RHI - HireQuest: Trading At A Premium Multiple For A Reason

2023-06-19 02:34:46 ET

Summary

- HireQuest trades at a premium earnings multiple compared to its industry peers. I think it deserves this premium.

- This premium is mainly due to its historic and expected high return on invested capital, and its growth going forward.

- Despite this, I don’t think an investment at this multiple compensates investors enough for the risk of a bad recession that would cause a spike in unemployment.

- In this article, I'll compare HireQuest to Robert Half and Heidrick & Struggles in order to make this point.

The secret regarding HireQuest, Inc. ( HQI ) is out. It operates a higher margin business model, it is run by owner operators with a history of smart capital allocation, and it has a long runway for growth as it continues to consolidate the fragmented staffing industry.

I say the secret is out because the stock has gone up more than 100% over the past 12 months, partly due to earnings growth but also due in large part to multiple expansion. In that time HireQuest's GAAP EV/EBIT multiple has increased from 12x to 24x. Even when using HireQuest's trailing twelve months adjusted EBITDA of $21.4m which subtracts stock-based comp and charges related to the most recent acquisition, the multiple is still quite high.

Does HQI deserve a premium multiple over its peers? I think it does. Its franchise model is higher margin and leads to recurring revenue streams that are more predictable. In addition to this, the company has a history of acquiring smaller staffing companies and integrating them into HireQuest's ecosystem very efficiently. Consolidating the staffing industry is what will lead to long-term growth so the ability to do this effectively deserves a premium. This efficient integration of acquisitions is in large part due to an experienced CEO and management team that also owns a large portion of HireQuest's equity. Good capital allocation with aligned management absolutely deserves a premium.

But I am also wary of just how large that premium is over its industry peers. Earnings multiples are functions of return on invested capital ((ROIC)), growth, cost of capital and tax rates. When comparing multiples between companies within the same industry, cost of capital and tax rates are generally similar so growth and ROIC will be the main drivers of its multiple compared to industry peers.

When taking these factors into account, I think HireQuest deserves to be trading at a premium. In this article, I will go into more detail on why this is the case. I will compare growth, ROIC and return on incrementally invested capital (ROIIC) between HireQuest, Robert Half International Inc. ( RHI ), and Heidrick & Struggles International, Inc. ( HSII ), two peers within the staffing industry.

HireQuest's Differentiated Business Model

HireQuest differs from most other large publicly traded staffing companies in that it practices a franchise model. This leads to many benefits including better expense control, more aligned incentives with operators of the franchises and more of a recurring stream of revenue. This also works well with an acquisition model as it makes integrations of new acquisitions much more straightforward and cost efficient.

This is not only true in theory but has been proven in practice. HireQuest has a history of earning high returns on acquisitions up to this point and the low cost model was especially beneficial in 2020 during the peak of the pandemic as they maintained a high operating margin despite a decline in revenue.

In addition to the business model that allows for these efficiencies, HireQuest's CEO, Rick Hermanns, has years of industry experience and a history of making smart acquisitions as seen by the fantastic financial results over the past few years. Since 2019, revenue has grown at a 24% CAGR, operating income has grown at a 20% CAGR and the share count has only grown at 5% CAGR. The best part about this performance is that it's an asset-light business and there is little to no maintenance capital expenditures required to maintain these earnings. This means that these earnings convert very well to free cash flow.

To continue growing however, they will need to spend cash on acquisitions. But as long as the return on these acquisitions continues to be well above and beyond the cost of capital, management is creating value for shareholders.

The market has recognized this value creation as the stock has risen 300%+ since the end of 2019. This is in part due to the growth in earnings per share discussed above but also due to multiple expansion. In mid-2020, HireQuest was trading at a trailing 12 month GAAP EV/EBIT ratio of around 10 compared to the current GAAP EV/EBIT of 25. The current ratio includes one-off charges related to the most recent MRI acquisition, but even if we add back those expenses, the current EV/EBIT ratio is 21.5. I will go into why this multiple is deserved below.

Valuation

As I mentioned above, earnings multiples are determined by growth, ROIC, cost of capital and taxes. Because cost of capital and taxes are generally similar among peers from the same industry, the difference in the earnings multiple between HireQuest, Robert Half and Heidrick & Struggles should be largely determined by growth and ROIC.

The following are the trailing 12 month GAAP EV/EBIT multiples for the 3 companies:

| HireQuest |

| 24.90 |

| Heidrick & Struggles |

| 4.00 |

| Robert Half |

| 8.75 |

I already described HireQuest's growth and ROIC story above, so I will briefly touch on Heidrick & Struggles, and Robert Half below. As a note, all of my ROIC calculations include goodwill and other intangible assets as acquisitions are a necessary part of growth for these businesses.

Heidrick & Struggles

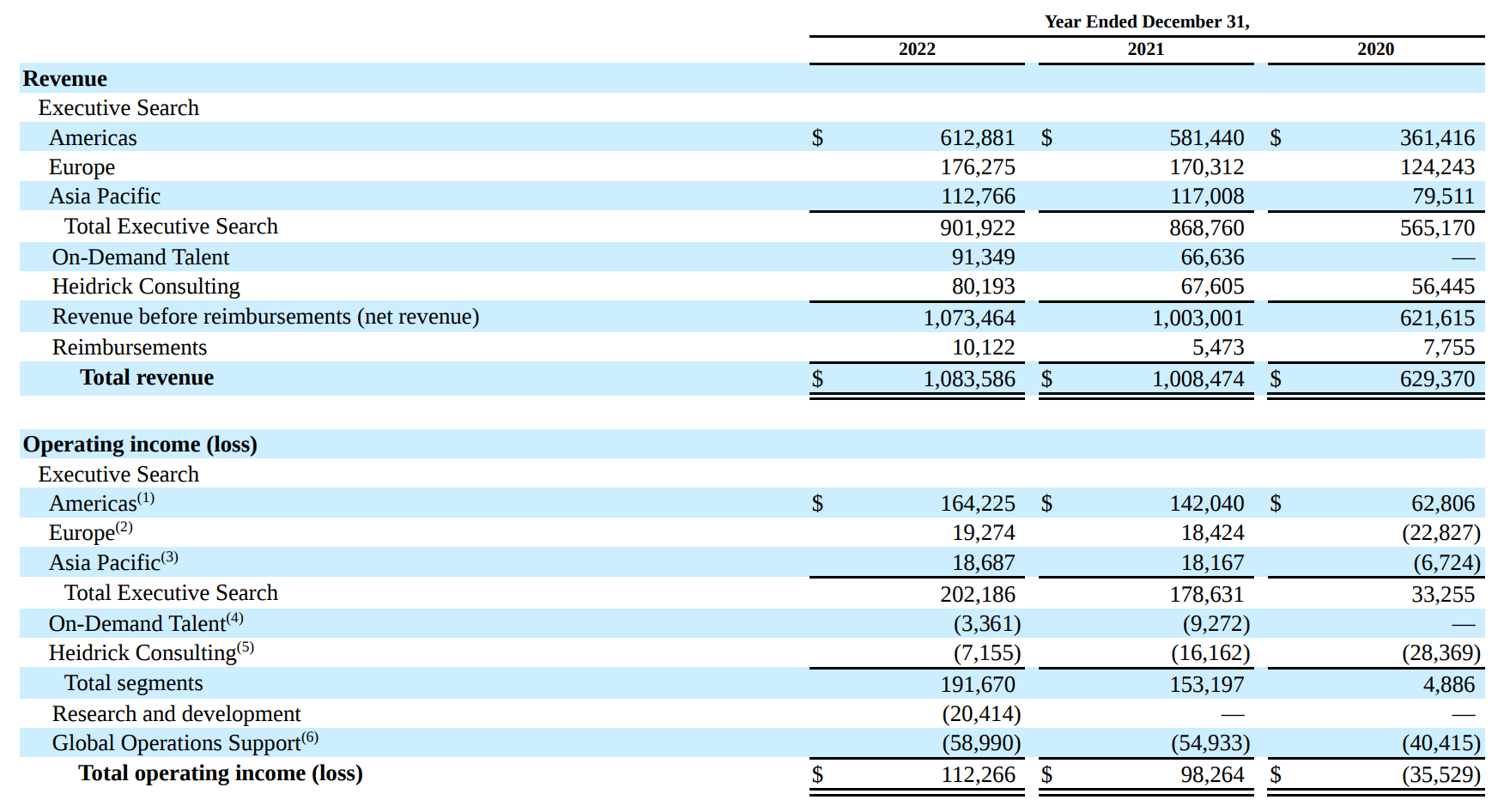

In 2022, I calculated Heidrick & Struggles' ROIC to be 21%. While this looks high, much of this return is based on old assets that earn high returns. Recently, the company has been expanding into new segments besides staffing and these new segments are losing money.

Heidrick and Struggles Results by Segment (Heidrick and Struggles 2022 Annual Report)

{kind=link}

All of the recent acquisitions have been going towards these newer segments so even though ROIC is high due to older assets generating high returns, returns on new acquisitions are far below the cost of capital and destroying value for shareholders. Along with this, revenue and earnings declined in Q1 2023.

The market recognizes the low growth ahead and the likelihood that value destructing capital allocation decisions will continue and is correctly assigning a low multiple to the stock. This is despite the fact that they grew revenue and earnings from 2019-2022.

Robert Half

For 2022, I calculated Robert Half's ROIC to be 47%. This is very high. Revenue has grown at a 5% CAGR since 2019 but earnings have grown at a 15% CAGR in that same time so most of the earnings growth has come from margin expansion. However in Q1 2023, revenue declined 5% year over year while earnings declined 27% so it seems that whatever operating leverage Robert Half has gained over the past few years reversed quite quickly.

Despite the history of a high ROIC, the market is seeing the revenue decline and earnings decline which will lead to lower ROIC going forward. No growth and lower ROIC, despite being above the cost of capital, leads to a lower multiple.

Comparing the Three

I calculated HireQuest's 2022 ROIC to be 46%, the same as Robert Half's and much higher than Heidrick & Struggles. However HireQuest saw 30% year over year revenue growth in Q1 2023 compared to a decline in revenue for the others. This growth came with a decline in earnings due to the integration of the most recent acquisition, MRI, but management claims that these inefficiencies will be resolved. The market clearly believes this given the currently high multiple.

Time will tell if this multiple is warranted. There is some chance of an upcoming crack in the labor market and if this weakness leads to a decline in earnings for HireQuest, I expect its earnings multiple to correct and the stock to drop in a big way as it is a large divergence from what the market expects. However, if HireQuest can continue to grow as it has in the past despite labor market weakness, integrate MRI effectively, and continue to make acquisitions at a high rate of return, this stock looks undervalued.

For a price target, I will create three scenarios for EBIT and an EV/EBIT multiple in 2025, assign a probability to each and add the expected values. In the first, HireQuest grows EBIT at 10% per year and ends up with a EV/EBIT multiple of 15. In the second, EBIT grows at 15% and the final multiple is 20. And third, EBIT grows 20% per year and the final multiple is 25. The enterprise values in the scenarios are $335m, $510m and $725m respectively.

Assigning a 50% probability to the 10% growth scenario, a 30% probability to the 15% growth scenario and a 20% probability to the 20% growth scenario leads to an expected enterprise value of $465m. Compared to the current $339m EV this does not provide adequate returns to warrant an investment.

I am assigning a higher probability to the lowest growth scenario to be conservative and to account for what I believe is a high risk of labor market weakness in the second half of this year and in 2024. If you disagree with that, you may assign different probabilities. But the main point I am trying to make is that I don't think an investment at the current multiple of earnings provides enough reward for the potential risk of a bad recession.

Final Thoughts

HireQuest trades at a premium multiple compared to its peers. This premium is due to the market believing that HireQuest will be able to grow and maintain a high ROIC going forward despite any labor market weakness that may be upcoming.

I personally don't feel comfortable building a position in HireQuest while it trades at this premium multiple. I understand those that wish to hold it if they have owned it for some time but I don't think an investment at this multiple compensates me enough for the risk of a bad recession that would cause a spike in unemployment thus a decline in HireQuest's earnings. However, I understand the quality of HireQuest's business model and the quality of its management team so I will surely revisit if the multiple declines or if that bad recession occurs.

I may miss out on good returns over the next few years by not investing now but I don't think the risk/reward is in my favor at this point, given the potential upcoming economic risks.

Ironically, a bad recession may be good for HireQuest in the long run as it will allow them to acquire struggling staffing firms at low prices. This would make an investment in HireQuest at that point even more lucrative.

For further details see:

HireQuest: Trading At A Premium Multiple For A Reason