HGV - Hilton Grand Vacations Q2: Profit Peaks Potential Margin Squeeze

2023-08-06 22:52:59 ET

Summary

- Hilton Grand Vacations Inc. demonstrated a commendable recovery in Q2 with strong revenue and non-GAAP EPS, driven by its Financing and Club and Resort divisions.

- Challenges in sales efficiency, increasing sales expenses, and potential profit margin squeeze persist.

- HGV's performance lags behind the S&P 500 Index, making it advisable for investors to wait for clearer signs of sustainable growth before considering further investments.

Thesis

Hilton Grand Vacations Inc. (HGV) demonstrated a commendable recovery in Q2 showcased by non-GAAP EPS of $0.85 that beat by $0.01, and revenue of $1.01B that beat by $11.42M, driven by the strength of its Financing and Club and Resort divisions. However, caution is warranted as challenges in sales efficiency, increasing sales expenses, and potential profit margin squeezes persist. Although undervalued and experiencing steady operational profitability growth, HGV's performance lags behind the S&P 500 Index, making it advisable for investors to wait for clearer signs of sustainable growth before considering further investments.

Company Profile

Since its inception in 1992, Hilton Grand Vacations Inc. has established a prominent presence in the timeshare industry, operating under the respected Hilton Grand Vacations brand. Its strategic framework is divided into two fundamental sectors: Real Estate Sales and Financing, which markets and sells Vacation Ownership Interests (VOI) and offers financing and loan services, and Resort Operations and Club Management, which handles onsite management of timeshare properties and offers a broad array of services such as exchange, leisure travel, and reservations. With a commitment to versatile operation and customer satisfaction, this model enables the company to effectively cater to diverse aspects of the timeshare experience.

Hilton Grand Vacations Q2 Earnings Highlights

As Hilton Grand Vacations navigates a normalizing economic terrain, recent financial outcomes radiate some pockets with a sense of optimism, with a few bullish indicators discernible within the company's quarterly report . Notably, HGV recorded a 6% uptick in total revenue for the second quarter, cresting at just beyond the $1 billion mark. According to management, this achievement, rooted in the strength and tenacity of the Financing and Club and Resort divisions, underscores HGV's potent recovery and resilient performance across its various operational sectors.

The Real Estate division, another critical component of HGV's portfolio, showcased its stability despite prevailing headwinds. The total contract sales for the segment, totaling $612 million, marginally fell short of last year's figure, an outcome that may very well deserve applause when considering the high-water mark set by last year's Key Performance Indicators (KPIs). This outcome also reaffirms the segment's core growth rate, which stood at a fairly impressive 21%.

Another laudable outcome is HGV's successful efforts to drive new buyer tours. The company experienced a surge of nearly 30% in this aspect, suggesting that its customer acquisition strategies are bearing fruit. Investors are probably pleased to learn that the new buyer contract sales accounted for 32% of the total for the quarter - the highest ratio since Q3 2019.

While the Volume Per Guest ((VPG)) was down from the previous year, it was still 17% ahead of the Q2 2019 figures, implying enhanced efficiency in the sales department. Meanwhile, the cost of the product was only 14% of net VOI sales, less than the previous quarter and year, demonstrating effective cost containment measures.

In the realm of finance, HGV continued its forward march, boasting a quarterly revenue of $76 million and a profit of $52 million. With the segment's margin moving in the right direction to 68% from last year's 66%, a profitable trajectory is evident.

As of June 30, HGV's liquidity position was approximately $920 million. This places the company in a good financial state, poised to capitalize on growth opportunities and absorb potential shocks. Lastly, HGV's net leverage on a trailing twelve months ((TTM)) basis stood at a comfortable 2.69 times.

Performance

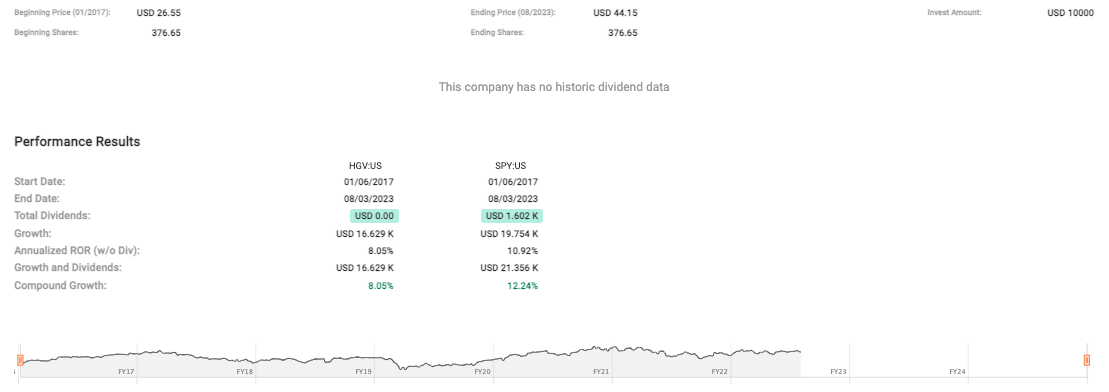

From an initial glance, especially considering the negative impacts from the pandemic, the share price of HGV has seen a commendable increase over this medium-term period (see data below) from January 2017 to August 2023, rising from USD 26.55 to USD 44.15. That's an impressive move of approximately 66.17%.

{kind=link}

However, this puts HGV in a trailing position behind the S&P 500 Index in both growth and annualized ROR. Specifically, the growth of HGV stands at USD 16.629K (based on an initial $10k investment) compared to the USD 19.754K generated by the S&P. Moreover, the Annualized ROR (without dividends) of HGV rests at a solid 8.05%, but yet again, it lags behind S&P, which clocks in at 10.92%.

Valuation

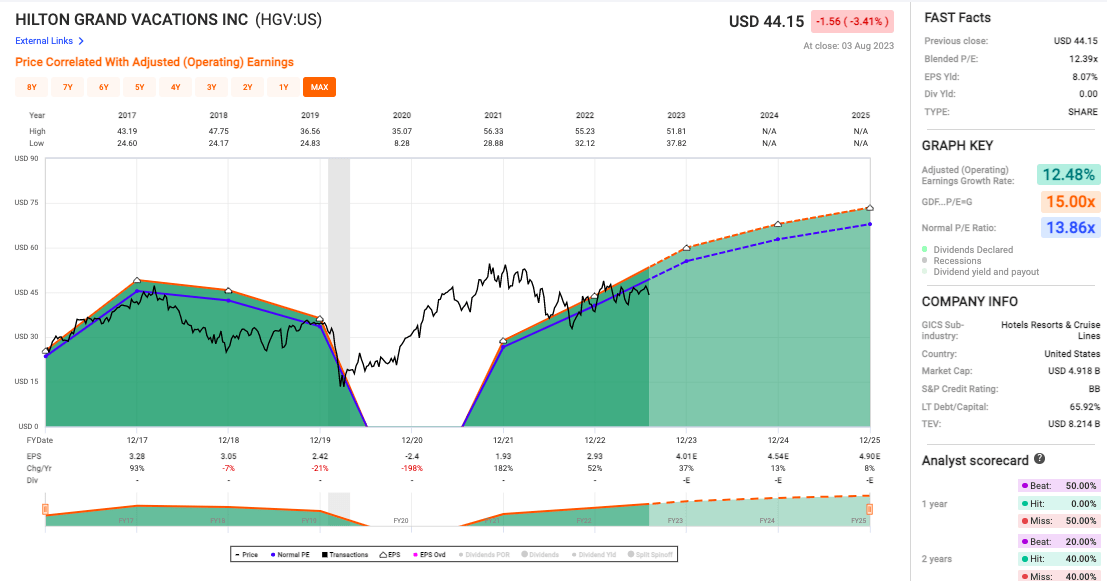

Hilton Grand Vacations' Blended P/E ratio stands at 12.39x, below the normal P/E ratio of 13.86x. Given this data, it appears HGV is currently undervalued in comparison to its historical norms.

{kind=link}

On another positive note, HGV's Adjusted Operating Earnings Growth Rate of 12.48% reveals the company is experiencing steady growth in its operational profitability, a crucial aspect for any business, especially in the hospitality sector, where competition is fierce and profitability can be volatile.

Risks & Headwinds

While Hilton Grand Vacations' Q2 report portrays elements of an encouraging landscape, there remain a few areas that warrant caution and careful scrutiny. Specifically, HGV's Volume Per Guest ((VPG)), a crucial metric for sales efficiency, lagged behind the near-record levels seen in the previous year. Though it outpaced the figures from Q2 2019, the year-over-year decline raises a red flag and could potentially point towards challenges in maintaining sales productivity.

The expenses tied to sales and marketing in the Real Estate division also spark concern. These costs ascended to $275 million for the quarter, accounting for a sizeable 45% of contract sales. When compared to the 36% observed in Q2 of the prior year, the mounting expenditure could potentially encroach upon HGV's profitability.

Moreover, evidence suggests there may be a squeeze on HGV's profit margins. Margins in the Real Estate division dipped to 31% from 38% in the previous year, while the Rental and Ancillary segment also experienced a marginal reduction, falling from 12% to 11%. Despite reporting a respectable 7% growth in revenue for the quarter within the Rental and Ancillary domain, the segment's profit only hit $89 million, with margins retracting to 67% from the 70% seen in the prior year.

Also of note, HGV tapped into $13 million of its adjusted free cash flow during the quarter, which comprised $22 million expended on inventory and did not include $22 million in acquisition-related costs. Should this trend persist, it could gradually erode HGV's liquidity position, posing further challenges to the company's financial stability.

While HGV's recently approved share repurchase program offers some optimism, the company is targeting a steady quarterly repurchase outlay of approximately $100 million. However, if the market climate takes a turn for the worse, this strategy could potentially stretch HGV's financial bandwidth and risk overexerting its resources.

Final Takeaway

I would rate Hilton Grand Vacations as a "hold." While HGV showcases a solid recovery with a 6% uptick in revenue, a resilient Real Estate division, and efficient cost-containment measures, some concerns linger. Sales efficiency and increasing sales and marketing expenses in the Real Estate division warrant caution, and a potential squeeze on profit margins in various divisions is concerning. Despite a promising share price increase, HGV's performance lags behind the S&P 500 Index. Given its current undervaluation and steady operational profitability growth, the stock has potential, but existing headwinds suggest it would be prudent to wait for clearer signs of sustainable growth before buying more shares.

For further details see:

Hilton Grand Vacations Q2: Profit Peaks, Potential Margin Squeeze