HIO - HIO: One Of The Better Junk Bond CEFs With A Double-Digit Yield

2024-01-18 16:02:54 ET

Summary

- The Western Asset High Income Opportunity Fund Inc. offers a current yield of 10.87%, higher than many other junk bond funds.

- The HIO fund has managed to outperform the Bloomberg junk bond index on a total return basis over the past three years, despite not using leverage.

- The fund primarily invests in high-yield bonds and has taken precautions to protect against defaults, but the risk lies in interest rates rather than defaults.

- The fund will probably decline over the next few months because economic data does not support the rate cuts baked into its price, but the lack of leverage should help.

- The fund can probably sustain its current distribution and is trading at a discount, albeit a smaller discount than it has averaged over the past month.

The W estern Asset High Income Opportunity Fund Inc. ( HIO ) is a closed-end fund, or CEF, that income-seeking investors can employ to meet their goals. The fund's 10.87% current yield stands as a testament to its success in this area, as that is a considerably higher yield than what is available from many other junk bond funds today.

For example, the BNY Mellon High Yield Strategies Fund ( DHF ), which we discussed a few days ago, only offers a 7.83% yield at the current market price. The very interesting thing about this fund though is that it manages to achieve this very high yield without the use of leverage. That is something that could put the fund in an advantageous position relative to its peers as the lack of leverage should mean that it will decline much less in the event of a market correction driven by the Federal Reserve's failing to reduce interest rates to the degree that the market expects.

The recent consumer spending report that corresponded to the holiday season came in somewhat hotter than expected, which could reduce the probability that the Federal Reserve will succumb to the market's current demands for a rate reduction at the March meeting. As such, this fund might be a better holding than some of its peers, but we should investigate it further, as it is difficult to understand how the fund is able to pay out its current yield in the current environment without making destructive distributions.

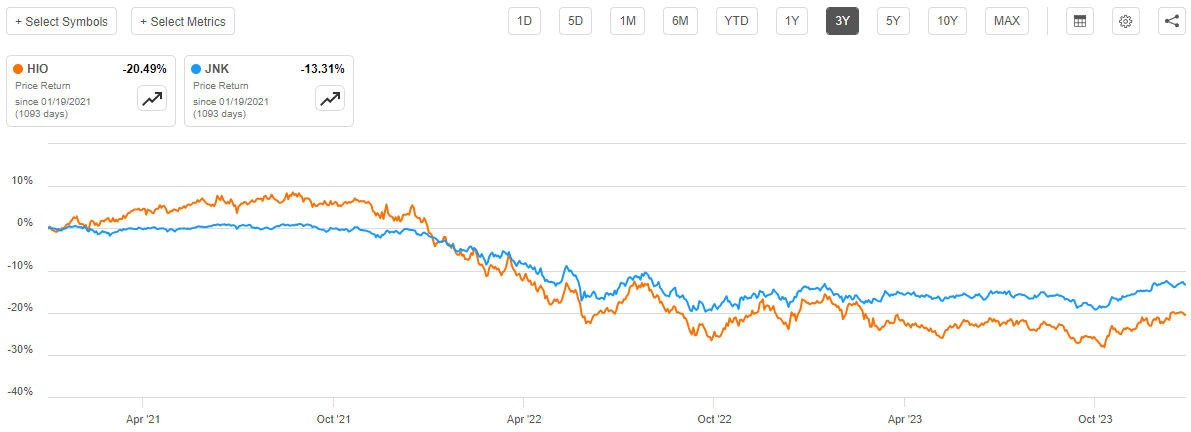

At first glance, the Western Asset High Income Opportunity Fund does not look especially impressive. The fund's share price has underperformed the Bloomberg High Yield Very Liquid Index ( JNK ) over the past three years. As we can clearly see here, the fund is down 20.49% compared to the 13.31% decline of the index:

{kind=link}

That seems especially disappointing for an unleveraged fund. The index itself does not use leverage, so we would not expect that the fund's share price would decline much more than the index, although some underperformance might be expected since the Western Asset High Income Opportunity Fund may be realizing capital gains that then get paid out. Index funds rarely realize gains on a fund level so that would not result in any outflow of capital.

However, as I have pointed out many times in the past, the distributions paid by a closed-end fund should always be taken into account as part of a performance analysis. This is because these funds tend to distribute both their capital gains and their investment income, which results in the distribution yield being significantly higher than most comparable index funds. These outsized distributions can fully or partially offset share price declines and always result in investors actually receiving a much higher level of performance than the share price alone would indicate. When we include the distributions in the performance chart, we see that investors in the Western Asset High Income Opportunity Fund actually did a bit better than investors in the index fund. Over the trailing three-year period, the Western Asset High Income Opportunity Fund delivered a 3.06% total return compared to a 2.35% total return for index investors:

{kind=link}

This performance is still very unlikely to turn the head of any investor. After all, a 3.06% return over an entire three-year period is not particularly impressive. A money market or high-yield savings account would have beaten that. However, the three-year period shown above was perhaps one of the most challenging periods for bonds that we have seen so far this century as the reversal from the incredibly loose monetary policy of the pandemic period to today's period of monetary tightening has wreaked a great deal of havoc on bond prices. Junk bonds at least have outperformed investment-grade corporates and government bonds, as both securities have such low yields that they were unable to offset the price declines.

Naturally, though, the fund's past performance is not nearly as important as its future performance. Let us discuss this fund now and see how promising it could be as an investment going forward.

About The Fund

According to the fund's website , the Western Asset High Income Opportunity Fund has the primary objective of providing its investors with a very high level of current income. This makes a great deal of sense considering that this is a bond fund that invests primarily in high-yield debt securities ("junk bonds"). According to CEF Connect, the fund currently has 97.03% of its assets invested in bonds with the remainder in things such as convertible securities and preferred stock. It also has a small allocation to cash:

CEF Connect

As I have mentioned in various previous articles, bonds are by their very nature current income vehicles. Investors purchase a bond at face value, receive a steady stream of coupon payments that serve as income, and then get the bond's face value back at maturity. There are no net capital gains over the bond's lifetime and the only net investment returns over the full term of the bond are the coupon payments. It is generally the same story with preferred stocks, except that they do not always have a maturity date. This is the reason why bonds and preferred stocks are generally called "fixed-income" securities.

The convertible bonds in the portfolio are a bit of a different story, as they can certainly deliver capital gains. This comes from the conversion feature, as these securities can be converted into common stocks under certain circumstances and these common stocks can deliver net capital gains over time. This is the only way that the fund's secondary objective of delivering capital appreciation makes sense, but the 1.51% allocation to convertible securities is too small for the fund to really be able to generate significant capital gains from these securities. This is particularly true because not all convertible securities end up becoming eligible for conversion.

The fund's website specifically mentions that the Western Asset High Income Opportunity Fund focuses on investing its assets in high-yield bonds. This is almost necessary for an unleveraged bond portfolio to deliver anything that most income-focused investors would consider to be an acceptable yield, especially over most of the past fifteen years or so.

For example, take a look at this chart, which shows the yield of the ten-year U.S. Treasury note (US10Y) over the past decade:

{kind=link}

As we can clearly see, over most of the period the note's yield was under 3.00% and it spent a good portion of the entire decade under 2.50%. That is a $25,000 annual income from a $1 million investment. I doubt that most people who managed to accumulate a $1 million portfolio over their careers would consider $25,000 per year to be a reasonable level of income. Investment-grade corporates are a bit higher than the ten-year Treasury, but even with those it was difficult to get much above a 4.00% yield over most of the last decade. Thus, junk bonds have been about the only reasonable option for income-seeking investors to earn the yields that they want. This is especially true considering that the incredibly low bond yields and rapid growth of the money supply pushed many investors into common stocks, pushing yields of those assets down.

Unfortunately, junk bonds have something of a bad reputation among many conservative investors and retirees because the issuers of these bonds are considered to have a very high risk of defaulting on their debt obligations. In that case, naturally, investors may not get their principal back and it becomes more difficult to replace lost principal the closer that one gets to retirement. The fact that the Western Asset High Income Opportunity Fund is investing primarily in junk bonds may thus worry some people. Fortunately, a look at the credit quality of the fund's portfolio may help to reduce some concerns. Here is a high-level overview:

{kind=link}

We immediately see that 19.85% of the fund's portfolio is invested in BBB-rated securities. These are actually investment-grade bonds, not junk bonds. We also see that 64.85% of the fund's assets are invested in securities rated either BB or B. Those are the two highest possible ratings for junk bonds. The official bond ratings scale says that companies whose securities are rated BB or B have sufficient financial strength to carry their existing debt obligations even in the event of a short-term economic shock, such as a recession. While BB and B-rated companies do not have quite as much financial strength as a company that is rated investment-grade, the risks of default should not be much higher unless the economy enters into a severe recession or something similar. Overall, 84.7% of the fund's portfolio is rated B or higher, so we can see that this fund is not investing in highly speculative bonds that have a very high-risk high-reward profile.

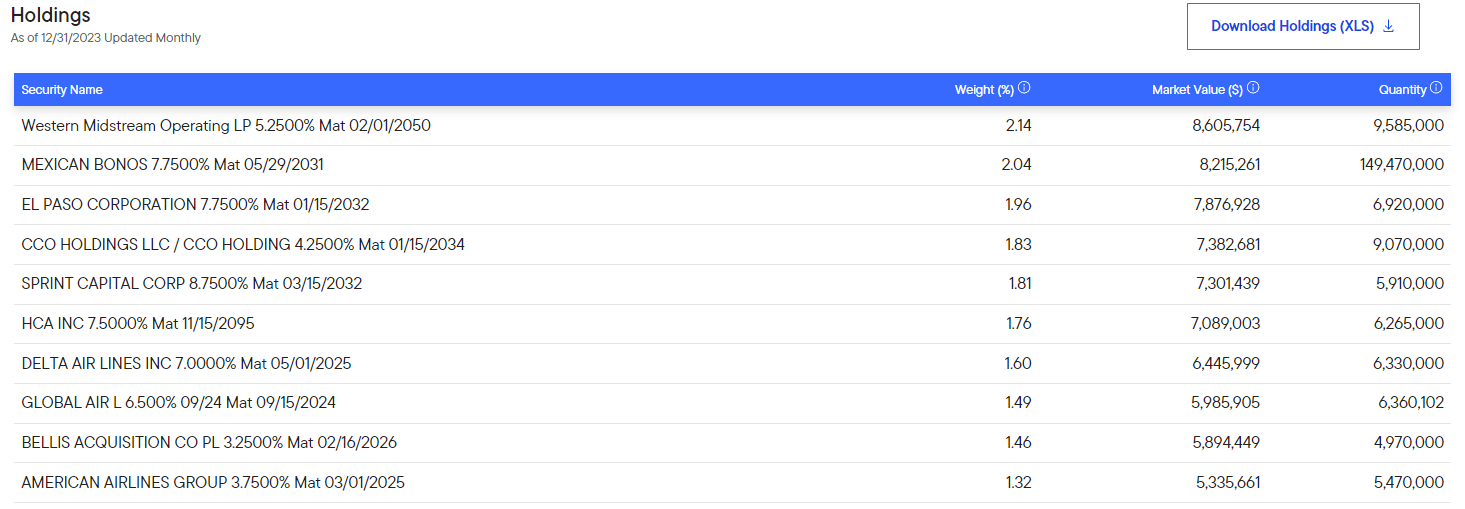

The fact that this fund is investing in higher-quality speculative-grade debt is not the only step that it is taking to limit the losses that its investors might suffer in the event of a default. The fund currently has 240 unique positions, which should result in any individual issuer only accounting for a very small percentage of the fund's total assets. Here are the largest issuers whose securities are included in the fund's portfolio:

{kind=link}

As we can see, the largest issuer with securities in the fund's portfolio is Western Midstream Partners ( WES ) and it only accounts for 2.14% of the fund's total assets. That is not an especially large position, as even a total loss from a position of this size would be quickly erased by the coupon payments that the fund receives from the other securities in the portfolio. The fund also has less than 20% exposure to every individual sector, so even problems that might affect a number of companies in a single sector (such as a cutback in consumer spending that causes problems for consumer discretionary companies) should not completely devastate the fund's portfolio.

Overall, the fund appears to have taken as many precautions as it realistically can to protect its investors against the risk of losses due to defaults. This is something that could be especially important today since Moody's Investor Service expects junk bond defaults to increase over the course of 2024. When we also consider that this fund is not using leverage, which would amplify its losses in the event of a default, we should be able to sleep relatively easily. The big risk here is interest rates, not defaults.

The Market Versus The Federal Reserve

Over most of the past decade, one of the most common statements among traders is that you "don't fight the Fed." However, the market appears to be doing that so far this year. As I have pointed out in a number of previous articles on other bond funds, the market is currently expecting that the Federal Reserve will cut interest rates at a fairly rapid pace this year. As of right now, the market is expecting about six interest rate cuts in 2024. Yesterday's speech by Federal Reserve governor Chris Waller did reduce the expected terminal rate in the Fed futures market by six basis points, but the market is still basically expecting that the Federal Reserve Open Market Committee will cut interest rates at all but one of its meetings after the first 25 or 50-basis point rate cut in March.

This morning's strong retail sales data, when combined with last week's still-hot inflation report, reduces the possibility of such a near-term interest rate cut. For those who missed the news, this morning's retail sales report showed that the American consumer continued to remain strong and increased spending by 0.6% month-over-month. That is higher than the 0.4% Bloomberg consensus and clearly shows that the interest rate increases that the Federal Reserve imposed on the economy over the course of 2022 and the first half of 2023 have not yet had the desired effect of cooling off the economy. Indeed, the economy has thus far been very resistant to the rising costs of obtaining credit, with recent reports actually suggesting that it has been improving over the past two months.

It is very difficult to see how the Federal Reserve can justify cutting interest rates six times in 2024 when economic data is coming in as strongly as it is. This is particularly true considering that 2024 is an election year, and so any significant shift in monetary policy will be viewed as an attempt to either help or hinder the incumbent party politically. The Federal Reserve has historically attempted to avoid such accusations of partisan interference.

As bonds have priced in the market's expectations of six rate cuts in 2024 with the first one coming in March, any failure on the part of the Federal Reserve to deliver that will almost certainly punish bond prices. That is the most likely scenario right now unless something goes seriously wrong with the financial system, such as a crisis in the repo market (see here ). This scenario would cause the shares of the Western Asset High Income Opportunity Fund to decline from today's levels as the bonds that are held by the fund decline in price.

With that said, the fund's lack of leverage should help it in such a decline. As I have pointed out in various previous articles, the use of leverage amplifies a fund's losses when the price of the assets in its portfolio declines. In theory, then, this fund's net asset value should hold up a bit better than its leveraged peers in a market correction that accompanies the failure of the Federal Reserve to cut interest rates to the degree that the market expects. After all, this fund does not have the effects of leverage amplifying its losses.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Western Asset High Income Opportunity Fund is to provide its investors with a very high level of current income. In pursuance of that objective, the fund invests in a portfolio that primarily consists of junk bonds. These securities deliver the bulk of their investment returns in the form of direct payments made to their owners. In this case, that would be the fund. The fund pools all of the coupon payments that it receives from its bonds and combines them with any capital gains that it manages to generate from the price fluctuations that accompany changes in interest rates. It then pays all of the money in the pool out to its investors, net of its own expenses. Junk bonds tend to have fairly high yields, especially in today's high-interest rate environment. As such, we might assume that the fund's business model would result in the fund's shares boasting a very high yield.

This is certainly the case, as the Western Asset High Income Opportunity Fund pays a monthly distribution of $0.0355 per share ($0.426 per share annually), which gives it a 10.87% yield annually. This is a higher yield than that possessed by most other junk bond closed-end funds, which is very surprising considering that this fund does not employ leverage to boost the effective yield that it receives from the assets in its portfolio. Unfortunately, this fund has not been especially consistent with respect to its distribution over its history. As we can see here, the fund has both raised and cut its distribution numerous times over its thirty-year history:

{kind=link}

The fact that the fund's distribution has varied to such a degree over its lifetime might be something of a turn-off for any investor who is seeking to earn a high level of income from the assets in their portfolios. However, the fund did increase its payout back in October of 2023 so that might improve its perception among some investors. The real concern here though is that today's inflationary environment has rapidly increased the cost of maintaining a certain lifestyle, so we need more income to cover our bills than we did a few years ago. This fund's recent distribution hike helps a lot here, but its unreliability over the long term could lead some readers to believe that they cannot depend on it.

However, the fund's history is not necessarily the most important thing for anyone who is considering purchasing the fund's shares today. After all, anyone who purchases the fund today will receive the current distribution at the current yield and will not be affected by any events that have occurred in the past. The most important thing for anyone considering purchasing the fund today is its ability to sustain its distribution at the current level. Let us investigate this.

Fortunately, we have a fairly recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund's most current financial report corresponds to the full-year period that ended on September 30, 2023. This is nice because it can give us a good idea of how well the fund managed to perform in a number of widely disparate market environments. For example, both the last quarter of 2022 and the summer of 2023 were characterized by periods of pessimism in which bond yields were generally rising and prices were falling. That probably caused the fund to take some losses. The exact opposite was the case in the first half of 2023, which was a period in which investors were expecting that the Federal Reserve would cut interest rates in the second half of 2023 and were bidding up bond prices in an attempt to front-run the pivot. While the market proved to be wrong about the pivot, it still provided the fund with the opportunity to make some profits. This report should show us how well the fund managed to avoid losses and take advantage of the market opportunities that it was presented with over the period.

During the full-year period, the Western Asset High Income Opportunity Fund received $37,222,667 in interest and $107,775 in dividends from the assets in its portfolio. We deduct foreign withholding taxes from these amounts to arrive at a total investment income of $37,314,892 over the year. The fund paid its expenses out of this amount, which left it with $33,461,263 available for shareholders. That was, unfortunately, not enough to cover the $34,758,763 that the fund paid out in distributions during the period. It did manage to get very close to fully covering its distributions, but this still might be somewhat concerning as we would prefer a fixed-income fund to fully cover its distributions with net investment income.

However, there are other methods through which the fund can obtain the money that it needs to cover its distributions. For example, it might be able to make some profits by trading bonds and exploiting the price fluctuations that frequently occur in the capital markets. Unfortunately, the fund had mixed results in this task during the period. It reported net realized losses of $39,654,795 that were only partially offset by net unrealized gains of $34,302,918 over the period. Overall, the fund's net assets decreased by $6,649,377 over the full-year period after accounting for all inflows and outflows.

The fund also experienced declining net assets during the previous full-year period. In the full-year period that ended on September 30, 2022, the fund's net assets declined by $116,504,941 after accounting for all inflows and outflows. This is not sustainable over any sort of extended period since the lower the fund's assets, the greater the return that it needs to earn in order to maintain the distribution at a given level. Naturally, the higher the required return, the more difficult it is to achieve.

With that said, we probably do not have to worry about a distribution cut in the near term. The fund came very close to covering its distribution in the most recent period solely out of net investment income and it seems likely that its income improved a bit since junk bond yields increased over that full-year period. The fund's management also saw fit to increase its distribution, which was a very timely increase as the recent market excitement has undoubtedly provided the fund with the opportunity to make some trading profits. As such, we should not need to worry about the sustainability of the distribution for now.

Valuation

As of January 16, 2024 (the most recent date for which data is available as of the time of writing), the Western Asset High Income Opportunity Fund has a net asset value of $4.26 per share but the shares trade for $3.91 each. This gives the fund's shares an 8.22% discount on net asset value at the current price. This is not as attractive as the 10.44% discount that the shares have had on average over the past month, so potential investors might be best off waiting until the price becomes a bit more attractive before buying shares.

Conclusion

In conclusion, the Western Asset High Income Opportunity Fund looks like a very solid junk bond fund for the current environment. The fund has a great deal of both issuer and sector diversification and appears to have taken reasonable precautions to protect its investors against the risk of defaults.

It does seem likely that the fund's shares will decline in the near future, as economic data continues to come in very strong, which suggests that the Federal Reserve will not deliver the rate cuts that are currently priced into bonds. However, this fund's lack of leverage should help it hold up a bit better in such an environment. As such, investors might not want to be as quick to dump this fund as some of its peers. It is probably a good idea to keep some exposure to assets that will benefit from rate cuts and this fund appears to be one of the better ways to do that.

For further details see:

HIO: One Of The Better Junk Bond CEFs With A Double-Digit Yield