BVH - Hilton Grand Vacations: Questionable M&A Makes Shares Unattractive

2023-11-08 03:28:00 ET

Summary

- Hilton Grand Vacations shares have fallen over 20% since August and continue to decline, making it an opportune time to sell.

- The company's Q3 earnings were mixed, with adjusted EPS slightly lower and revenue falling short.

- The core business is slowing down, with sales of vacation ownership and sales and marketing fees declining.

- It is taking on debt to pay an over 100% premium for BVH with synergy targets that are very aggressive.

Shares of Hilton Grand Vacations (HGV) have fallen over 20% since August, turning negative over the past year, and Monday added to the pain. A mixed quarter, combined with an M&A announcement, sent shares down 8%. Given the decline witnessed already, it is an opportune time to ask if now is a time to "bottom fish" or if further downside remains in shares. Given the business is deteriorating, I think investors need to seriously consider the timing of taking on debt to pay a large premium to acquire a company. I view shares still as a sell.

{kind=link}

In the company's third quarter, HGV earned $0.98 in adjusted EPS, which beat by a penny, but revenue was 2% short at $1.02 billion. Adjusted EBITDA fell to $269 million from $338 million last year. Alongside this, it moved the mid-point of guidance down by about $100 million to $1.01 billion with the Maui wildfires a $20 million headwind. $10 million of the Q3 EBITDA decline can be attributed to Maui.

The Maui wildfire is likely to be a one-time event; if the company just reduced guidance in sympathy with that headwind, I would have been willing to look through it, and I suspect most investors would have as well. However, its guidance cut was far greater, and that is because the core business is slowing. Buying a timeshare (or vacation ownership) is a discretionary activity. It benefitted over the past two years as travel resumed.

However with much of that tailwind complete and with still-high inflation and lower personal savings, momentum is fading. Sales of vacation ownership fell by a third to $367 million. While I do not expect a recession, I also struggle to see an argument for why sales activity would materially rise given elevated interest rates and an economy that does not seem likely to accelerate meaningfully. Sales and marketing fees also fell by $7 million to $170 million.

On the positive side, resort management and rental fees rose by nearly 8% to $309 million. This was aided by 2% member growth. While slower than the 4% seen last year, it is still positive. HGV is also able to push price with revenue exceeding member growth by 6%. I do think this pace of pricing is likely to slow. In aggregate, real estate margins declined to 33.8% from 40.5%

Member growth lags sales activity, and with sales running at a slower pace, I do expect to see member growth continue to moderate. The other issue is whether we see increased defaults on time shares loans. In some ways, HGV and its competitor Marriott Vacations Worldwide ( VAC ) are analogous to credit card companies. They lend on an unsecured basis at a high rate. The ensuing financing income drives the lion's share of their income.

Just like the credit card companies, they are now seeing increased delinquencies and defaults as credit conditions normalize. Plus, a consumer struggling to make ends meet will likely default on their timeshare before a car or house. So far this year, loan loss receivables are $46 million from $32 million last year. It carries about $470 million in reserves against its $1.82 billion of time-share receivables.

When sales are strong, defaults are no big deal. HGV can reclaim the ownership interest and sell it to someone else, while there is a default, the loss may be minimal. But with sales also slowing, it may struggle to resell these interests, reducing its membership fees as its member count declines via defaults.

HGV also has a complex capital structure. It carries $2.7 billion of regular debt and $1 billion of nonrecourse debt. It has securitization structures where it houses much of its loans. If all of these loans were to default, in theory, HGV itself does not need to pay off this debt. However, it withdraws significant cash flow from these structures (as the loans pay higher rates than the secured debt does), which could decline if defaults rise.

Year to date, adjusted free cash flow has been $277 million from $656 million last year. In the quarter, $162 million of it $257 million in free cash flow came from its non-recourse debt. In addition to its free cash flow contribution, its business depends on being able to finance new sales; if this becomes more difficult, it will have to further slow sales, reducing future management fees. This is a pro-cyclical business model, and I expect to see further free cash flow pressure over the next year.

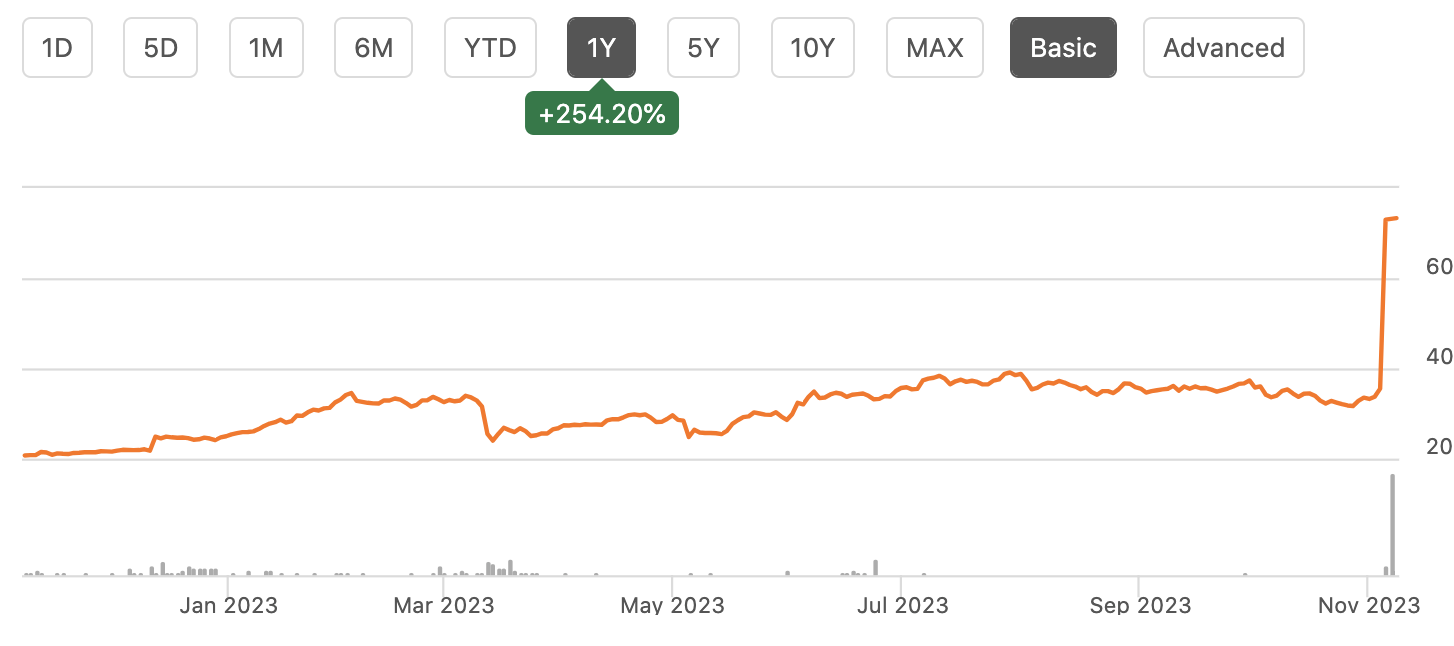

In addition to these mixed results, on Monday, HGV announced it would be buying Bluegreen Vacations ( BVH ) in cash at $75 a share, more than double where shares were trading Friday. That is about a $300 million premium, and it has been a wonderful ride for BVH shareholders who have more than tripled their money this year. HGV will also assume about $900 million in debt. Just given the magnitude of this premium, it is hard not to question the premium HGV is paying to acquire these 49 resorts, growing its portfolio by a third.

{kind=link}

Leverage will rise to 3.4x, and it will take 18 months to get back to the company's 2-3x leverage target. This also assumes $100 million cost synergies and $75-100 million in EBITDA contribution from revenue synergies. At a time of elevated rates with the core business slowing, moving so far above its debt target and staying there well into 2025 feels like risky timing, especially is there is a recession. HGV will likely have to pay over 8% interest to finance this purchase, creating a very high hurdle to create positive returns for its shareholders.

BVH has $700 million of operating expenses , so it needs to cut costs by 14% to hit the synergy target. There is also $4 billion in combined revenue. Even assuming a 40% margin, this would require $250 million in incremental revenue to hit that synergy target. To approach these targets, there will need to tremendous cross-team overlap and cross-selling opportunities. These savings are needed to merit the premium HGV is paying, and I think investors should have some caution on their attainability.

BVH has $140 million in adjusted EBITDA. Absent synergies, HGV is paying nearly 11x. At full synergies, HGV is paying 4.4x EBITDA. HGV is trading at 7.5x EBITDA, including non-recourse debt at today's share price. To justify this price, it needs to get $60 million in synergies. That is possible, but that simply merits this price at HGV's $34 share price. To merit a price higher than that and be accretive, more than $60 million in synergies will need to be found.

In this economic environment, I think if you invest in a pro-cyclical business, you want to invest in a company with a strong balance sheet that can withstand downturns. Because of its reliance on withdrawing cash from securitizations, HGV already has a leveraged balance sheet. To add debt on top of that to pay a premium at a time vacation sales are falling feels very pro-cyclical and leaves uncomfortably little room for error. HGV also trades 2x book value, which given the risk in its loan portfolio, feels expensive.

With just a 5% free cash flow yield, shares to me do not reflect the combined risk posed by deterioration in its business as well as increased financial leverage. I think the market was right to react so negatively to this announcement. I view shares as a sell. Ultimately, the decision making of this management team is confusing and very aggressive to me, and even at 10x forward earnings, I do not believe these risks are factored in sufficiently. Investors should invest their capital elsewhere.

For further details see:

Hilton Grand Vacations: Questionable M&A Makes Shares Unattractive