HLMN - Hillman Solutions: Disappointing Quarterly Results

2023-08-21 11:58:29 ET

Summary

- HLMN announced Q2 FY23 results with a decline in net sales and net income.

- The company's performance was disappointing due to underperformance in robotics and its digital solutions and protective solutions business.

- HLMN's current share price is down from its IPO price, and technical analysis suggests a bearish trend. I believe the stock is overvalued and not backed by strong growth.

Hillman Solutions Corp. ( HLMN ) offers hardware-related products worldwide. It recently announced its Q2 FY23 results. I will review its quarterly results in this report. I think it is currently overvalued, and its growth rate doesn't justify its high valuation. Hence I assign a hold rating on HLMN.

Financial Analysis

HLMN recently announced its Q2 FY23 results . The net sales for Q2 FY23 were $380 million, a decline of 3.5% compared to Q2 FY23. I think underperformance in its robotics and digital solutions and protective solutions business was the major reason behind the revenue decline. The revenue from the robotics and digital solutions business declined by 2% in Q2 FY23 compared to Q2 FY22. I believe a decline in manual key duplication sales was the main reason behind the decline in RDS business sales. The revenues from the protective solutions business declined by 17% in Q2 FY23 compared to Q2 FY22. I think the major reason behind the decline was lower foot traffic. Its adjusted gross margins in Q2 FY23 declined by 110 basis points. The company cleared off a significant percentage of the high-cost inventory from the previous year in Q2 FY23 which I think led to a decline in gross margins.

Seeking Alpha

Its net income also declined in Q2 FY23 by 48.5%. In FY22, the company had to face a lot of headwinds like supply chain constraints and labor issues, but in Q2 FY23, these challenges decreased, so in my view, the company's performance in Q2 FY23 was quite disappointing. In addition, the current steel prices are lower than what they were in FY22, so I believe it might affect its revenue growth in FY23. Hence I believe its FY23 revenue might be lower than FY22 revenue. In FY22, the company reported net sales of $1.49 billion, and the management expects its FY23 net sales to be around $1.5 billion. Hence the company expects stagnant revenue, and I believe this might adversely affect the company's share price in the coming quarters.

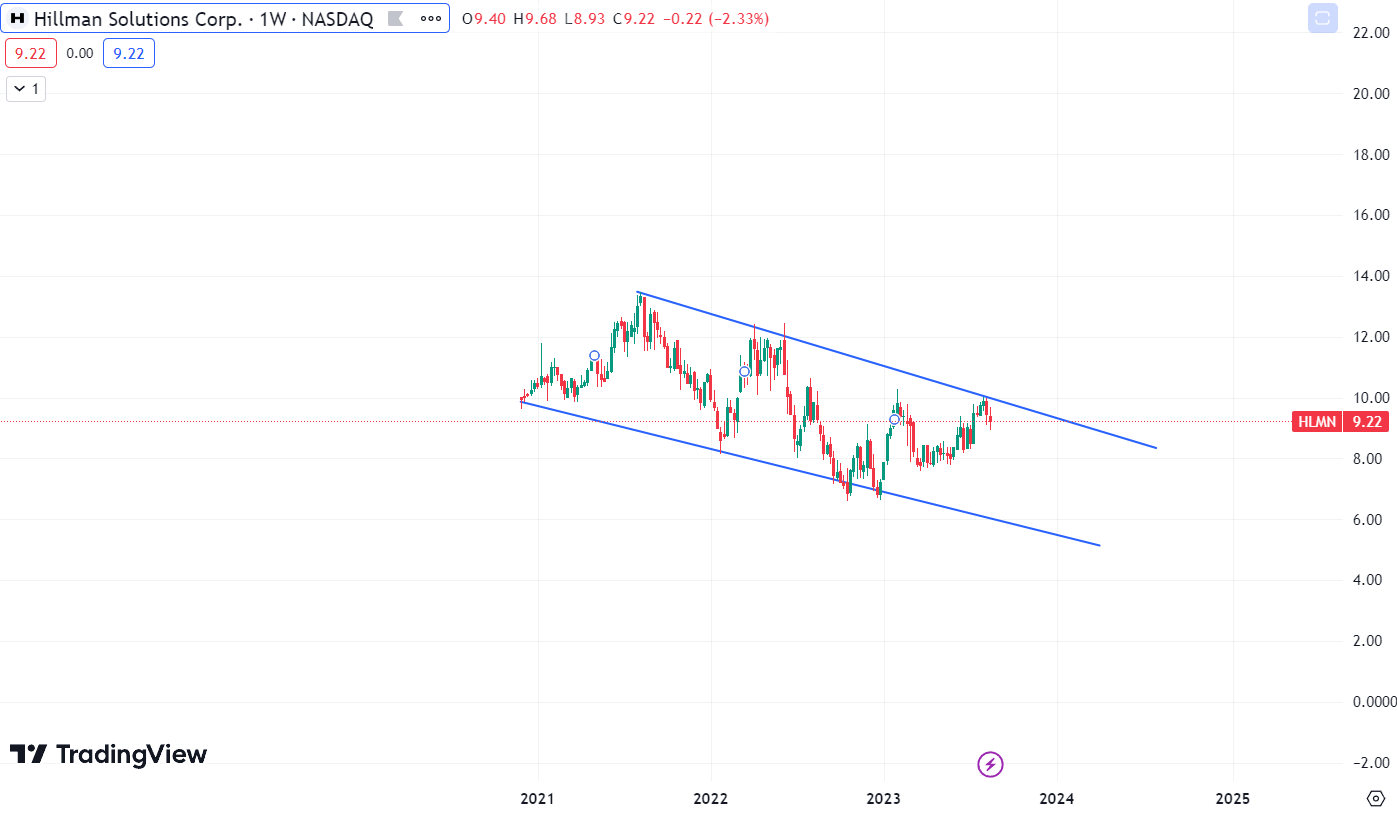

Technical Analysis

{kind=link}

HLMN is trading at the $9.2 level. Its current share price is down by 7.6% from its IPO price level. The company debuted in 2020, which means that this stock has failed to provide any returns to its investors in the last three years, and I highly doubt that it will provide any returns to the investors in the near term because the price action formed here is bearish. The stock has been stuck in a channel pattern since its IPO debut and has faithfully followed the pattern ever since. The current stock price is near the resistance line of the pattern, and recently after touching the resistance line, the stock formed a red candle which shows selling pressure is present in the stock, and I believe the stock might fall from the current level due to selling pressure. Hence I believe the price action that the stock has formed is quite bearish, and in my view, one should avoid buying it at the current level. There is a high chance that the stock might reach the support line, which is at $6.5, because that's what the stock has done in the past. After touching the resistance line, the stock has gone down to the support line.

Should One Invest In HLMN?

First, look at HLMN's valuation. HLMN has a P/E [TTM] ratio of 24.26x which is higher than the sector median of 16.85x. HLMN has an EV / EBITDA [TTM] ratio of 14.36x compared to the sector ratio of 11.88x. Currently, HLMN is trading at a premium valuation but looking at its growth rate; I think it doesn't deserve to trade at a higher valuation. Its quarterly result has been poor, and its future growth expectations aren't significant. Hence I believe HLMN is currently overvalued. Looking at its growth rate, I think it can trade around the P/E ratio of 17x, and its EPS [FWD] is $0.39. This gives us a share price of $6.6, which is way lower than its current share price. Hence based on its growth, I think it should trade lower than its current price level. Hence I would advise to avoid it because its quarterly results have been poor, and its future growth expectations show that the management expects close to no growth, so I think the high valuation is not backed by strong growth. In addition, its technical chart shows that we might see a fall in the share price. Hence I assign a hold rating on HLMN.

Risk

Steel, aluminum, and copper are just a few of the metals used to make their products. In addition, various resin-based, commodity-based components that are influenced by oil price changes are used in the production of LNS. They are susceptible to fluctuations in their underlying manufacturing costs and obtain the majority of their products from third parties. Additionally, they use third parties for transportation, exposing them to freight cost changes to move goods from their suppliers to distribution centers and then to customers. They are also affected by changes in the price of gasoline for the field sales and service force, as well as changes in the price of diesel fuel. Costs could significantly rise as a result of this cost inflation. Their financial health could be negatively impacted if they are unable to offset any cost increases brought on by the variables mentioned above through various customer price measures and cost-cutting activities. In contrast, if there is deflation, they can feel pressure from the public to lower prices. There can be no guarantee that they could lower their cost base (via discussions with suppliers or other actions) to counteract any such price concessions that could negatively affect their operations and cash flow.

Bottom Line

Their quarterly result has been disappointing, and the future growth expectation isn't significant. The steel prices are also lower, which might affect the company's sales in the coming quarters. Hence I believe it is best to avoid it for now because I think the stock might not be able to provide returns to the investors. In addition, its current valuation seems high. Hence I assign a hold rating on HLMN.

For further details see:

Hillman Solutions: Disappointing Quarterly Results