MLKN - HNI And Kimball Tie-Up May Be MillerKnoll 2.0

2023-05-31 10:43:41 ET

Summary

- HNI Corporation's acquisition of Kimball raises concerns due to the potential downturn in office furniture sales and increased debt load.

- Weakness in HNI's Residential Building Products segment could be a structural issue, not just cyclical, as gas fireplaces face health and green energy concerns.

- HNI's increased leverage and potential pressure from tax loss selling later this year may lead to further downside for the company's shares.

One commercial furniture manufacturer levers up to buy another. Where have I seen this before?

MLKN Stock Price (yCharts (author annotated))

HNI Corporation ( HNI ) is doing the same by purchasing Kimball ( KBAL ) in a $485 million deal (valuation at the time of the announcement; slightly less now.) While the deal is not starting at the lofty valuation the MillerKnoll ( MLKN ) deal was, there are a lot of question marks, including paying a massive premium and loading up on debt at a time office furniture sales may enter a protracted downturn.

My Views on the Business Combination

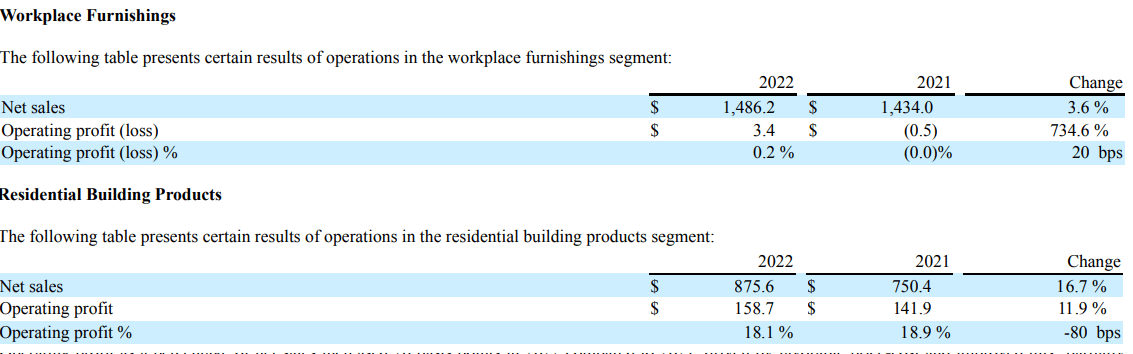

HNI Corporation has two major divisions: Workplace Furnishings and Residential Building products. In 2022, nearly all of HNI's profits came from Residential Building Products, where HNI is projecting revenue to decline in the "high 20's to low 30's range" this year.

{kind=link}

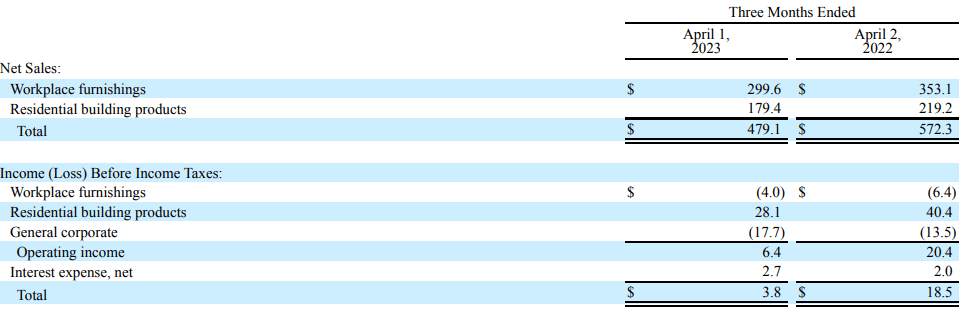

The weakness in Workplace Furnishings hasn't changed into 2023 with another loss (although this business does have some seasonality, so typically H2 is stronger H1.)

{kind=link}

Kimball's recent results are also unimpressive to me, especially considering that they've run down their backlog, which has declined from $180 million just two quarters ago to $134.5 million now.

{kind=link}

Ultimately, my very high level view is one that is bearish on Office Furniture suppliers in general. The industry had some help from COVID re-openings with office reconfigurations, while supply chain issues partially limited supply across the industry. These positive impacts are largely wrapping up, which I believe is going to result in a far more competitive industry going forward, including from used office furniture. So far, most of these companies have held onto their pricing and in HNI's case, increased price in March. I doubt this pricing power will continue for much longer.

Residential Building Products is HNI's other division where they derived nearly all their profit last year. The name is a bit of a misnomer; HNI describes itself as a "a leading manufacturer and marketer of hearth products." For those that don't know what a "hearth" product is, it's basically a fireplace. Here's what management says for an outlook on the last conference call

Our Residential Building Products segment is prepared for a period of weaker demand. Consistent with our previously discussed expectations, weakening macroeconomic conditions and softer housing-related demand negatively impacted Residential Building Products during the first quarter. However, productivity savings, cost reduction actions and continued price cost improvement offset nearly half of the volume-related pressure. As a result, segment operating margin remained in the mid-teens. This was the 11th straight quarter with an operating margin in excess of 15%. Not unexpectedly, segment orders softened in the quarter.

...

We expect segment revenue to decline at a year-over-year rate in the high 20% to low 30% range. This decline reflects both a return to normal seasonality and weakening new construction and remodel/retrofit demand.

It makes sense that Residential Building Products would correlate with new home construction, although new home construction has been fairly resilient in the face of much higher interest rates.

New Residential Construction, May 2023 (US Census, HUD)

In addition to the cyclical factors, I think there's something else that may be driving sales lower in this segment: the recent trend in banning gas stoves . While I personally find the claims that gas stoves and fireplaces are suddenly bad for your health dubious, if I were a home builder or buyer, I may have second thoughts about including a gas fireplace because of this.

Weakness is this segment could be a structural issue, and not just a cyclical.

Increased leverage from the deal

HNI's current debt structure looks like this:

HNI Debt (HNI Q1-23 10-Q)

Not too troublesome, but they're now going to add another $330 million of floating rate debt to this, bringing yearly cash interest expense up to ~$35 million from around ~$10 million now, to go along with a 10% dilution in the common shares.

Why shares could drop in the short term (and probably stay there)

The HNI buyout of Kimball is structured so that Kimball shareholders receive $9 and 0.13 shares of HNI for each share they own. With Kimball's share price around $12.40, the vast majority of value of Kimball's shares are being returned in cash.

I find it much more likely that these existing shareholders just sell their HNI stub, rather than reinvest the cash back in HNI stock.

Kimball was an office furniture company that was mostly unlevered; the new company is a moderately levered office furniture company and fireplace supplier. For investors that want office furniture exposure, levered MillerKnoll is available at 8x forward earnings while Steelcase ( SCS ) is available at 10x, versus the projected 14x earnings for HNI (note: I don't trust any of these estimates, but they are what they are right now.)

From there, considering the price action of HNI, without some drastic turnaround in the business that I believe is unlikely, HNI could feel further pressure from tax loss selling later this year.

Conclusion

When I review the Herman Miller/Knoll tie-up, these projections stand out

- Combined, both will have pro forma annual revenue of ~$3.6B and pro forma adj. EBITDA of ~$552M; includes the expected $100M of run-rate cost synergies (within two years of closing) leading to adj. EBITDA margins of ~16%.

- Transaction is expected to be accretive to Herman Miller's adj. cash earnings per share in the first year post transaction closure.

At the time, sales were booming, and they exceeded revenue targets. But EBITDA and EPS badly missed anyhow, and the shares have lost 70% of their value since.

I could see the same happening with HNI, especially considering they've been focused on streamlining their cost structure already and are already benefitting from lower input costs, but are projecting sales declines, rather than increases.

Ultimately, I see this as a company that's levering up to double down on office furniture at a really poor time and is fully exposed to any weakening in the economy. Health and green energy concerns around HNI's hearth business represent another potential risk to monitor.

I believe HNI represents a poor risk/reward and shares have further downside from here.

For further details see:

HNI And Kimball Tie-Up May Be MillerKnoll 2.0