar Trading Volume = $2,280,000

HFRO is a fairly liquid stock and usually trades with a bid-asked spread of one or two cents. But when the market gets slow, the spread can widen to four cents or higher. There is often limited size available on both the bid and asked. I would recommend using multiple smaller size orders to accumulate a position. When you use a market order, you will usually get some price improvement and receive a price somewhere between the bid and the asked price.

I believe that HFRO is at a decent level for a starting purchase now at a 33% discount. I would get more aggressive if/when the discount ever gets back above 36%.

If HFRO receives an award from the Credit Suisse lawsuit, there could be a small "pop" in the NAV.

Even if HFRO ultimately loses the Credit Suisse lawsuit and is awarded nothing, I feel the current 33% discount, high distribution yield, and future share buybacks by management make the fund a decent buy now.

For further details see:

Highland Income Fund: This Controversial CEF Has Become More Shareholder-Friendly