RYLPF - Hims & Hers Health: Expect Strong EBITDA Growth As Revenue Growth Remains Strong

2023-07-13 07:50:01 ET

Summary

- I recommend a buy rating due to Hims & Hers Health's strong growth, expanding EBITDA margins, and potential in the growing telehealth market.

- I see room for further margin expansion as HIMS increases fulfillment capacity through affiliated pharmacies.

- Despite competition from larger players, the Company's strong balance sheet and growing profitability position it well for future growth and potential acquisitions.

Overview

My recommendation for Hims & Hers Health ( HIMS ) is a buy rating as I expect the business to continue growing strongly, which should drive strong EBITDA growth as margins expand from here.

Note that I previously rated a buy rating for HIMS due to the large TAM, strong brand position and value proposition, business model, and growth momentum. I believe that as long as management does not mess up on execution, it should be able to continue capturing share in this space.

Business

HIMS's telehealth platform connects patients with specialists in many different areas of medicine, such as mental health, dermatology, primary care, and more.

Industry

According to Grand View Research, the worldwide telehealth market will grow from its 2022 valuation of $83.5 billion at a CAGR of 24% between 2023 and 2030.

My take is that there are more and more people having access to the internet, and technological advancements in smartphones are making it possible to fill in the gaps in telehealth service delivery and accessibility. As a result of the COVID-19 pandemic and the measures taken to contain it, there has been a dramatic increase in the demand for telehealth services over the past year. Because COVID-19 made it more difficult to provide healthcare, most hospitals and clinics switched to providing care online. In addition, the rising interest in virtual health management of chronic diseases is fueling the expansion of the industry.

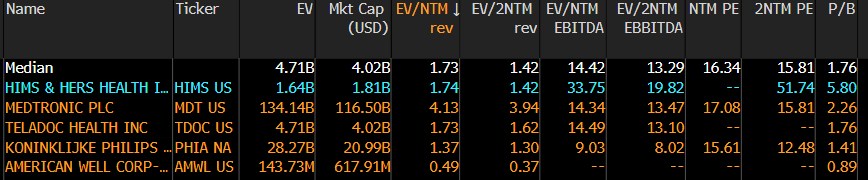

Major competitors include: Medtronic ( MDT ) , Teladoc Health ( TDOC ), American Well ( AMWL ), Doctor on Demand, Koninklijke Philips ( OTCPK:RYLPF ), etc.

Investment highlights

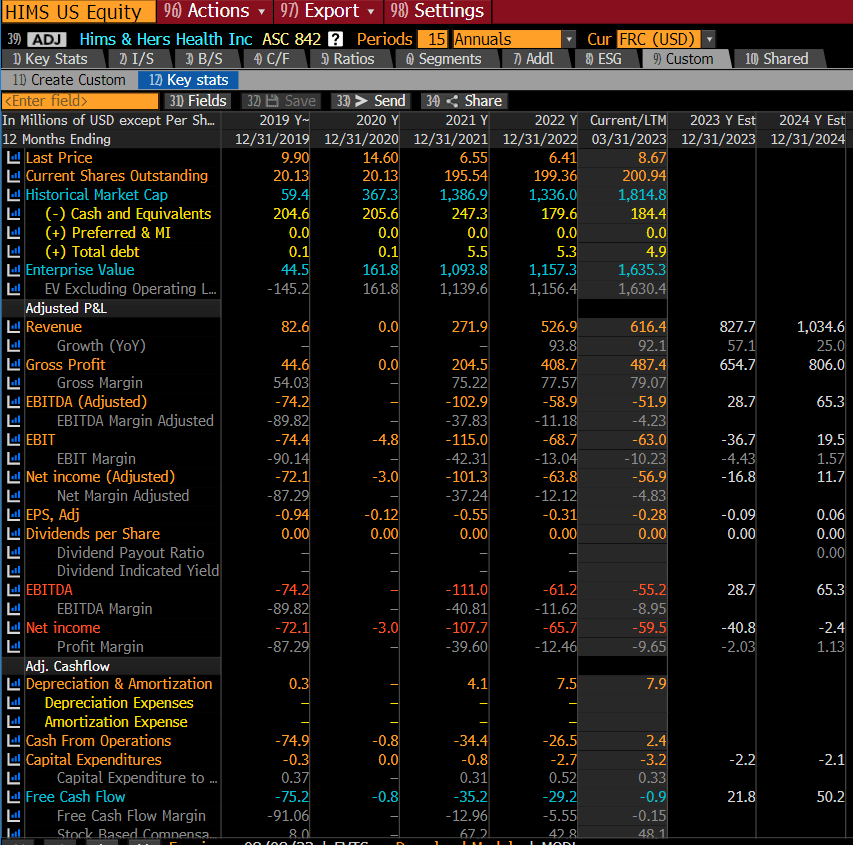

Management raised revenue projections for 2023 after a strong first quarter. The newly guided revenue has a range of $810 to $830 million, or a growth rate of roughly 56% compared to the previous estimate of 41%. In addition, EBTIDA guided range is now $25 to $30 million. I believe there is room for growth in EBITDA margins over the long term as HIMS is now using its network of affiliated pharmacies to fill about 60% of orders; by year's end, they hope to increase that number to 80%. An increase in margins is possible as a result of this increase in fulfillment capacity.

Financials highlights

HIMS's total revenue for the 1Q23 was $190.8 million, representing an increase of 88% year over year and exceeding consensus expectations of $179.1 million. Positively impacting the bottom line was the company's continued success in expanding its subscriber base and AOV, both of which came in at 96% year-over-year growth. The final subscriber tally for Q1 was over 1.2 million, an increase of 87% year over year and 16% sequentially. The average order value increased by 15% year-over-year, to $90.

Adjusted EBITDA of $6.1 million was driven by a strong top-line performance and a 100bps sequential improvement in gross margin, which was aided by longer duration subscriptions and scale. However, I anticipate a return to a gross margin in the mid-70s over the course of the next few quarters as HIMS reinvests in enhancing the customer experience.

While investors may have seen HIMS's telehealth business grow as a result of the Covid pandemic, I think the company is reaping the benefits of business as usual, with demand for its products and services remaining strong.

{kind=link}

HIMS has a strong balance sheet, with $180 million in net cash. Given that the company has already achieved profitability, I don't see any risk with the balance sheet. Instead, HIMS now has the ability to conduct bolt-on transactions if the opportunity arises.

Valuation

Author's valuation model

According to my model, HIMS is worth $11.28 in FY24, a 30% increase. This target price is based on my 20+% annual growth forecast for the next two years. The rationale for the lower-than-historical growth rate is to remain conservative and within the long-term guided range of management.

HIMS is now trading at 1.74x forward revenue, which I believe is reasonable given that the average multiple for peers is 1.73x. Because HIMS is not profitable, benchmarking valuation by comparing relative sales growth is a good way. HIMS growth is the highest in the group, but due to its low margin profile, it merits a premium over higher valued peers.

{kind=link}

{kind=link}

Risk

Competition for HIMS comes from both well-established medical facilities and cutting-edge telehealth startups. These larger competitors might have strong distribution network and financial capacity to drive the same product offering at a lower price, making it hard for HIMS to scale.

Conclusion

I maintain my buy rating for HIMS based on the strong revenue growth and potential for expanding EBITDA margins. The telehealth platform offered by HIMS connects patients with specialists in various medical fields, positioning the company in a growing market. The telehealth industry is projected to experience significant growth due to increased internet access and advancements in smartphone technology. HIMS's management raised revenue projections for 2023 after a robust first quarter, and there is room for further margin expansion as fulfillment capacity increases through affiliated pharmacies. Financially, HIMS has demonstrated strong performance, with impressive revenue growth and a solid subscriber base. With a strong balance sheet and profitability achieved, HIMS is well-positioned for future growth and potential acquisitions. Considering valuation, HIMS is trading at a reasonable multiple compared to peers. However, competition from larger players remains a risk. Overall, HIMS shows promise for continued success in the telehealth industry.

For further details see:

Hims & Hers Health: Expect Strong EBITDA Growth As Revenue Growth Remains Strong