HQI - HireQuest: Short-Term Worries Have Created An Opportunity

2023-08-15 13:03:49 ET

Summary

- I am upgrading HireQuest to a buy with a $30 price target based on my 2024 EBITDA estimate of $21.68 million and a 20x EBITDA multiple.

- This opportunity is available as the stock dropped sharply due to disappointing Q2 earnings were released and negative comments about Q3 and Q4 from CEO Rick Hermanns.

- I believe this drop also occurred due to some investors losing patience as they were waiting for expenses to roll off from the MRI acquisition.

- The long-term story has not changed, however. HireQuest still has a superior business model and a history of superior capital allocation, so it deserves a premium earnings multiple.

I initiated coverage of HireQuest, Inc. ( HQI ) with a hold rating despite acknowledging the fact that the stock likely deserves to trade at a high earnings multiple due to its superior business model and history of high returns on acquisitions.

Also in that report, I mentioned some of the near term risks given its high multiple and the economic uncertainties on the horizon. I wrote that “there is some chance of an upcoming crack in the labor market and if this weakness leads to a decline in earnings for HireQuest, I expect its earnings multiple to correct and the stock to drop in a big way as it is a large divergence from what the market expects.” This scenario occurred and affected Q2 earnings quite negatively. The stock also fell 25% the day these results were announced and erased most of the YTD gains.

Much of this drop can be attributed to the decline in earnings but I also believe it is due to the MRI profitability narrative losing its strength. I think a portion of HireQuest’s investor base was likely holding due to the story that the MRI acquisition would lead to better profitability as HireQuest would be able to revitalize MRI’s franchise base which had been declining prior to the acquisition. The poor results from this quarter have likely caused some investors to throw in the towel. It’s one thing to be patient with an acquisition when growth is strong, it’s another thing to be patient when growth slows due to a weaker economy.

I don’t believe this story is over and I don't believe the MRI acquisition was a mistake, but more impatient investors may have been expecting benefits from the acquisition to occur at a faster pace.

In the report, I also wrote that “a bad recession may be good for HireQuest in the long run as it will allow them to acquire struggling staffing firms at low prices. This would make an investment in HireQuest at that point even more lucrative.” We are currently at that point. As my thoughts on the quality of HireQuest’s business model and superior management have not changed, I am upgrading the stock to a buy with a price target of $30 based on my FY2024 EBITDA estimate of $21.68 million and a 20x EBITDA multiple.

Q2 Update

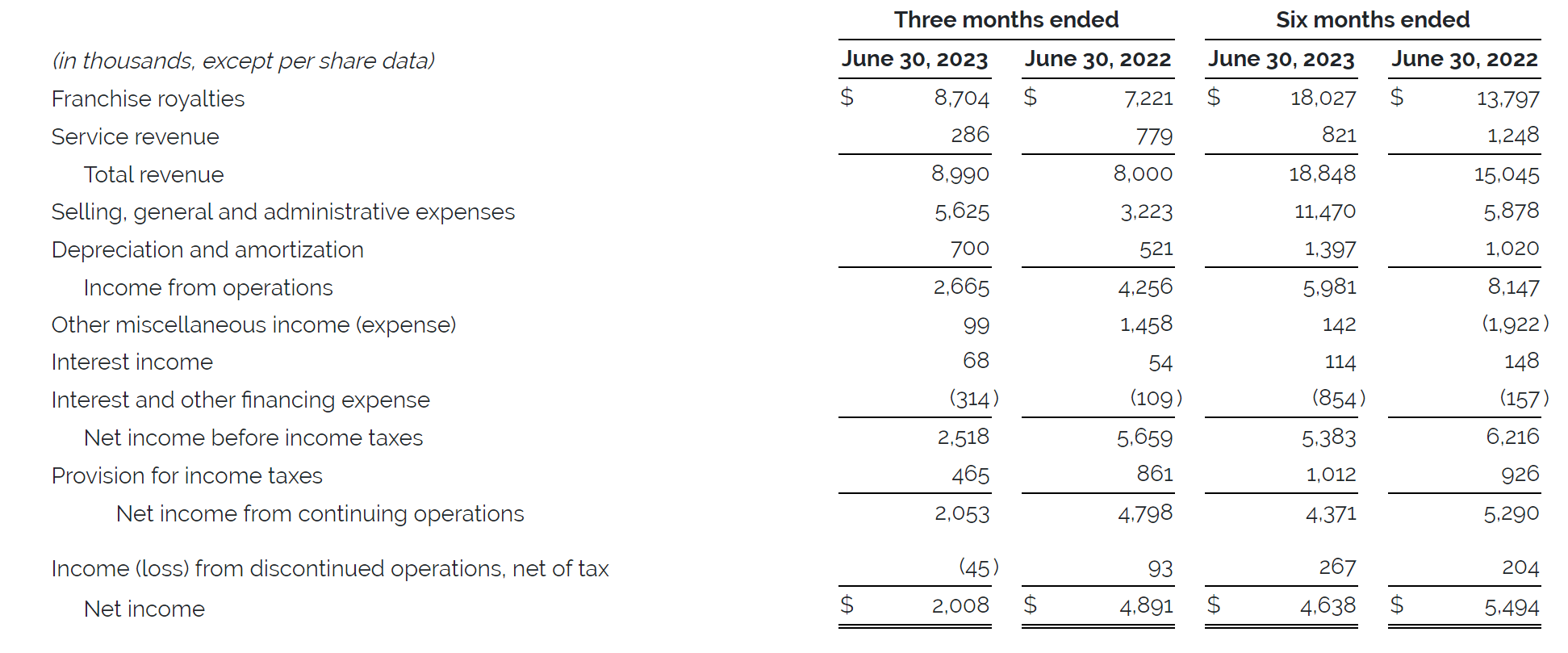

While revenue increased 12% year over year to $9 million in Q2, operating income dropped 37% to $2.7 million. This combination of higher revenue and lower operating income is primarily due to higher system-wide sales from the MRI acquisition, higher workers comp related expenses, and lingering costs that have yet to roll off from the MRI acquisition.

HireQuest Q2 Financial Results (Q2 2023 Earnings Press Release)

{kind=link}

Despite revenue being up, there was a 6% decline in revenue from existing staffing offices. This information was likely not welcomed by investors. CEO Rick Hermanns pointed out that this result was much better relative to other staffing firms due to HireQuest’s franchise model which incentivizes organic growth, and due to HireQuest’s high concentration of franchises in Florida and Texas, which have stronger economies relative to other states.

Investors were likely further spooked when Hermanns answered a question about demand in the third and fourth quarters:

I haven't seen anything in this quarter or and really don't see anything coming from the Fed that would get me to believe that we're going to get relief any time before the end of the year. And so I think that -- I don't see that at least from internal growth. I don't see that recovering until the economy begins to recover. And even I remember sitting probably in a call at the end of the year, it's kind of like, look, you can't forecast what the economy is going to do, and we are definitely susceptible to it. But all that being said is, I don't expect our same-store sales to improve any time before the end of the year. I'm not seeing it. But if something happens where the economy does turn, we'll be right with it.

This type of candor regarding a difficult subject is great to see from a CEO even if the answer did not provide any comfort.

Besides the many demand related questions, costs in the third and fourth quarters were a point of emphasis on the earnings conference call. Hermanns mentioned in his prepared remarks that Q2 SG&A expenses not including workers compensation related expenses were sequentially lower than Q1 SG&A by $600 thousand despite total revenue being only $300 thousand lower, implying that SG&A expenses are trending down. The following is the relevant excerpt from the call:

As we continue to integrate MRI and drive synergies across our business, we expect to bring expenses down over the balance of the year. In the second quarter, we continued to make progress and excluding the effect of workers' compensation insurance, Q2 SG&A was approximately $4.9 million compared to $5.7 million in Q1. We just want to make sure that we drive synergies thoughtfully and in a sustained fashion.

Additionally, Hermanns mentioned that all cost cutting measures will be felt in full by Q4 although overall SG&A will be higher on a year over year basis due to standard expenses from MRI. This will be relevant in my FY2023 and FY2024 forecast below.

Cash flows were lower due to lower operating income and negative effects from working capital changes but I don’t think investors are worried about HireQuest’s conversion of earnings to cash flow going forward. The story investors will be focused on for the next 6-18 months will be the stabilization of HireQuest revenue ex-MRI, normalization of expenses as MRI is fully integrated, and how these factors translate into EBITDA.

Forecast and Valuation

The following estimates are mainly based on prior trends in HireQuest’s financials, and commentary from Rick Hermanns from the most recent earnings call.

On the call, Hermanns mentioned that Q3 revenue will increase sequentially as it normally does although to a lesser extent than in the past, that workers compensation expense will start to decline in Q3 and Q4, and that Q4 SG&A expenses will have all costs cuts taken into account. With these guideposts, I am predicting H2 2023 revenue of $19.1 million, workers comp expense of $600 thousand, SG&A expenses ex-workers comp equal to $9.13 million and D&A equal to $1.6 million. This would lead to FY2023 EBITDA of $16.79 million.

For 2024, before any acquisitions, I am assuming revenue is the same as 2023 at $37.98 million, SG&A expenses (including workers compensation expenses) are 45% of revenue, and D&A is equal to $3.5 million. This would lead to FY2024 EBITDA of $20.88 million.

I could end my forecast here but Hermanns mentioned that he believes there will be another acquisition in the next 12 months so I am adding a small acquisition into my estimates. Based on his comments about being able to integrate a small acquisition without adding many costs, I am assuming HireQuest makes a $2 million acquisition on a firm doing $30 million in system-wide sales. With a 4x EBITDA purchase price, I assume this acquisition would be immediately accretive to EBITDA to the tune of $500 thousand.

Adding this to my estimate leads me to forecast EBITDA of $21.38 million in FY 2024. With a 20x multiple, HireQuest’s EV would be $433 million. Assuming they hold $5 million in cash, they reduce short-term borrowings to $12 million from $16 million, and there are 14 million fully diluted shares outstanding by the end of 2024, HireQuest’s equity would trade for $30 per share.

HireQuest Forecast and Price Target (Created by Author)

A 20x multiple is high, but HireQuest’s long term quality metrics remain the same and it is in line with past multiples.

Risks

The risks going forward are once again related to the economy. HireQuest is still trading at a relatively high trailing twelve months EBITDA multiple, and an even higher forward EBITDA multiple. Despite the fact that the stock is somewhat de-risked as investor expectations are lower, further weakness in the job market is a big possibility.

This is difficult to predict because much of the staffing market weakness is attributable to weakness in the IT sector, which has recently been one of the weakest labor market sectors. This could lead to a staggered effect with relative strength in the IT sector as the economy laps the weakness from 2022 and 2023, and relative weakness in other sectors that are currently stronger. These complications make it easier to take more of a business first approach to valuing HireQuest, as over the long term, sustainability of business quality metrics such as ROIC and capital allocation will drive the stock.

While a longer term holding period for HireQuest could bail investors out of short-term volatility there are also issues that come with business size, as the larger HireQuest, is the more difficult it will be to make accretive acquisitions.

The MRI acquisition, while successful, led to concerns from investors about costs and short-term borrowings, especially in a period with economic weakness. HireQuest will be forced to make larger acquisitions as they grow and this will be far more difficult to do efficiently, even for proven capital allocators like Rick Hermanns and HireQuest’s management team. Future acquisitions could fall short of the typical hurdle rate and could lead to longer periods of earnings volatility.

Final Thoughts

HireQuest hit a speed bump in Q2 2023 as a decline in existing staffing revenue, and higher expenses led to a steep decline in operating income. This led to a sharp decline in the stock as the profitability narrative of the MRI acquisition grew weaker and comments from Rick Hermanns regarding a potential bounce back in Q3 and Q4 did not provide any comfort.

Despite this, the long-term story regarding the higher quality business model and superior capital allocation has not changed and I believe these short term worries are providing an opportunity for investors to buy HireQuest at an attractive price. I am upgrading HireQuest to a buy with a $30 price target based on my 2024 EBITDA estimate of $21.68 million and a 20x EBITDA multiple.

For further details see:

HireQuest: Short-Term Worries Have Created An Opportunity