HTH - Hilltop Holdings: Growth And Sustainability On Top But Hold For Now

2023-05-20 03:50:15 ET

Summary

- Hilltop Holdings, Inc. maintained a robust performance in the face of market volatility.

- Its impeccable financial positioning remains one of its sturdy foundations.

- Market views are mixed, but macroeconomic improvements may continue.

- Dividends are enticing, given the consistent payouts and decent yields.

- The stock price keeps increasing, but the upside potential stays limited.

Hilltop Holdings, Inc. (HTH) operates in a highly volatile and cyclical market landscape. Interest rates remain elevated, affecting many banking operations. Despite this, HTH stays afloat with its prudent portfolio management. Its revenues and margins have expanded, leading to increased returns. Moreover, its stellar Balance Sheet shows excess capital and impressive liquidity levels. Indeed, its bank is the jewel of the crown. HTH must expand its banking segment outside Texas and improve its digital experience. That way, it can sustain or stimulate its growth potential.

Meanwhile, it remains an ideal stock due to its capital returns. Dividends and share repurchases are consistent and increasing. Likewise, the stock price stays in an uptrend. Investment returns are decent if we compare the stock price and company earnings. But we may have to wait for a better entry point as the current price shows limited upside potential.

Company Performance

It's been almost a year since I last covered Hilltop Holdings, Inc. At that time, macroeconomic volatility started to peak as inflation skyrocketed. The impact was most evident in interest-sensitive assets and liabilities. Today, it faces similar challenges, given the persistent interest rate hikes. But we can see improvements in its operations as it capitalizes on its prudence.

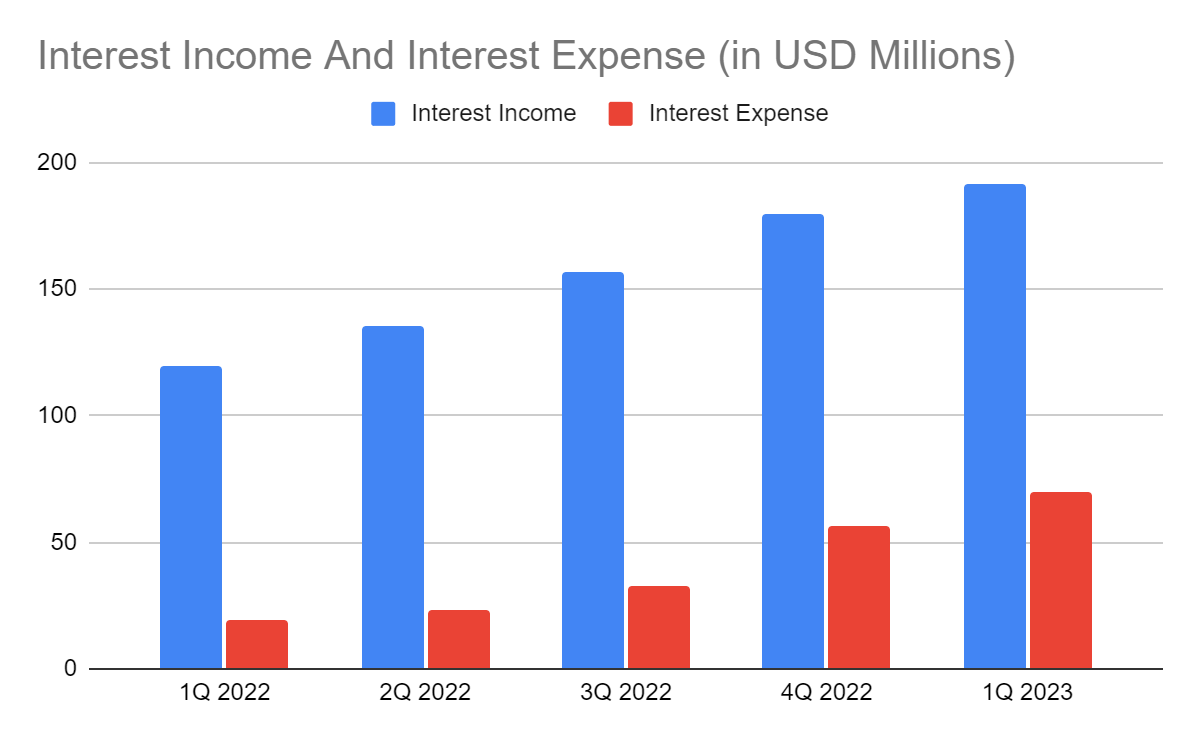

As a financial holding company, it offers various financial products and services. It operates in three segments namely Banking, Broker Dealer, and Mortgage Origination. With that, the primary revenue streams are the yields or interest income on loans and investments. In 1Q 2023, interest income reached $191.43 million , a 60% year-over-year increase. This massive increase was impeccable, given the intense macroeconomic headwinds.

Its banking segment remained the primary driving force as it benefited from higher interest rates. Loans remained the primary revenue component, comprising almost two-thirds of interest income. Aside from interest rate hikes, the company enjoyed its excellent loan quality. Its non-performing loans decreased from 0.33% to 0.30%. It showed increased collectibility of loans, which was impressive due to the risk of defaults and delinquencies. Even better, the composition of its loans was suitable in the high-interest environment. The commercial side of loans comprised 59% of the total loans. They were CRE and C&I loans. In essence, the loans had higher returns and better hedges against risks due to collateral. CRE loans may still be risky, given the massive changes in the real estate market. It also offered construction and residential loans. Yet, there are opportunities it can seize to expand its operations. We will discuss them further in the following section.

Interest Income And Interest Expense (MarketWatch)

{kind=link}

Investment securities also drove yield growth after increasing by 70%. They also comprised 25% of the total interest income, making them a primary component. Even better, 98% of them were government-backed securities. They were in the form of treasuries and municipal bonds. In general, these securities are suitable for the current market landscape. They are more inflation-linked, so they have better yields during interest rate hikes. They also have better hedges against potential valuation losses. As a whole, HTH continued to flourish, primarily due to its prudent portfolio diversification.

Meanwhile, the other two segments remained hammered. These were most evident in the lower non-interest income. Its mortgage production income and mortgage loan origination fees decreased by 64% and 12%. The thing is, the banking segment is the star of the business. Meanwhile, the two segments continue to hamper its growth potential. We can see it in historical averages as the two segments remained lower than pre-pandemic levels. From this perspective, HTH may have to refocus its core operations. It may have to focus on what it does best and know how to improve its weak points. Digital adaptation is also one of the things it must improve. If we compare it to the industry, the bank appears to be moving relatively slower. The company must improve on this part since it is crucial in increasing operational efficiency. It can also attract more demand for its services as more transactions go online. But overall, the core operations remained solid as the banking segment. Expanding outside Texas can be wise if it wants to capture more customers.

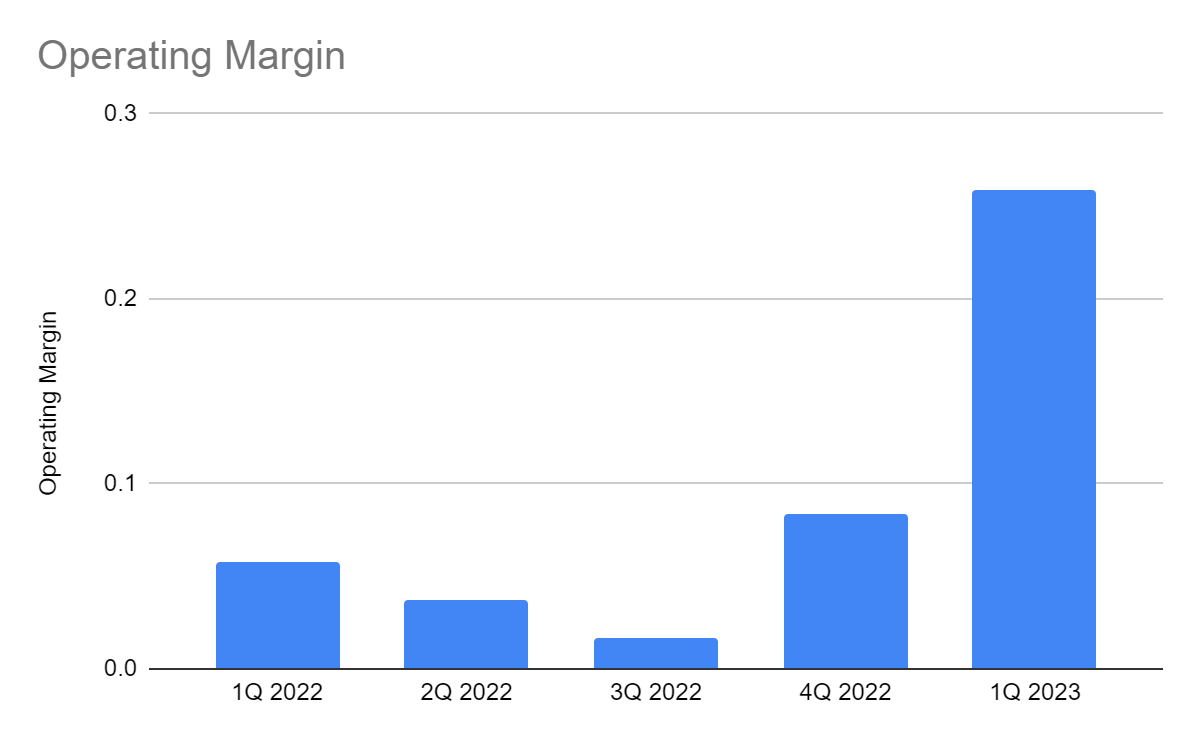

Interest expenses also increased this quarter. At $69.72, it more than tripled in only a year. Deposits were the main contributors as part of its core business. Despite this, the increase in interest income remained higher. Also, non-interest expenses remained flat at $232 million. The amount was also the lowest in five quarters. As such, the company was most efficient in 1Q 2023. It led to an operating margin of 26% versus 5% in 1Q 2022.

Operating Margin (MarketWatch)

{kind=link}

This year, Hilltop may face similar challenges as recession woes persist. But with efficient and prudent asset management, the company can stabilize its operations. Interest rates may remain a double-edged sword. Yet, the decreasing inflation can be a source of hope. We will discuss them further in the following section.

How Hilltop Holdings, Inc. May Remain Solid This Year

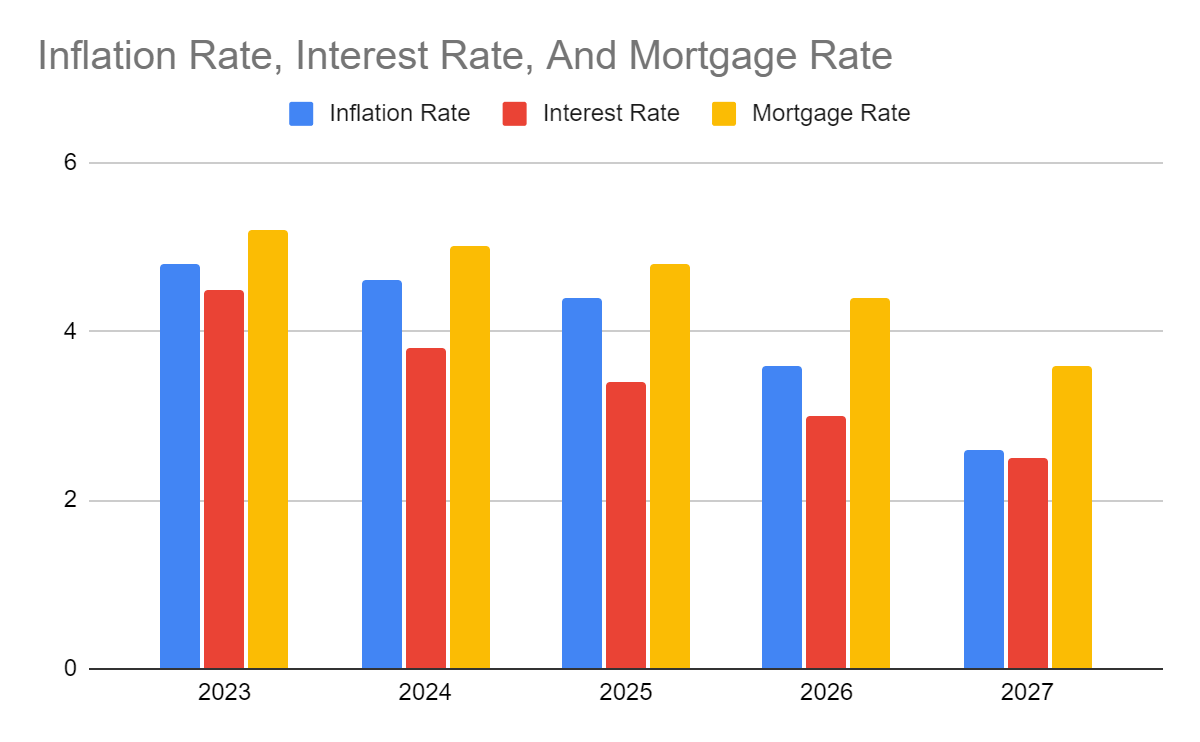

Hilltop Holdings, Inc. started the year strong with its robust performance. Even so, it must not be too complacent as recession fears seep into millions of households and businesses. Interest rates continue to increase and are now above 5%. While higher interest rates mean higher loan yields, defaults and delinquencies may become a problem. It can lead to higher credit loss provisions and reduce operating income. The consolation is that most of its loans are for commercial purposes. Also, interest rate increments are already flat at 25 bps for two consecutive quarters.

Despite this, there are opportunities the company can seize as inflation continues to relax. It shows that the strategy of The Fed continues to pay off. And if the downward pattern continues, interest rate hikes may continue to slow down in the second half. At 4.9% , inflation is 46% lower than the 9.1% peak in 2022. Its impact may not materialize anytime soon, but it can increase confidence among consumers, borrowers, and investors. Although lower inflation does not mean lower prices, stability may be seen in the long run.

Another factor to consider is the real estate market since it offers CRE, construction, and multifamily residential loans. The mortgage origination segment may be directly affected. Yet, the softer demand may not lead to a real estate market crash due to many reasons. First, the price increase in the market was driven by the demand influx, not cost-push factors like labor and building materials. Second, property shortages remain high. At the start of the year, the US was short of 6.5 million . But as of this writing, shortages are higher at 7.3 million housing units. It can be attributed to the lower median home prices in 1Q 2023. As such, home sales and loan demand increased for three consecutive months. It is no surprise analysts still expect a 5.4% increase in home prices this year. While the increase rate is lower than in 2022, price and mortgage stability. may improve.

Inflation Rate, Interest Rate, Mortgage Rate (Author Estimation)

{kind=link}

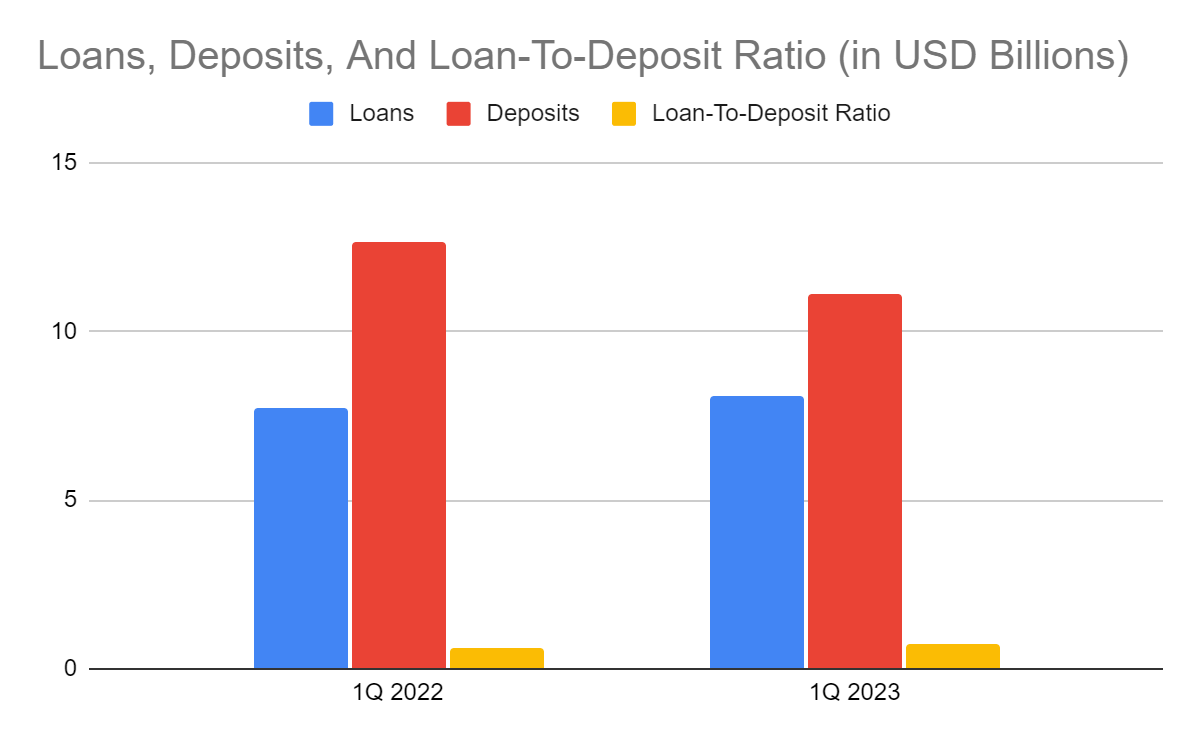

But what makes Hilltop a solid company is its impeccable financial positioning. Its high liquidity levels are demonstrated by its management of loans and deposits. Aside from prudent loan diversification, its conservative approach remained one of its core strengths. Organic loan growth and deposit inflows are evident, showing increased demand for customers and borrowers. More importantly, its loan-to-deposit ratio remains low at 73%. It is an impeccable aspect since it gives the company adequate reserves if there are defaults and delinquencies. The company can lend more to realize more loan yields and interest income.

Loans, Deposits, And Loan-To-Deposit Ratio (MarketWatch)

{kind=link}

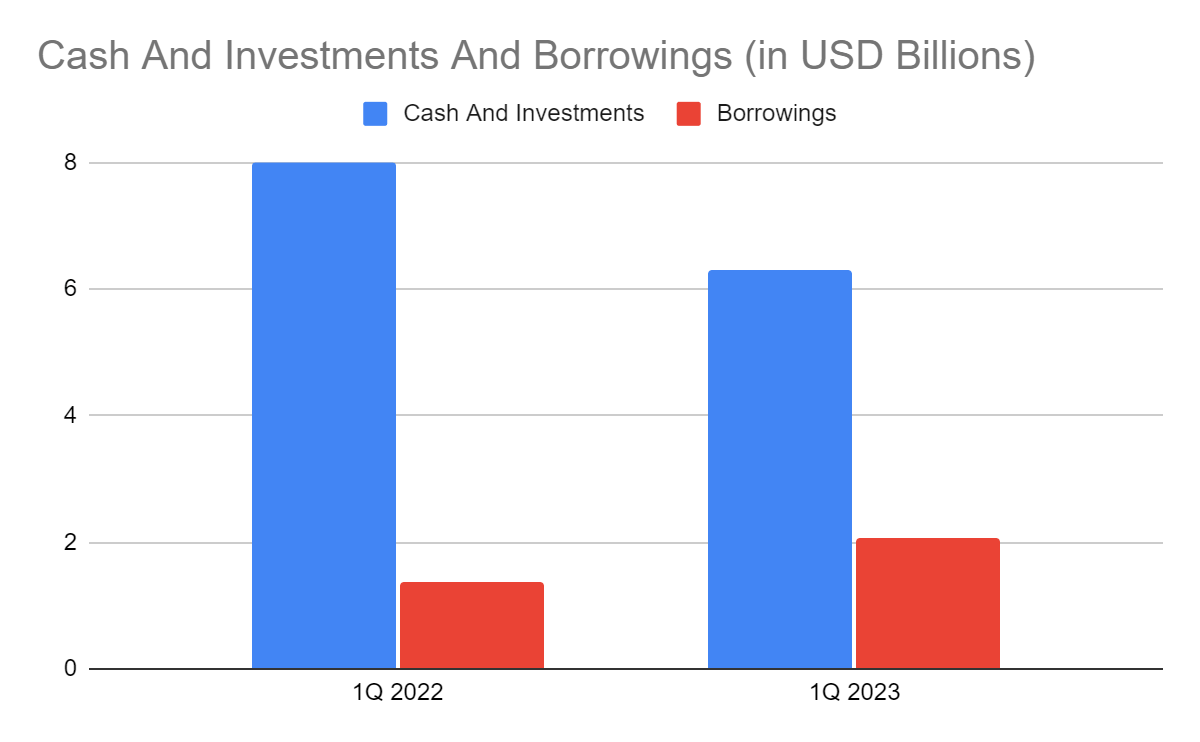

Moreover, its liquid assets remain high. Its cash levels remain high at $1.8 billion, or 11% of the total assets. Although it decreased by 41% from 1Q 2023, it can still cover borrowings with current maturities. Its average cash burn every month is $102,000. So without borrowings, share issuance, and income, cash can cover 18 months of operations. The thing is, HTH generates increasing income. If we combine cash with investments, their amount will be equivalent to 37% of the total assets. They can also cover all liabilities, excluding deposits. This aspect shows that the company continues to balance growth and viability with sustainability.

Cash And Investments And Borrowings (MarketWatch)

{kind=link}

Stock Price Assessment

The stock price of Hilltop Holdings, Inc. remains in an uptrend. There have been noticeable corrections in the past two years, but the rebound was substantial. At $30.99, the stock price is 5% higher than last year's value. It also increased by 29% from its 2022 dip. The stock stays on my watchlist, and it was a wise decision to buy shares at its lows. But given the current stock price, we must evaluate it with extra caution. We can use the PB Ratio with the current BVPS and PB Ratio of 32.05 and 0.98x. But if we use the current BVPS and the average PB Ratio of 0.95x, the target price will be $30.46. The stock price remains fairly valued but the upside potential is limited. It is also quite higher than the intrinsic value of the company.

But what I like about this stock is its decent capital returns. It continues to raise dividends with yields of 2.01%, higher than the S&P 600 average of 1.72%. Aside from the recent dividends of $16 per share, it repurchased shares for $4.5 million or $31.15 per share. Investment returns are also decent if we compare cumulative company retained earnings to the average change in stock price. Since 2019, the company has generated an EPS of $13.25, while it distributed dividends at $1.75 per share. With that, the company had cumulative retained earnings of $11.48. Meanwhile, the stock price increased by $12.91, leading to a $0.51 difference. It also means that for every $1 retained earnings, the stock price increased by $1.12. As such, the stock price increase remained reasonable relative to company earnings. To assess the stock price better, we will use the DCF Model.

FCFF $81,300,000

Cash $1,800,000,000

Borrowings 2,080,000,000

Perpetual Growth Rate 4.4%

WACC 9.2%

Common Shares Outstanding 65,023,000

Stock Price $30.99

Derived Value $29.97

The derived value adheres to the supposition of a potential overvaluation. There may be a 4% downside in the next 12-18 months. While its fundamentals are impressive, investors must be careful about buying shares at the current stock price.

Bottomline

Hilltop Holdings, Inc. remains a solid company with a solid business model. The banking segment remains its cornerstone amidst market volatility. Even better, it ensures sustainability with its impressive financial positioning and excess capital. Its adequacy allows it to cover its capital returns through dividends and share repurchases. Despite this, the stock price shows limited upside potential. It is just about the same as the intrinsic value of the company. So, I will have to wait for a better entry point before buying more shares. But keeping holdings in this company may be a wise decision. The recommendation, for now, is that Hilltop Holdings, Inc. is a hold.

For further details see:

Hilltop Holdings: Growth And Sustainability On Top, But Hold For Now