HIFS - Hingham Institution for Savings: Taking A More Cautious Outlook For 2023

Summary

- Hingham shares rallied nicely to end 2022, and as such, I'm dialing back my enthusiasm a bit for the time being.

- The bank has a tremendous management team and superior business model, however, it is not well-positioned to face the current interest rate environment.

- I suspect shares may be rangebound until we start seeing signs of interest rates reversing course.

Hingham Institution for Savings ( HIFS ) is a regional bank based out of Hingham, Massachusetts. The bank is notable for having the best efficiency ratio of any multi-branch bank in the United States. This exceptionally lean operating structure combined with a low-risk lending strategy has led to superior returns through multiple full business cycles for Hingham shareholders.

HIFS stock traded for around $5 in the early 1990s as the Gaughen family took over the bank and improved its business model. Since then, shares have now risen to $300 a pop, and that doesn't even count the firm's dividends and special dividends along the way.

However, while Hingham's business model is one of the best for the long-term within the banking industry, it faces significant short-term headaches related to higher interest rates. Hingham's business model was designed around interest rates remaining low, and it actually sees profitability decline -- unlike most peer banks -- when interest rates move up sharply.

Given the short-term headwinds to the model, I suspect that 2023 may be something of a "lost year" for Hingham. I last covered the bank in October 2022, rating shares a strong buy . Shares have since rallied 20%. Given the improvement in share price along with lingering clouds on the horizon as far as intermediate-term profitability goes, and I am dialing back my enthusiasm a bit for the time being. Here's why.

Hingham Has A Weak Deposit Base

Banks have a two-sided balance sheet. We tend to think more about their loans. Who does a bank lend to, at what rate, and how much risk is taken in doing so?

But the liability side of the ledger matters as well. Where does a bank get its deposits from, how much is it paying for them, and how much sensitivity does the bank face from higher interest rates?

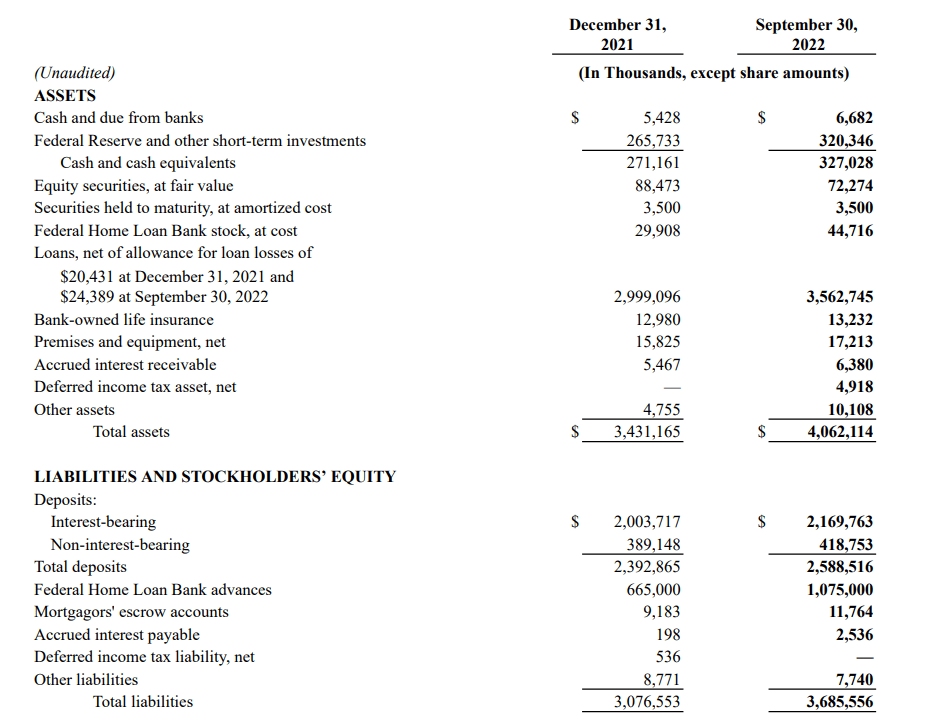

Hingham has a modest deposit base compared to its assets, as the 3Q balance sheet below shows:

{kind=link}

The bank had $3.6 billion of outstanding loans as of Q3, up from $3.0 billion at the end of 2021. To fund these loans, however, Hingham had just $2.6 billion of deposits, and that figure only grew by $200 million versus 2021 while outstanding loans grew at three times that rate.

Where is Hingham getting the rest of its money to fund its loans if not deposits of the bank? You can see it on the ledger, there is a $1.1 billion advance from the Federal Home Loan Bank.

The issue with that, however, is that FHLB money tends to cost far more for banks to access than what it could get from other sources. To that point, in Q3, Hingham paid slightly more in interest on its $1.1 billion of FHLB borrowings than its $2.6 billion of deposits. It's expensive not to have a strong deposit base in the current interest rate environment. This hardly wipes out the bank's profitability or business model entirely, but it will be uphill sledding trying to grow earnings until interest rates start to come back down.

Furthermore, a bank would ideally have more non-interest-bearing deposits. In the case of Hingham, it has just $419 million of such funds, however, which is a drop in the bucket compared to its $3.6 billion loan book.

This is a trade-off for having such a stellar efficiency ratio. Hingham hasn't invested heavily in customer service or gathering deposits. That was a wise choice for many years as banks could obtain funds for practically no cost regardless of the source. Now, however, Hingham is having to turn to higher-cost FHLB funds or brokered deposits. This will hit the bank's net interest margin "NIM" for the foreseeable future.

To add to that, Hingham is now offering significantly higher certificate of deposit rates than it would have in the past. For example, at the time of this writing, Hingham is offering a 4.07% interest rate for 9-month CDs, and 3.92% interest on 13-month CDs.

Hingham has traditionally earned a NIM of around 3% over the past decade, give or take a few basis points. To earn a 3% NIM on funds that Hingham is paying 4% annually for, it has to make new loans at a 7% interest rate. That is certainly possible in the current interest rate environment. However, given Hingham's focus on making high-quality loans with minimal credit risk, it may be hard to achieve traditional profitability metrics given the bank's outsized reliance on external funding sources.

There is another complication which clouds the outlook for 2023 even further. This is that Hingham holds a meaningful equity position on its balance sheet, amounting to a $72 million stock portfolio at the end of Q3. This was, however, down sharply from $88 million at the end of 2021.

This was not a bad investment result compared to the S&P 500 over the same period. Regardless, it's a meaningful decline in valuation for a bank of this size. And, due to accounting rules for this sort of investment, Hingham has to mark stock market losses as an immediate loss which causes a reported hit to earnings.

By contrast, in 2020 and 2021, Hingham was getting to report higher earnings per share figures because the stock market was rallying and so the equity investments on its balance sheet kept gaining in value. As I expect 2023 to be another volatile year for the stock market, I don't foresee the equity piece of Hingham's balance sheet providing too much help to either earnings or investor sentiment this year. That said, Q4 2022 earnings (which are to be announced shortly) should show a significant gain on equity investments as compared to Q3 as the market was up meaningfully in the last quarter of 2022.

HIFS Stock Verdict

If I could only own one bank stock in the United States for the next decade or longer, it would be Hingham Institution for Savings. The Gaughen family has done an incredible job delivering consistent shareholder value and building a distinct bank. Its focus on unmatched efficiency has made Hingham a tremendously profitable bank even in an industry that has generally struggled since the 2008 financial crisis. I have the utmost confidence in Hingham's management team to navigate the current interest rate shock.

That said, I can't sugarcoat the outlook for 2023 in particular. Hingham's business model has centered around having stable low interest rates. It has achieved such high efficiency ratios and returns on equity, historically, because it hasn't invested too heavily in its deposit base. In a world of zero interest rate policy, Hingham's decision to not invest aggressively in the deposit base made a ton of sense.

However, the bill for that decision is now coming due. Hingham will have to figure out how to finance the liability side of its balance sheet into this sharply higher interest rate environment. And there's a good chance that it simply won't be able to get the same improvement out of its loans to keep its interest spread flat.

Putting the pieces together, there's a decent chance that earnings will be down for 2023. As Hingham is already trading at a significantly higher P/E ratio than many other peer banks, this does not bode well for the bank's intermediate-term share price outlook.

This is confirmed from looking at the bank's historical price-to-book valuation range as well. Historically, Hingham has almost always been a superior buying opportunity when shares traded at 1.5x book value or less. Meanwhile, I'd be more cautious buying above the 2.0x range, particularly with the near-term economic outlook being more challenging. Here's how HIFS shares have been valued over the past ten years:

1.73x book value is still toward the low end of Hingham's range, but it's out of the deep discount range we saw a few months ago, when shares fell under the 1.5x level.

As you can see, Hingham shares also declined in valuation during the 2018 rate hiking cycle, and they didn't really respond even as that ended by early 2019. I suspect we may see a similar result now, where Hingham shares consolidate around their current share price as the current Fed rate hike cycle draws to a close. Only when we start to hear rumors about Fed cuts again, I'd imagine, will Hingham's shares blast off toward new highs once again.

As such, I still have a favorable view on Hingham shares today, particularly for longer-term investors. That said, I don't anticipate the stock appreciating much further in value until 2024, making this a story that will require some patience.

For further details see:

Hingham Institution for Savings: Taking A More Cautious Outlook For 2023