HIFS - Hingham Institution for Savings: A Well-Run Bank With Great Growth Potential

2023-09-05 05:20:17 ET

Summary

- Hingham's dual growth strategy focuses on expanding deposits and loans in existing, affluent markets, leveraging specialized services to enhance profitability and mitigate expansion risks.

- Hingham's long-tenured management and high insider ownership, including the CEO's significant stake, signal deep commitment and alignment with long-term shareholder value.

- HIFS excels in net interest margin and loan quality, but struggles with interest rate sensitivity, affecting its recent efficiency ratio and performance.

- Using key metrics like ROA and Price-to-Book, I calculated a 20.4% expected annual return for HIFS at the current price of $202.20.

Investment Thesis

I'm convinced that Hingham Institution for Savings (HIFS) is a buy. The bank's dual-pronged growth strategy, which targets both deposits and loans in wealthy, established markets, is especially promising. This strategy is amplified by their Specialized Deposit Group, designed to meet the specific needs of commercial clients. This not only enhances the bank's net interest margin but also bolsters its overall profitability. Additionally, the long-standing management team and substantial insider ownership, including a noteworthy investment by the CEO, signal a deep-rooted commitment to enhancing shareholder value over the long term. Although HIFS has generally performed well in terms of Net Interest Margin and the quality of its loans, it has shown some sensitivity to interest rate changes, affecting its recent efficiency metrics. Nevertheless, my detailed valuation, based on key indicators like ROA and Price-to-Book, suggests an expected annual return of 20.4% at the current share price of $202.20. Given all these elements, I see HIFS as an outstanding investment opportunity.

Company Overview

Hingham Institution for Savings, a Massachusetts-chartered bank founded in 1834, has a strong foothold in the Greater Boston area. Specializing in personal and business banking, the bank offers a comprehensive suite of services including savings and checking accounts, mortgage and commercial loans, as well as wealth management services. Known for its exceptional customer service, the bank has carved out a niche in both residential and commercial lending markets. With a long-standing history of stability, community involvement, and a focus on technology-driven solutions, Hingham Institution for Savings is committed to delivering consistent growth and robust returns for its shareholders, making it a trusted financial partner in the community.

Long Runway for Expansion

I see Hingham's small size and concentrated market presence as an exciting opportunity which presents investors with a long runway for growth. To capitalize on this potential, and to continue to grow sustainably into the foreseeable future, the company has clearly outlined a dual growth strategy, which focuses on expanding deposits and loans/equity within their current markets.

The bank's approach to deposit growth is particularly noteworthy, as it leverages its Specialized Deposit Group ((SDG)) to cater to the nuanced needs of commercial clients. This is a notable move, given that commercial deposits are typically the cheapest form of funding for banks, thereby enhancing the bank's net interest margin ((NIM)) and overall profitability. In my opinion the deposit side has historically been the weaker side of the company, with the bank relying on a mix of retail and commercial deposits, wholesale deposits, and borrowings. The composition of its interest-bearing liabilities (IBL) reveals a strategic focus on term certificates, which make up 39% of IBL, followed by money markets at 26%, and wholesale and other borrowings at 30%. Regular interest-bearing deposits and Negotiable Order of Withdrawal ((NOW)) accounts make up a smaller portion at 4% and 1% respectively. Because of their reliance on IBLs the bank is sensitive to the Federal Reserve's fund rate, which is a factor in why the bank has been struggling in recent quarters as the interest on much of the bank's deposits have increased, compressing their NIM.

Moreover, HIFS's loan and asset growth strategy is equally compelling. The bank is targeting expansion in dense, coastal cities with favorable demographics, such as San Francisco and Washington D.C., which it entered in 2021 and 2016, respectively. These markets are characterized by substantial wealth, supply constraints, and a high concentration of multifamily real estate, making them ideal for the bank's specialized loan offerings. While the bank currently lacks a local office and staff in San Francisco, this could be viewed as an untapped growth opportunity rather than a limitation. The bank's intent to replicate its Boston model in these cities through new branches and strategic local investments further underscores its growth potential.

What sets HIFS apart is its disciplined approach to growth. Rather than diluting its focus by entering new markets, the bank is deepening its footprint in existing markets where it already has a presence. This allows HIFS to leverage its existing knowledge and relationships, thereby mitigating the risks typically associated with geographic expansion. That being said, should the company choose to expand into further markets in the future, and extend their growth runway, I have a strong belief they will be able to replicate what they have done in Washington D.C and San Francisco markets.

A Proven and Reliable Management Team

Perhaps one of the most impressive aspects of Hingham is the long-tenured management team and board of directors. In my view, the long tenure of HIFS' directors is a strong indicator of a stable and well-run organization. I can't stress enough how valuable it is to have a team that's been through the ups and downs of market cycles. Their institutional knowledge is something that can't be easily replicated and often leads to better strategic decisions. This experience is particularly important to HIFS as the board of directors have to approve any potential loan over $1 million.

Now, let's talk about insider ownership. The fact that directors and executives own over 31% of the company is a huge green flag for me. When management has that much skin in the game, you can bet they're not just clocking in and out. They're likely as invested in the long-term success of the company as any shareholder would be. It's a sign that they believe in what they're doing, and that's the kind of team I want to invest alongside.

As of 2022, the CEO, Robert Gaughen, and his family owned about 15% is another strong point. This isn't pocket change; it's a significant portion of his personal wealth. When a CEO is that invested, it tells me they're not just there for the salary or the perks. They're in it for the long haul, and they have every incentive to increase shareholder value.

But what really stands out for me is the ratio of the CEO's share ownership to his salary, he currently holds shares worth approximately 16 times his annual salary . In my experience, when a CEO's financial well-being is that tightly bound to the company's performance, it often leads to decisions that benefit everyone invested in the company as the CEO has as much to lose or gain from the journey as you do.

So, putting it all together, these factors make me feel that the management team at HIFS is not just competent but also deeply committed to the company's success.

Keeping an Eye on Their Key Metrics

Another impressive aspect of HIFS historically has been its strong performance relative to its peers, although I acknowledge that recently the company has been struggling, as it generally does in a rate rising economic environment, due to its interest sensitive deposits, which I discussed before.

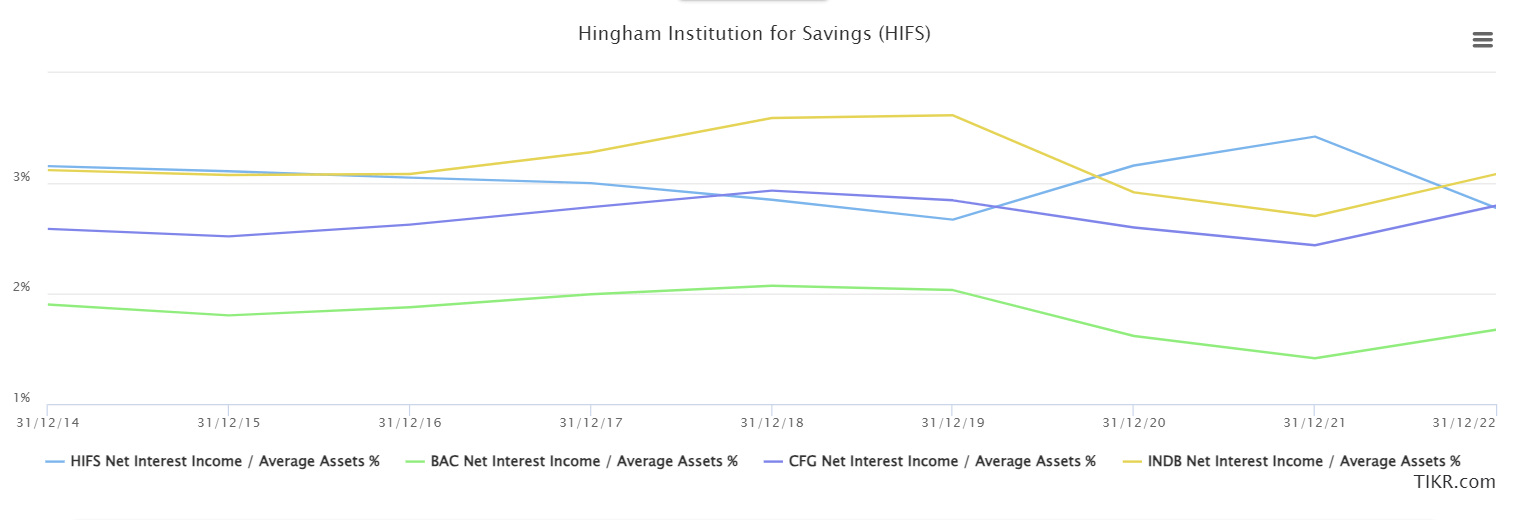

Firstly, let's talk about Net Interest Margin ((NIM)). HIFS has a 10-year median NIM of 3.2% , which is quite competitive when compared to other banks like Citizens Financial Group (CFG), Independent Bank Corp. (INDB) and Bank of America Corp. (BAC). What you'll notice when comparing these banks is the sharp decline in NIM for HIFS over the past year which I think highlights its sensitivity to change in interest rates.

{kind=link}

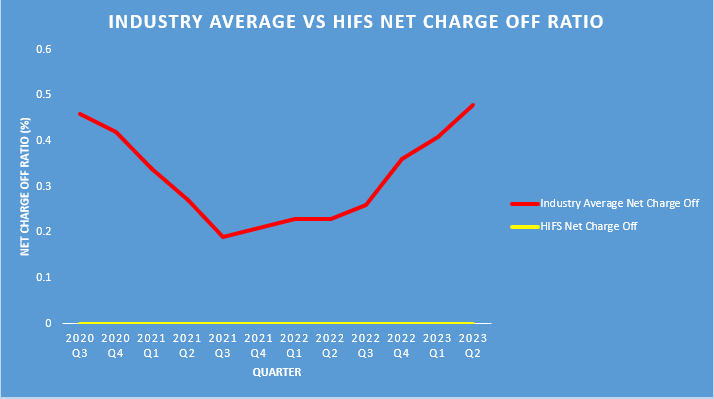

Despite this, I think that what sets HIFS apart is the quality of its loans. The bank specializes in low-risk loans, particularly in commercial and residential real estate lending. This conservative approach to lending has resulted in minimal net charge-offs (NCOs), even during financial crises. The company demonstrated this in the most recent earnings, as they reported that they did not record any charge-offs in the first six months of 2023, a time when there was immense uncertainty in the banking sector and other banks reported an up-tick in NCOs .

Industry Average vs. HIFS Net Charge Offs (DJTF Investments)

{kind=link}

The efficiency ratio has historically been another strong point for HIFS. Over the years, the bank has become increasingly efficient, with its ratio becoming one of the best in the industry. This means that a larger portion of their net income is not being eaten up by operating expenses, making the bank more profitable. However, the efficiency ratio has taken a hit over the past few quarters as the company reported an increase to 55.03% for the second quarter of 2023 , as compared to 21.30% for the same period last year. This is a substantial increase which I believe in in large part due to their interest sensitive business model. I anticipate that the efficiency ratio will improve once the company is able to source new loans with higher interest rates, mitigating the impacts felt by the increase in deposit interest.

Lastly, the bank's asset to equity ratio is relatively high at 10.78, but this isn't necessarily a red flag. Given that HIFS specializes in low-risk loans, they can afford to be more leveraged. The bank has been deleveraging over time, which is a prudent move, but their current level of leverage is justifiable given their low net charge-offs.

Financial Analysis

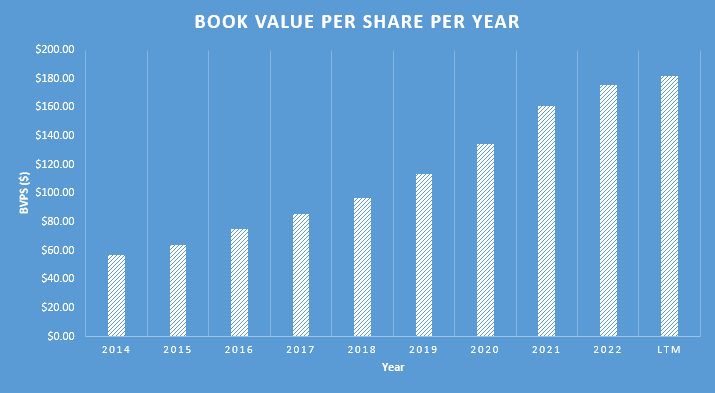

Over the last half-decade, Hingham Institution for Savings has exhibited robust financial health. The company's revenue has consistently climbed, rising from $62.78 million in 2018 to $82.58 million in the last 12 months (LTM). This equates to a compound annual growth rate ((CAGR)) of around 5.6%. While the earnings per share ((EPS)) have experienced some volatility, peaking at $30.65 in 2021 before declining to $17.85, it's important to note that 2021 was a particularly strong year for the company, likely representing a cyclical high in the interest rate cycle. On the other hand, the book value per share has been on a steady upward trajectory, increasing from $97.07 in 2018 to $181.75 LTM, with an impressive CAGR of about 13.37%. This consistent growth in book value suggests that Hingham has effectively enhanced its intrinsic value over these years.

HIFS Book Value per Share (HIFS)

{kind=link}

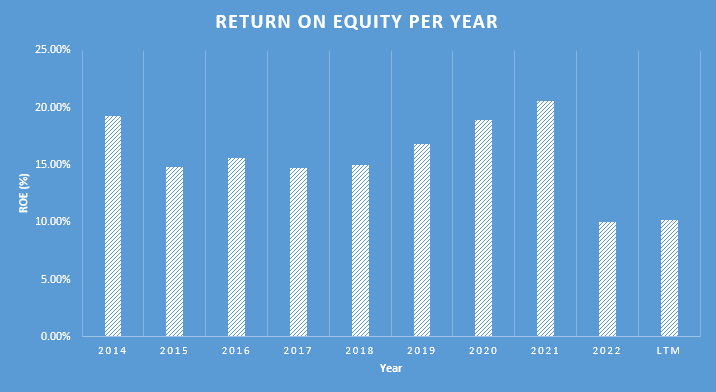

HIFS has consistently demonstrated remarkable performance in terms of its Return on Assets (ROA) and Return on Equity ((ROE)). These key metrics not only outperform industry averages but also indicate efficient asset management and effective use of shareholder equity. The 5-year average ROA of 1.50% shows that Hingham is adept at converting its investments into profits, while the strong 5-year average ROE of 15.32% reveals that it provides excellent returns to its shareholders.

{kind=link}

I expect Hingham's upcoming quarterly earnings results to be another tough one given we have continued to see rate rises by the Fed. My anticipation is that for the next 12 months, things will slowly start to turn around for the company as they begin to secure new loans with higher interest rates which will reserve the downtrends the company has been experiencing with key metrics such as NIM and efficiency ratio. I anticipate the company will continue to issue low-risk commercial and residential loans and as such we will continue to see very low to no net charge offs.

Looking beyond the next 12 months, assuming the Fed does not continue to quickly raise rates, I believe that HIFS should return to strong growth and I fully expect the return to impressive levels across all the key metrics I previously mentioned, especially given that the management team has proven in the past that they are consistently meeting or exceeding their outlined goals and have reliably demonstrated a firm desire to return value to shareholders in a sustainable manner.

Valuation

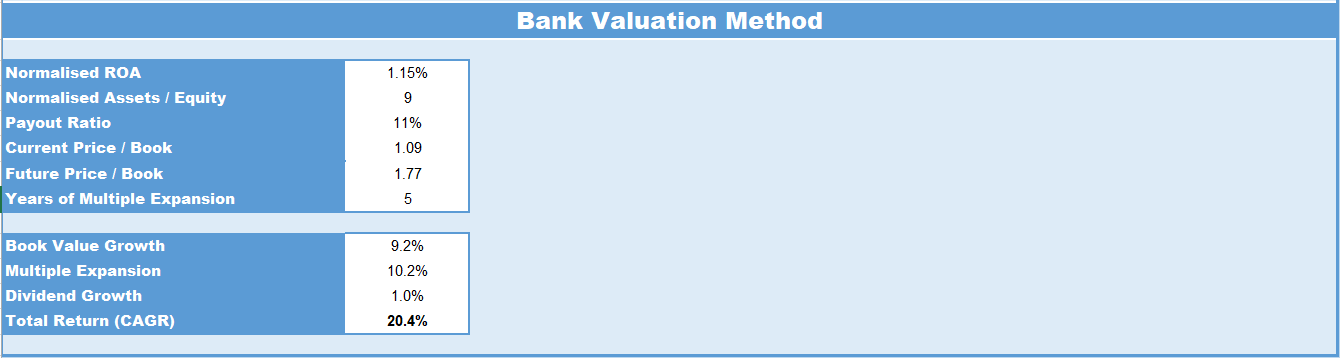

In my view, valuing bank stocks requires a specialized, balance-sheet focused approach. Traditional methods like discounted cash flows or Price to Earnings ((PE)) ratios are less effective due to banks' cyclical and leverage-heavy nature. That's why I prioritize metrics like ROA, Assets-to-Equity Ratio, and Price-to-Book Ratio. ROA measures efficiency, while the Assets-to-Equity ratio gauges risk, and Price-to-Book shows the premium over net asset value. I also consider the payout ratio to understand how much earnings are retained for growth. Finally, I calculate an expected return, incorporating these metrics and building in a margin of safety. I believe that this method provides a comprehensive view of both current valuation and future potential, making it ideal for long-term investment decisions.

For HIFS I have chosen a normalized ROA of 1.15%, a conservative figure based on a 10-year median of 1.25% and recent trends, outside of the last year nearing 2%. I've also set the normalized asset-to-equity ratio at 9.0%, reflecting the bank's recent downtrend from around 13 to 10.78. My chosen payout ratio is 11%, in line with the bank's strategy of retaining more earnings for reinvestment.

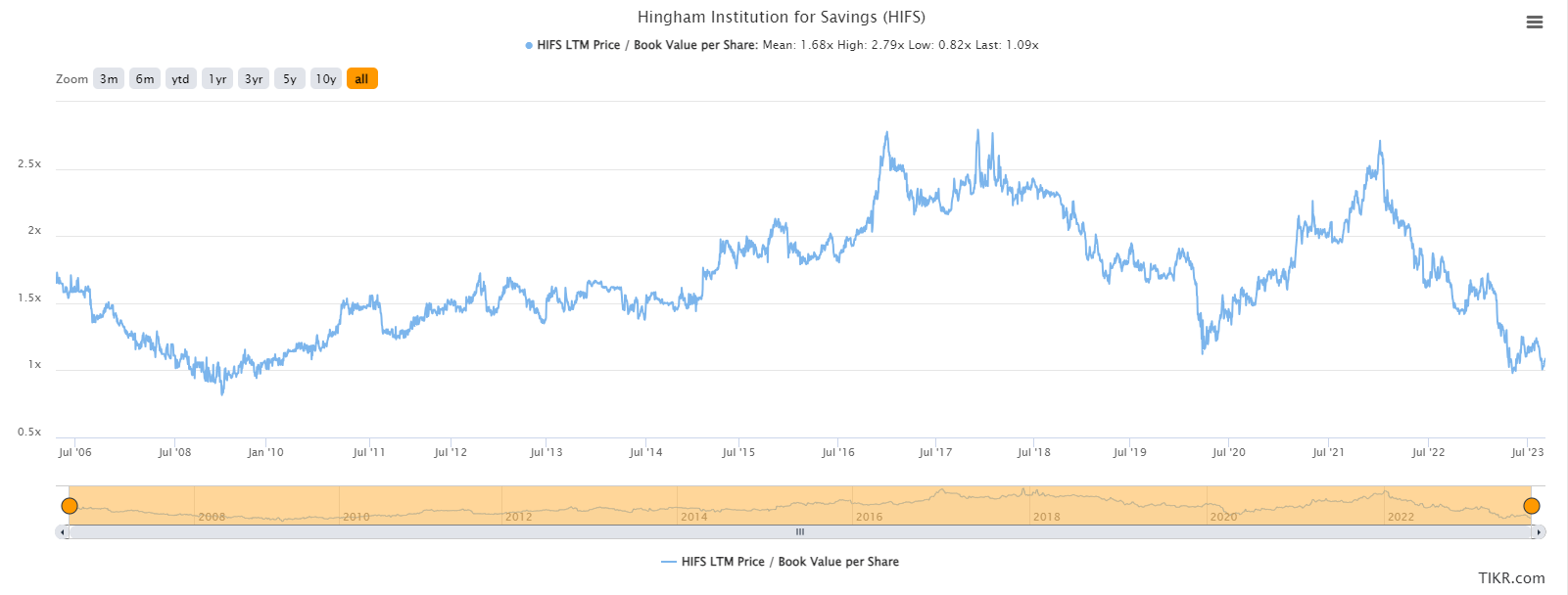

For the Price-to-Book ratio, I've used its current value of 1.09 and projected a future ratio of 1.77, based on a 3-year mean. I've also set a time frame of five years for the multiple to expand to this level. Using these inputs, I calculate a total expected return of 20.4% per year at the current share price of $202.20.

{kind=link}

Furthermore, given that the bank rarely sees a price-to-book value around 1, with the last time being during the Global Financial Crisis ((GCF)), a time when the company was far less robust than it is today, I believe that HIFS represents an excellent opportunity and is a buy in my opinion.

{kind=link}

Risks

In my view, the bank's liquidity management strategy seems well-thought-out but not without risks. They maintain a significant level of overnight cash for immediate liquidity needs and diversify their funding sources, which include customer deposits, nationally marketed time deposits, brokered time deposits, and Federal Home Loan Bank of Boston ((FHLB)) borrowings. However, there are vulnerabilities. Adverse operating results or industry changes could make it difficult to access these funding sources. Additionally, the bank's ability to accept brokered deposits is contingent on maintaining a "well-capitalized" status under banking regulations. Losing this status would require an FDIC waiver to continue using brokered deposits, adding another layer of risk.

Another concern is the bank's dependence on key personnel. The competition for top talent in the banking industry is fierce, and the loss of key employees could significantly impact client relationships and, by extension, the bank's performance. This is particularly concerning given that new hires may face activity restrictions due to agreements with their previous employers.

The fluctuations in interest rates could continue to narrow the net interest income, which is the lifeblood of any bank. While the bank has asset and liability management policies to mitigate this, the risk remains. Additionally, local economic conditions, particularly in eastern Massachusetts and the Washington DC metro area, are crucial. A downturn could impact both the bank's ability to attract deposits and the repayment capabilities of its borrowers, thereby affecting loan collateral values.

Conclusion

Hingham's dual growth strategy is particularly compelling, focusing on expanding both deposits and loans within affluent, existing markets. This approach is further enhanced by their Specialized Deposit Group, which aims to cater to the unique needs of commercial clients, thereby boosting the bank's net interest margin and overall profitability. The bank's long-tenured management team and high insider ownership, including a significant stake by the CEO, strongly indicate a deep commitment to long-term shareholder value. While HIFS has historically excelled in Net Interest Margin and loan quality, it has shown some vulnerability to interest rate fluctuations, impacting its efficiency ratio and recent performance. However, after a thorough valuation using key metrics like ROA and Price-to-Book, I've calculated an impressive expected annual return of 20.4% at the current share price of $202.20. Given these factors, I believe HIFS presents an excellent investment opportunity.

For further details see:

Hingham Institution for Savings: A Well-Run Bank With Great Growth Potential