HPK - HighPeak Energy May Have To Reduce Its 2023 Development Plans

2023-05-03 22:38:30 ET

Summary

- HighPeak Energy is projected to burn $331 million during 2023 at current $70 WTI oil strip.

- This would leave it with limited or no liquidity depending on how much its borrowing base is increased.

- Thus HighPeak will need to trim its development plans if oil remains near current levels, or otherwise do an equity raise.

- While HighPeak's leverage does not look exceptionally high, it does have all its debt maturing in 2024 at the moment.

- HighPeak's credit facility debt may also mature in October 2023 if it does not refinance its February 2024 notes by then.

HighPeak Energy's ( HPK ) attempts to rapidly grow production may be hindered by relatively weak oil prices. HighPeak's growth strategy could work well at $90 WTI oil, but at $70 WTI oil it may end up with around $331 million in cash burn in 2023 if it continues with its original 2023 development plans.

HighPeak also has some near-term debt concerns, with all of its debt currently maturing in 2024 and its credit facility maturity moving up to October 2023 if its February 2024 notes aren't refinanced by then.

I estimate HighPeak's value at $18 per share if it can successfully carry out its 2023 development plans. However, I am neutral on HPK stock due to its debt maturity risks as well as the potential for substantial dilution to help pay off some of its debt.

2023 Results At $70 WTI Oil

HighPeak now expects to average approximately 50,000 BOEPD during 2023 at its guidance midpoint and is aiming for an exit production rate of 58,000 BOEPD to 66,000 BOEPD. HighPeak's Q4 2022 production was 85% oil, but its proved reserves are 80% oil and its PDP reserves are 77% oil.

I am modeling HighPeak's 2023 production at 82% oil, 10.5% NGLs and 7.5% natural gas, with an average of 50,000 BOEPD.

At current strip of $70 WTI oil, HighPeak is projected to generate $1.123 billion in revenues after hedges.

| Type |

| Barrels/Mcf |

| $ Per Barrel/Mcf |

| $ Million |

| Oil |

| 14,965,000 |

| $71.00 |

| $1,063 |

| NGLs |

| 1,916,250 |

| $27.00 |

| $52 |

| Natural Gas |

| 8,212,500 |

| $1.95 |

| $16 |

| Hedge Value |

| -$8 |

| Total |

| $1,123 |

HighPeak expects to average four to five drilling rigs during 2023, along with two to three frac crews. This is expected to result in approximately $1.205 billion in capex, which accounts for most of HighPeak's costs.

| Expenses |

| $ Million |

| Lease Operating Expense |

| $100 |

| Production And Ad Valorem Taxes |

| $62 |

| Cash G&A |

| $12 |

| Cash Interest |

| $75 |

| Capital Expenditures |

| $1,205 |

| Total Expenditures |

| $1,454 |

HighPeak's cash burn is now projected to reach $331 million in 2023 based on its guidance and current strip of $70 WTI oil.

Debt Situation

HighPeak ended 2022 with around $714 million in net debt, including $475 million in notes due 2024 ($225 million in February 2024 and $250 million in November 2024) and $270 million in credit facility debt. HighPeak also had $31 million in cash on hand at the end of 2022.

HighPeak's projected 2023 cash burn would get it to $1.056 billion in net debt by the end of 2023, including its current dividend payments. This is leverage of 1.1x, which isn't unreasonably high in itself. However, HighPeak's credit facility may be more of a limitation. The borrowing base for that facility was $550 million at the end of 2022, while there were aggregate elected commitments of $525 million.

HighPeak's projected year-end 2023 credit facility borrowings are around $581 million, which exceeds its current borrowing base. Thus at $70 WTI oil, HighPeak will either need another borrowing base increase (along with an increase in aggregate elected commitments) to fund its full 2023 development plans.

HighPeak also has potential issues with near-term debt maturities. All of HighPeak's debt currently matures in 2024. HighPeak's credit facility has a springing maturity that results in the credit facility maturity date moving up to October 2023 if the February 2024 notes aren't repaid/refinanced by then.

Notes On Valuation

I now value HighPeak at approximately $18 per share in a long-term $75 WTI oil and $3.75 NYMEX gas scenario. This is based on a 3.0x EV to EBITDAX multiple less its projected year-end 2023 net debt. It also has 8.3 million outstanding warrants with an exercise price of $11.50 that are factored into this calculation. This assumes that HighPeak can meet its guidance for 2023 though and complete its original development plans.

HighPeak has mentioned potentially growing production by a further 46% in 2024 with a 25% capex reduction compared to 2023. However, I believe that there is significant risk that HighPeak doesn't achieve its 2024 targets. HighPeak badly missed on its May 2022 guidance numbers. HighPeak's 2023 guidance looks generally achievable, but I am skeptical about its ability to reach its 2024 targets.

Notes On Inventory

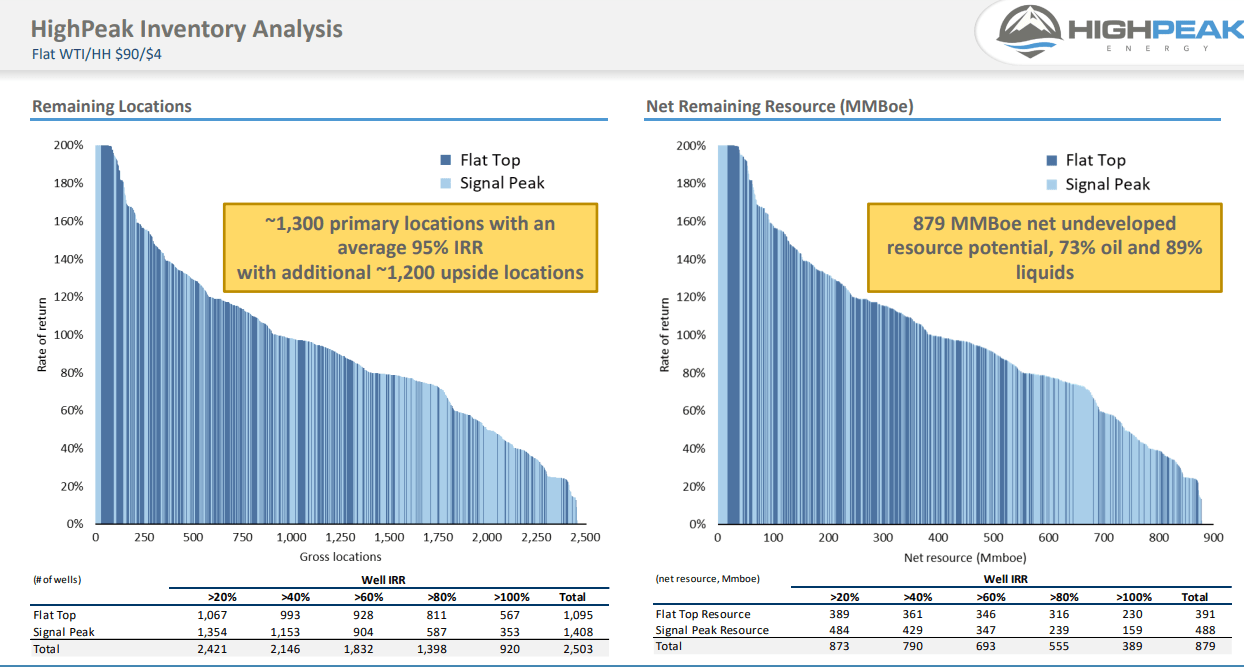

HighPeak claims that it has around 18 years of potential locations based on its 2023 development pace of turning approximately 140 wells to sales. However its inventory analysis is based on $90 WTI oil, which is a very aggressive price to use. I would like to see it report estimated IRRs based on $70 or $75 WTI oil instead.

{kind=link}

As well, HighPeak has focused development on the western portion of its Flat Top acreage. There is additional development risk towards the eastern part of its position there.

Conclusion

HighPeak is now projected to end up with $331 million in cash burn in 2023 at current strip of $70 WTI oil if it sticks to its original development plans. This would put it at risk of fully utilizing its credit facility borrowing capacity. HighPeak's credit facility may also mature in October 2023 if it doesn't deal with its February 2024 notes by then.

If HighPeak can navigate its debt maturities and successfully complete its original 2023 development plans, its stock may have a modest amount of upside from current levels. However, due to the debt risks and the significant possibility of HighPeak needing to do an equity raise and/or reduce its development plans, I am neutral on HighPeak at its current share price.

For further details see:

HighPeak Energy May Have To Reduce Its 2023 Development Plans