HIVE - HIVE Blockchain: Market Mispricing Ethereum Merge

Summary

- Though it fluctuates with the relative prices of Bitcoin and Ethereum, about a third of HIVE's mining revenues in June came from Ethereum.

- HIVE's Ethereum mining equipment cannot be transitioned to another equally as profitable business segment. And the relatively large Ethereum revenue stream cannot be easily replaced.

- From a market cap to hash rate perspective, HIVE shares do not appear to be pricing in The Merge.

- HIVE's adjusted costs and expenses, excluding depreciation, share-based compensation, interest expense, impairments, and foreign exchange losses are about $15,000 per coin.

After years of delays, the Ethereum ( ETH-USD ) platform appears set in the coming weeks to shift from a proof-of-work consensus mechanism for verifying and tracking transactions, to a proof-of-stake consensus. Follow-up over the last couple of weeks of a practice merge on the Goerli testnet showed it was successful and a sufficient final test to now move to The Merge on the mainnet. The first step will begin on September 6th, with the final transition estimated for September 15th. This switch will mark a seminal moment for the crypto space because of the history, size, and complexity of the platform.

The Merge will be a catalyst for change across the industry. For the highly profitable Ethereum miners, the shift will be the end of an era as their computational computer equipment will no longer be used to secure the network. Under the new proof-of-stake consensus, more simple computer nodes "holding" substantial amounts of ETH are trusted and rewarded for validating and securing the platform.

Chief among the large, NASDAQ listed crypto miners with a sizeable Ethereum business is HIVE Blockchain ( HIVE ). Though it fluctuates with the relative prices of Bitcoin ( BTC-USD ) and Ethereum, about a third of HIVE's mining revenues in June came from Ethereum. For comparison, about 10% of Hut 8's ( HUT ) mining revenues are Ethereum based.

Also important to note, since 2021 Ethereum mining has generally had a higher margin than Bitcoin mining. This has given Ethereum miners one advantage in cost comparisons to Bitcoin-only miners. Lastly for reference, over the past year HIVE has had about three-quarters of a percent of the total Ethereum hash rate, a sizable share.

So HIVE is particularly dependent on Ethereum mining. However the specific equipment used cannot be transitioned to another equally as profitable mining opportunity or business segment. And the relatively large revenue stream cannot be easily replaced, affecting HIVE's earnings outlook. A section below considers the details of some of the options HIVE and Ethereum miners have for their GPU equipment and power sources. While estimates do vary, from my perspective a majority of the Ethereum revenues and earnings will not be replaced in the coming quarters.

However before this outlook and path forward discussion, it is necessary to show that this coming disruption to revenues and earnings has not been priced into the shares. First and foremost, HIVE is not relatively cheap from the commonly used metric of market cap to hash rate. This is especially true as HIVE's hash rate will take the largest hit among the larger-cap, western miners following a successful merge on the Ethereum platform.

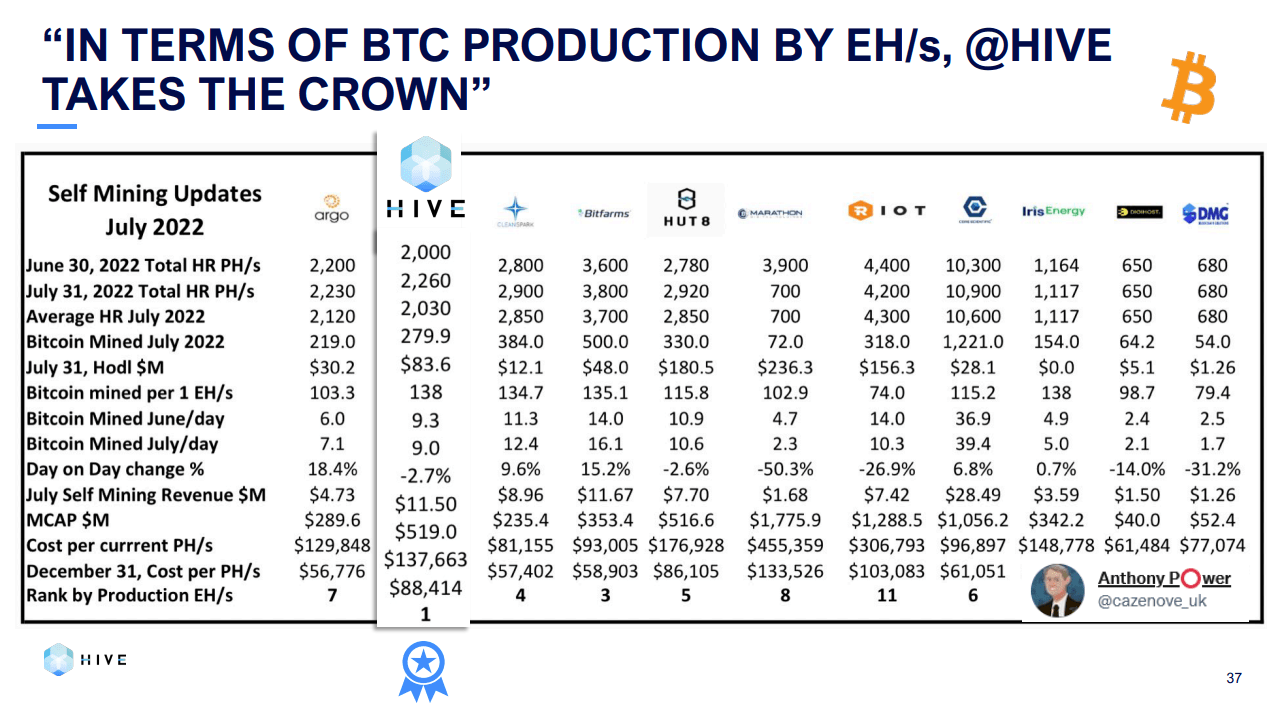

Consider the following slide from HIVE's Q1 F2023 Results Webcast . Note the internal data graphic is from Anthony Power with Compass Mining.

www.hiveblockchain.com/investors/presentation/

{kind=link}

The main point of the slide shows that HIVE has the highest production relative to its operational hash rate, as seen in the "Bitcoin mined per 1 EH/s" metric. This metric is a good measure of efficiency and uptime.

However for the current discussion, focus on the "July 31, 2022 Total HR PH/s", "MCAP ", and "Cost per current PH/s" metrics. These metrics form a market cap to production capacity comparison that is the starting point for relative valuations of the crypto miners. Of course, there are other meaningful valuation factors at play such as balance sheet strength and hash rate growth trajectory. Bear those considerations in mind, but set them aside for the moment.

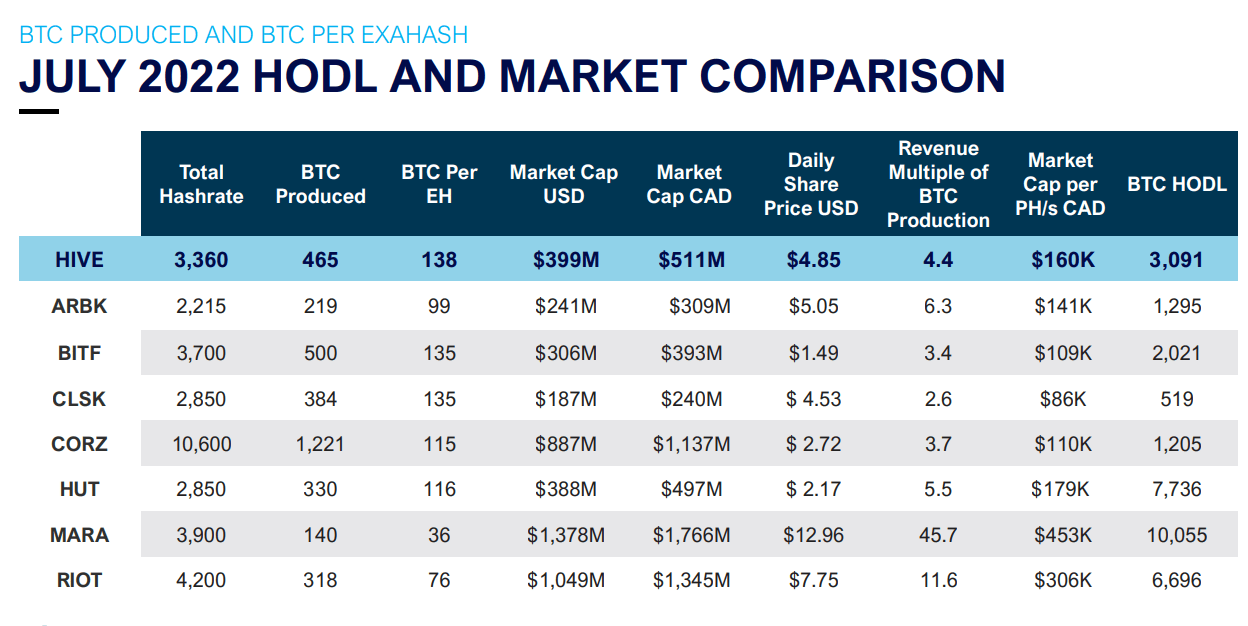

With a few exceptions in the table above, one can divide the MCAP by the July Hash Rate to get the "cost" per PH/s. So importantly, this cost is not related to an operational cost, but rather the cost a shareholder theoretically pays per unit of production. At $137,663 per PH/s, HIVE falls somewhat in the middle.

First lets quickly go over the exceptions in the calculations above. The cost per PH/s for Marathon Digital ( MARA ) uses its installed capacity rather than July Hash Rate as the company experienced major disruptions at their two largest facilities in July. The Iris Energy ( IREN ) calculation has also been adjusted, though I am not familiar enough with their operations to explain.

Lastly and most importantly, for fairness HIVE's calculation has been adjusted to include its Ethereum production. Often for ease of use, the differently denominated Ethereum production figures are converted to a Bitcoin equivalent. In July for HIVE, Ethereum mining represented about 1550 PH/s of Bitcoin equivalent hash rate and 40% of the total. So rather than using the 2260 PH/s of Bitcoin production capacity in July, the total Bitcoin equivalent hash rate of 3770 PH/s was used in the calculation above. Put more plainly, the $519,000,000 market cap was divided by 3770 PH/S to get the cost per PH/s of $137,663.

The upshot, assuming HIVE's Ethereum mining ends in September, is that HIVE's stock looks substantially more expensive from a market cap to hash rate perspective. Assuming the extreme, with no replacement hash rate source, the cost per PH/s goes to about $230,000 (more on replacement options below). In any case, from a market cap to hash rate perspective, HIVE shares do not appear to be pricing in The Merge.

As they are Canada based, have similarly size power supplies, hash rates and market caps, HIVE is often compared to Hut 8 and Bitfarms ( BITF ). Note Bitfarms has no Ethereum mining while Hut 8 has about 10% of its revenues from Ethereum.

Comparative Hash Rates and Power Supplies (www.hiveblockchain.com/investors/presentation/)

{kind=link}

The graph directly below shows the price movements in the three companies since early July when the successful merger on the Sepolia testnet brought more heightened certainty to a near term merge on Ethereum's mainnet. There was no discernible downward reaction in the relative pricing of HIVE.

The graphic below shows the price movements since last year's successful London hard fork on the Ethereum platform. The London hard fork was an important point on the path to transitioning to a proof-of-stake. And here there is no discernible, growing divergence in valuations during the intervening period of increasing expectations of The Merge.

For consideration below, the normalized price change compared to Bitcoin-only miners Riot Blockchain ( RIOT ) and Marathon Digital over the past year are included. Note the continued, close correlation between HIVE and Marathon Digital.

So in general, as seen in the market cap to hash rate comparisons above, HIVE seems priced to include its Ethereum production. And when compared to the Bitcoin-only miners, the price over time has not reflected a substantial change from the advancement of plans to transition Ethereum to proof-of-stake. Taking the two lines of thought together, The Merge effects on HIVE do not appear adequately anticipated by the market.

Replacement Hash Rate and Revenue Streams

As a general rule, the equipment used to mine Ethereum is different than that for Bitcoin. Ethereum is mined by graphics cards (GPUs) while Bitcoin is mined with application-specific integrated circuits [ASIC]. Before moving to the plans for HIVE's GPUs if The Merge occurs on schedule, a quick disclaimer is needed. HIVE has conducted GPU-based mining since 2017 and nothing in the following discussion is a disparagement of the ROI of their prior GPU investments. Ethereum mining has been highly profitable for HIVE and a core reason for their past success.

HIVE's GPUs consist of two types of cards. There are a number of options and a number of moving variables affecting the first type, which are mostly older Advanced Micro Devices ( AMD ) cards. Without getting too far into the hash rate, difficulty and rewards structure discussion, these cards will likely be reassigned to other GPU minable coins, especially Ethereum Classic ( ETC-USD ). From my layman's knowledge and opinion, it would be optimistic to assume a quarter of these cards' prior revenues could be replaced, and at only a marginal profitability level.

At the end of last year HIVE acquired data center grade cards from Nvidia ( NVDA ). These cards have additional applications in high-performance computing. HIVE is building a new business segment and plans revenue streams from providing services like AI, rendering and molecular modelling. Note that Hut 8 has similarly diversified their business. But uncertainty remains as to the execution, timing, size and margins of this segment's revenues. And a key difference to keep in mind between crypto mining and a data center business is that customer experience components add complexity.

HIVE Valuation

Above I argued that HIVE currently has an average production capacity relative to its market cap, but that following The Merge it will be among the more expensive miners from that perspective. Looking further, it is difficult in general to assign a valuation to the digital asset miners in the current near break-even environment, especially using an earnings stream method. Also, because of the volatility of Bitcoin, retrospective looks do not adequately capture the current or go-forward outlook.

Despite these limitations, consider the following valuation metrics for HIVE:

seekingalpha.com

HIVE's Factor Grades above are relative to the information technology sector.

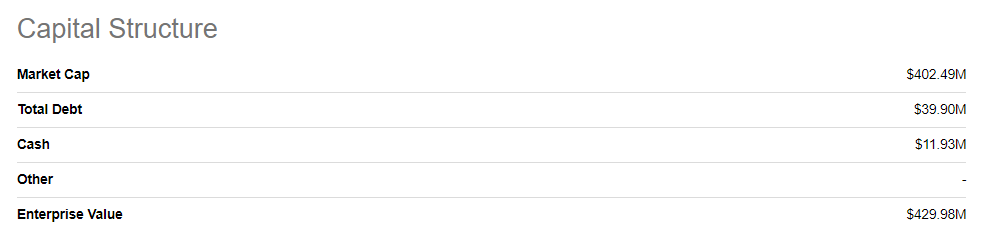

EV Calculation

{kind=link}

Note HIVE's low net debt level. For reference it is similar to Hut 8's and Bitfarms', but contrasts with Marathon Digital's and Core Scientific's ( CORZ ) meaningfully higher levels. Of course, both Marathon Digital and Core Scientific have substantially larger fleets and faster planned growth trajectories.

Not included in the "Cash" entry above are digital currencies valued at $71.4 million at quarter end. For a comparison of digital assets held by the miners, HIVE provided the following graphic in their Q1 F2023 Results Webcast (link above). Note the final column. Again HIVE falls toward the middle and importantly, these assets are relatively large compared to the current market cap.

www.hiveblockchain.com/investors/presentation/

{kind=link}

Moving to the EBITDA side of the discussion, HIVE's adjusted EBITDA is dependent on the underlying price of Bitcoin, the production cost per coin and their general expenses. Before covering these, it is useful to quickly note how HIVE is calculating its adjusted EBITDA in the MDA document . They are adjusting for items such as the revaluation of digital currencies and impairments on equipment, but they are not adjusting for non-cash changes in the value of specific investments, like with Valor Inc. Appropriately, the company also does not correct for foreign exchange gains or losses in its adjusted EBITDA, though in the following discussion this is excluded.

During the second calendar quarter HIVE's operating and maintenance expense including power fees was $17.2 million. 821 Bitcoins and 7675 Ether were mined. Assuming an average price of $32,500 per Bitcoin during the quarter and $44.2 million in combined mining revenues, there were 1368 BTC equivalents produced. This means the average operating costs per coin was $12,573. General expenses per coin divided out to $2,460. So HIVE's adjusted costs and expenses per coin, excluding depreciation, share-based compensation, interest expense, impairments, and foreign exchange losses was about $15,000.

As a simplified and snapshot look, assume Bitcoin prices remain near $20,000 and HIVE grows its hash rate at the same pace the total network hash rate increases. Further assume HIVE replaces half of the lost Ethereum production and thereby produces 1100 Bitcoin equivalents each quarter. Taken together, adjusted EBITDA per quarter would be about $5.5 million. This scenario would yield an expensive EV/EBITDA in the 20x range. But note the price leverage, at $25,000 per bitcoin, this metric cuts in half to a reasonable 10x.

HIVE Rating, Takeaway and Major Risk

I am applying a sell rating to HIVE Blockchain. This is indicative of an expectation that the stock will underperform the market and mining industry. As discussed just above, HIVE is highly leveraged to the price of Bitcoin and will perform strongly with a Bitcoin price recovery. However HIVE may underperform its mining peers as it transitions from Ethereum mining following The Merge. This is especially true as Ethereum currently represents over a third of revenues and profits and is without a quick and easy replacement. As an alternative consider Bitfarms; a comprehensive look at their operations can be found here .

The largest risk to this positioning is lost opportunity in the case of a delay or failure in The Merge that extends the proof-of-work consensus. Depending on how one counts, The Merge has been pushed out six times from about 2017. In the recent MDA, HIVE argued:

The Company believes the broader Ethereum ecosystem derives resilience, decentralization and high security by Ethereum remaining as a proof-of-work system despite wide-ranging pressures on the Ethereum Foundation to transition into PoS, including recent blog posts suggesting a September 2022 Merge date. The Company notes that it cannot ascertain with certainty, when or if Ethereum will transition to Proof of Stake, as there have been numerous historical instances of changes to these targets.

Source: Management's Discussion and Analysis , hiveblockchain.com, 8/16/2022 (link above)

However, for technical reasons it is now much less likely that The Merge will be delayed again. There still remains a hard to quantify chance of major issues with the mainnet, consensus layer or associated blockchains at The Merge. But this too seems unlikely to cause a continuation of proof-of-work consensus for the "official" fork.

HIVE will be expensive relative to its peers from a market cap to hash rate perspective following The Merge on the Ethereum platform.

My new marketplace service is coming soon. Complete Crypto Analytics is launching in the near future and will have an in-depth, dedicated Bitcoin miner comparison feature. Please keep reading my articles here for updates so you can reserve your spot as a Legacy Discount Member. There will be a generous introductory price for early subscribers. Thank you for following my work.

For further details see:

HIVE Blockchain: Market Mispricing Ethereum Merge